%201.avif)

.png)

.png)

Virtual CFO for Startups

A virtual CFO for startups is a part-time, remote financial leader who provides the same level of strategic guidance a full-time CFO would, but without the six-figure salary. Startups use virtual CFOs to manage cash flow, build financial forecasts, prepare for fundraising, and make smarter spending decisions during the early stages of growth.

In this article, we cover what a virtual CFO actually does for startups, how this role is different from a traditional CFO or bookkeeper, when your startup needs one, and what to look for before hiring. We also walk through the key financial areas a virtual CFO handles, from burn rate tracking to investor-ready reporting.

What Is a Virtual CFO for Startups and Why Does It Matter

A virtual CFO for startups is an outsourced financial professional who provides chief financial officer services on a part-time or contract basis. Instead of working in your office full time, a virtual CFO works remotely and focuses on high-level financial strategy, planning, and decision support.

This matters because most early-stage companies cannot afford a full-time CFO. According to Salary.com, the median base salary for a CFO in the United States is around $437,000 per year. When you add bonuses, benefits, and equity, total compensation can easily exceed $750,000 annually, according to data from Cowen Partners Executive Search. For a startup running on a seed round or Series A, that kind of fixed cost is simply not realistic.

A virtual CFO fills that gap. You get senior-level virtual CFO support for a fraction of the cost. According to Business Research Insights, the global virtual CFO market was valued at roughly $3.91 billion in 2024 and is projected to reach $8.17 billion by 2032, growing at a compound annual growth rate of about 9.6%. That growth tells a clear story. More startups and small businesses are turning to this model because it works.

What Is the Difference Between a CFO and a Virtual CFO

The difference between a CFO and a virtual CFO is the employment model, not the expertise. A traditional CFO is a full-time, in-house executive who sits on the leadership team and handles all financial operations day to day. A virtual CFO provides the same strategic services, but on a part-time, remote, or project basis.

For startups, the virtual model makes more sense for several reasons. First, cost. A full-time CFO at a small company with under $50 million in revenue still earns between $150,000 and $300,000 in base salary alone, according to industry reports from Visdum. Second, flexibility. A virtual CFO can scale hours up during a fundraise or a big financial decision and scale back down during quieter months. Third, speed. You can bring a virtual CFO on board in days instead of the 120 to 180 days it typically takes to recruit a full-time CFO, according to Staffing Soft research.

Around 80% of startups operate without a CFO in the early stages, according to The Wall Street Journal. That means the vast majority of founders are making critical financial decisions without any executive-level financial guidance. A fractional CFO closes that gap without locking you into a permanent hire you may not be ready for.

Is a CFO for a Small Company Worth It

Yes, a CFO for a small company is worth it, especially when you use the virtual model. The data supports this clearly. According to CB Insights, 29% of startups fail because they run out of funding. A separate report from QuickBooks found that 82% of businesses experience cash flow problems at some point. These are exactly the issues a CFO is trained to prevent.

A virtual CFO helps a small company track burn rate, forecast revenue, manage working capital, and plan around seasonal fluctuations. They also prepare the financial reports that banks, investors, and lenders want to see before writing a check. Without this level of financial oversight, small companies often spend too fast, miss tax deadlines, or fail to catch warning signs in their numbers until it is too late.

Forbes has reported that 70% of startups with poor budgeting fail. That number alone shows the value of having someone who can build and monitor a real budget. Even on a part-time basis, a business consultant with CFO-level expertise can change the financial trajectory of a small company.

Does a Small Company Need a CFO

A small company needs a CFO when the financial decisions become too complex for the founder or a bookkeeper to handle alone. This usually happens when revenue crosses a certain threshold, when you start raising outside capital, when you hire employees, or when tax obligations become more layered.

We see this pattern often. A founder handles their own books in year one, maybe with help from a bookkeeper or an accountant. But once the business starts growing, things like revenue recognition, payroll taxes, multi-state compliance, and investor reporting pile up fast. At that point, the founder is spending hours every week on finance instead of building the product or closing sales.

According to a Startup Genome report, only 40% of startups achieve profitability. The other 60% either break even or lose money. Having a virtual CFO in place does not guarantee profit, but it does mean your financial plan is being built and monitored by someone who knows how to read the signals, adjust the course, and help you get there faster.

How to Hire a CFO for a Startup

Hiring a CFO for a startup starts with knowing what you actually need. Not every startup needs a full-time CFO on day one. In most cases, a virtual or fractional CFO is the right first step.

When Should a Startup Bring on a Virtual CFO

A startup should bring on a virtual CFO when financial decisions start affecting the direction of the business. Common trigger points include preparing for a funding round, negotiating a large contract, onboarding investors, building a financial model, or setting up tax planning strategies for the first time.

If you are spending more time in spreadsheets than building your product, that is a clear sign you need help. If investors are asking for financial projections and you are not sure how to build them, that is another sign. The Kauffman Foundation has noted that first-time founders have only an 18% success rate. Having experienced financial leadership on your side can significantly improve your odds.

What to Look for in a Virtual CFO

Look for someone with experience working with startups specifically. The financial needs of a startup are very different from a mature company. Your virtual CFO should have experience with cash flow modeling, fundraising support, burn rate analysis, and investor reporting. They should also be comfortable working with cloud-based tools like QuickBooks Online, Xero, or other modern accounting platforms.

Industry-specific knowledge is also important. A virtual CFO who understands SaaS metrics will serve a software startup better than someone whose background is in manufacturing. The same goes for e-commerce, healthcare, or service-based startups. Each has its own financial patterns and challenges.

What Does a Virtual CFO Do for Startups

A virtual CFO for startups handles the financial strategy and oversight that founders typically cannot do on their own. The role is broader than bookkeeping or tax filing. It covers planning, analysis, and decision support across the entire business.

Cash Flow Forecasting and Burn Rate Management

Cash flow is the single biggest financial concern for any startup. According to the U.S. Small Business Administration, cash flow problems are the leading cause of failure among profitable small companies. A virtual CFO builds rolling cash flow forecasts, usually on a 13-week cycle, so you can see exactly where your money is going and how long your runway lasts.

Burn rate management ties directly into this. Your virtual CFO tracks how fast you are spending money relative to your revenue and funding. If your burn rate is too high, they will recommend specific cuts or timing adjustments. If you have room to invest, they will help you figure out where to put the money for the best return.

Financial Modeling and Investor-Ready Reporting

Startups that plan to raise capital need clean, professional financial models. Investors want to see revenue projections, unit economics, customer acquisition costs, and a clear path to profitability. According to Crunchbase funding analysis, companies with dynamic financial forecasting are 2.7 times more likely to raise follow-on funding.

A virtual CFO builds these models and keeps them updated. They also prepare the financial statements that investors review during due diligence. Clean books and well-organized reports send a strong signal to anyone considering putting money into your company.

Budgeting and Resource Allocation

Startups burn through resources fast when there is no budget in place. A virtual CFO creates a realistic budget based on your revenue, funding, and growth goals. They then monitor actual spending against that budget every month and flag any areas where you are over or under.

This is especially important for startups with limited runway. According to Sequoia Capital's survival guide, companies with less than 12 months of runway should immediately adjust spending or accelerate fundraising. A virtual CFO keeps that clock visible and actionable.

Tax Strategy and Compliance

Tax planning is not just an end-of-year task. For startups, it starts the moment you choose your business entity. An S-Corp, C-Corp, or LLC each comes with different tax treatments, and the wrong choice can cost thousands of dollars every year.

A virtual CFO works alongside your CPA to make sure your startup takes advantage of every available deduction, credit, and incentive. They also track estimated tax payments, multi-state nexus obligations, and payroll taxes so nothing falls through the cracks. We handle startup advisory work like this regularly, and it often saves founders from expensive surprises.

Why Do 90% of Startups Fail

Approximately 90% of startups fail due to a combination of factors, including lack of market demand, running out of cash, team issues, and poor financial management. According to CB Insights, 42% of startups fail because they built a product nobody wanted to pay for. Another 29% fail because they simply ran out of money.

Financial mismanagement is a thread that runs through most of these failures. Even startups with a great product can collapse if they burn through cash too fast, fail to plan for slow revenue months, or do not track their spending accurately. Data from DemandSage shows that 70% of startups fail between their second and fifth year, which is exactly the period when financial complexity grows the fastest.

This is why a virtual CFO can be so valuable. They bring discipline to the financial side of the business during the years when the risk of failure is highest. They do not just track the numbers. They interpret them and turn them into decisions that help the company survive and grow.

Reason for Startup FailurePercentageSourceNo market demand for the product42%CB InsightsRan out of cash or funding29%CB InsightsWrong team or leadership issues23%CB InsightsGot outcompeted in the market19%CB InsightsCash flow and financial management problems82% experience issuesQuickBooksPoor budgeting70% failForbesUnderestimated operating costs48%Startup Genome

Sources: CB Insights (2022), QuickBooks, Forbes, Startup Genome

How Much Does a Virtual CFO Cost Compared to a Full-Time CFO

A virtual CFO typically costs between $3,000 and $10,000 per month on a retainer basis. Hourly rates range from $200 to $400 per hour for project-based work, such as fundraising preparation or financial model building. Compare that to a full-time CFO, whose base salary alone ranges from $300,000 to $450,000 per year, according to multiple salary surveys for 2025.

The savings are significant. A startup paying $5,000 per month for a virtual CFO spends $60,000 per year. That is roughly 15 to 20% of what a full-time CFO would cost in base salary alone, before benefits, equity, and bonuses. For a company still finding product-market fit, those savings can extend your runway by months.

According to Embroker's startup statistics, U.S. venture capital investment reached $190.4 billion in 2024, a 30% increase from 2023. That tells us the startup ecosystem is highly active, and the founders who manage their capital wisely will outlast those who do not. A virtual CFO helps you stretch every dollar further while still getting the financial leadership you need.

What Financial Metrics Should Startups Track

Startups should track the financial metrics that directly affect survival and growth. A virtual CFO sets up dashboards and reporting systems so you can see these numbers at a glance.

Burn Rate and Runway

Burn rate is how much cash your startup spends each month beyond what it earns. Runway is how many months you can operate before the money runs out. These two numbers together tell you whether your current spending pace is sustainable. Sequoia Capital recommends maintaining at least 18 to 24 months of runway in the current funding environment.

Monthly Recurring Revenue and Growth Rate

For SaaS and subscription-based startups, monthly recurring revenue is the core health metric. Your virtual CFO tracks this alongside your month-over-month growth rate to see whether revenue is accelerating or slowing down. Investors pay close attention to this number, and a consistent upward trend makes fundraising much easier.

Customer Acquisition Cost and Lifetime Value

Customer acquisition cost tells you how much it costs to win a new customer. Lifetime value tells you how much revenue that customer generates over time. A healthy startup has a lifetime value that is at least three times the acquisition cost. Your virtual CFO monitors this ratio and helps you adjust marketing and sales spending accordingly.

Working with a firm that offers strategic business planning can help you tie these metrics into a bigger growth plan that keeps your company on track.

How a Virtual CFO Helps Startups Prepare for Fundraising

A virtual CFO helps startups prepare for fundraising by building the financial infrastructure that investors expect to see. This includes a three-to-five-year financial model, clean historical financials, a clear explanation of unit economics, and a cap table that is organized and up to date.

According to Crunchbase research, poor financial modeling leads to unexpected cash shortfalls in 76% of failed startups. Investors know this, and they look for startups that have a CFO or financial leader who can explain the numbers confidently. A virtual CFO coaches the founder on how to present financials during pitch meetings and due diligence calls.

Before a Series A or seed round, a virtual CFO also runs scenario modeling. This means building multiple versions of your financial plan based on different outcomes, like what happens if revenue grows 20% slower than expected, or what happens if a major customer churns. This kind of preparation gives investors confidence that you have thought through the risks.

Having solid business formation and entity structure in place before fundraising is also critical. Investors want to see that your company is set up correctly from a legal and tax perspective.

Signs Your Startup Needs a Virtual CFO Right Now

Not every startup needs a virtual CFO from day one, but most need one sooner than they think. Here are clear signals that it is time to bring one on.

You are spending more than $50,000 per month and do not have a clear picture of where the money is going. You are about to raise your first round of outside funding. Investors are asking for financial projections, and you are not sure how to build them. You missed a tax deadline or got hit with an unexpected tax bill. Your bookkeeper is great at data entry but cannot answer strategic financial questions. You are hiring employees and need help with payroll, benefits, and compensation planning.

According to the U.S. Bureau of Labor Statistics, about 20% of startups fail within the first year. By year five, that number climbs to nearly 50%. The startups that survive often have one thing in common. They made smarter financial decisions earlier in the process. A virtual CFO is one of the most effective ways to make sure that happens. Here in Miami, we work with startups at every stage and see firsthand how early financial guidance changes outcomes.

Frequently Asked Questions

How Much Does a Virtual CFO Make

A virtual CFO makes between $150 and $400 per hour on a project basis, or between $3,000 and $10,000 per month on a retainer. Annual earnings vary widely depending on the number of clients and the complexity of the work. Some experienced virtual CFOs earn over $200,000 per year working with multiple startups simultaneously.

What Is the Hourly Rate for a CFO

The hourly rate for a CFO ranges from $200 to $400 per hour for virtual or fractional work. For full-time salaried CFOs, the equivalent hourly rate is roughly $210 per hour based on a median base salary of $437,000, according to Salary.com data for 2025.

Can an LLC Get Grant Money

Yes, an LLC can get grant money, though options are more limited than for nonprofits. Federal grants from agencies like the Small Business Administration and the Department of Energy are available to for-profit LLCs in specific industries. State and local governments also offer grants for small businesses in areas like clean energy, technology, and job creation.

How to Get Clients for Virtual CFO

Virtual CFOs get clients by building a strong referral network with CPAs, bookkeepers, attorneys, and business consultants. They also create content that demonstrates their expertise, speak at industry events, and partner with startup incubators and accelerators. According to Techstars, startups in accelerator programs are 3 times more likely to succeed, so connecting with those programs is a smart channel.

Is $20,000 Enough to Work With a Financial Advisor

Yes, $20,000 is enough to work with a financial advisor, especially if you choose a fee-only advisor who charges a flat rate or hourly fee. Many advisors work with clients at all asset levels, and some specialize in working with early-career professionals or small business owners.

How Much Should a Startup CEO Pay Themselves

A startup CEO should pay themselves enough to cover basic living expenses without draining the company's cash reserves. According to Deel, the average startup CEO salary is around $148,000 per year, though this varies widely based on funding stage, industry, and location. Pre-revenue founders often take much less, sometimes between $50,000 and $80,000.

Is AI Replacing Bookkeepers

AI is automating many routine bookkeeping tasks like data entry, bank reconciliation, and invoice processing. It is not fully replacing bookkeepers yet, but it is changing the role. Bookkeepers who learn to use AI-powered tools are becoming more efficient and valuable. The strategic financial work that a virtual CFO or CPA handles is much harder for AI to replicate because it requires judgment, context, and experience.

Putting It All Together

A virtual CFO gives startups the financial leadership they need without the heavy cost of a full-time executive hire. From cash flow forecasting and burn rate tracking to investor-ready reporting and tax strategy, the right virtual CFO turns financial uncertainty into a clear, actionable plan. The data is consistent. Startups with stronger financial management survive longer, raise more capital, and grow faster.

If your startup is approaching a fundraising round, scaling the team, or just trying to get better visibility into the numbers, now is a good time to bring in experienced financial guidance. At NR CPAs & Business Advisors, we work with founders and growing companies to bring structure and clarity to their finances. Reach out to us at (954) 231-6613 to start the conversation.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

IRS CP14 Notice: Your First Bill For Unpaid Taxes

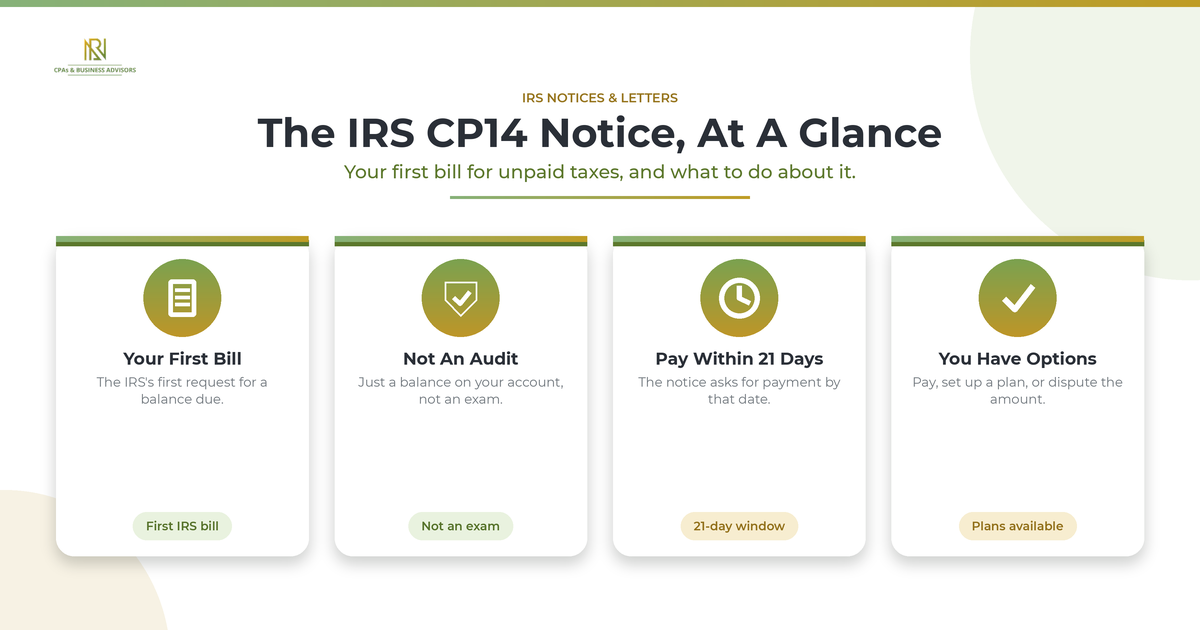

An IRS CP14 notice is the IRS's first bill, a letter telling you that you owe money on unpaid taxes and asking you to pay within 21 days. According to the IRS, it is not an audit; it means your return was processed and your account shows a balance due, including any interest and penalties. If you already paid, you may not owe anything, so it is worth verifying before you send a payment.

What Is An IRS CP14 Notice?

A CP14 is the IRS's first billing notice, formally the Notice of Tax Due and Demand for Payment, sent when your account shows an unpaid balance. According to the IRS, it is issued after your tax return is processed and the records show you owe money on unpaid taxes. The notice lays out the tax year, the amount you owe in tax, interest, and penalties, and a deadline to pay. Receiving one does not mean you are being audited or that a lien or levy has started. It is the opening step in resolving a balance, and the IRS sends millions of them each year.

Is A CP14 Notice Bad?

A CP14 is serious but routine, and it is fixable. It is the IRS's standard first request for payment, not a penalty notice in itself and not a sign of an audit, though the balance it shows can include penalties and interest on top of the tax. What matters is acting on it rather than ignoring it, because the amount only grows while it sits. Handled promptly, most CP14 balances are straightforward to pay or dispute.

Why Did You Get A CP14 Notice?

You received a CP14 because the IRS processed a return showing a balance due that was not paid in full by the deadline. According to the IRS, the two basic triggers are filing a return with a balance due and not paying the taxes owed by the due date. Common underlying causes include underpaid estimated taxes, an extension that postponed your filing date but not your payment due date, or a balance left after the IRS adjusted your return. Sometimes it is simply a timing issue, where you paid but the payment had not yet posted to your account when the notice was generated.

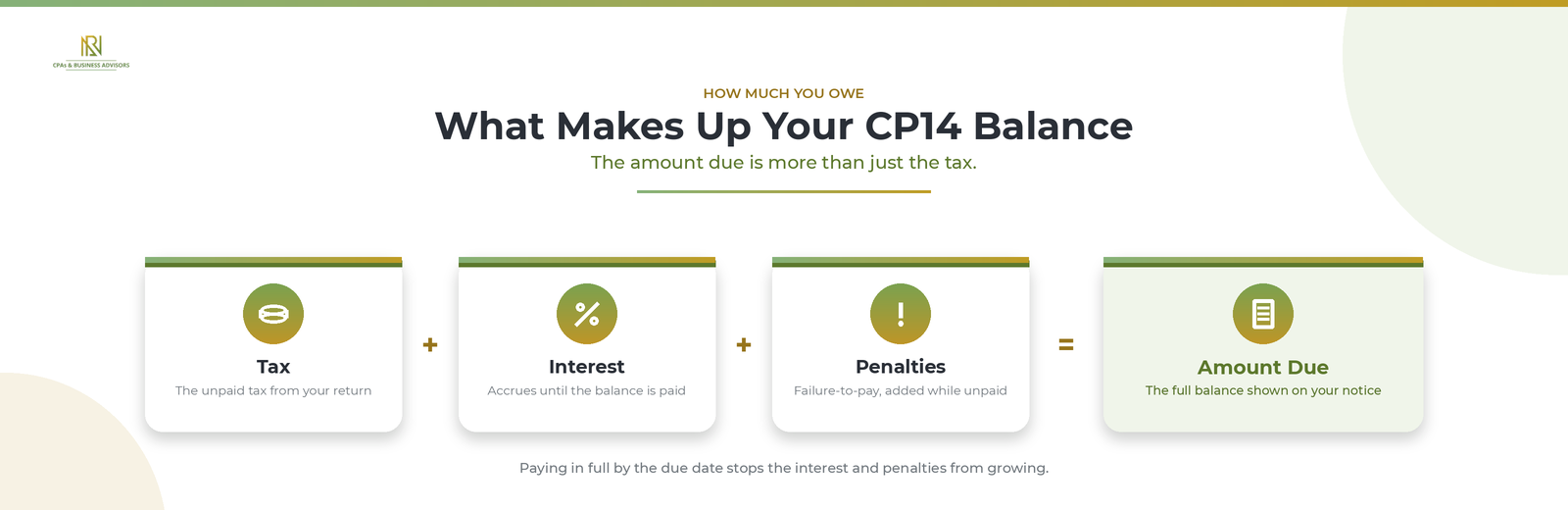

How Much You Owe And When It's Due

The CP14 shows your full balance, tax plus interest and penalties, and asks you to pay within 21 days of the notice date. According to the IRS, interest accrues on the unpaid amount and a failure-to-pay penalty is added while the balance goes unpaid, so paying in full by the date on the notice stops further interest and penalties from building. The Taxpayer Advocate Service notes that if the balance is not fully paid within about 60 days, the IRS can move forward with collection. The 21-day request is the window to act, not a hard cutoff after which nothing else happens.

What If You Already Paid?

If you already paid in full, don't pay again; verify your account first, because the IRS has acknowledged sending CP14 notices in error. According to the IRS, some taxpayers who paid on time, electronically or by check, received a CP14 because the payment had not finished processing or posted with an error, and it advised those taxpayers not to respond or pay a second time while it corrects the accounts, with penalties and interest adjusted automatically once the payment is applied. To confirm where you stand, sign in to your IRS Online Account and review your tax account transcript, checking that each payment posted to the right year and amount. A misapplied payment, a still-processing amended return, or an estimated payment credited to the wrong period are common reasons a balance shows when you don't actually owe it. If your records don't match the notice, dispute it in writing to the address on the notice, including your name, the tax year, and copies of your proof such as cancelled checks or payment confirmations, and keep your originals.

How To Pay Your CP14

If the amount is correct, the fastest resolution is to pay it. According to the IRS, you can pay online, and paying by the due date on the notice limits the interest and penalties you owe. Include the notice's reference details with your payment so it is applied to the right year, and keep a record of the confirmation. Paying the full balance closes the notice; if you can't pay all of it, you still have options.

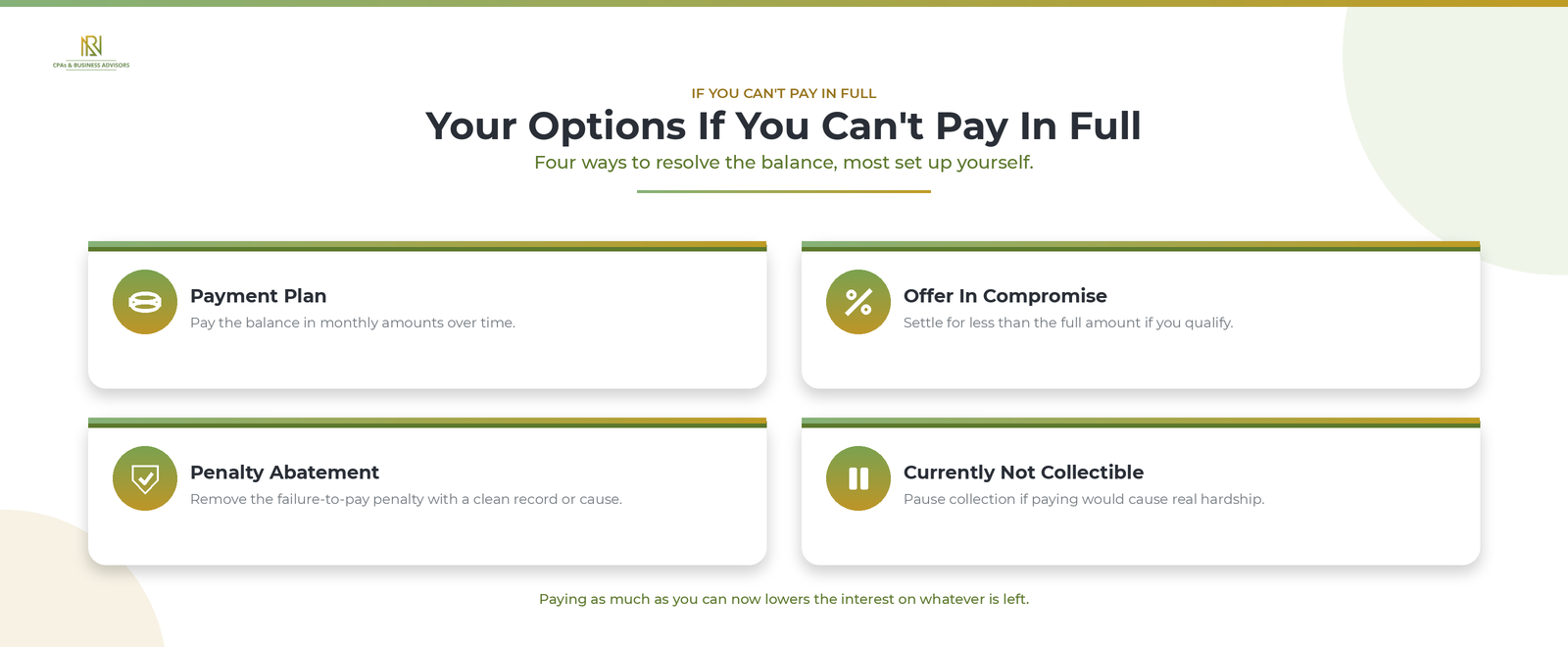

What If You Can't Pay In Full?

If you can't pay the whole balance, you have several options, and you can set most of them up yourself. According to the IRS, the main paths are:

- A payment plan, or installment agreement, that lets you pay the balance in monthly amounts over time, available online for many individual balances.

- An offer in compromise, which settles the debt for less than the full amount when you qualify.

- First-time penalty abatement or reasonable-cause relief, which can remove the failure-to-pay penalty if you have a clean recent history or a valid reason.

- A temporary delay of collection, sometimes called currently not collectible status, if paying would create real hardship.

Even if you choose a plan, paying as much as you can now reduces the interest that keeps accruing on the remaining balance. Setting up an installment agreement with your response also signals to the IRS that you intend to resolve the balance.

What Happens If You Ignore A CP14 Notice?

Ignoring a CP14 doesn't stop the balance; it grows the debt and moves you toward collection. According to the IRS, interest and the failure-to-pay penalty keep accruing on the unpaid amount, and if you don't resolve the balance the account advances through further notices demanding payment. Left unaddressed, that path leads to enforced collection, which can include a federal tax lien or a levy on wages or bank accounts. Because the CP14 is the first and easiest point to deal with the balance, responding now, by paying, arranging a plan, or disputing it, is far cheaper than waiting.

Should You Handle It Yourself Or Get Help?

You can handle most CP14 notices yourself, especially when the balance is correct and you can pay or set up a plan online. According to the IRS, you can resolve a debt and manage your account without calling. Consider professional help when the balance is large, when you believe the notice is wrong and need to build a documented dispute, or when paying would cause hardship. A CPA or enrolled agent can pull your transcripts, verify the amount, and deal with the IRS for you, and a firm offering IRS tax resolution services can manage the response end to end. If cost is a barrier, a Low Income Taxpayer Clinic may help for free or a small fee. Either way, if you're not sure what your letter is asking, start with our overview of the general steps for any IRS letter.

Frequently Asked Questions

What is a CP14 notice? It is the IRS's first bill, telling you that you owe money on unpaid taxes and asking for payment within 21 days.

Is a CP14 notice bad? It is serious but routine and fixable. It is not an audit, and acting on it promptly keeps interest and penalties from growing.

How do I respond to a CP14 notice? Verify the balance against your records, then pay it, set up a payment plan if you can't pay in full, or dispute it in writing if the amount is wrong.

Is notice CP14 a civil penalty? No. The CP14 is a demand for payment of tax you owe, though the balance can include penalties and interest in addition to the tax.

What if I paid my taxes but received a CP14? Don't pay twice. Check your IRS account to confirm the payment posted, and if you paid in full and on time, the IRS has said affected taxpayers should not respond while it corrects the account.

A CP14 notice is the IRS letting you know about a balance and asking you to settle it, not a penalty or an audit. Confirm the amount is right, pay it or arrange a plan if it is, and dispute it with proof if it isn't. Dealt with inside the window it gives you, a CP14 is one of the simpler IRS notices to put behind you.

What to Do When You Receive an IRS Notice?

If you receive an IRS notice, don't panic. Read it carefully, find the notice number to see what it is about, check the deadline, and then either follow the instructions to respond or get a tax professional to help. Most IRS letters deal with one specific issue and are straightforward to handle once you know what they are asking for.

First, Don't Panic (And Don't Ignore It)

A letter from the IRS rarely means trouble, but you should never ignore it. According to the IRS, it sends notices for routine reasons, such as a balance due, a changed refund, or a simple question about your return, and most are resolved by reading the letter and taking the step it asks for. What you cannot do is set it aside. Acting promptly limits interest and penalties, and many notices carry a firm deadline. The calm, timely response is almost always the cheapest one.

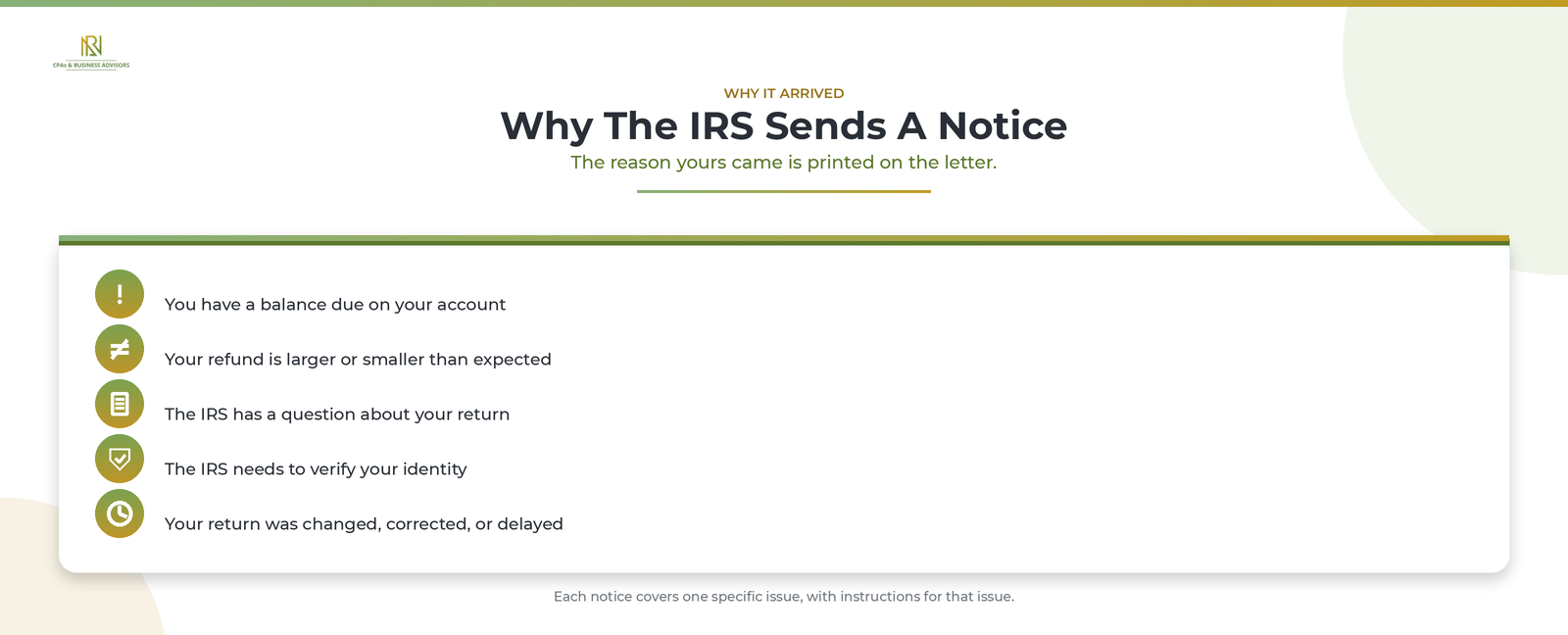

Why Did The IRS Send You A Notice?

The IRS contacts you when something on your account or return needs attention. According to the IRS, the most common reasons are:

- You have a balance due.

- Your refund is larger or smaller than you expected.

- The IRS has a question about your return or needs to verify your identity.

- The IRS changed or corrected your return.

- Your return is delayed in processing.

Each notice covers one specific issue and includes instructions for that issue, so the reason yours arrived is stated right on the letter.

What To Do When You Receive An IRS Notice

Work through the notice in order: read it, identify it, verify it, compare it to your return, note the deadline, respond, and keep a copy. According to the IRS, these steps handle the large majority of letters without a phone call or an office visit:

- Read the entire notice carefully to understand the issue and the action it asks for.

- Find the notice or letter number in the top right corner, such as CP14 or CP2000, and look it up on IRS.gov for a plain-English explanation.

- Verify the notice is genuine before you act or pay anything.

- Compare the notice against your tax return, and check which tax year it covers rather than assuming it is your most recent one.

- Note the response deadline and put it somewhere you will not miss it.

- Respond the way the notice tells you to, and only if it asks you to.

- Keep the notice and a copy of your response with your tax records.

The sections below cover the steps that trip people up most.

How To Tell If The Notice Is Real

A genuine IRS notice arrives by mail, never by text, email, or social media. According to the IRS, its first contact comes through the U.S. Postal Service, and it will never use social media or a text message to ask for personal or financial information. To confirm a letter is real, search the notice number on IRS.gov, where every notice is described. If the letter does not show up in that search or looks suspicious, call the IRS at 800-829-1040 and follow the representative's instructions rather than any contact details printed on a questionable letter.

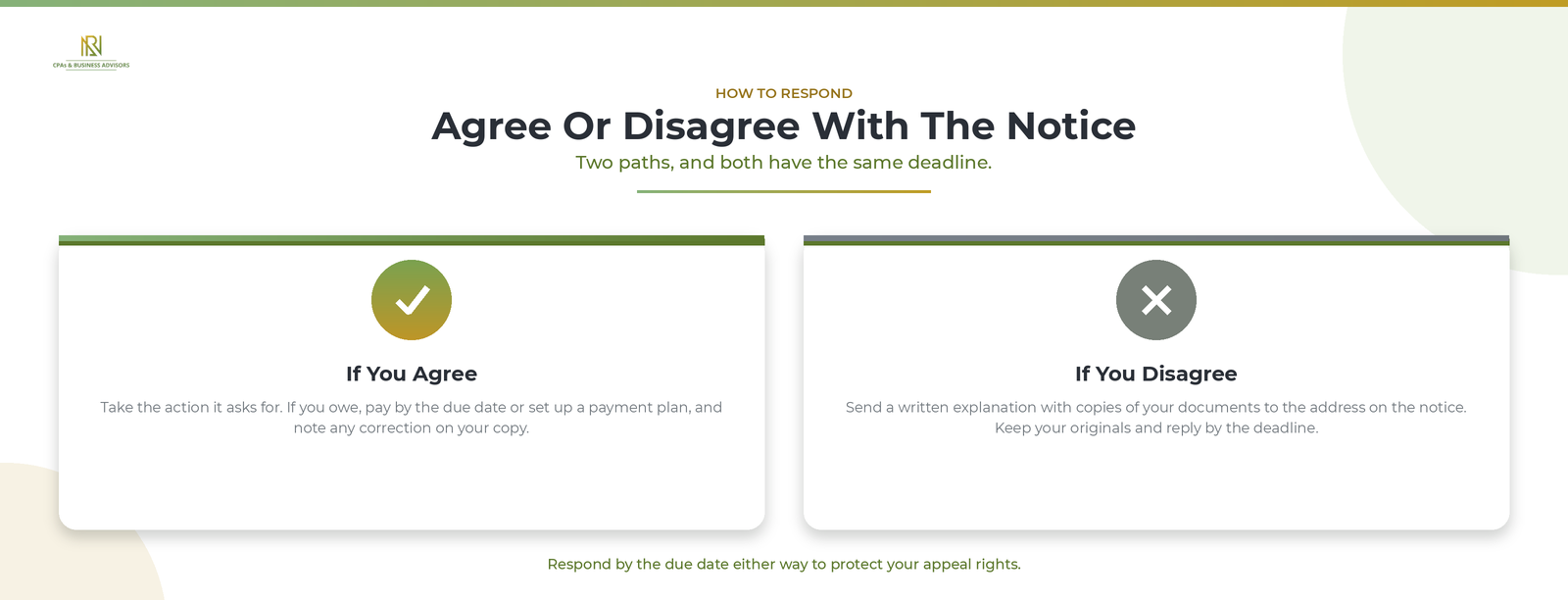

If You Agree With The Notice

If the notice is correct, simply do what it asks. According to the IRS, that usually means taking the requested action and, if you owe, paying by the due date to reduce interest and penalties. If you cannot pay in full, you can arrange to pay the balance over time and still send what you can now, writing the notice's reference number on your payment so the IRS applies it correctly. If the notice corrected your return and you agree, note the change on your own copy and keep it.

If You Disagree With The Notice

If you don't agree, you must respond by the deadline with a written explanation and proof. According to the IRS, you follow the dispute instructions on the notice, send a letter explaining why you disagree, and include copies of any documents that support your position, mailed to the address on the notice. Send copies and keep your originals, and allow at least 30 days for the IRS to reply. Responding by the due date is also what protects your right to appeal later.

How Long Do You Have To Respond?

Most IRS notices give you about 30 days to respond, though the exact window is printed on the letter and varies by notice type. According to the IRS, you should act by the due date shown, because replying on time both limits added interest and penalties and guarantees your appeal rights. If you need more time, call the number in the top right corner of the notice before the deadline passes.

What Happens If You Ignore An IRS Notice?

Ignoring a notice doesn't make it go away; it makes the problem larger. According to the IRS, when you don't respond, interest and penalties keep building and the IRS moves ahead with whatever the letter proposed, which can mean assessing tax you might have disputed or starting collection on a balance. Some letters carry legal deadlines, and missing them costs you options, such as the chance to take a disputed amount to the U.S. Tax Court. Whatever the notice, the safe move is to respond within the window it gives you. If yours is a specific letter like a CP2000 underreported income notice or a CP14 balance due notice, follow the steps for that notice in particular.

Should You Handle It Yourself Or Get Help?

You can resolve most IRS notices on your own, especially simple ones where you agree and just need to pay or send a document. According to the IRS, the majority of correspondence can be handled without calling or visiting an office. Bring in a professional when the amount is large, when you disagree and need to build a documented case, or when the letter signals an examination. A CPA, enrolled agent, or tax attorney can deal with the IRS for you, and a firm offering IRS tax resolution services can manage the whole response. If cost is a concern, a Low Income Taxpayer Clinic may be able to represent you for free or a small fee.

Can You View IRS Notices Online?

Yes, you can see many IRS notices in your online account. According to the IRS, you can view digital copies of select notices and even go paperless for certain letters by signing in to your IRS Online Account. That is also a useful way to confirm a balance or check that a payment has been applied before you respond to a notice about it.

Frequently Asked Questions

How do I respond to an IRS notice? Follow the instructions printed on the notice, and reply only if it asks you to, using the response form or the address provided, within the deadline.

Why would the IRS send me a notice? Usually because you have a balance due, your refund changed, the IRS has a question about your return, or it corrected something on your account.

How long do I have to respond to an IRS notice? Typically about 30 days, but the exact deadline is on the letter and depends on the notice type.

What happens if I ignore an IRS notice? Interest and penalties grow, the IRS proceeds with its proposed change or collection, and you can lose the right to dispute the amount.

Do I need to call the IRS? Usually not. Reply only if the notice instructs you to, and if you must call, use the number in the top right corner with your return and the letter in hand.

An IRS notice is a request to handle one specific thing, not a reason to dread the mailbox. Read it, confirm what it is and that it is genuine, mark the deadline, and respond the way it asks, or hand it to a professional if it is complex. Taken in order and on time, almost every IRS letter is far easier to resolve than it first looks.