%201.avif)

.png)

.png)

How a CFO Improves Cash Flow?

A CFO improves cash flow by building accurate forecasts, tightening collections, controlling expenses, and timing payments so cash is always available when the business needs it. Without this kind of financial oversight, even profitable companies can run into serious trouble paying bills, making payroll, or funding growth.

In this article, we break down the specific ways a CFO manages and improves cash flow, the key metrics they track, the tools they use, and the signs that your business needs this level of financial leadership. We also cover how cash flow management connects to bigger decisions like hiring, expanding, and raising capital.

What Is CFO in Terms of Cash Flow

A CFO in terms of cash flow is the person responsible for making sure money moves through the business at the right speed and in the right direction. While bookkeepers record transactions and accountants prepare reports, a CFO looks ahead. They forecast when cash will come in, when it will go out, and what gaps might appear weeks or months before they happen.

Cash flow is not the same as profit. A business can show a healthy profit on paper and still not have enough cash to cover next week's payroll. According to a Q4 2025 survey by OnDeck and Ocrolus, cash flow is the second biggest concern for small business owners at 29%, right behind inflation at 31%. This tells you that cash flow is not just an accounting issue. It is a survival issue.

The U.S. Small Business Administration has noted that poor cash flow management, not lack of revenue, is the leading cause of failure among otherwise profitable companies. A CFO steps in to prevent that by building systems that give you clear visibility into your cash position every single week. We see this pattern regularly with our virtual CFO clients. The businesses that track cash flow closely are the ones that survive downturns and grow faster during good times.

What Are the Benefits of Having a CFO

The benefits of having a CFO are better financial visibility, smarter spending decisions, faster collections, stronger relationships with lenders and investors, and a clear plan for growth. A CFO turns raw financial data into actionable decisions that protect your cash and increase your margins.

According to a 2025 report from KPMG, proactively managing working capital through aligned metrics, dedicated leadership, and transparent accountability is a key driver of return on invested capital. That is exactly what a CFO does. They do not just watch the numbers. They manage the numbers.

A Bluevine survey of 1,000 small business owners found that only 30% said their profitability was above expectations in 2025, down sharply from 57% in 2024. That kind of drop shows how quickly the financial environment can shift. Having a CFO in place means you are not reacting to those shifts after the damage is done. You are adjusting in real time because someone is watching the dashboard every week.

For growing businesses, a CFO also brings credibility with banks and investors. Clean financial reports, reliable forecasts, and organized books signal that the company is well managed. That makes it easier to get loans approved, negotiate better terms, and attract outside capital when the time is right.

What Are the 4 Roles of a CFO

The four roles of a CFO are financial planning, cash flow management, risk management, and strategic advising. Each role connects directly to how well money moves through the business.

Financial Planning and Forecasting

A CFO builds the financial plan that drives every other decision in the company. This includes annual budgets, revenue projections, hiring plans, and capital expenditure schedules. According to a Blackline survey, nearly 49% of finance professionals worry about the reliability of their cash flow data. A CFO fixes that by creating systems that produce accurate, up-to-date numbers the leadership team can trust.

The foundation of good financial planning is the rolling 13-week cash flow forecast. Every Monday, the CFO or controller updates this model with the actual cash position from the previous Friday, adjusts projections based on new invoices, vendor bills, and payment terms, and flags any week where cash might dip below a safe threshold. This gives the business owner a clear picture of exactly what is coming and when.

Cash Flow Management

This is the core of what a CFO does day to day. They manage the timing of cash inflows and outflows so the business always has enough liquidity to operate. That means monitoring accounts receivable to make sure customers pay on time, managing accounts payable so the company pays strategically without damaging supplier relationships, and building cash reserves for slow periods.

According to the 2025 Small Business Credit Survey, 51% of small businesses face uneven cash flows. A CFO smooths out those ups and downs through disciplined financial reporting and weekly cash reviews.

Risk Management

A CFO identifies financial risks before they become problems. This includes tracking customer concentration (if one client makes up 30% of your revenue, that is a risk), monitoring debt levels, watching for cost increases that could squeeze margins, and stress-testing the financial plan against worst-case scenarios. According to McKinsey research, companies that engage in proactive scenario planning are 33% more likely to recover financially within six months after a disruption compared to those that do not.

Strategic Advising

Beyond the numbers, a CFO serves as a strategic partner to the CEO or business owner. They help evaluate expansion opportunities, assess the ROI of new hires, model the financial impact of entering new markets, and advise on pricing strategy. A good CFO connects every financial decision back to cash flow because cash is what keeps the business alive. This is where strategic business planning and financial leadership overlap.

What Are Ways to Improve Cash Flow

The most effective ways to improve cash flow are speeding up collections, controlling expenses, timing payments strategically, improving invoicing practices, and building a cash reserve. A CFO implements all of these at once as part of a coordinated cash flow strategy.

Speed Up Collections

Late payments are one of the biggest cash flow killers for small businesses. According to Gitnux research, about 61% of small businesses report cash flow issues caused by late payments. An average of 93% of all companies experience at least some late payments from customers.

A CFO attacks this problem from multiple angles. They set clear credit policies for new customers, shorten payment terms where possible (moving from Net 60 to Net 30, for example), automate invoice reminders, and follow up on overdue accounts promptly. According to Gitnux data, companies that offer early payment discounts see a 23% reduction in their average accounts receivable days. The general rule is that a Days Sales Outstanding (DSO) under 45 days is healthy, according to the Corporate Finance Institute. If your DSO is above that, a CFO will build a plan to bring it down.

Control and Time Your Expenses

A CFO reviews every recurring expense to find waste, negotiate better rates, and cut spending that does not produce a clear return. They also time payments strategically. This does not mean paying late. It means using the full payment window available to you so cash stays in your account longer without damaging vendor relationships.

Extending Days Payable Outstanding (DPO) by even a few days can free up significant working capital. A CFO balances this carefully, because stretching payments too far can lead to late fees or damaged supplier trust. The goal is to pay on time, not early, unless there is a discount that makes it worthwhile.

Build a Cash Reserve

According to the OnDeck and Ocrolus small business report, 47% of small businesses are building cash reserves as a hedge against inflation and uncertainty. A CFO helps determine the right reserve level based on your monthly operating costs, revenue volatility, and upcoming financial commitments. Most financial advisors recommend keeping three to six months of operating expenses in reserve, but the right number depends on your specific business.

What Are the Key KPIs for CFOs

The key KPIs for CFOs are operating cash flow, Days Sales Outstanding (DSO), Days Payable Outstanding (DPO), cash conversion cycle, burn rate, gross profit margin, and working capital ratio. These metrics give a CFO everything they need to monitor and improve how cash moves through the business.

KPIWhat It MeasuresWhy It Matters for Cash FlowOperating Cash FlowCash generated from core business operationsShows whether the business funds itself or relies on outside moneyDays Sales Outstanding (DSO)Average days to collect payment after a saleA DSO under 45 days is healthy; above that means cash is stuck in invoicesDays Payable Outstanding (DPO)Average days to pay suppliersLonger DPO keeps cash in the business longer, if managed carefullyCash Conversion Cycle (CCC)Days to turn inventory and sales into cashLower CCC means faster cash flow; combines DSO, DPO, and inventory daysWorking Capital RatioCurrent assets divided by current liabilitiesA ratio above 1.2 signals healthy short-term liquidityGross Profit MarginRevenue minus cost of goods sold as a percentageHigher margins leave more cash after covering direct costsBurn RateMonthly cash spend beyond revenue (for startups)Determines how many months the business can operate before running out of cash

Sources: Corporate Finance Institute, KPMG 2025 Cash Flow Leadership Report, NetSuite CFO KPI Guide, insightsoftware

A CFO tracks these numbers weekly or monthly, depending on the pace of the business. According to NetSuite, if DSO has steadily risen from 45 to 60 days, the CFO would investigate collections processes, credit policies, and customer payment behaviors before that lag starts to squeeze cash flow. That kind of early warning is what separates a well-managed business from one that is constantly reacting to cash crunches.

What Are Five Rules of Cash Flow

Five rules of cash flow that every business should follow are: forecast cash weekly, invoice fast and follow up faster, time your payables carefully, keep a cash reserve for emergencies, and never confuse profit with cash.

The first rule is the most important. A rolling 13-week cash flow forecast is the single best tool a CFO uses to prevent cash surprises. By updating it every week, you always know what is coming in, what is going out, and where any gaps might appear. According to Vayana research, only 2% of CFOs have full confidence in their cash flow visibility, a number that has not improved in recent years. That gap between what CFOs need and what most companies actually have is exactly where cash flow problems start.

The second rule is about speed. The faster you send invoices after delivering a product or service, the faster you get paid. A CFO makes sure invoicing happens within 24 hours of delivery, not days or weeks later. They also set up automated reminders so past-due accounts do not slip through the cracks.

The third rule is about timing. Paying bills early feels responsible, but it drains your cash faster than necessary. A CFO schedules payments to use the full available window without incurring late fees. The fourth rule is building a reserve so that one slow month does not put the business in danger. And the fifth rule is a mindset shift. Many business owners look at their profit and loss statement and think they are doing fine, while their bank account tells a different story. A CFO keeps both in focus at all times.

What Is the 3 Way Cash Flow Model

The 3 way cash flow model is a financial forecasting tool that connects three core financial statements: the income statement (profit and loss), the balance sheet, and the cash flow statement. When all three are linked together in one model, changes in one statement automatically flow through to the others, giving you a complete picture of your financial position.

This model is one of the most powerful tools a CFO uses. For example, if you record a large sale on credit, the income statement shows higher revenue, the balance sheet shows higher accounts receivable, and the cash flow statement shows that the cash has not arrived yet. Without all three connected, you might think you have more cash than you actually do.

According to Prophix research, one real estate company that switched from manual spreadsheet budgeting to a connected forecasting model saw a 50% increase in budget accuracy and a 6.7% increase in operating margin. That is the kind of improvement a properly built 3 way model delivers. We help businesses build this kind of financial infrastructure through our CFO services, so leadership always has a clear, connected view of the numbers.

What Are the Top 3 Priorities for a CFO

The top 3 priorities for a CFO are maintaining healthy cash flow, improving profitability, and supporting strategic growth. Every other task a CFO handles, from budgeting to compliance to investor reporting, feeds into one of these three goals.

Cash flow always comes first because without it, the other two are impossible. A business cannot invest in growth or improve margins if it cannot make payroll or pay its vendors. According to data from the U.S. Bureau of Labor Statistics, about 20% of businesses fail in the first year and nearly 50% fail within five years. Cash flow problems are a factor in most of those failures.

Profitability is the second priority. A CFO looks at gross margins, operating expenses, and net income to find places where the business is leaking money. Even small improvements matter. Cutting unnecessary software subscriptions, renegotiating vendor contracts, or adjusting pricing by a few percentage points can add thousands of dollars to the bottom line every month.

Growth is the third priority, but only when cash flow and profitability support it. A CFO models the financial impact of every growth decision, whether it is hiring a new team member, opening a second location, or launching a new product line. They make sure the business can afford to grow without putting its cash position at risk. This kind of forward planning is central to what we do with business consulting clients who are scaling up.

What Is the Rule of 40 in Cash Flow

The Rule of 40 in cash flow is a benchmark used mainly by SaaS and technology companies to measure whether a business is balancing growth and profitability well. The formula is simple: add your revenue growth rate to your profit margin. If the total is 40 or higher, the company is in strong financial shape.

For example, if a company is growing revenue at 25% per year and has a 20% profit margin, its Rule of 40 score is 45. That is healthy. If a company is growing at 50% per year but losing 15% on margins, its score is 35. That tells the CFO to watch spending carefully because the growth is coming at the expense of profitability.

The Rule of 40 matters for cash flow because it forces business owners to think about growth and profitability at the same time, not one or the other. A CFO uses this metric to guide conversations about how fast to scale, when to invest, and when to pull back. According to industry benchmarks, companies that consistently score above 40 attract higher valuations and raise capital more easily because investors see them as efficient growers, not just fast growers.

How a CFO Uses Tax Planning to Protect Cash Flow

Tax planning is one of the most overlooked ways a CFO protects cash flow. Overpaying taxes, missing deductions, or getting hit with penalties all drain cash that the business could use for operations or growth.

A CFO works with your CPA to time income and expenses in a way that minimizes your tax burden legally. This includes accelerating deductions into the current year, deferring income when possible, taking advantage of tax credits like the Research and Development (R&D) credit, and making sure estimated tax payments are accurate so you do not overpay or underpay.

According to data from the IRS, underpayment penalties cost businesses millions of dollars every year. A CFO prevents that by tracking quarterly estimated payments and adjusting them based on actual income. They also evaluate whether your business entity type, such as an S-Corp, C-Corp, or LLC, is still the most tax-efficient structure as the company grows. A tax planning strategy that was right two years ago might not be right today, and a CFO keeps that under review.

For businesses here in Miami and across the country, we regularly see owners leave significant money on the table simply because nobody is looking at the full tax picture alongside the cash flow picture. A CFO connects both.

When Your Business Needs a CFO for Cash Flow Management

Your business needs a CFO for cash flow management when the financial complexity outgrows what a bookkeeper or owner can handle alone. There are several clear trigger points.

Revenue is growing but cash always feels tight. You are making money on paper but struggling to pay bills on time. Customers are paying late and nobody is following up systematically. You are about to hire employees, take on debt, or expand into a new market. You missed a tax deadline or got surprised by a large tax bill. You are preparing to raise capital from investors or apply for a business loan.

According to the Federal Reserve's Small Business Credit Survey, only 46% of small employer firms were profitable in 2024. Another 35% broke even, and 19% operated at a loss. Those numbers show that most small businesses are not generating enough cash to grow comfortably on their own. A CFO can often find the cash a business needs by fixing timing issues, cutting waste, and tightening collections, without raising prices or taking on debt.

You do not always need a full-time CFO. A fractional or virtual CFO gives you the same expertise on a part-time basis at a fraction of the cost. For many small and midsize businesses, this is the most efficient way to get senior-level financial leadership without the overhead of a full-time executive salary.

How a CFO Improves Cash Flow for Growing Companies

Growing companies face a specific cash flow challenge. Revenue goes up, but so do expenses, and expenses often arrive before the revenue does. This is called the growth trap, and a CFO is the person who keeps the business from falling into it.

When a company grows fast, it typically needs to hire more people, invest in equipment or technology, carry more inventory, and spend more on marketing. All of those costs hit the bank account immediately. But the revenue from those investments might take weeks or months to show up. A CFO manages that gap by building detailed cash flow projections that account for the timing difference between spending and earning.

According to the 2025 Small Business Credit Survey, 48% of small employer firms cite weak sales as a financial challenge, up from 44% the prior year. That means even companies that are investing in growth are not always seeing immediate returns. A CFO keeps the business from overextending during that in-between period by setting spending limits tied to actual cash, not projected revenue.

They also negotiate better payment terms with both customers and vendors. Getting customers to pay in 30 days instead of 60, or getting a supplier to extend your payment window from 15 days to 30, can free up tens of thousands of dollars in working capital. Those kinds of negotiations are a core part of what a CFO does every day.

Proper startup advisory work at the early stages can prevent most cash flow problems from developing in the first place. The earlier you build good financial habits, the easier it is to manage cash as the business scales.

Frequently Asked Questions

What Are the 5 C's in Finance

The 5 C's in finance are Character, Capacity, Capital, Collateral, and Conditions. Lenders use these five factors to evaluate whether a borrower is creditworthy. Character refers to the borrower's reputation and track record. Capacity measures their ability to repay based on income and existing debts. Capital is the borrower's personal investment in the business. Collateral is the asset backing the loan. Conditions cover the economic environment and the purpose of the loan.

What Are the Two Main Skills a CFO Needs

The two main skills a CFO needs are financial analysis and strategic communication. A CFO must be able to read complex financial data, spot trends, and build forecasts. But they also need to translate those numbers into plain language that the CEO, board members, and investors can understand and act on. According to McKinsey, today's CFOs spend more time on strategic advising than on traditional accounting tasks.

What Are the Top Ten CFO Responsibilities

The top ten CFO responsibilities are cash flow forecasting, budgeting, financial reporting, tax strategy, risk management, fundraising support, cost control, accounts receivable management, strategic planning, and investor relations. These responsibilities span both the day-to-day operations of the finance function and the long-term strategic direction of the company.

How Old Are CFOs Usually

CFOs are usually between 45 and 55 years old when they first take on the role, according to industry surveys. Most CFOs have at least 15 to 20 years of experience in finance or accounting before stepping into the position. That depth of experience is why their guidance on cash flow and financial strategy is so valuable.

What Is CFO Salary Per Month

A CFO salary per month in the United States is roughly $25,000 to $37,500 based on a median annual salary range of $300,000 to $450,000, according to Salary.com and Cowen Partners salary data for 2025. Total compensation including bonuses, equity, and benefits often pushes the monthly figure much higher, especially at larger companies.

How to Be an Excellent CFO

To be an excellent CFO, you need to combine deep financial knowledge with the ability to lead, communicate clearly, and think strategically. The best CFOs are not just good with numbers. They understand the business, anticipate problems before they happen, and present solutions that the leadership team can act on quickly. According to the Finance Alliance, top CFOs also invest in technology, automate routine tasks, and focus their time on high-impact decisions that affect cash flow and profitability.

What Is the 3-3-3 Rule in Marketing

The 3-3-3 rule in marketing says you have 3 seconds to grab attention, 3 minutes to deliver your message, and 30 minutes to follow up. It is a framework for creating content and campaigns that connect quickly with your audience. While this is a marketing concept, CFOs care about it because marketing spend directly affects cash flow. A CFO reviews marketing ROI to make sure every dollar spent on advertising is producing a measurable return.

The Takeaway

A CFO improves cash flow by building systems that give you clear visibility into your money, every week. From rolling forecasts and faster collections to smarter business formation decisions and disciplined expense management, a CFO turns financial guesswork into a plan you can trust. The data is clear. Businesses that manage cash flow proactively survive longer, grow faster, and make better decisions under pressure.

If your business is growing and cash still feels tight, or if you want to get ahead of cash flow problems before they start, we are here to help. At NR CPAs & Business Advisors, we work with businesses at every stage to build the financial clarity and structure that healthy cash flow requires. Reach out to our team at (954) 231-6613 to start the conversation.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

IRS CP14 Notice: Your First Bill For Unpaid Taxes

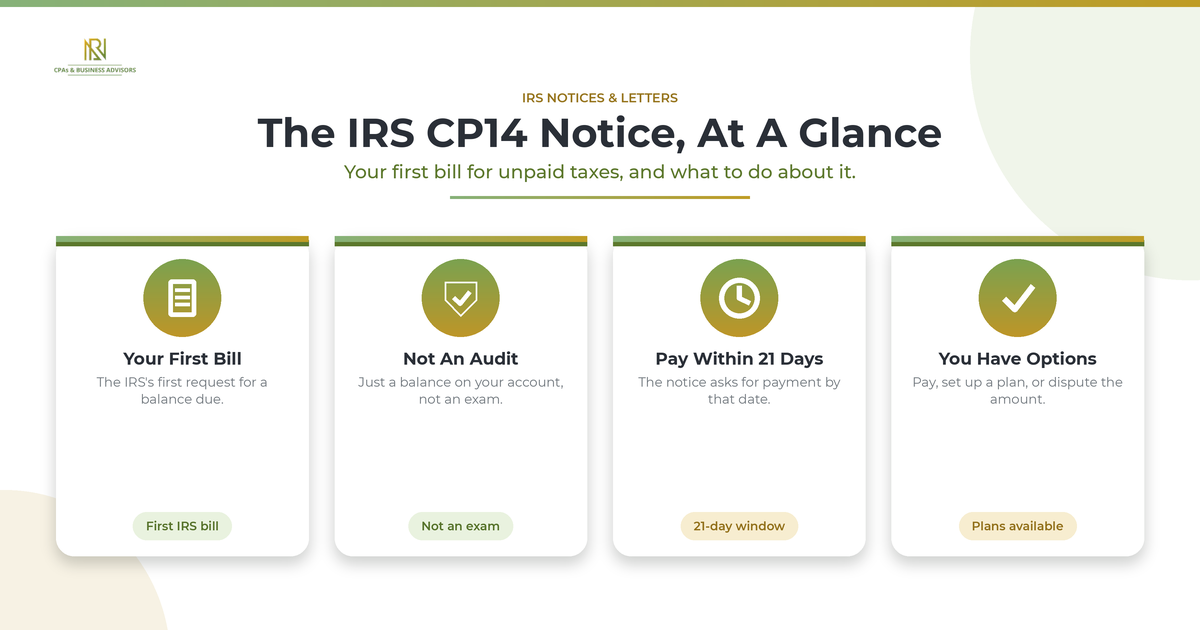

An IRS CP14 notice is the IRS's first bill, a letter telling you that you owe money on unpaid taxes and asking you to pay within 21 days. According to the IRS, it is not an audit; it means your return was processed and your account shows a balance due, including any interest and penalties. If you already paid, you may not owe anything, so it is worth verifying before you send a payment.

What Is An IRS CP14 Notice?

A CP14 is the IRS's first billing notice, formally the Notice of Tax Due and Demand for Payment, sent when your account shows an unpaid balance. According to the IRS, it is issued after your tax return is processed and the records show you owe money on unpaid taxes. The notice lays out the tax year, the amount you owe in tax, interest, and penalties, and a deadline to pay. Receiving one does not mean you are being audited or that a lien or levy has started. It is the opening step in resolving a balance, and the IRS sends millions of them each year.

Is A CP14 Notice Bad?

A CP14 is serious but routine, and it is fixable. It is the IRS's standard first request for payment, not a penalty notice in itself and not a sign of an audit, though the balance it shows can include penalties and interest on top of the tax. What matters is acting on it rather than ignoring it, because the amount only grows while it sits. Handled promptly, most CP14 balances are straightforward to pay or dispute.

Why Did You Get A CP14 Notice?

You received a CP14 because the IRS processed a return showing a balance due that was not paid in full by the deadline. According to the IRS, the two basic triggers are filing a return with a balance due and not paying the taxes owed by the due date. Common underlying causes include underpaid estimated taxes, an extension that postponed your filing date but not your payment due date, or a balance left after the IRS adjusted your return. Sometimes it is simply a timing issue, where you paid but the payment had not yet posted to your account when the notice was generated.

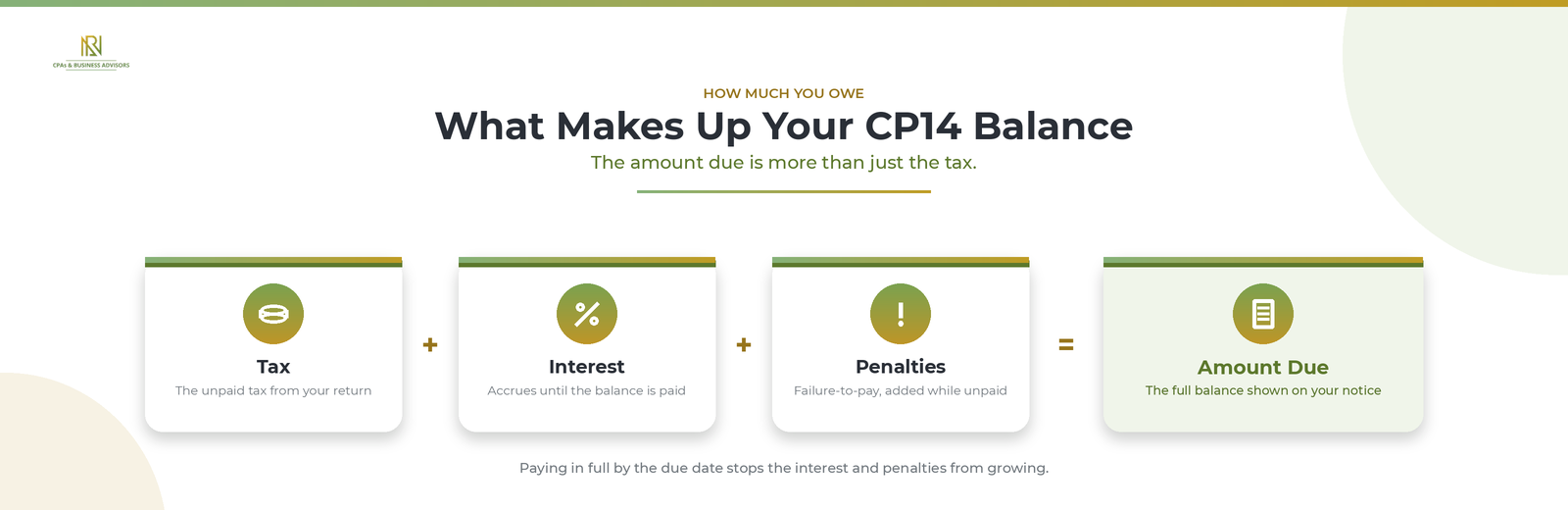

How Much You Owe And When It's Due

The CP14 shows your full balance, tax plus interest and penalties, and asks you to pay within 21 days of the notice date. According to the IRS, interest accrues on the unpaid amount and a failure-to-pay penalty is added while the balance goes unpaid, so paying in full by the date on the notice stops further interest and penalties from building. The Taxpayer Advocate Service notes that if the balance is not fully paid within about 60 days, the IRS can move forward with collection. The 21-day request is the window to act, not a hard cutoff after which nothing else happens.

What If You Already Paid?

If you already paid in full, don't pay again; verify your account first, because the IRS has acknowledged sending CP14 notices in error. According to the IRS, some taxpayers who paid on time, electronically or by check, received a CP14 because the payment had not finished processing or posted with an error, and it advised those taxpayers not to respond or pay a second time while it corrects the accounts, with penalties and interest adjusted automatically once the payment is applied. To confirm where you stand, sign in to your IRS Online Account and review your tax account transcript, checking that each payment posted to the right year and amount. A misapplied payment, a still-processing amended return, or an estimated payment credited to the wrong period are common reasons a balance shows when you don't actually owe it. If your records don't match the notice, dispute it in writing to the address on the notice, including your name, the tax year, and copies of your proof such as cancelled checks or payment confirmations, and keep your originals.

How To Pay Your CP14

If the amount is correct, the fastest resolution is to pay it. According to the IRS, you can pay online, and paying by the due date on the notice limits the interest and penalties you owe. Include the notice's reference details with your payment so it is applied to the right year, and keep a record of the confirmation. Paying the full balance closes the notice; if you can't pay all of it, you still have options.

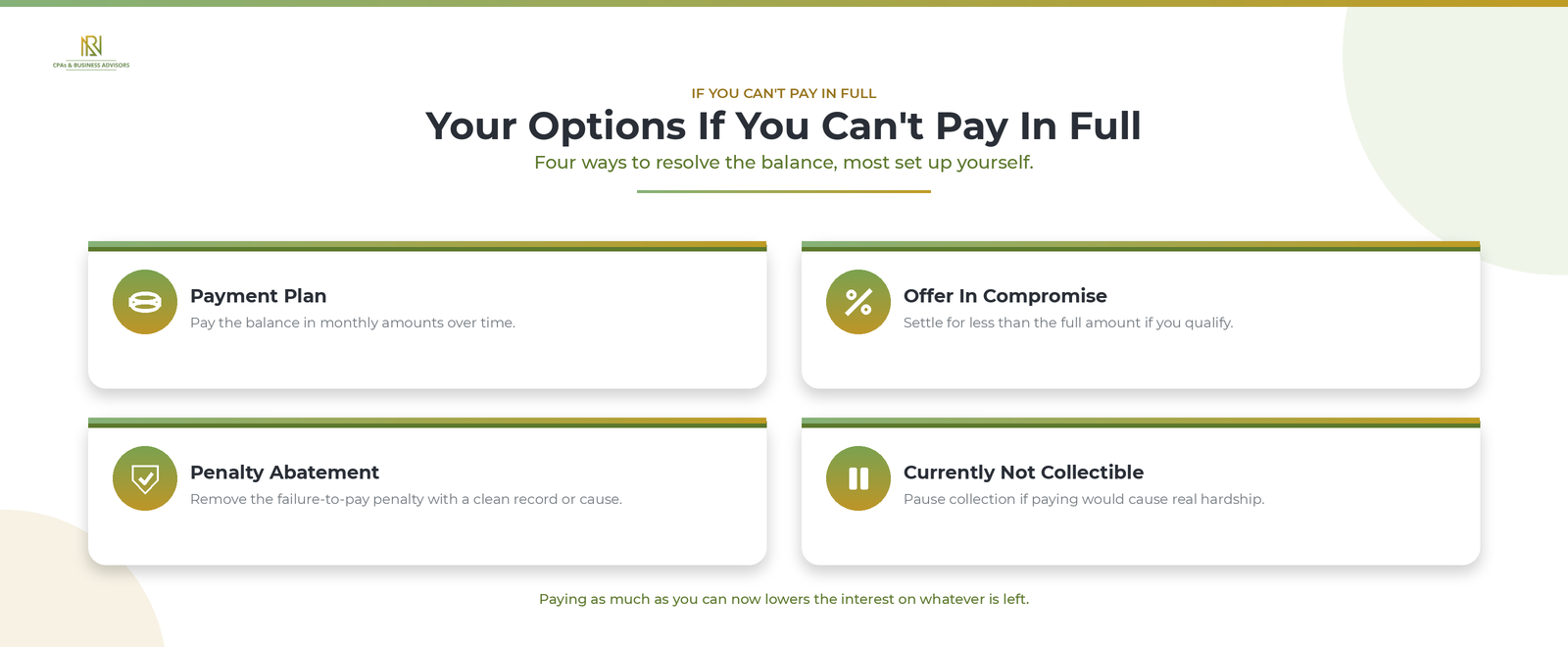

What If You Can't Pay In Full?

If you can't pay the whole balance, you have several options, and you can set most of them up yourself. According to the IRS, the main paths are:

- A payment plan, or installment agreement, that lets you pay the balance in monthly amounts over time, available online for many individual balances.

- An offer in compromise, which settles the debt for less than the full amount when you qualify.

- First-time penalty abatement or reasonable-cause relief, which can remove the failure-to-pay penalty if you have a clean recent history or a valid reason.

- A temporary delay of collection, sometimes called currently not collectible status, if paying would create real hardship.

Even if you choose a plan, paying as much as you can now reduces the interest that keeps accruing on the remaining balance. Setting up an installment agreement with your response also signals to the IRS that you intend to resolve the balance.

What Happens If You Ignore A CP14 Notice?

Ignoring a CP14 doesn't stop the balance; it grows the debt and moves you toward collection. According to the IRS, interest and the failure-to-pay penalty keep accruing on the unpaid amount, and if you don't resolve the balance the account advances through further notices demanding payment. Left unaddressed, that path leads to enforced collection, which can include a federal tax lien or a levy on wages or bank accounts. Because the CP14 is the first and easiest point to deal with the balance, responding now, by paying, arranging a plan, or disputing it, is far cheaper than waiting.

Should You Handle It Yourself Or Get Help?

You can handle most CP14 notices yourself, especially when the balance is correct and you can pay or set up a plan online. According to the IRS, you can resolve a debt and manage your account without calling. Consider professional help when the balance is large, when you believe the notice is wrong and need to build a documented dispute, or when paying would cause hardship. A CPA or enrolled agent can pull your transcripts, verify the amount, and deal with the IRS for you, and a firm offering IRS tax resolution services can manage the response end to end. If cost is a barrier, a Low Income Taxpayer Clinic may help for free or a small fee. Either way, if you're not sure what your letter is asking, start with our overview of the general steps for any IRS letter.

Frequently Asked Questions

What is a CP14 notice? It is the IRS's first bill, telling you that you owe money on unpaid taxes and asking for payment within 21 days.

Is a CP14 notice bad? It is serious but routine and fixable. It is not an audit, and acting on it promptly keeps interest and penalties from growing.

How do I respond to a CP14 notice? Verify the balance against your records, then pay it, set up a payment plan if you can't pay in full, or dispute it in writing if the amount is wrong.

Is notice CP14 a civil penalty? No. The CP14 is a demand for payment of tax you owe, though the balance can include penalties and interest in addition to the tax.

What if I paid my taxes but received a CP14? Don't pay twice. Check your IRS account to confirm the payment posted, and if you paid in full and on time, the IRS has said affected taxpayers should not respond while it corrects the account.

A CP14 notice is the IRS letting you know about a balance and asking you to settle it, not a penalty or an audit. Confirm the amount is right, pay it or arrange a plan if it is, and dispute it with proof if it isn't. Dealt with inside the window it gives you, a CP14 is one of the simpler IRS notices to put behind you.

What to Do When You Receive an IRS Notice?

If you receive an IRS notice, don't panic. Read it carefully, find the notice number to see what it is about, check the deadline, and then either follow the instructions to respond or get a tax professional to help. Most IRS letters deal with one specific issue and are straightforward to handle once you know what they are asking for.

First, Don't Panic (And Don't Ignore It)

A letter from the IRS rarely means trouble, but you should never ignore it. According to the IRS, it sends notices for routine reasons, such as a balance due, a changed refund, or a simple question about your return, and most are resolved by reading the letter and taking the step it asks for. What you cannot do is set it aside. Acting promptly limits interest and penalties, and many notices carry a firm deadline. The calm, timely response is almost always the cheapest one.

Why Did The IRS Send You A Notice?

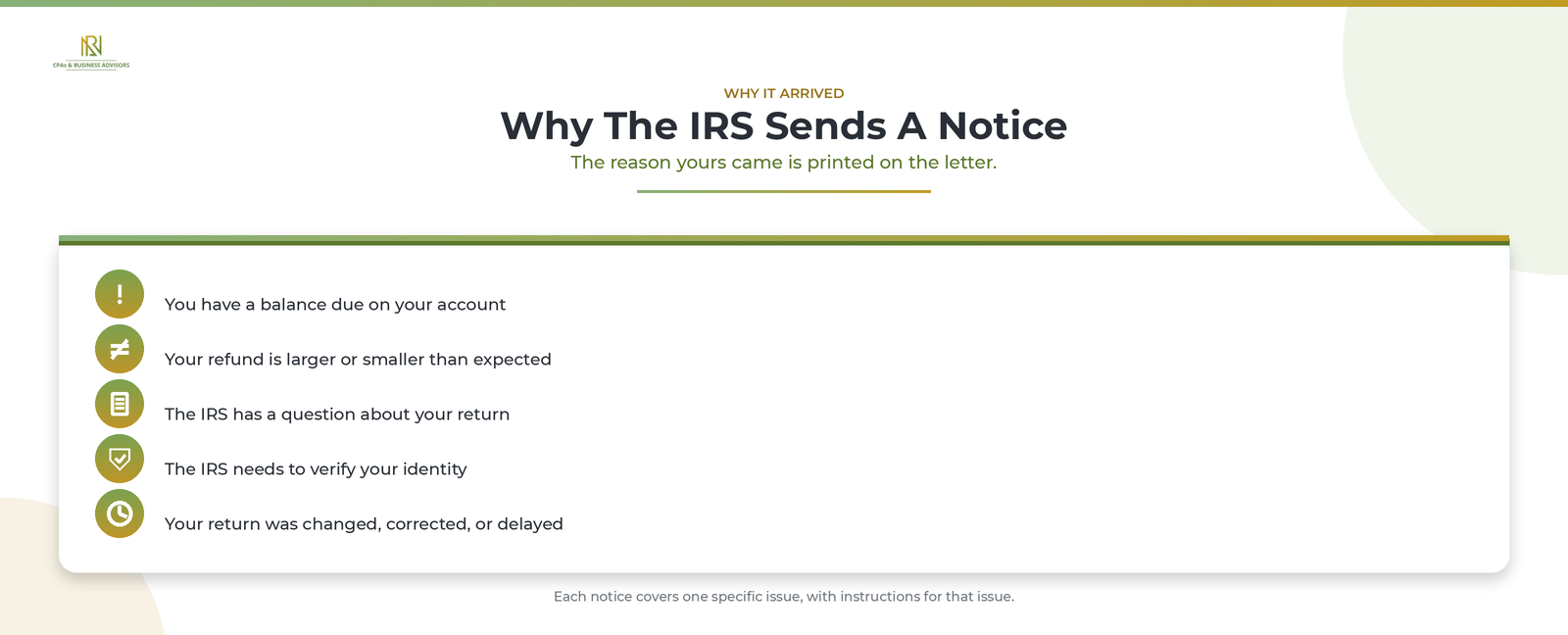

The IRS contacts you when something on your account or return needs attention. According to the IRS, the most common reasons are:

- You have a balance due.

- Your refund is larger or smaller than you expected.

- The IRS has a question about your return or needs to verify your identity.

- The IRS changed or corrected your return.

- Your return is delayed in processing.

Each notice covers one specific issue and includes instructions for that issue, so the reason yours arrived is stated right on the letter.

What To Do When You Receive An IRS Notice

Work through the notice in order: read it, identify it, verify it, compare it to your return, note the deadline, respond, and keep a copy. According to the IRS, these steps handle the large majority of letters without a phone call or an office visit:

- Read the entire notice carefully to understand the issue and the action it asks for.

- Find the notice or letter number in the top right corner, such as CP14 or CP2000, and look it up on IRS.gov for a plain-English explanation.

- Verify the notice is genuine before you act or pay anything.

- Compare the notice against your tax return, and check which tax year it covers rather than assuming it is your most recent one.

- Note the response deadline and put it somewhere you will not miss it.

- Respond the way the notice tells you to, and only if it asks you to.

- Keep the notice and a copy of your response with your tax records.

The sections below cover the steps that trip people up most.

How To Tell If The Notice Is Real

A genuine IRS notice arrives by mail, never by text, email, or social media. According to the IRS, its first contact comes through the U.S. Postal Service, and it will never use social media or a text message to ask for personal or financial information. To confirm a letter is real, search the notice number on IRS.gov, where every notice is described. If the letter does not show up in that search or looks suspicious, call the IRS at 800-829-1040 and follow the representative's instructions rather than any contact details printed on a questionable letter.

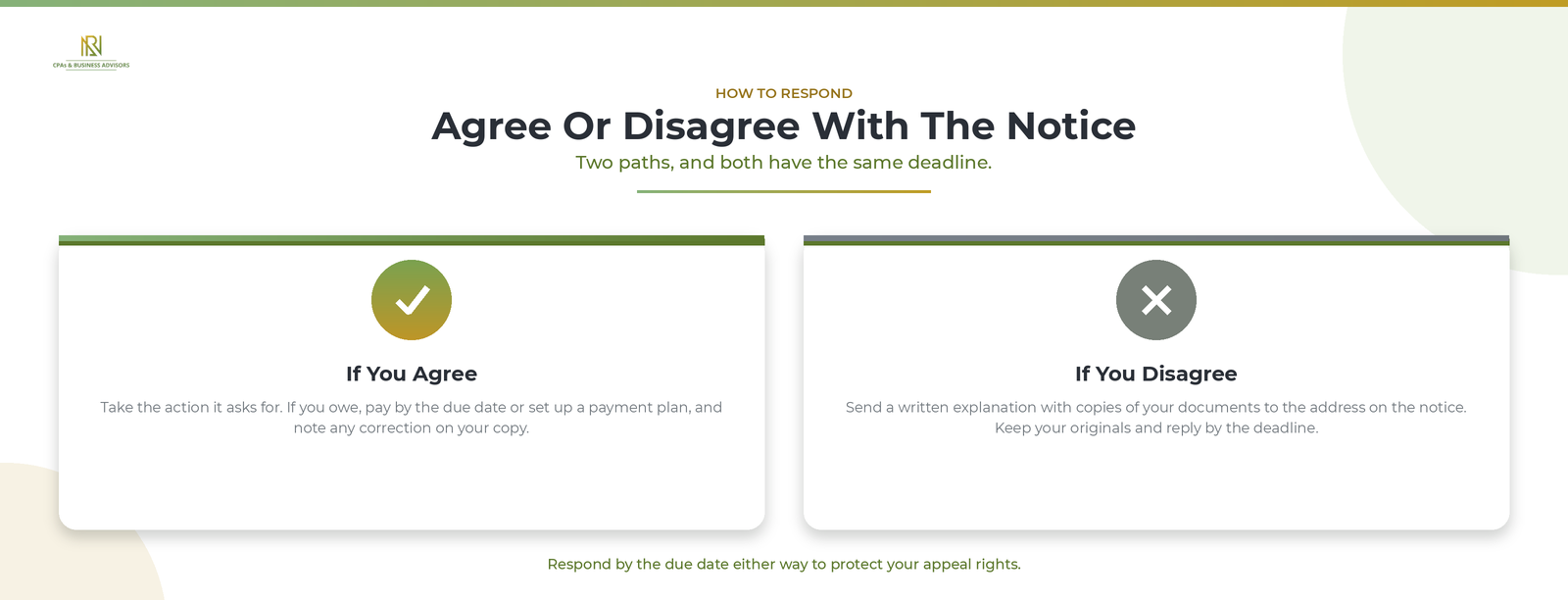

If You Agree With The Notice

If the notice is correct, simply do what it asks. According to the IRS, that usually means taking the requested action and, if you owe, paying by the due date to reduce interest and penalties. If you cannot pay in full, you can arrange to pay the balance over time and still send what you can now, writing the notice's reference number on your payment so the IRS applies it correctly. If the notice corrected your return and you agree, note the change on your own copy and keep it.

If You Disagree With The Notice

If you don't agree, you must respond by the deadline with a written explanation and proof. According to the IRS, you follow the dispute instructions on the notice, send a letter explaining why you disagree, and include copies of any documents that support your position, mailed to the address on the notice. Send copies and keep your originals, and allow at least 30 days for the IRS to reply. Responding by the due date is also what protects your right to appeal later.

How Long Do You Have To Respond?

Most IRS notices give you about 30 days to respond, though the exact window is printed on the letter and varies by notice type. According to the IRS, you should act by the due date shown, because replying on time both limits added interest and penalties and guarantees your appeal rights. If you need more time, call the number in the top right corner of the notice before the deadline passes.

What Happens If You Ignore An IRS Notice?

Ignoring a notice doesn't make it go away; it makes the problem larger. According to the IRS, when you don't respond, interest and penalties keep building and the IRS moves ahead with whatever the letter proposed, which can mean assessing tax you might have disputed or starting collection on a balance. Some letters carry legal deadlines, and missing them costs you options, such as the chance to take a disputed amount to the U.S. Tax Court. Whatever the notice, the safe move is to respond within the window it gives you. If yours is a specific letter like a CP2000 underreported income notice or a CP14 balance due notice, follow the steps for that notice in particular.

Should You Handle It Yourself Or Get Help?

You can resolve most IRS notices on your own, especially simple ones where you agree and just need to pay or send a document. According to the IRS, the majority of correspondence can be handled without calling or visiting an office. Bring in a professional when the amount is large, when you disagree and need to build a documented case, or when the letter signals an examination. A CPA, enrolled agent, or tax attorney can deal with the IRS for you, and a firm offering IRS tax resolution services can manage the whole response. If cost is a concern, a Low Income Taxpayer Clinic may be able to represent you for free or a small fee.

Can You View IRS Notices Online?

Yes, you can see many IRS notices in your online account. According to the IRS, you can view digital copies of select notices and even go paperless for certain letters by signing in to your IRS Online Account. That is also a useful way to confirm a balance or check that a payment has been applied before you respond to a notice about it.

Frequently Asked Questions

How do I respond to an IRS notice? Follow the instructions printed on the notice, and reply only if it asks you to, using the response form or the address provided, within the deadline.

Why would the IRS send me a notice? Usually because you have a balance due, your refund changed, the IRS has a question about your return, or it corrected something on your account.

How long do I have to respond to an IRS notice? Typically about 30 days, but the exact deadline is on the letter and depends on the notice type.

What happens if I ignore an IRS notice? Interest and penalties grow, the IRS proceeds with its proposed change or collection, and you can lose the right to dispute the amount.

Do I need to call the IRS? Usually not. Reply only if the notice instructs you to, and if you must call, use the number in the top right corner with your return and the letter in hand.

An IRS notice is a request to handle one specific thing, not a reason to dread the mailbox. Read it, confirm what it is and that it is genuine, mark the deadline, and respond the way it asks, or hand it to a professional if it is complex. Taken in order and on time, almost every IRS letter is far easier to resolve than it first looks.