%201.avif)

.png)

.png)

CFO Services for Growing Businesses

CFO services for growing businesses give companies the financial leadership they need to scale without the cost of a full-time hire. These services cover cash flow forecasting, budgeting, financial reporting, tax strategy, and decision support, all delivered by an experienced finance executive on a part-time or fractional basis. For most growing companies, this is the fastest way to get senior-level financial clarity without putting six figures on the payroll.

In this article, we cover what CFO services include, the four core roles a CFO plays, what the service typically costs, when your business needs one, how a CFO supports startups and scaling companies, and how this role compares to other financial professionals like CPAs and VPs of finance.

What Are CFO Services for Growing Businesses

CFO services for growing businesses are professional financial leadership engagements that give companies access to chief financial officer expertise on a part-time, fractional, or virtual basis. Instead of hiring a full-time CFO at a six-figure salary, you contract with a senior finance professional who handles your strategy, forecasting, and reporting on the hours your business actually needs.

The model has been growing fast. According to Business Research Insights, the global virtual CFO market was valued at roughly $3.91 billion in 2024 and is projected to reach $8.17 billion by 2032, growing at a compound annual growth rate of 9.6%. A separate report from Fractionus noted that demand for fractional CFOs, CMOs, and CTOs grew 68% from 2023 to 2024. Growing businesses are turning to this model because it delivers executive-level guidance at a price point they can actually afford.

The work itself is the same as what an in-house CFO does. You get help with rolling cash flow forecasts, monthly financial reviews, budget vs. actual analysis, fundraising preparation, investor reporting, tax timing, and big-picture financial decisions. The difference is the engagement structure. We work with growing businesses out of our Miami office on a flexible basis, scaling our hours up during fundraising or year-end planning and scaling back during quieter periods. That flexibility is one of the main reasons our virtual CFO clients stay engaged for years rather than burning through a full-time hire.

What Do CFO Services Include

CFO services include cash flow forecasting, financial reporting, budgeting and planning, tax strategy oversight, fundraising support, KPI tracking, risk management, and strategic decision support. The exact mix depends on your stage and goals, but every engagement starts with getting clear visibility into your numbers.

According to a Blackline survey of finance professionals, nearly 49% worry about the reliability of their cash flow data. That gap is exactly what CFO services close. A 2025 KPMG report found that proactively managing working capital through aligned metrics, dedicated leadership, and transparent accountability is a key driver of return on invested capital. In plain language, businesses that put a senior finance professional in charge of working capital make more money on every dollar they invest.

Cash Flow Forecasting and Management

Cash flow forecasting is the single most important service a CFO delivers. The standard tool is a rolling 13-week cash flow forecast that gets updated every Monday. This shows you exactly what cash is coming in, what is going out, and where any gaps will appear over the next three months. According to Vayana research, only 2% of CFOs report full confidence in their cash flow visibility, which means most companies are flying blind on the one number that keeps them alive. A 2025 OnDeck and Ocrolus survey found cash flow ranked as the second biggest concern for small business owners at 29%, just behind inflation at 31%.

A CFO also tightens collections, manages vendor payment timing, and builds cash reserves. Gitnux research found that 61% of small businesses report cash flow issues caused by late payments, and 93% of all companies experience at least some late payments from customers. We tackle this through clear credit policies, automated invoice reminders, and disciplined follow-up that pulls the average payment timeline down without damaging client relationships. This is the same kind of cash flow discipline we build for every growing business we work with.

Financial Reporting and Analysis

A CFO produces clean, reliable monthly reports that include the income statement, balance sheet, and cash flow statement. These reports are then translated into plain language so the business owner can act on them. According to a 2025 PwC CFO Pulse survey, 70% of CFOs say improving the quality of management reporting is a top priority, because raw financial data on its own does not drive decisions.

Beyond the standard three statements, a CFO sets up dashboards that track KPIs like gross margin, operating margin, customer acquisition cost, lifetime value, and Days Sales Outstanding. According to the Corporate Finance Institute, a healthy DSO sits below 45 days. If your number is climbing past that, a CFO will pinpoint why and build a plan to fix it. Our financial statements work plugs directly into this kind of analysis.

Tax Strategy and Compliance Oversight

Tax strategy is one of the most underused ways a CFO protects cash. Overpaying taxes, missing deductions, or paying penalties drains cash that could have funded payroll, hiring, or growth. A CFO works alongside your CPA to time income and expenses for the lowest legal tax bill, take advantage of credits like the R&D credit, and keep estimated quarterly payments accurate so the IRS does not surprise you in April. Proactive tax planning often pays for the entire CFO engagement on its own.

Strategic Planning and Decision Support

A CFO helps you make the big calls. Should you hire that new sales rep? Open a second location? Raise capital or take on debt? Acquire a competitor? Every one of those decisions has a financial impact that needs to be modeled before you commit. A CFO builds scenario models that show the cash and profit impact of each option. McKinsey research found that companies engaged in proactive scenario planning are 33% more likely to recover financially within six months after a disruption. Our strategic planning work centers around exactly this kind of modeling.

What Are the 4 Roles of a CFO

The 4 roles of a CFO are steward, operator, strategist, and catalyst. This framework comes from Deloitte and is used by finance leaders across every industry to describe what a modern CFO actually does day to day.

The steward role is about protecting the company. The CFO safeguards assets, manages risk, closes the books accurately, and keeps the company compliant with regulations. This is the foundation. Without a strong steward, none of the other roles matter because the underlying numbers cannot be trusted.

The operator role is about running an efficient finance function. The CFO oversees the day-to-day operations of accounting, treasury, payables, receivables, and reporting. The goal is to get accurate financial information out fast and at a reasonable cost. According to a 2025 Gartner CFO survey, 82% of finance leaders say accelerating the close process is a key operational goal.

The strategist role is about shaping the direction of the company. A CFO brings financial discipline to long-term planning, evaluates growth opportunities, and helps decide where to invest capital. According to a Deloitte CFO Signals survey, 64% of CFOs spend more time on strategic work today than they did five years ago.

The catalyst role is about driving change. A CFO instills a financial mindset across the organization, partners with other leaders to push performance improvements, and champions initiatives that move the company forward. This is the role that separates a transactional finance leader from a true business partner.

Is a Fractional CFO Worth It

Yes, a fractional CFO is worth it for most growing businesses between $1 million and $50 million in annual revenue. The return on investment usually shows up within the first three to six months through better cash flow timing, lower tax liability, improved margins, and smarter spending decisions.

According to a pricing survey by Eagle Rock CFO, most growing companies see a 3 to 10 times return on their fractional CFO investment. The savings typically come from three places. First, fewer expensive mistakes because someone with experience is reviewing the big decisions before they happen. Second, more disciplined spending because there is now a budget and someone watching it. Third, faster collections and smarter payment timing that free up working capital.

The cost difference compared to a full-time hire is significant. According to data from Cowen Partners and Salary.com, total compensation for a full-time CFO at a growing company ranges from $300,000 to $500,000 per year once you add bonuses, benefits, and equity. A fractional CFO engagement typically runs $36,000 to $120,000 per year for the same level of strategic guidance. That is a 70 to 85% cost reduction without giving up the expertise.

The model works because most growing businesses do not need a CFO 40 hours a week. They need someone for 10 to 30 hours a month who knows what to look for, what questions to ask, and what to do about the answers. A fractional engagement gives you exactly that, with the flexibility to scale up during fundraising or scale down during quieter periods.

How Much Do CFO Services Cost

CFO services cost between $2,000 and $15,000 per month for fractional engagements, depending on the scope of work, the size of the business, and the experience level of the CFO. According to a 2025 industry pricing survey from Eagle Rock CFO, most growing companies pay between $4,000 and $8,000 per month for part-time CFO support.

Pricing breaks down by company stage. Early-stage startups using 8 to 15 hours per month typically pay $1,400 to $4,000 monthly, according to data from Graphite Financial. Growth-stage businesses using 20 to 40 hours per month usually pay $5,000 to $12,000. Mid-market companies with more complex needs can pay $10,000 to $20,000 monthly for senior-level fractional engagements.

Compare that to the cost of a full-time hire. According to multiple 2025 salary surveys, the median base salary for a CFO in the United States runs $300,000 to $437,000. Add a 15 to 25% bonus, equity of 0.5 to 2%, and benefits at roughly 20 to 30% of base salary, and the total package can exceed $500,000 per year. According to K38 Consulting, businesses that switch from full-time to fractional save 60 to 80% on their finance leadership costs.

What Is the Hourly Rate for a CFO

The hourly rate for a CFO ranges from $175 to $450 per hour in 2025 for fractional or virtual work, according to multiple industry pricing surveys. Most experienced fractional CFOs charge between $200 and $350 per hour, with rates climbing higher for specialized industry expertise or work tied to major events like fundraising or acquisitions.

According to research published by Bennett Financials, entry-level fractional CFOs charge $150 to $250 per hour, mid-level CFOs charge $250 to $400 per hour, and senior CFOs with deep experience or industry specialization charge $400 to $600 per hour. The hourly rate alone does not tell the full story. The total monthly cost depends on how many hours your business actually needs, which is usually less than founders expect.

For comparison, the equivalent hourly rate of a full-time CFO is roughly $210 to $250 per hour based on a $437,000 median annual salary and a standard 2,080 work-hour year, according to Salary.com data. That number does not include the cost of benefits, equity, payroll taxes, or recruiting fees, which can add another 30 to 40% on top.

Does a Small Business Need a CFO

A small business needs a CFO when financial complexity outgrows what a bookkeeper or owner can handle alone. This usually happens when revenue crosses $1 million annually, when the company starts hiring employees, when outside funding enters the picture, or when tax obligations become harder to manage.

The data backs up the value. According to the U.S. Bank study widely cited in small business research, 82% of small businesses that fail do so because of poor cash flow management. That single statistic explains why bringing in CFO-level expertise pays off so quickly. A CFO is trained to spot cash flow problems weeks or months before they hit, which gives the business time to adjust spending, accelerate collections, or arrange short-term financing.

Growing businesses also benefit from CFO-level business consulting on big decisions. When a small business is making a major hire, signing a long-term lease, taking on debt, or expanding into a new market, the financial impact of getting the decision wrong is large. A CFO models those decisions before they happen so the owner can choose with confidence. According to the Federal Reserve's 2025 Small Business Credit Survey, only 46% of small employer firms were profitable in 2024, with another 35% breaking even and 19% operating at a loss. That tells you most small businesses are running too tight to absorb expensive financial mistakes.

How to Find a CFO for a Startup

To find a CFO for a startup, focus on the fractional or virtual model first, look for someone with direct startup experience, and prioritize industry fit over name-brand resumes. Most startups under Series B do not need a full-time CFO and often cannot afford one, so the fractional path is almost always the right starting point.

Look for three things specifically. First, real startup experience, meaning the person has worked with companies at your stage and understands the financial patterns of early-stage growth. Second, industry knowledge that fits your business model. A SaaS-focused CFO will serve a software startup better than a generalist, just like a restaurant-experienced CFO will serve a food business better. Third, comfort with modern cloud-based accounting tools like QuickBooks Online, Xero, NetSuite, or whatever stack your company uses. According to Salary.com data, 80% of startups operate without a CFO in the early stages, which means founders often make critical financial decisions without senior guidance.

You can find fractional CFOs through CPA firms that offer the service, through specialized fractional executive networks, or through referrals from your bank, attorney, or accelerator. Vet candidates by asking for case studies, references from companies at your stage, and a clear scope of what they will and will not handle each month. Strong startup advisory support during the first year of business often shapes whether the company makes it to year five.

Why Do 90% of Startups Fail

Approximately 90% of startups fail because of a combination of poor product-market fit, running out of cash, team problems, and financial mismanagement. According to CB Insights, 42% of startups fail because they built a product nobody wanted to pay for, and 29% fail because they simply ran out of money. Both of those issues connect back to financial planning and discipline.

Cash runway is the most measurable risk. Sequoia Capital recommends maintaining 18 to 24 months of cash runway in the current funding environment, but data from Carta shows the median startup operates with closer to 12 months. When a startup runs out of cash before reaching its next milestone, the company either dies or has to raise money on terms that hurt the founders. A CFO prevents that by building forecasts that show the runway clearly and adjusting spending months in advance when the math starts looking tight. Strong business formation decisions at the start (entity type, ownership structure, equity setup) also play a role in whether a startup is positioned to attract capital later.

According to Forbes, 70% of startups with poor budgeting fail. The U.S. Bureau of Labor Statistics tracks that about 20% of new businesses fail within the first year, climbing to roughly 50% by year five and 65% by year ten. These are the numbers that make CFO-level financial guidance so valuable in the early stages. The startups that survive are usually the ones that brought in senior financial thinking before the problems arrived, not after.

Is a CFO Higher Than a CPA

A CFO is generally higher than a CPA in terms of seniority within a company, though the two roles serve different functions. A CPA, or Certified Public Accountant, is a licensed professional who specializes in accounting, tax, and audit work. A CFO is an executive-level position responsible for the entire financial direction of a company. Many CFOs hold the CPA license, but not all CPAs are CFOs.

The roles also differ in focus. A CPA looks backward, recording transactions accurately, preparing financial statements, and filing tax returns. A CFO looks forward, building forecasts, modeling scenarios, and guiding decisions. Both roles matter, and growing businesses often need both at the same time. According to a 2025 AICPA Trends Report, 75% of CFOs have an accounting background, while only 30% are actively licensed CPAs.

At our firm, we combine both functions because most growing businesses get more value from one team that handles tax, accounting, and CFO-level strategy together. That coordination avoids the gaps that happen when the bookkeeper, the tax preparer, and the CFO all work separately and never compare notes.

How CFO Services Support Scaling Companies

CFO services support scaling companies by adding financial discipline at the exact stage when growth puts the most pressure on cash, processes, and decision-making. Revenue going up sounds like a good problem, but it usually means expenses are also going up, often before the new revenue actually shows up in the bank account. That timing gap is where most scaling companies stumble.

A CFO closes the gap in four ways. They build detailed cash flow projections that account for the timing difference between spending and earning. They set spending limits tied to actual cash on hand rather than projected revenue. They negotiate better payment terms with customers and vendors to free up working capital. And they monitor unit economics so the business is not growing into unprofitable territory.

According to the 2025 Small Business Credit Survey from the Federal Reserve, 48% of small employer firms cite weak sales as a top financial challenge, up from 44% the prior year. Even companies that are scaling face revenue softness in some periods. A CFO keeps the business from overextending during those slower stretches. Our CFO services are built specifically for this kind of growth-stage support.

CFO Services vs Other Financial Support Options

Growing businesses often try to decide between hiring a full-time CFO, contracting a fractional or virtual CFO, leaning on their CPA, or upgrading their bookkeeper. Each option fits a different stage and budget. The table below shows how these options compare on the key factors that matter to a growing business.

OptionTypical Annual CostStrategic ValueBest ForFull-Time CFO$300,000 to $500,000+Very high, daily presenceCompanies over $20M revenueFractional or Virtual CFO$36,000 to $120,000High, strategic focusGrowing companies $1M to $50MCPA or Accounting Firm$5,000 to $30,000Moderate, tax and compliance focusEstablished small businessesBookkeeper$3,000 to $12,000Low, data entry and recordsVery early-stage businesses

Sources: Salary.com 2025 CFO salary data, Cowen Partners Executive Search 2025 compensation report, Eagle Rock CFO 2025 pricing survey, K38 Consulting fractional CFO pricing guide 2025, Graphite Financial 2025 hourly rate guide.

Signs Your Growing Business Needs CFO Services Now

The clearest signs your growing business needs CFO services are revenue growth that is not translating to cash in the bank, a financial picture that feels foggy or out of date, upcoming fundraising or lending conversations, surprise tax bills, and major decisions that have to be made without solid numbers behind them.

Specific trigger points we see often include monthly revenue exceeding $100,000 with no clear visibility into profit by service or product line, plans to hire two or more new employees in the next 90 days, an upcoming bank loan application or investor pitch, a missed tax deadline or unexpected IRS notice, a contract or partnership opportunity that needs financial modeling before signing, and a sense that the books are accurate but the numbers do not actually answer the questions you have.

According to a CBIZ small business survey, 67% of small business owners say they want better financial guidance but feel they cannot afford a full-time hire. Fractional and virtual models exist precisely to solve that. Founders running early-stage companies often find that a startup CFO guide gives them the same financial discipline larger companies pay full-time CFOs for. Here in Miami, we work with growing businesses that hit one or more of these trigger points every month and are looking for senior financial leadership without the full-time price tag.

What CFO Services Look Like in Practice

CFO services in practice are organized around a regular monthly rhythm with specific deliverables and checkpoints. A typical engagement includes weekly cash flow updates, monthly financial close reviews, quarterly strategy meetings, and on-call support for one-off decisions that come up between scheduled touchpoints.

In a typical month, the CFO reviews the prior month's financials within five business days of close, holds a 60 to 90 minute meeting with the business owner to walk through the results, updates the rolling 13-week cash flow forecast, flags any KPI trends that need attention, and prepares for any time-sensitive decisions on the horizon. Weekly cash flow check-ins happen by email or short calls, and quarterly meetings dive deeper into long-term strategy, hiring plans, and capital decisions.

The deliverables stay the same across most engagements: a clean monthly financial package, a 13-week cash forecast, a KPI dashboard, an updated annual budget with variance tracking, and a strategic memo or scenario model for any major decision in flight. According to a 2025 Deloitte CFO Signals report, 78% of finance leaders report that scenario modeling has become a core part of their monthly work, up from 52% in 2021.

Frequently Asked Questions

Is a CFO Higher Than a VP

A CFO is higher than a VP in most company structures. The CFO sits on the executive leadership team and reports directly to the CEO, while VPs typically report to the CFO or another C-suite executive. The CFO has authority over all financial functions including treasury, accounting, FP&A, and investor relations, while a VP of Finance usually focuses on a narrower slice of those responsibilities.

How Many Hours a Day Does a CFO Work

A full-time CFO typically works 9 to 12 hours a day, according to executive workload surveys. Fractional and virtual CFOs work different schedules depending on the client load, often putting in 5 to 8 hours per day spread across multiple companies. According to a 2025 Korn Ferry executive survey, 62% of CFOs report working more than 50 hours per week, and 38% report working more than 60.

What Keeps a CFO Up at Night

What keeps a CFO up at night is cash flow uncertainty, talent retention, regulatory risk, and the accuracy of forecasts. According to a 2025 Protiviti CFO survey, 71% of CFOs list cash flow management as a top concern, followed by economic uncertainty at 64% and cybersecurity risk at 58%. The single biggest worry is usually whether the forecast in front of them is actually right, because everything else depends on it.

What Is a CFO Not Responsible For

A CFO is not responsible for daily bookkeeping, sales execution, product development, customer service, or marketing strategy. The CFO oversees the financial impact of all of those functions but does not run them. Bookkeeping is handled by accountants and bookkeepers. Sales is owned by a VP of Sales or CRO. Product, marketing, and operations each have their own leaders, and the CFO partners with them rather than directing them.

How Much Should I Pay My CFO

How much you should pay your CFO depends on whether you hire full-time or fractional. For a full-time CFO at a growing company, expect $250,000 to $500,000 in total compensation, according to 2025 Cowen Partners salary data. For a fractional CFO, expect $3,000 to $10,000 per month for 10 to 30 hours of monthly support, according to industry pricing surveys. The right number depends on your revenue stage, industry, and the complexity of the work.

What Is the Average CFO Bonus

The average CFO bonus runs between 25% and 50% of base salary, according to 2025 compensation surveys from Cowen Partners and Heidrick & Struggles. At larger public companies, total cash bonuses for CFOs averaged $367,000 in 2024, according to Spencer Stuart data. At growing private companies, bonuses are typically smaller in absolute dollars but represent a similar percentage of base pay, often tied to specific financial targets like EBITDA, cash flow, or revenue growth.

What Are the Top CFO Responsibilities

The top CFO responsibilities are cash flow management, financial planning and analysis, financial reporting, tax strategy, risk management, capital allocation, investor relations, and supporting the CEO on major strategic decisions. According to a 2025 McKinsey CFO Pulse report, today's CFOs spend 45% of their time on strategic work, 30% on operational finance, and 25% on stewardship and compliance, a major shift from a decade ago when stewardship dominated.

The Takeaway

CFO services for growing businesses give you the financial leadership you need to scale without committing to a full-time hire. From cash flow forecasting and KPI tracking to fundraising preparation and tax strategy, a fractional or virtual CFO brings the same expertise as an in-house executive at a fraction of the cost. The data is clear. Businesses that bring in senior financial guidance earlier survive longer, raise more capital, and grow with more confidence.

If your company is scaling, planning a fundraise, or just trying to get better visibility into the numbers, the right time to bring in CFO-level support is usually sooner than you think. At NR CPAs & Business Advisors, we work with growing businesses across the country to bring clarity, structure, and strategy to their finances. Reach out to our team at (954) 231-6613 to start the conversation.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

IRS Notices Explained: What Each Letter Means And What To Do?

What Is An IRS Notice

An IRS notice is official correspondence that the Internal Revenue Service sends through the U.S. mail to inform you about a specific issue with your federal tax return or account. According to the IRS, the agency sends notices for reasons ranging from a simple math correction on your return to an unpaid balance or a request for additional documentation. Receiving a notice does not necessarily mean you made a mistake or owe additional tax, and many notices can be resolved by following the instructions printed on the document.

The IRS draws a practical distinction between two categories of mail. A notice is typically system-generated and addresses a specific account issue such as a balance due, a refund adjustment, or a processing change. A letter, by contrast, often comes from an individual IRS employee or department and may request information, confirm an action, or relate to an ongoing examination. Both arrive by U.S. mail, and both include a notice or letter number in the upper right corner of the first page that identifies exactly what the correspondence is about.

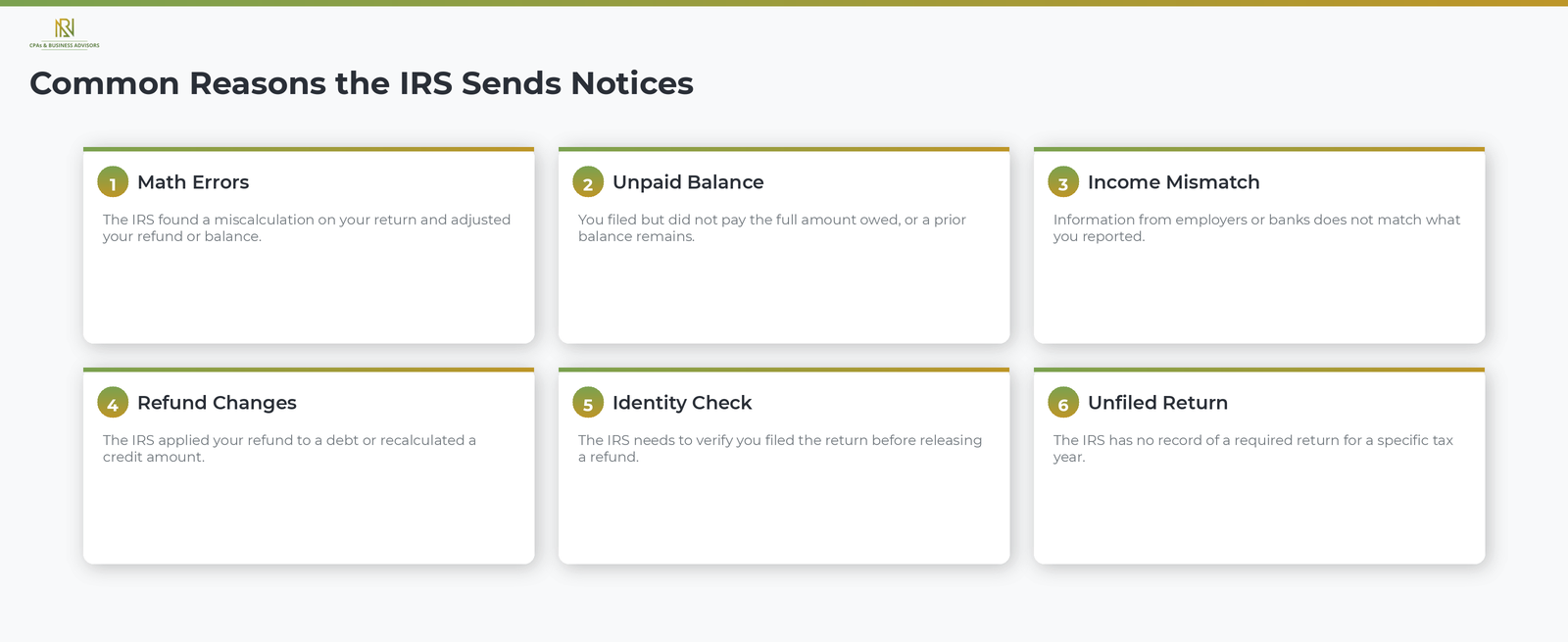

Common Reasons The IRS Sends Notices

The IRS sends notices most often because of a discrepancy on your tax return, an unpaid balance, or a change the agency made to your account. According to the IRS, the most frequent triggers include the following situations.

- Math errors or miscalculations on your return. The IRS caught an arithmetic mistake and adjusted your refund or balance accordingly.

- An unpaid tax balance. You filed a return but did not pay the full amount owed, or a prior balance remains on your account.

- Unreported or underreported income. Information the IRS received from employers, banks, or other third parties does not match what you reported on your return.

- Refund changes. The IRS applied your refund to a prior debt or adjusted the amount because of a credit recalculation.

- Identity verification. The IRS needs to confirm that you filed the return before releasing a refund.

- Unfiled returns. The IRS has no record of a required return for a specific tax year.

Not every IRS notice signals a problem. Some correspondence simply confirms a change you requested, acknowledges information you submitted, or notifies you that the IRS closed its review of your account.

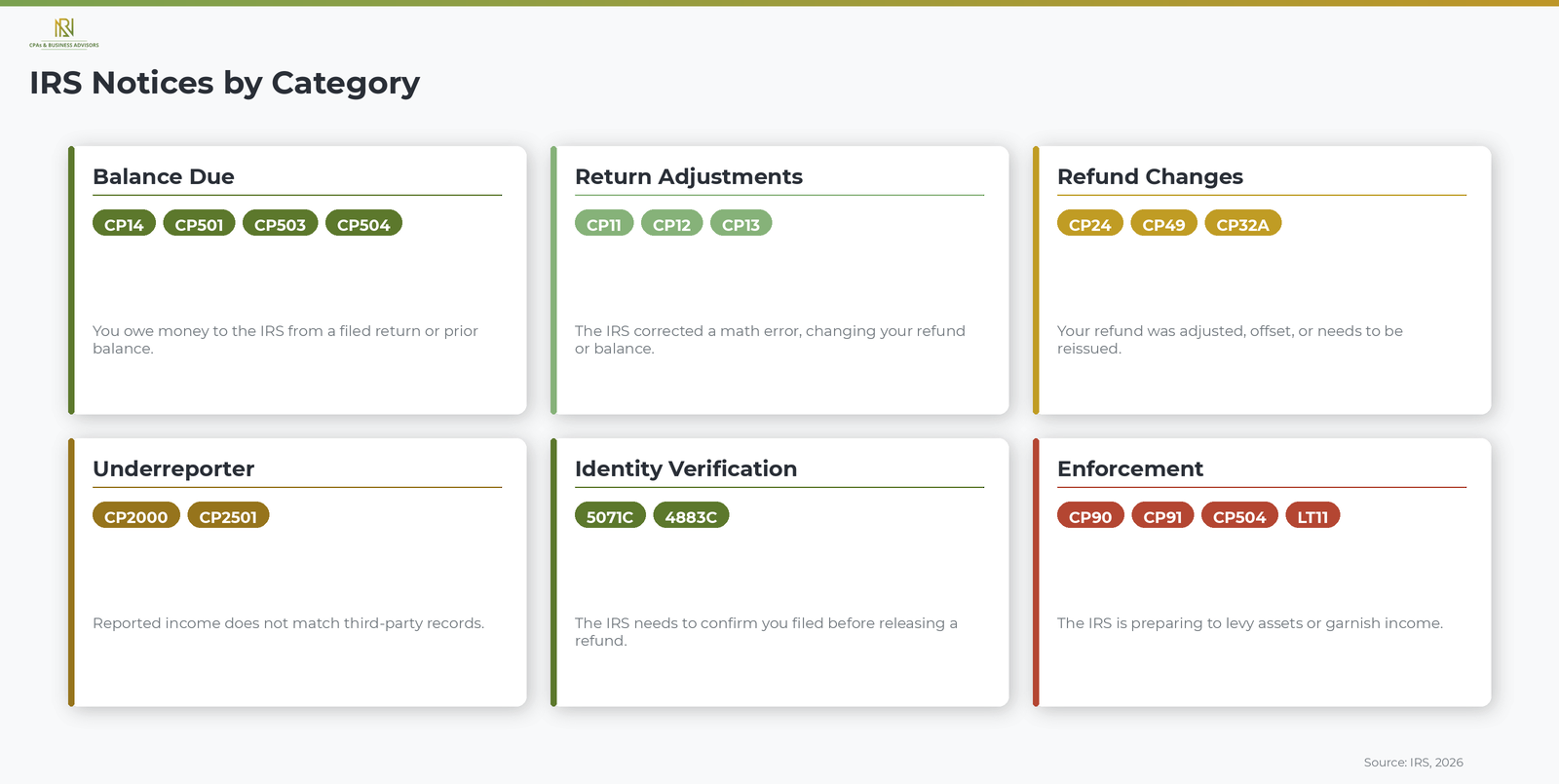

Most Common Types Of IRS Notices

IRS notices fall into several broad categories based on why the agency issued them. Understanding which category your notice belongs to helps you assess its urgency and determine what kind of response it requires. The notice number, printed in the upper right corner of the first page, identifies the specific type.

Balance Due Notices

Balance due notices inform you that you owe money to the IRS. The most common is the CP14, which is the initial notice the agency sends when a filed return shows an unpaid amount. If you received a CP14 notice, our complete guide to this balance due letter explains the specific charges, deadlines, and response options. Subsequent reminders in the collection sequence include the CP501, CP503, and CP504, each carrying increased urgency.

Return Adjustment Notices

The IRS sends adjustment notices when it corrects an error on your return. A CP11 means the correction resulted in a balance you now owe. A CP12 means the correction resulted in a larger refund or a change to the amount you expected. A CP13 means the correction left your balance at zero with no additional amount owed and no refund due. According to the IRS, each of these notices explains exactly what changed and how the recalculated amount was determined.

Refund-Related Notices

These notices address changes to the amount or timing of your refund. A CP24 notifies you that the IRS found a difference between your estimated tax payments and the amount posted to your account, resulting in a potential overpayment credit. A CP49 notifies you that the IRS applied all or part of your refund to a prior tax debt. A CP32A asks you to contact the IRS so the agency can reissue a refund check.

Underreporter Notices

An underreporter notice means the income or payment information the IRS received from third parties does not match what you reported. The CP2000 is the primary notice in this category and one of the most frequently issued IRS letters. According to the IRS, a CP2000 is not a bill but a proposed adjustment that explains how the recalculated tax was determined. Taxpayers who receive a CP2000 notice can review our full guide to this underreporter letter for response steps and dispute options.

Identity Verification Notices

Identity verification notices ask you to confirm that you filed the return in question before the IRS will release a refund. Common examples include Letter 5071C and Letter 4883C. According to the IRS, these letters are part of the agency's efforts to prevent tax-related identity theft and typically require you to verify your identity online at IRS.gov or by calling the toll-free number printed on the letter.

Enforcement And Collection Notices

Enforcement notices signal that the IRS is preparing to take collection action against your assets. A CP504 warns that the IRS intends to levy your state tax refund. A CP90 or LT11 is a final notice of intent to levy bank accounts, wages, and other property, and it grants you the right to request a Collection Due Process hearing within 30 days. Certain enforcement notices, such as the CP90, may arrive as certified mail requiring your signature. A CP91 warns that the IRS intends to levy up to 15 percent of your Social Security benefits.

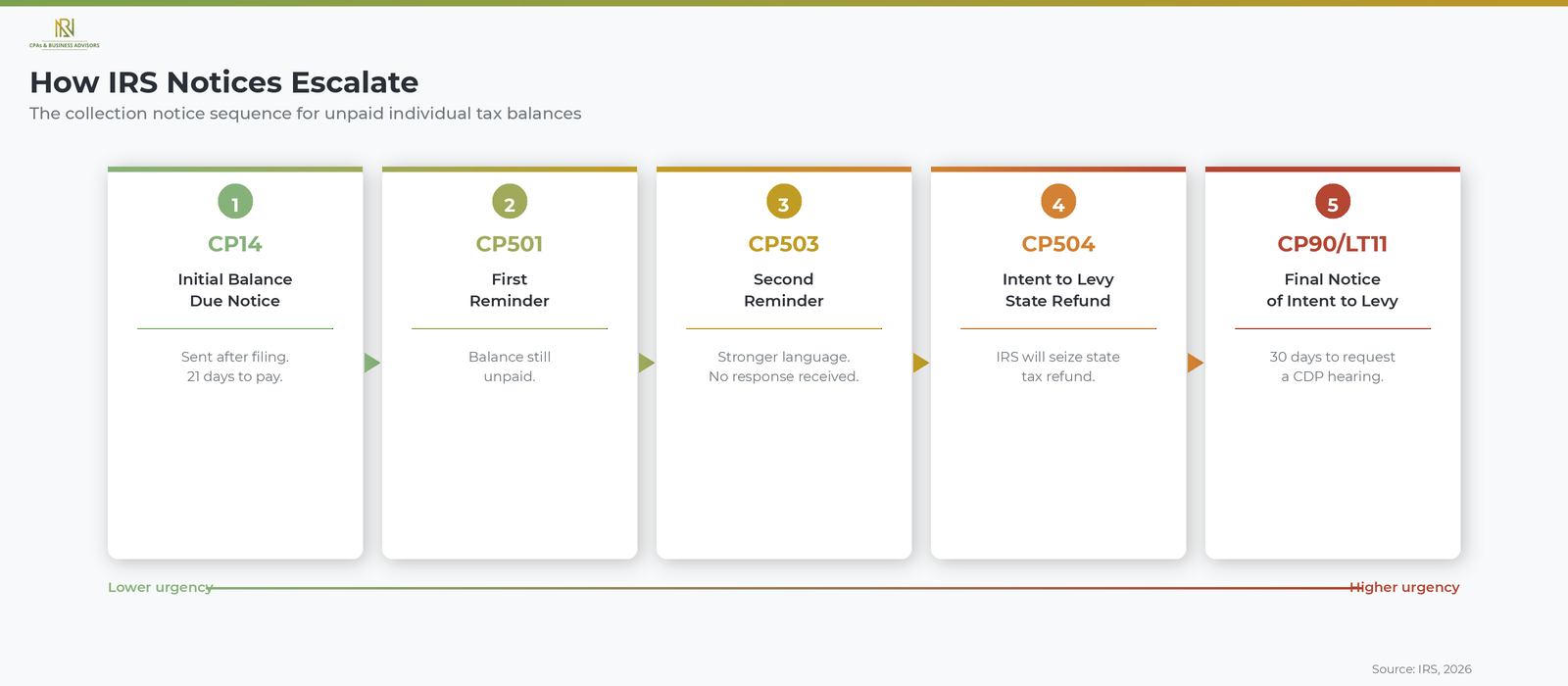

How IRS Notices Escalate From Reminder To Enforcement

IRS collection notices follow a specific sequence that grows more urgent at each stage, and each notice includes a deadline that starts the clock on the next escalation step. According to the IRS, the standard progression for an unpaid individual tax balance works as follows.

- CP14: the initial balance due notice, sent shortly after you file a return with an unpaid amount.

- CP501: a first reminder that your balance remains unpaid.

- CP503: a second reminder with stronger language, noting that the IRS still has not received your payment or a response.

- CP504: a notice of intent to levy your state income tax refund if you do not pay or contact the IRS to arrange a resolution.

- CP90 or LT11: the final notice of intent to levy your wages, bank accounts, and other assets. This notice also informs you of your right to a Collection Due Process hearing, which you must request within 30 days.

Responding at any point in this sequence can slow or stop the escalation. Taxpayers who cannot pay the full amount may qualify for a structured IRS payment plan or installment agreement. Our guide to these structured repayment options covers the application process, payment thresholds, and how interest is calculated on the remaining balance. Those facing significant financial hardship may also qualify for the IRS Fresh Start program, which provides expanded installment terms and penalty relief for eligible individuals and businesses.

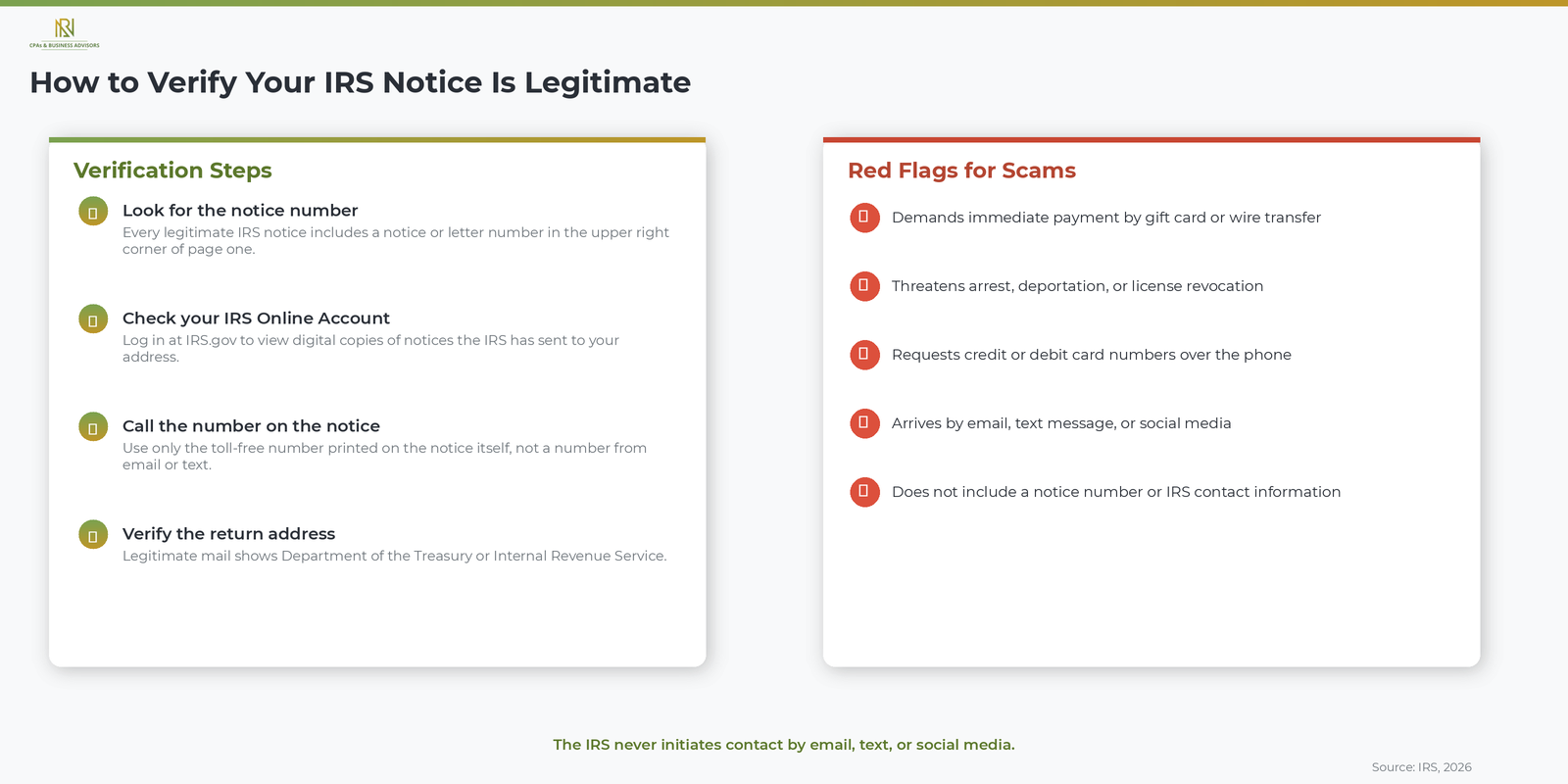

How To Verify Your IRS Notice Is Legitimate

A legitimate IRS notice arrives by U.S. mail, references a specific tax year and notice number, and never asks you to click a link or provide personal information through email or text. According to the IRS, the agency does not initiate contact with taxpayers by email, text message, or social media to request personal or financial information. Any communication that does so is a scam.

To confirm that a notice you received is genuine, take the following steps.

- Look for the notice or letter number in the upper right corner of the first page. Every legitimate IRS notice includes one.

- Log in to your IRS Online Account at IRS.gov. According to the IRS, many notices are viewable in your online account, which allows you to verify the correspondence directly against what the agency has on file.

- Call the toll-free number printed on the notice itself, not a number from an email, a text, or a website you found through a search.

- Check the return address. Legitimate IRS mail comes from a recognized IRS processing center, and the envelope typically includes "Department of the Treasury" or "Internal Revenue Service" in the return address.

According to the IRS, common red flags for fraudulent correspondence include demands for immediate payment by gift card or wire transfer, threats of arrest or deportation, and requests for credit or debit card numbers over the phone.

What To Do When You Receive An IRS Notice

Read the notice carefully, compare the information to your own tax records, and respond by the deadline printed on the document. Most IRS notices explain exactly what changed, why it changed, and what action you need to take. If you agree with the notice, follow the payment or documentation instructions provided. If you disagree, the notice will explain how to dispute the changes, which typically involves mailing a written response with supporting documents to the address on the notice.

The most critical step is acting before the deadline. Late responses can limit your options for disputing proposed changes or requesting a hearing. For a complete walkthrough of what to do when you receive an IRS notice, including what documentation to gather and how to organize your reply, our step-by-step response guide covers every stage from opening the envelope to confirming the issue is resolved.

When To Get Professional Help With An IRS Notice

Consider working with a CPA, Enrolled Agent, or tax attorney when your notice involves a large balance due, a proposed audit, an enforcement action such as a levy or lien, or a situation you do not fully understand. A qualified tax professional can communicate directly with the IRS on your behalf, identify resolution options you may not be aware of, and ensure your rights as a taxpayer are protected throughout the process. According to the IRS, you can authorize a representative by filing Form 2848, Power of Attorney and Declaration of Representative. Simple notices confirming a small refund adjustment or a zero-balance correction typically do not require professional assistance.

Frequently Asked Questions About IRS Notices

What Is The Most Common IRS Notice?

The CP14 is the most commonly issued IRS notice. According to the IRS, a CP14 is sent when a filed tax return shows an unpaid balance. The notice lists the amount owed, the payment due date, and the options available for resolving the balance.

How Do I Know If My IRS Notice Is Real?

A real IRS notice arrives by U.S. mail, includes a notice number in the upper right corner, and references a tax year tied to your account. According to the IRS, the agency never initiates contact by email, text, or social media. You can verify any notice by logging in to your IRS Online Account at IRS.gov.

What Happens If I Ignore An IRS Notice?

Ignoring an IRS notice allows penalties and interest to accumulate and moves your case further along the collection process. According to the IRS, unresolved balances can eventually lead to a federal tax lien on your property, levies on your bank accounts and wages, and garnishment of up to 15 percent of your Social Security benefits.

Can I View My IRS Notices Online?

Yes, many IRS notices are available through your IRS Online Account. According to the IRS, you can log in at IRS.gov to view digital copies of notices the agency has sent to your address on file, which provides a convenient way to review your correspondence without waiting for mail delivery.

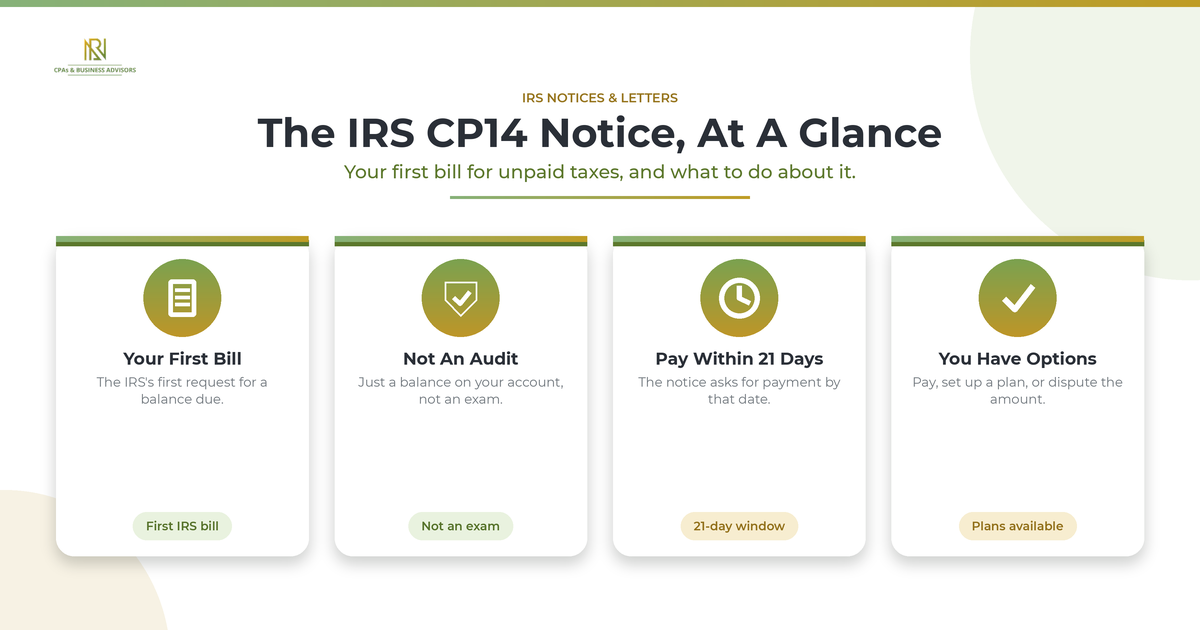

IRS CP14 Notice: Your First Bill For Unpaid Taxes

An IRS CP14 notice is the IRS's first bill, a letter telling you that you owe money on unpaid taxes and asking you to pay within 21 days. According to the IRS, it is not an audit; it means your return was processed and your account shows a balance due, including any interest and penalties. If you already paid, you may not owe anything, so it is worth verifying before you send a payment.

What Is An IRS CP14 Notice?

A CP14 is the IRS's first billing notice, formally the Notice of Tax Due and Demand for Payment, sent when your account shows an unpaid balance. According to the IRS, it is issued after your tax return is processed and the records show you owe money on unpaid taxes. The notice lays out the tax year, the amount you owe in tax, interest, and penalties, and a deadline to pay. Receiving one does not mean you are being audited or that a lien or levy has started. It is the opening step in resolving a balance, and the IRS sends millions of them each year.

Is A CP14 Notice Bad?

A CP14 is serious but routine, and it is fixable. It is the IRS's standard first request for payment, not a penalty notice in itself and not a sign of an audit, though the balance it shows can include penalties and interest on top of the tax. What matters is acting on it rather than ignoring it, because the amount only grows while it sits. Handled promptly, most CP14 balances are straightforward to pay or dispute.

Why Did You Get A CP14 Notice?

You received a CP14 because the IRS processed a return showing a balance due that was not paid in full by the deadline. According to the IRS, the two basic triggers are filing a return with a balance due and not paying the taxes owed by the due date. Common underlying causes include underpaid estimated taxes, an extension that postponed your filing date but not your payment due date, or a balance left after the IRS adjusted your return. Sometimes it is simply a timing issue, where you paid but the payment had not yet posted to your account when the notice was generated.

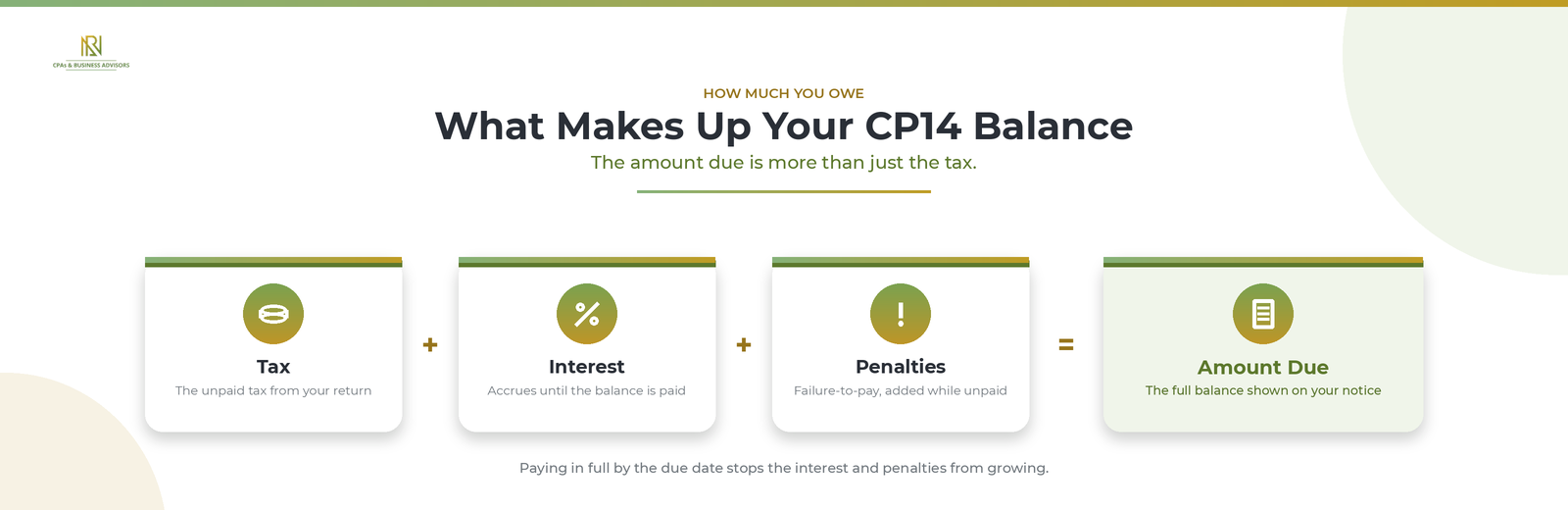

How Much You Owe And When It's Due

The CP14 shows your full balance, tax plus interest and penalties, and asks you to pay within 21 days of the notice date. According to the IRS, interest accrues on the unpaid amount and a failure-to-pay penalty is added while the balance goes unpaid, so paying in full by the date on the notice stops further interest and penalties from building. The Taxpayer Advocate Service notes that if the balance is not fully paid within about 60 days, the IRS can move forward with collection. The 21-day request is the window to act, not a hard cutoff after which nothing else happens.

What If You Already Paid?

If you already paid in full, don't pay again; verify your account first, because the IRS has acknowledged sending CP14 notices in error. According to the IRS, some taxpayers who paid on time, electronically or by check, received a CP14 because the payment had not finished processing or posted with an error, and it advised those taxpayers not to respond or pay a second time while it corrects the accounts, with penalties and interest adjusted automatically once the payment is applied. To confirm where you stand, sign in to your IRS Online Account and review your tax account transcript, checking that each payment posted to the right year and amount. A misapplied payment, a still-processing amended return, or an estimated payment credited to the wrong period are common reasons a balance shows when you don't actually owe it. If your records don't match the notice, dispute it in writing to the address on the notice, including your name, the tax year, and copies of your proof such as cancelled checks or payment confirmations, and keep your originals.

How To Pay Your CP14

If the amount is correct, the fastest resolution is to pay it. According to the IRS, you can pay online, and paying by the due date on the notice limits the interest and penalties you owe. Include the notice's reference details with your payment so it is applied to the right year, and keep a record of the confirmation. Paying the full balance closes the notice; if you can't pay all of it, you still have options.

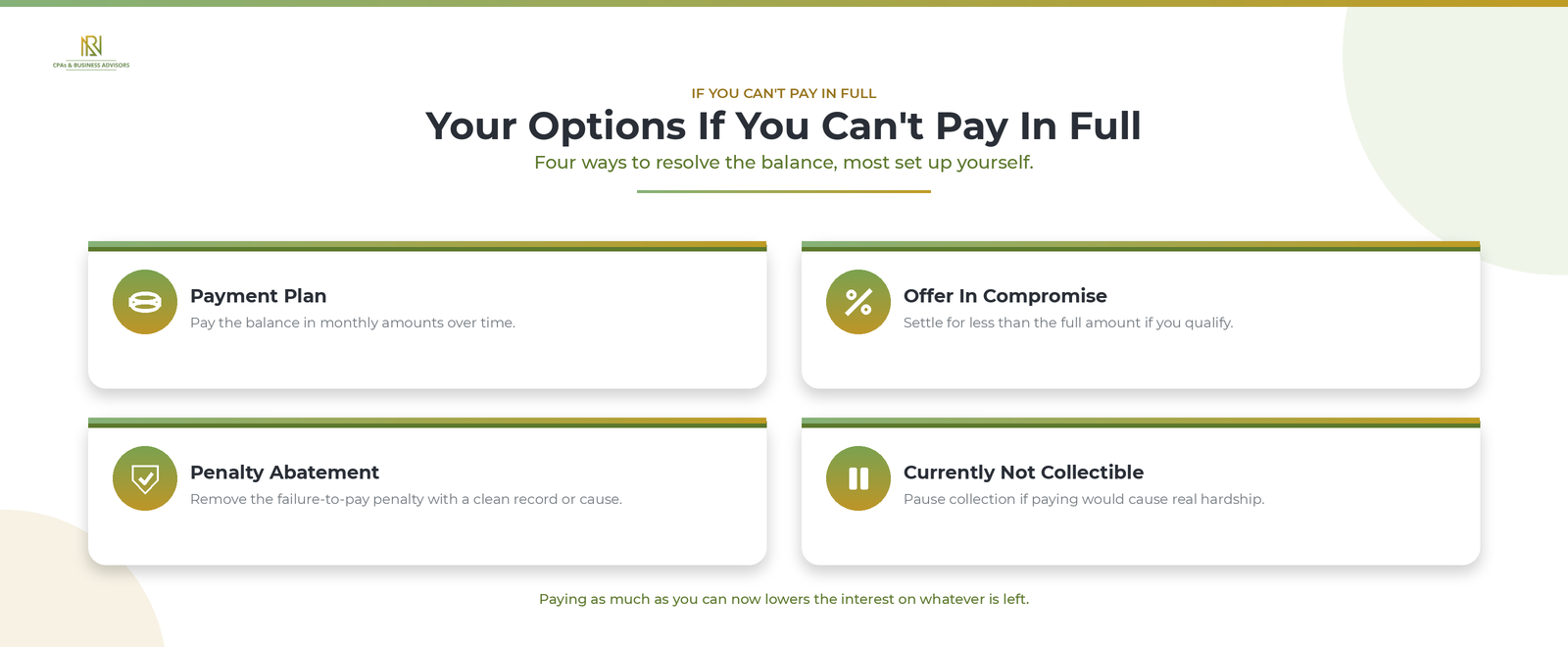

What If You Can't Pay In Full?

If you can't pay the whole balance, you have several options, and you can set most of them up yourself. According to the IRS, the main paths are:

- A payment plan, or installment agreement, that lets you pay the balance in monthly amounts over time, available online for many individual balances.

- An offer in compromise, which settles the debt for less than the full amount when you qualify.

- First-time penalty abatement or reasonable-cause relief, which can remove the failure-to-pay penalty if you have a clean recent history or a valid reason.

- A temporary delay of collection, sometimes called currently not collectible status, if paying would create real hardship.

Even if you choose a plan, paying as much as you can now reduces the interest that keeps accruing on the remaining balance. Setting up an installment agreement with your response also signals to the IRS that you intend to resolve the balance.

What Happens If You Ignore A CP14 Notice?

Ignoring a CP14 doesn't stop the balance; it grows the debt and moves you toward collection. According to the IRS, interest and the failure-to-pay penalty keep accruing on the unpaid amount, and if you don't resolve the balance the account advances through further notices demanding payment. Left unaddressed, that path leads to enforced collection, which can include a federal tax lien or a levy on wages or bank accounts. Because the CP14 is the first and easiest point to deal with the balance, responding now, by paying, arranging a plan, or disputing it, is far cheaper than waiting.

Should You Handle It Yourself Or Get Help?

You can handle most CP14 notices yourself, especially when the balance is correct and you can pay or set up a plan online. According to the IRS, you can resolve a debt and manage your account without calling. Consider professional help when the balance is large, when you believe the notice is wrong and need to build a documented dispute, or when paying would cause hardship. A CPA or enrolled agent can pull your transcripts, verify the amount, and deal with the IRS for you, and a firm offering IRS tax resolution services can manage the response end to end. If cost is a barrier, a Low Income Taxpayer Clinic may help for free or a small fee. Either way, if you're not sure what your letter is asking, start with our overview of the general steps for any IRS letter.

Frequently Asked Questions

What is a CP14 notice? It is the IRS's first bill, telling you that you owe money on unpaid taxes and asking for payment within 21 days.

Is a CP14 notice bad? It is serious but routine and fixable. It is not an audit, and acting on it promptly keeps interest and penalties from growing.

How do I respond to a CP14 notice? Verify the balance against your records, then pay it, set up a payment plan if you can't pay in full, or dispute it in writing if the amount is wrong.

Is notice CP14 a civil penalty? No. The CP14 is a demand for payment of tax you owe, though the balance can include penalties and interest in addition to the tax.

What if I paid my taxes but received a CP14? Don't pay twice. Check your IRS account to confirm the payment posted, and if you paid in full and on time, the IRS has said affected taxpayers should not respond while it corrects the account.

A CP14 notice is the IRS letting you know about a balance and asking you to settle it, not a penalty or an audit. Confirm the amount is right, pay it or arrange a plan if it is, and dispute it with proof if it isn't. Dealt with inside the window it gives you, a CP14 is one of the simpler IRS notices to put behind you.