%201.avif)

.png)

.png)

Virtual CFO for Restaurant Businesses

A virtual CFO for restaurant businesses gives owners senior financial leadership on a part-time, remote basis at a fraction of the cost of a full-time hire. The role covers cash flow forecasting, food and labor cost control, profit margin analysis, tax planning, and the strategic decisions that keep a restaurant alive in an industry where most businesses run on a 3 to 5% net margin. For independent restaurants and small groups, a virtual CFO is often the difference between scraping by and actually growing.

In this article, we cover what a virtual CFO actually does for a restaurant, how the role differs from a traditional CFO, what it costs, whether outsourcing makes sense, the real restaurant failure data, and when your operation is ready for this kind of financial support.

What Is a Virtual CFO for Restaurant Businesses

A virtual CFO for restaurant businesses is an experienced chief financial officer who works with restaurant operators remotely, on a part-time or fractional schedule, instead of as a full-time in-house executive. The work is identical to what a full-time CFO would do, including cash flow management, financial planning, reporting, and strategic guidance. The difference is the engagement structure, which gives restaurants senior expertise without the six-figure salary commitment.

The restaurant industry is enormous and tight on margins, which is why this model has caught on. According to the National Restaurant Association 2025 State of the Restaurant Industry report, the U.S. restaurant and foodservice industry is projected to reach $1.5 trillion in sales in 2025, with traditional restaurants alone generating over $1.1 trillion. That same report shows the industry employs nearly 15.9 million people, making it the second largest private employer in the country. With that level of activity and competition, restaurant operators cannot afford to manage their finances on guesswork.

Yet most restaurants do exactly that. Profit margins in the industry typically run between 3 and 5%, according to data from Toast and the New York University Stern School of Business. According to ContinuServe research, 82% of restaurant failures could have been prevented with better financial management. A virtual CFO closes the gap by giving the owner the same financial discipline a $400,000-a-year executive would bring, but at a price point a $1 million to $20 million restaurant can actually afford.

What Does a Virtual CFO Do for Restaurants

A virtual CFO for a restaurant does cash flow forecasting, food and labor cost analysis, menu profitability reviews, financial reporting, vendor and lease negotiations, tax planning oversight, and strategic planning for expansion. Every one of those activities ties back to one goal: protecting the thin margins that keep a restaurant in business.

According to the National Restaurant Association, 38% of operators say recruiting and retaining employees is their top challenge in 2025, while rising food costs and labor expenses continue to squeeze profitability. A virtual CFO helps the owner stay ahead of those pressures by watching the numbers daily and adjusting before small problems turn into closures. Restaurants that work with us get this exact kind of structured oversight, plugged into our broader restaurant accounting framework.

Cash Flow Management for Restaurants

Cash flow management for restaurants is the most critical service a virtual CFO delivers, because restaurants live and die by daily cash movement. Food, labor, rent, and utilities all hit the bank account on different cycles than the revenue they support, creating a constant timing puzzle that an experienced CFO knows how to solve.

According to a U.S. Bank study widely cited in small business research, 82% of small businesses that fail do so because of poor cash flow management. For restaurants, that number is even more relevant because revenue can swing 20 to 40% week to week based on weather, seasonality, and local events. A virtual CFO builds a rolling 13-week cash flow forecast that gets updated weekly, so the owner always knows what is coming in, what is going out, and where any gaps will appear. The same kind of cash flow discipline that protects larger companies is exactly what keeps a restaurant alive through slow months.

Food and Labor Cost Control

Food and labor are the two biggest expenses in any restaurant, and together they form what the industry calls prime cost. According to ContinuServe research, prime cost should stay within 60 to 65% of revenue for a restaurant to remain profitable. Food cost should run between 28 and 35% of revenue, and labor should stay below 30%. When either of those numbers slips, profitability collapses fast.

A virtual CFO tracks these numbers weekly. They review food cost by category, identify waste and over-ordering, analyze portion sizing against menu pricing, and flag any vendor who has quietly raised prices. According to industry estimates cited in Restroworks research, restaurants waste 30 to 40% of their food inventory, which is one of the fastest ways to destroy margin without realizing it. On the labor side, the CFO tracks scheduling efficiency, overtime patterns, and labor cost as a percentage of sales by shift and by day part. Building this kind of weekly review rhythm into the operation is a core part of our restaurant bookkeeping approach for every client.

Menu Profitability and Margin Analysis

Not every menu item makes money equally. A virtual CFO runs menu engineering analysis to identify which dishes drive the most profit, which are loss leaders, and which need to be repriced or removed. According to Toast research, restaurants that conduct quarterly menu profitability reviews see margin improvements of 2 to 5 percentage points within the first year, which is a massive gain in an industry where the average net margin is only 3 to 5%.

This work goes deeper than just looking at the most popular items. The CFO breaks down food cost per dish, labor time per dish, and contribution margin to find the items that are quietly draining profit even when they sell well. We pair this analysis with structured financial statements so the owner can see the full picture month over month.

Tax Strategy and Compliance Oversight

Restaurants face a tax landscape most other small businesses do not, including sales tax, tip reporting, payroll taxes, FICA tip credit eligibility, depreciation on equipment, and complex compliance around employee meals. A virtual CFO works alongside the tax preparer to time income and expenses, accelerate depreciation where it helps, and capture every credit the business is entitled to. According to the IRS, the FICA tip credit alone saves eligible food and beverage establishments thousands of dollars per year by offsetting the employer's share of Social Security and Medicare taxes paid on reported tips.

Proactive tax planning for restaurants often pays for the entire CFO engagement on its own. Catching a missed credit, avoiding an underpayment penalty, or shifting a major equipment purchase into the right tax year can mean the difference between writing a check to the IRS and getting one back.

What Is the Difference Between a CFO and a Virtual CFO

The difference between a CFO and a virtual CFO is the engagement model, not the expertise. A traditional CFO is a full-time in-house executive who sits in the office, attends every leadership meeting, and manages an internal finance team. A virtual CFO provides the same strategic guidance, financial planning, and decision support, but on a part-time, remote, or project basis.

For restaurant operators, the virtual model usually makes more sense. According to Salary.com data for 2025, a full-time CFO in the United States earns a median base salary of $437,000, with total compensation often exceeding $500,000 once benefits, bonuses, and equity are factored in. A restaurant generating $2 million to $10 million in annual revenue and running on a 4% net margin simply cannot absorb that kind of fixed overhead. According to Business Research Insights, the global virtual CFO market was valued at roughly $3.91 billion in 2024 and is projected to reach $8.17 billion by 2032, growing at a compound annual rate of 9.6%. Restaurants and other margin-sensitive businesses are a major part of that growth.

The work itself looks the same. A virtual CFO reviews monthly financials, leads quarterly planning sessions, builds cash flow forecasts, prepares lender or investor packages, and supports major decisions like opening new locations or restructuring debt. Modern cloud-based accounting tools like QuickBooks Online, Restaurant365, and Toast Connect mean a virtual CFO has the same visibility into your numbers as someone sitting in the back office.

Is a Fractional CFO Worth It for a Restaurant

Yes, a fractional CFO is worth it for most restaurants doing more than $1 million in annual revenue. The return on investment typically shows up within three to six months through better food cost control, smarter scheduling, faster collections, lower taxes, and avoided mistakes that would have cost far more than the engagement fee.

According to an industry pricing survey from Eagle Rock CFO, growing companies see a 3 to 10 times return on their fractional CFO investment, often paying for the engagement within the first two quarters. For restaurants specifically, even a 1% improvement in prime cost on a $3 million operation puts $30,000 back on the bottom line each year, which usually exceeds the entire annual cost of a part-time CFO. A fractional CFO often finds margin gains far larger than that within the first 90 days.

The model also fits how restaurants actually operate. A restaurant does not need a CFO sitting in a back office 40 hours a week. It needs someone who reviews weekly numbers, runs monthly close, leads a quarterly planning session, and is available by phone or email when a big decision comes up. That is exactly what 10 to 30 hours of monthly fractional CFO support delivers, at 60 to 80% less than the cost of a full-time hire.

Can You Outsource a CFO

Yes, you can outsource a CFO. Outsourcing a CFO means hiring an external financial executive or firm to handle strategic financial leadership on a part-time, remote, or project basis. For restaurants, this is now the most common way to get senior financial guidance because cloud-based accounting and POS systems make remote financial management as effective as in-person work.

According to Deloitte's 2024 Global Outsourcing Survey, 80% of executives plan to maintain or increase their outsourcing investment over the next 12 months. Another study from Mordor Intelligence found the global finance and accounting outsourcing market reached $54.79 billion in 2025 and is projected to grow to $85.92 billion by 2031. That growth is being fueled by businesses that want senior financial expertise without the cost and rigidity of a full-time hire.

The key to a successful outsourced CFO relationship is a structured engagement with clear deliverables. The best arrangements include weekly cash flow check-ins, monthly financial close reviews, quarterly strategic planning sessions, and on-call support for time-sensitive decisions. When those elements are in place, outsourcing performs just as well as an in-house hire, and often better, because the outsourced CFO brings cross-industry experience to the table. Many restaurant clients combine this with structured business consulting to tackle operational issues that show up alongside financial ones.

How Much Does a Virtual CFO Cost

A virtual CFO costs between $2,000 and $15,000 per month for fractional or part-time engagements, depending on the size of the restaurant, the scope of work, and the experience of the CFO. According to a 2025 pricing survey from Eagle Rock CFO, most growing companies pay between $4,000 and $8,000 per month for ongoing CFO support.

For restaurants specifically, pricing usually breaks down by business size. A single-location independent doing $1 million to $3 million in revenue typically pays $2,000 to $5,000 per month for 8 to 15 hours of CFO support. A multi-location operator or growing concept doing $3 million to $10 million usually pays $5,000 to $10,000 per month for 20 to 30 hours. Larger restaurant groups with several locations or rapid growth plans can pay $10,000 to $15,000 monthly for more comprehensive engagement.

Compare those numbers to a full-time CFO. According to 2025 salary data from Cowen Partners and Salary.com, total compensation for a full-time CFO at a growing private company ranges from $300,000 to $500,000 per year, with benefits and equity pushing the package even higher. According to K38 Consulting research, businesses that switch from full-time to fractional save 60 to 80% on their finance leadership costs without sacrificing strategic value. For a restaurant, that savings can fund an entire kitchen renovation or marketing campaign in a single year.

What Is the Hourly Rate for a CFO

The hourly rate for a CFO ranges from $175 to $450 per hour in 2025 for fractional or virtual engagements, according to multiple industry pricing surveys. Most experienced fractional CFOs serving restaurants charge between $200 and $350 per hour, with rates climbing higher for restaurant industry specialists or work tied to major events like new location openings or refinancing.

According to research published by Bennett Financials, entry-level fractional CFOs charge $150 to $250 per hour, mid-level CFOs charge $250 to $400 per hour, and senior CFOs with deep industry expertise charge $400 to $600 per hour. For comparison, the equivalent hourly rate for a full-time CFO earning a $437,000 base salary is roughly $210 per hour, based on a 2,080-hour work year, according to Salary.com. That number ignores benefits, equity, payroll taxes, and recruiting costs, which add 30 to 40% on top.

The hourly rate is less important than the total monthly cost and the results delivered. A $300 per hour CFO working 15 hours per month costs $4,500. If that CFO improves food cost by 1.5 percentage points on a $3 million restaurant, the annual savings reach $45,000, which is more than the entire year of CFO fees. Looking at it this way, the question is not whether the rate is high. The question is whether the return covers the cost, and for restaurants, it almost always does.

What Percentage of Restaurants Fail in 5 Years

Approximately 50% of restaurants fail within 5 years of opening, according to multiple industry sources including the National Restaurant Association and Restroworks research. The 10-year survival rate is about 35%, meaning roughly two out of every three restaurants close within a decade.

The myth that 90% of restaurants fail in their first year is not accurate. According to Restroworks data, only 17 to 30% of restaurants close in their first year, not 90%. Datassential, which actually tracks restaurant closures from review sites, reported a first-year failure rate as low as 0.9% in 2025, the lowest since at least 2018. That said, the long-term picture is still tough. Independent restaurants struggle the most because they lack the brand recognition, supply chain efficiency, and operational systems of larger chains. According to NOVA research, individual independent outlets experience an average failure rate of 17%, while franchised operations have far better survival odds.

The single biggest reason restaurants fail is poor financial management, not bad food or weak concepts. According to ContinuServe research, 82% of restaurant failures could have been prevented with better financial systems. A virtual CFO addresses the root causes head on. They build cash flow forecasts that prevent payroll surprises, monitor prime cost weekly so margin slippage gets caught early, analyze menu profitability so the right items are pushed, and watch the financial trends that signal trouble before it becomes terminal. According to Datassential analysis, restaurants with stronger cost control and margin analysis tools survive at materially higher rates than those without.

Is a Digital CFO Better Than a Traditional CFO

A digital CFO is better than a traditional CFO for most growing restaurants because the role combines financial expertise with cloud-based accounting tools, real-time dashboards, and remote collaboration. A traditional CFO still works on Excel exports and in-person meetings, while a digital CFO uses live data from your POS, accounting platform, and payroll system to make decisions in real time.

For restaurants, this matters a lot. Restaurant data moves fast. Sales by hour, food cost by category, labor by shift, and tip distributions all change daily. A digital CFO connects these data sources into dashboards that update automatically, so decisions are made on numbers from yesterday or last week instead of waiting for month-end close. According to a 2025 Gartner CFO survey, AI adoption in finance functions has nearly doubled in two years, and 82% of finance leaders say accelerating the close process is a top operational goal.

That said, technology is only as good as the financial judgment behind it. The best results come from a digital CFO who combines real-time data tools with deep experience in restaurant operations, tax law, and strategic planning. We work this way with every restaurant client, pairing cloud-based reporting with hands-on strategic planning so the data actually drives smart decisions.

Restaurant Financial KPIs a Virtual CFO Tracks

The restaurant financial KPIs a virtual CFO tracks every week are prime cost, food cost percentage, labor cost percentage, gross margin, sales per labor hour, average ticket, and cash flow. Each one tells the owner something specific about the health of the business, and together they make up the financial dashboard that drives every operational decision.

Prime cost is the headline number. According to ContinuServe research, prime cost should stay between 60 and 65% of revenue. Anything above 70% signals a serious margin problem that needs immediate attention. Food cost percentage usually runs 28 to 35%, depending on concept and pricing strategy. Labor cost percentage typically runs 25 to 32%, with quick-service restaurants lower and full-service restaurants higher. According to industry data from Toast and Square, top-performing quick-service restaurants achieve EBITDA margins of around 18 to 19%, while fast-casual restaurants average 21 to 23%, both well above the 3 to 5% net margin of typical independent full-service operations.

Beyond cost percentages, a virtual CFO tracks sales per labor hour to measure productivity, average ticket size to spot pricing or upsell issues, and weekly cash position to make sure payroll and vendor obligations can be met. According to a Q4 2025 OnDeck and Ocrolus survey, 29% of small business owners rank cash flow as their top concern, second only to inflation. For restaurants, that ranking is usually even higher because of the daily cash cycle.

Virtual CFO vs Other Financial Support for Restaurants

Restaurant owners often weigh several options for financial support, including a full-time CFO, a virtual or fractional CFO, a CPA firm, or a bookkeeper. Each fits a different stage and budget. The table below compares the key factors that matter most to a restaurant operator.

Support OptionTypical Annual CostStrategic DepthBest ForFull-Time CFO$300,000 to $500,000+Very high, in-house dailyRestaurant groups over $30M revenueVirtual or Fractional CFO$24,000 to $120,000High, strategic focusRestaurants $1M to $30MCPA Firm$5,000 to $25,000Moderate, tax and complianceEstablished small restaurantsBookkeeper$3,000 to $15,000Low, transaction recordingBrand-new or single-location

Sources: Salary.com 2025 CFO compensation data, Cowen Partners Executive Search 2025, Eagle Rock CFO 2025 pricing survey, K38 Consulting 2025 fractional CFO guide, Graphite Financial 2025 hourly rate data.

When a Restaurant Should Hire a Virtual CFO

A restaurant should hire a virtual CFO when financial complexity outgrows what the owner or a bookkeeper can manage alone. The most common triggers are crossing $1 million in annual revenue, opening a second location, applying for a business loan, considering an investor, or seeing revenue grow without profit keeping pace.

Specific signs we see often include prime cost creeping above 65% with no clear cause, payroll feeling tight even on weeks that looked strong on the POS, vendor invoices stacking up while cash sits in receivables, an upcoming lease renewal or new location decision, a surprise tax bill, or an offer to buy the business that requires clean financials. According to the Federal Reserve's 2025 Small Business Credit Survey, only 46% of small employer firms were profitable in 2024, with 35% breaking even and 19% operating at a loss. Restaurants tend to skew toward the bottom half of that range because of their thin margins.

Restaurants also benefit from CFO support during expansion. According to the National Restaurant Association, 29% of operators plan to open new locations in 2025. Opening a second or third location adds enormous financial complexity, including new leases, equipment financing, additional payroll, and the cash drain of a ramp-up period. A virtual CFO builds the financial model for the new site, manages the timing of capital outlays, and tracks the new location against its targets so the owner knows quickly whether the expansion is working. We pair this with structured business formation guidance for owners who are setting up new entities for additional locations.

How a Virtual CFO Helps Restaurants Open New Locations

A virtual CFO helps restaurants open new locations by building the financial model for the expansion, securing the right financing, managing the buildout budget, and tracking the new site against performance targets after opening. Each of these steps has a specific deliverable, and getting any of them wrong can sink the whole project.

The financial model is the starting point. The CFO builds projections for the new location based on market data, comparable units, and realistic ramp-up timelines. According to industry research from Restroworks, most new restaurants take 6 to 18 months to reach break-even, and some take up to 3 years. The CFO bakes that timeline into the cash flow plan so the operator does not run out of capital before the new location is profitable.

The financing side comes next. A virtual CFO prepares the financial package that banks and SBA lenders want to see, including three to five years of historical financials, projections for the new site, personal financial statements for the guarantor, and a clear use-of-funds breakdown. With a well-prepared package, restaurants are far more likely to get approved at favorable terms. After opening, the CFO tracks the new location against the projections weekly, flagging any variance early so adjustments can be made before small problems compound.

How a Virtual CFO Manages Restaurant Cash Flow

A virtual CFO manages restaurant cash flow by building a rolling 13-week forecast, monitoring daily sales and bank balances, timing vendor payments strategically, watching credit card processing deposits, and building reserves for slow weeks. The forecast is the central tool, and it gets updated every Monday morning so the owner always sees the next 90 days clearly.

Restaurants also face unique cash flow timing issues. Credit card processors typically hold funds for 1 to 3 business days, payroll runs every two weeks regardless of sales, food vendors usually want payment within 7 to 30 days, and rent is due on the first of every month. We see this firsthand with restaurant clients in Miami and across the country, where the same operator who looks profitable on the P&L can still struggle to make payroll if cash timing is not actively managed. According to a 2025 OnDeck and Ocrolus survey, 47% of small businesses are actively building cash reserves as protection against uncertainty. For restaurants, the recommended reserve is at least four to six weeks of operating expenses, which is enough to cover payroll and rent during a weather event, a remodel, or a slow seasonal period.

A virtual CFO also tightens vendor payment terms where possible. Negotiating Net 30 instead of Net 15 with a major food supplier can free up tens of thousands of dollars in working capital. On the receivable side, catering invoices and corporate accounts often have payment delays that need to be managed. According to Gitnux research, 61% of small businesses report cash flow issues caused by late payments, and a CFO addresses that with clear credit terms and automated follow-up. Our CFO services for restaurant clients build all of this into a single, organized monthly rhythm.

What a Restaurant Owner Can Expect Each Month

What a restaurant owner can expect each month from a virtual CFO is a clean monthly financial close, a 60 to 90 minute review meeting walking through the prior month's results, an updated 13-week cash forecast, a KPI dashboard showing prime cost and other key metrics, and a list of action items for the coming month.

The monthly meeting covers what changed, what is working, and what needs attention. The CFO points out where food cost moved, why labor came in above or below target, which menu items drove the most profit, and what the cash position looks like over the next quarter. They also flag any tax planning opportunities, financing decisions, or growth conversations that need to happen soon. Between scheduled meetings, the CFO is available by phone and email for time-sensitive questions, like whether the business can afford an unexpected equipment repair or how to handle a slow week that did not match the forecast.

According to a 2025 Deloitte CFO Signals survey, 78% of finance leaders report that scenario modeling has become a core part of their monthly work, up from 52% in 2021. For restaurants, that scenario work translates into questions like what happens to cash if a slow August comes in 15% below last year, or what the financial impact would be of raising menu prices by 4%. A virtual CFO models those questions before they have to be answered, so the owner can make decisions with confidence.

Frequently Asked Questions

How Much Does a Virtual CFO Make

A virtual CFO makes between $150,000 and $300,000 per year on average when working with multiple clients on a fractional basis, according to industry compensation research. Earnings depend on the number of clients, the size of those clients, and the CFO's experience and industry specialization. Hourly rates of $175 to $450 across 10 to 25 hours per week of billable work produce that annual range.

What Is the Salary of a Virtual CFO

The salary of a virtual CFO ranges from $150,000 to $300,000 annually for independent practitioners, while virtual CFOs employed by accounting firms typically earn $130,000 to $220,000 plus bonuses. According to Salary.com data for 2025, the median base salary for a full-time CFO in the U.S. is $437,000, but most virtual CFOs work with multiple clients rather than carrying a single full-time CFO salary at one company.

How Much Should I Pay My CFO

How much you should pay your CFO depends on whether you hire full-time or fractional and the size of your restaurant. For a fractional or virtual CFO, expect to pay $3,000 to $10,000 per month for 10 to 30 hours of support, according to 2025 industry pricing surveys. For a full-time CFO at a multi-unit restaurant group, expect $250,000 to $500,000 in total annual compensation, according to Cowen Partners salary data.

How Much to Pay a Fractional CFO

How much to pay a fractional CFO depends on hours and complexity. Most restaurants pay $200 to $350 per hour, or $3,000 to $10,000 per month on a retainer covering 10 to 30 hours. According to Eagle Rock CFO 2025 pricing research, the most common retainer range for small to mid-sized businesses is $4,000 to $8,000 monthly.

What Is the Average CFO Bonus

The average CFO bonus runs between 25 and 50% of base salary, according to 2025 compensation surveys from Cowen Partners and Heidrick & Struggles. At larger public companies, total cash bonuses for CFOs averaged $367,000 in 2024, according to Spencer Stuart data. At growing private restaurants and other private companies, bonuses are typically smaller in absolute dollars but represent a similar percentage of base pay, often tied to EBITDA, cash flow, or revenue growth targets.

How Much Does a CFO Charge Per Hour

A CFO charges between $175 and $450 per hour for fractional or virtual engagements in 2025, according to multiple industry pricing surveys. Most experienced fractional CFOs charge $200 to $350 per hour, with senior specialists charging up to $600 per hour for complex work like mergers, acquisitions, or major capital raises.

Will CFO Be Replaced by AI

CFO will not be replaced by AI, but the role is changing fast. AI is automating routine tasks like data entry, reconciliation, and basic reporting, which frees up the CFO to focus on judgment, strategy, and high-stakes decisions that machines cannot make. According to a 2025 Gartner CFO survey, AI adoption in finance functions has nearly doubled in two years, and most CFOs see AI as a tool that enhances their work rather than replaces it. For restaurants, the strategic judgment, relationship management, and operational insight a CFO provides cannot be automated.

Wrapping It Up

A virtual CFO gives restaurant owners the financial leadership the industry demands without the cost of a full-time hire. From prime cost tracking and rolling cash forecasts to expansion planning and tax strategy, the right virtual CFO turns the financial side of a restaurant from a source of stress into a source of clarity. The data is clear. Restaurants that bring in senior financial guidance protect their margins better, survive longer, and grow with more confidence in an industry where most operators struggle to make it past year five.

If you run a restaurant and want better control over your numbers, cleaner monthly reporting, and a financial partner who understands the realities of food and labor costs, we would be glad to talk. At NR CPAs & Business Advisors, we work with restaurants and other growing businesses to bring structure, clarity, and strategy to their finances. Give us a call at (954) 231-6613 to start the conversation.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

IRS CP504 Notice: Intent To Levy — What To Do Now

What Is An IRS CP504 Notice

An IRS CP504 is a Notice of Intent to Levy, meaning the IRS is informing you that it will seize your state tax refund, wages, bank accounts, or other property if you do not pay your unpaid tax balance or make payment arrangements immediately. According to the IRS, the CP504 is issued under Internal Revenue Code Section 6331(d) and represents the final automated balance due reminder before the agency begins active enforcement. If you have received this notice, the IRS has already sent prior correspondence about the same unpaid balance and has not received payment or a response.

The CP504 includes your Social Security number, the date of the notice, and the specific tax year and form the balance relates to. It breaks the total amount owed into original tax, assessed penalties, and accrued interest. The notice also provides payment instructions, explains your right to appeal under the Collection Appeals Program, and describes the consequences of not responding. For a broader overview of how all IRS notices work and what different notice types mean, our complete guide to IRS correspondence covers every category from adjustments to enforcement.

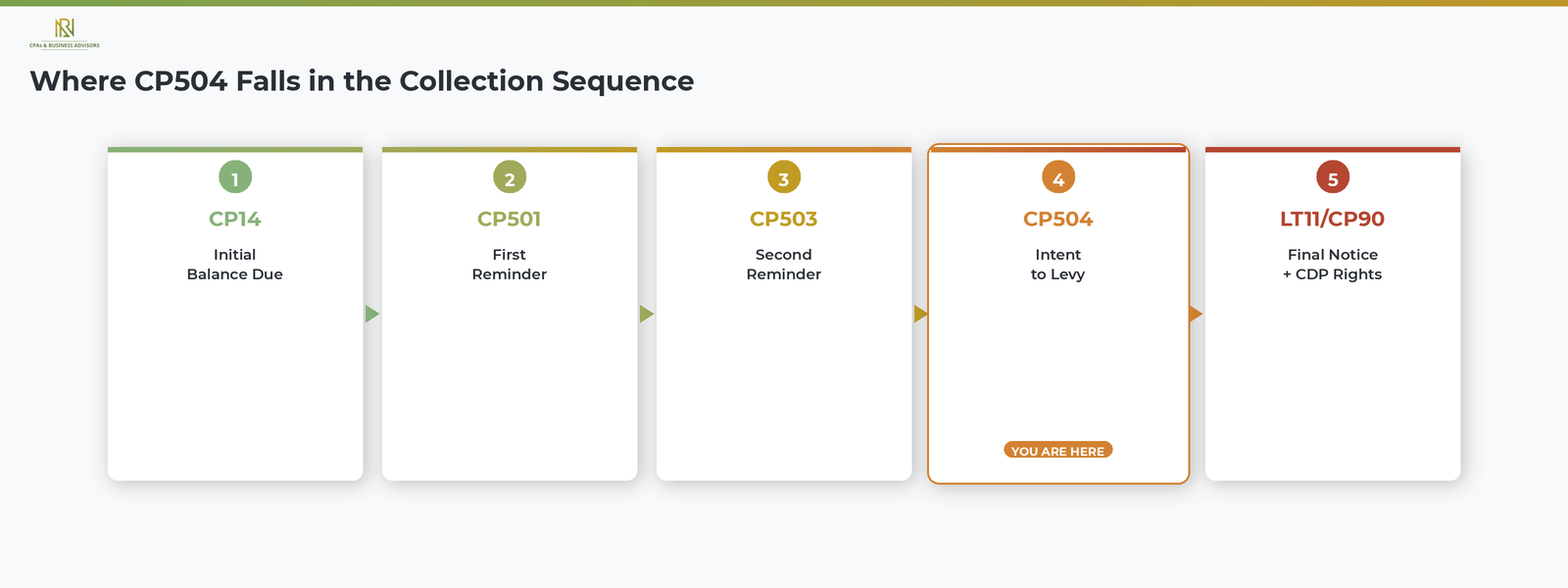

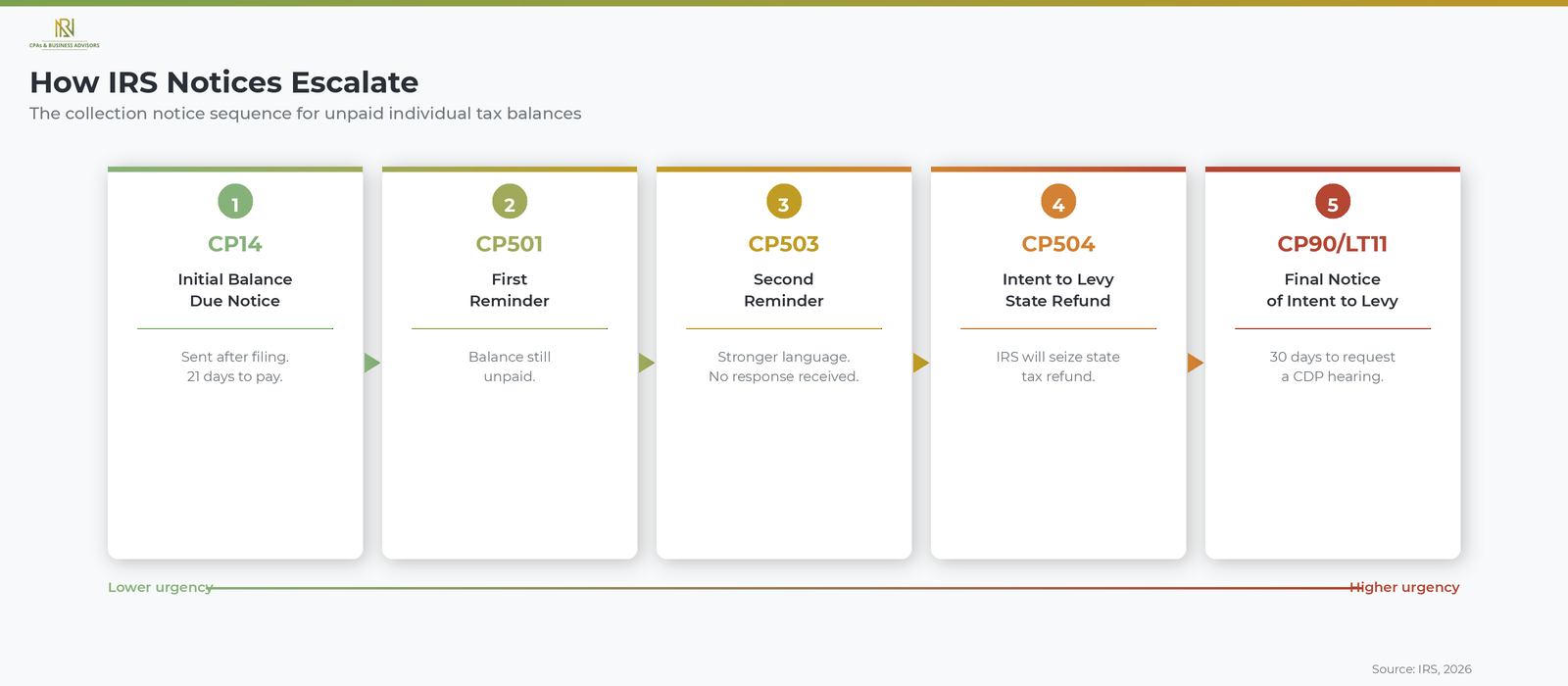

Where CP504 Falls In The IRS Collection Sequence

The CP504 is the fourth notice in a five-step collection sequence that the IRS follows when an individual taxpayer has an unpaid balance. Each notice in this sequence carries more urgency than the last, and the CP504 marks the transition point from automated reminders to active enforcement. According to the IRS, the standard progression works as follows.

- CP14: the initial notice that your tax return has an unpaid balance. Taxpayers who want to understand this first notice in the collection sequence can review our full guide to the CP14 balance due letter.

- CP501: a first reminder that the balance remains unpaid.

- CP503: a second reminder with stronger language, noting that the IRS has still not received payment.

- CP504: the Notice of Intent to Levy, warning that the IRS will begin seizing assets if you do not act.

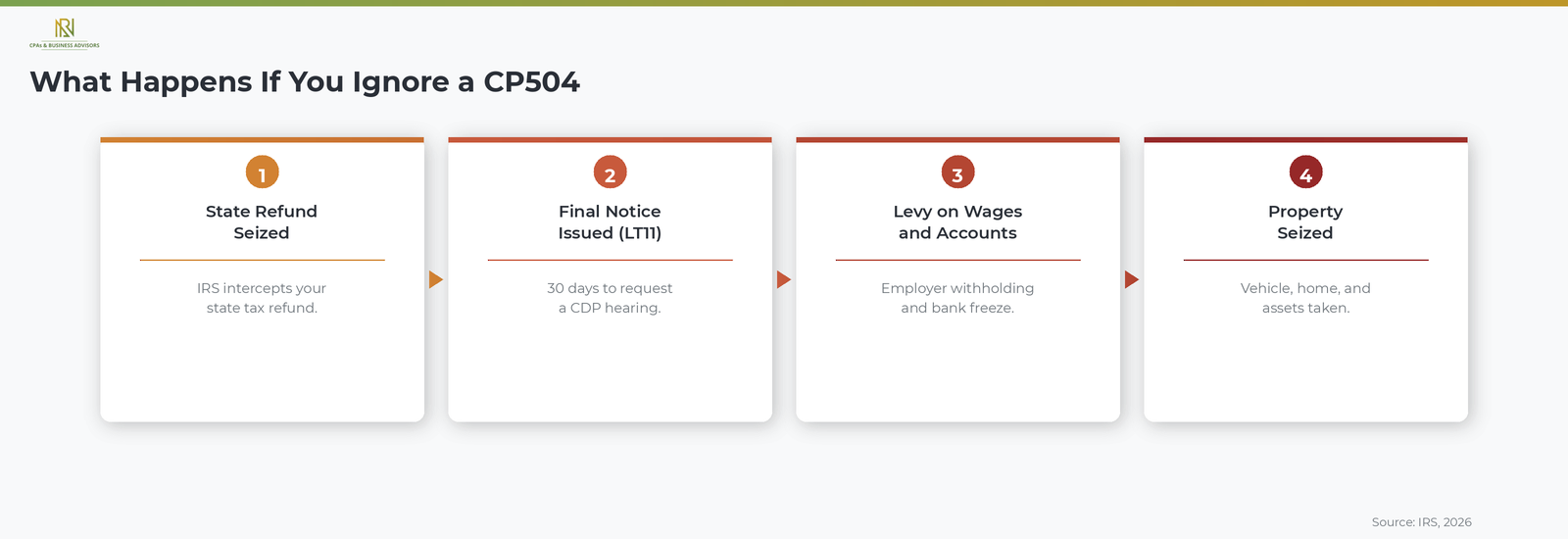

- LT11 or CP90: the Final Notice of Intent to Levy, which grants you the right to request a Collection Due Process hearing within 30 days before the IRS proceeds.

The critical difference between the CP504 and the notices that came before it is that the CP504 authorizes the IRS to levy your state income tax refund without further notice. The final notices that follow, LT11 and CP90, authorize the IRS to levy everything else, including wages, bank accounts, and personal property.

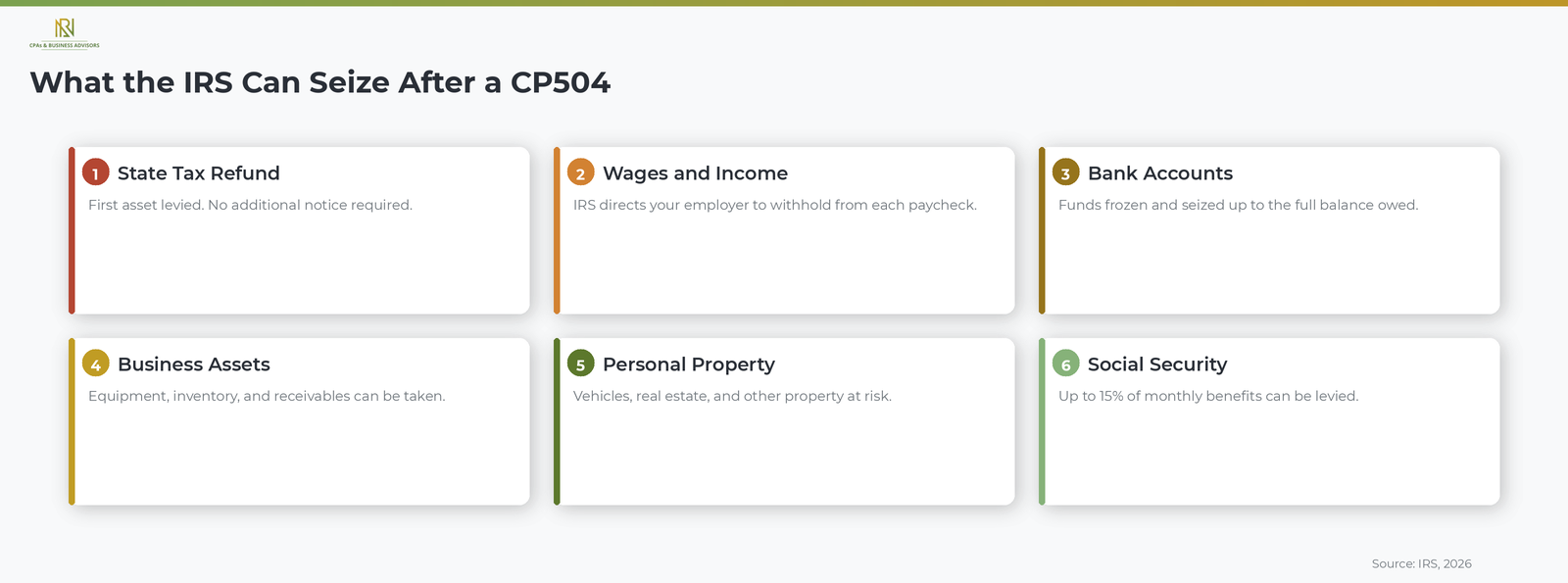

What The IRS Can Seize After A CP504 Notice

After sending a CP504, the IRS can immediately intercept your state income tax refund, and after issuing a subsequent final notice, it can seize virtually any other asset or income stream you have. According to the IRS, property subject to levy includes the following.

- State income tax refunds. According to the IRS, this is typically the first asset levied after a CP504 because the agency can intercept it without issuing an additional notice.

- Wages, salaries, and commissions. The IRS can direct your employer to withhold a portion of each paycheck until the debt is satisfied.

- Bank accounts. The IRS can freeze funds in your checking and savings accounts and seize the balance up to the total amount owed.

- Business assets. Equipment, inventory, and accounts receivable can all be seized to satisfy a business or individual tax debt.

- Personal property. According to the IRS, the agency can seize your vehicle, your home, and other real or personal property. The IRS is one of the few creditors authorized to take a personal residence despite state homestead protections.

- Social Security benefits. The IRS can levy up to 15 percent of your monthly Social Security payments.

In addition to levies, the IRS can file a Notice of Federal Tax Lien, which is a public claim against your current and future assets. According to the IRS, a lien can damage your credit, make it difficult to sell or refinance property, and establish the government's legal priority over other creditors. The FAST Act also authorizes the State Department to deny, revoke, or limit your passport if your tax debt meets the threshold for seriously delinquent tax debt.

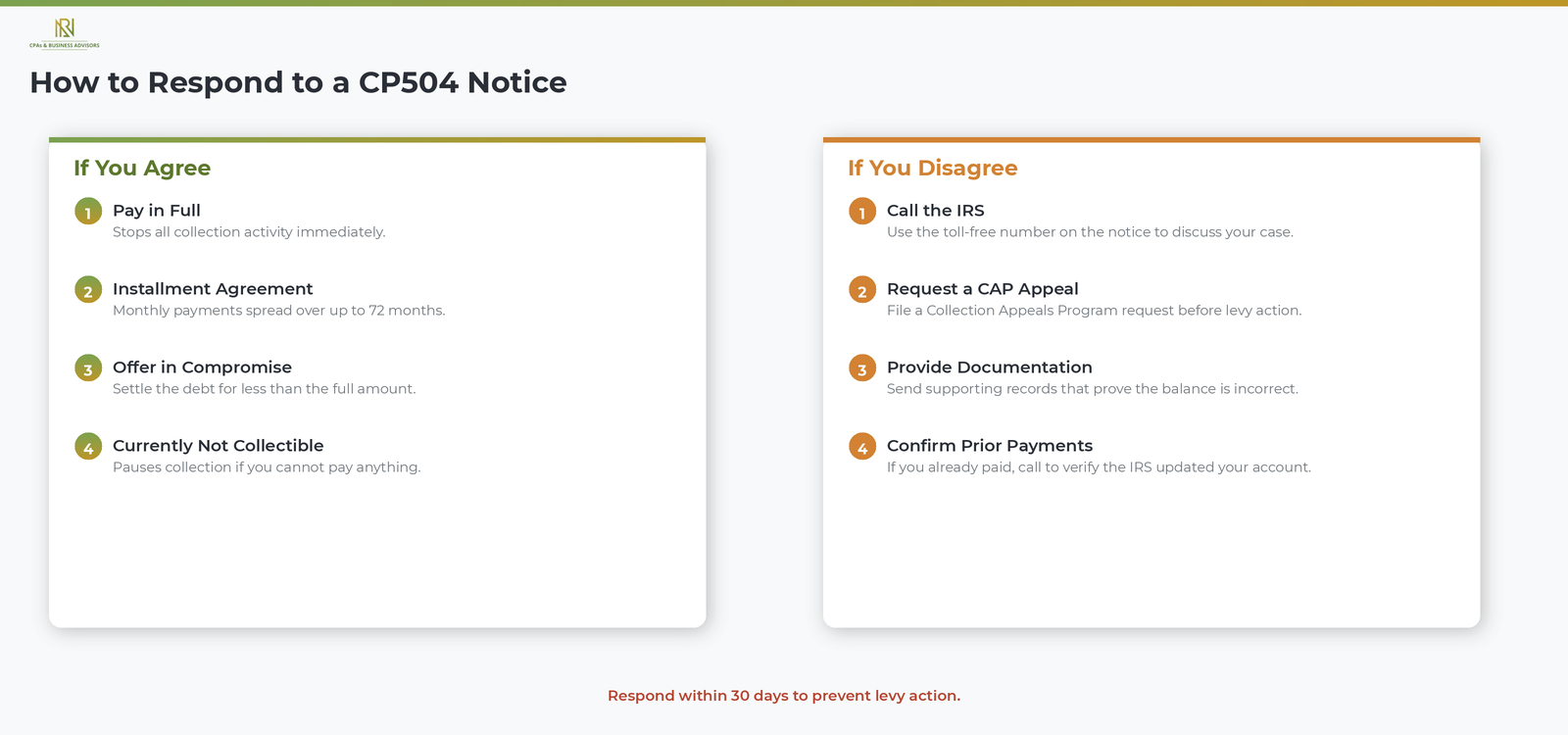

How To Respond To An IRS CP504 Notice

Respond to a CP504 as quickly as possible, ideally well within the 30-day window the IRS provides before taking levy action. Your best course of action depends on whether you agree or disagree with the amount the notice says you owe.

If You Agree With The Amount Owed

According to the IRS, you have several options for resolving the balance.

- Pay in full. The fastest way to stop collection activity is to pay the entire balance shown on the notice. You can pay online at IRS.gov, by phone, or by mailing a check with the payment voucher included in the notice.

- Set up an installment agreement. If you cannot pay the full amount at once, you may qualify for a monthly IRS payment plan or installment agreement. Our step-by-step guide to setting up structured payments covers the application process, balance thresholds, and how interest is calculated on the remaining amount.

- Submit an Offer in Compromise. If your financial situation makes it unlikely you can pay the full debt even with a payment plan, you may be able to settle for less than you owe through a formal Offer in Compromise.

- Request Currently Not Collectible status. If you have no ability to pay anything toward the debt, the IRS may temporarily pause collection activity by placing your account in Currently Not Collectible status. This does not eliminate the debt, but it stops levies while you remain unable to pay.

Taxpayers facing significant financial hardship may also qualify for the IRS Fresh Start program, which expands access to installment agreements and eases qualification thresholds for eligible individuals and businesses.

If You Disagree With The Amount Owed

If you believe the balance on the CP504 is incorrect, call the toll-free number printed on the notice immediately. According to the IRS, you can also request an appeal under the Collection Appeals Program before collection action takes place by following the instructions included in the notice. If you have already paid the balance or set up an installment agreement, contact the IRS at the number on the notice to confirm that your account reflects the payment or arrangement.

For general guidance on responding to any IRS correspondence, including how to organize supporting documentation and meet response deadlines, our guide on what to do when you receive an IRS notice provides a step-by-step walkthrough of the full response process.

What Happens If You Ignore A CP504 Notice

Ignoring a CP504 causes the IRS to escalate to its final enforcement steps, beginning with the seizure of your state tax refund and progressing to levies on your wages, bank accounts, and personal property. According to the IRS, the next notice after the CP504 is typically the LT11 or Letter 1058, labeled "Final Notice of Intent to Levy and Notice of Your Right to a Hearing." This notice grants you the right to request a Collection Due Process hearing within 30 days, which is your last formal opportunity to challenge the proposed levy or present an alternative resolution before the IRS takes action.

If you do not respond to that final notice, the IRS can proceed with levying all available assets, filing a federal tax lien that becomes part of the public record and affects your credit, and, for balances meeting the seriously delinquent threshold, certifying your debt to the State Department for passport denial or revocation. Penalties and interest continue to accrue on the unpaid balance throughout this process, increasing the total amount owed with each month that passes.

Difference Between CP504 And CP504B

The CP504 is issued to individual taxpayers for unpaid personal income tax, while the CP504B is issued to businesses for unpaid business tax obligations such as employment taxes or excise taxes. According to the IRS, both notices carry the same intent to levy warning and the same level of urgency. If you received a CP504B for a business tax account, the response options and deadlines are the same as those described above for the standard CP504.

Frequently Asked Questions About The IRS CP504 Notice

How Serious Is A CP504 Notice?

A CP504 is one of the most urgent notices the IRS issues. According to the IRS, it is a formal Notice of Intent to Levy that authorizes the agency to begin seizing your state tax refund immediately and signals that levies on wages, bank accounts, and property will follow if you do not respond.

What Comes After A CP504 Notice?

The next step after a CP504 is typically the LT11 or Letter 1058, the Final Notice of Intent to Levy. According to the IRS, this final notice grants you 30 days to request a Collection Due Process hearing. If you do not respond, the IRS can proceed with levying your assets.

Is A CP504 Sent By Certified Mail?

The CP504 is typically sent by regular U.S. mail, not certified mail. According to the IRS, the subsequent final notice (LT11 or CP90) may arrive by certified mail because it triggers Collection Due Process hearing rights and the IRS must document delivery.

Can I Set Up A Payment Plan After Receiving A CP504?

Yes, you can still apply for an installment agreement after receiving a CP504. According to the IRS, you can apply online through the IRS Online Payment Agreement tool at IRS.gov or by calling the toll-free number printed on the notice. Setting up a payment plan stops the escalation toward active levy action as long as you remain current on your payments.

IRS Notices Explained: What Each Letter Means And What To Do?

What Is An IRS Notice

An IRS notice is official correspondence that the Internal Revenue Service sends through the U.S. mail to inform you about a specific issue with your federal tax return or account. According to the IRS, the agency sends notices for reasons ranging from a simple math correction on your return to an unpaid balance or a request for additional documentation. Receiving a notice does not necessarily mean you made a mistake or owe additional tax, and many notices can be resolved by following the instructions printed on the document.

The IRS draws a practical distinction between two categories of mail. A notice is typically system-generated and addresses a specific account issue such as a balance due, a refund adjustment, or a processing change. A letter, by contrast, often comes from an individual IRS employee or department and may request information, confirm an action, or relate to an ongoing examination. Both arrive by U.S. mail, and both include a notice or letter number in the upper right corner of the first page that identifies exactly what the correspondence is about.

Common Reasons The IRS Sends Notices

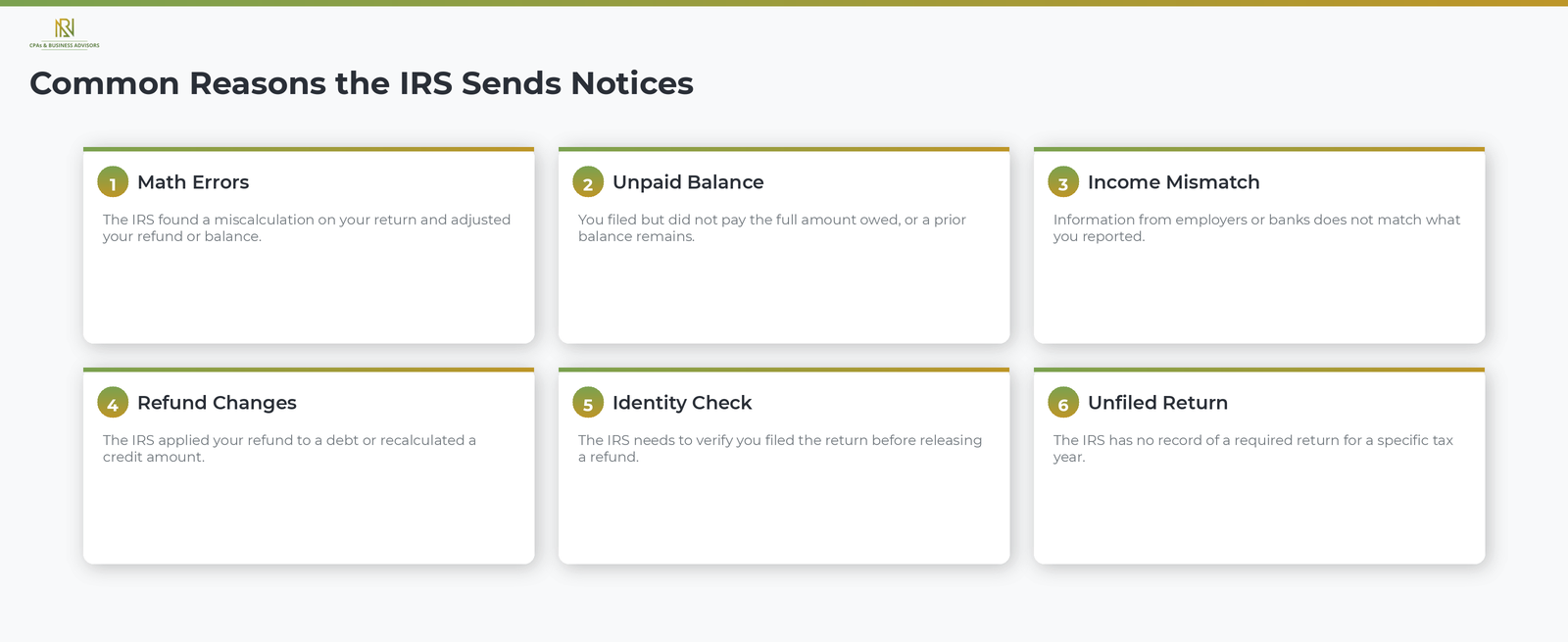

The IRS sends notices most often because of a discrepancy on your tax return, an unpaid balance, or a change the agency made to your account. According to the IRS, the most frequent triggers include the following situations.

- Math errors or miscalculations on your return. The IRS caught an arithmetic mistake and adjusted your refund or balance accordingly.

- An unpaid tax balance. You filed a return but did not pay the full amount owed, or a prior balance remains on your account.

- Unreported or underreported income. Information the IRS received from employers, banks, or other third parties does not match what you reported on your return.

- Refund changes. The IRS applied your refund to a prior debt or adjusted the amount because of a credit recalculation.

- Identity verification. The IRS needs to confirm that you filed the return before releasing a refund.

- Unfiled returns. The IRS has no record of a required return for a specific tax year.

Not every IRS notice signals a problem. Some correspondence simply confirms a change you requested, acknowledges information you submitted, or notifies you that the IRS closed its review of your account.

Most Common Types Of IRS Notices

IRS notices fall into several broad categories based on why the agency issued them. Understanding which category your notice belongs to helps you assess its urgency and determine what kind of response it requires. The notice number, printed in the upper right corner of the first page, identifies the specific type.

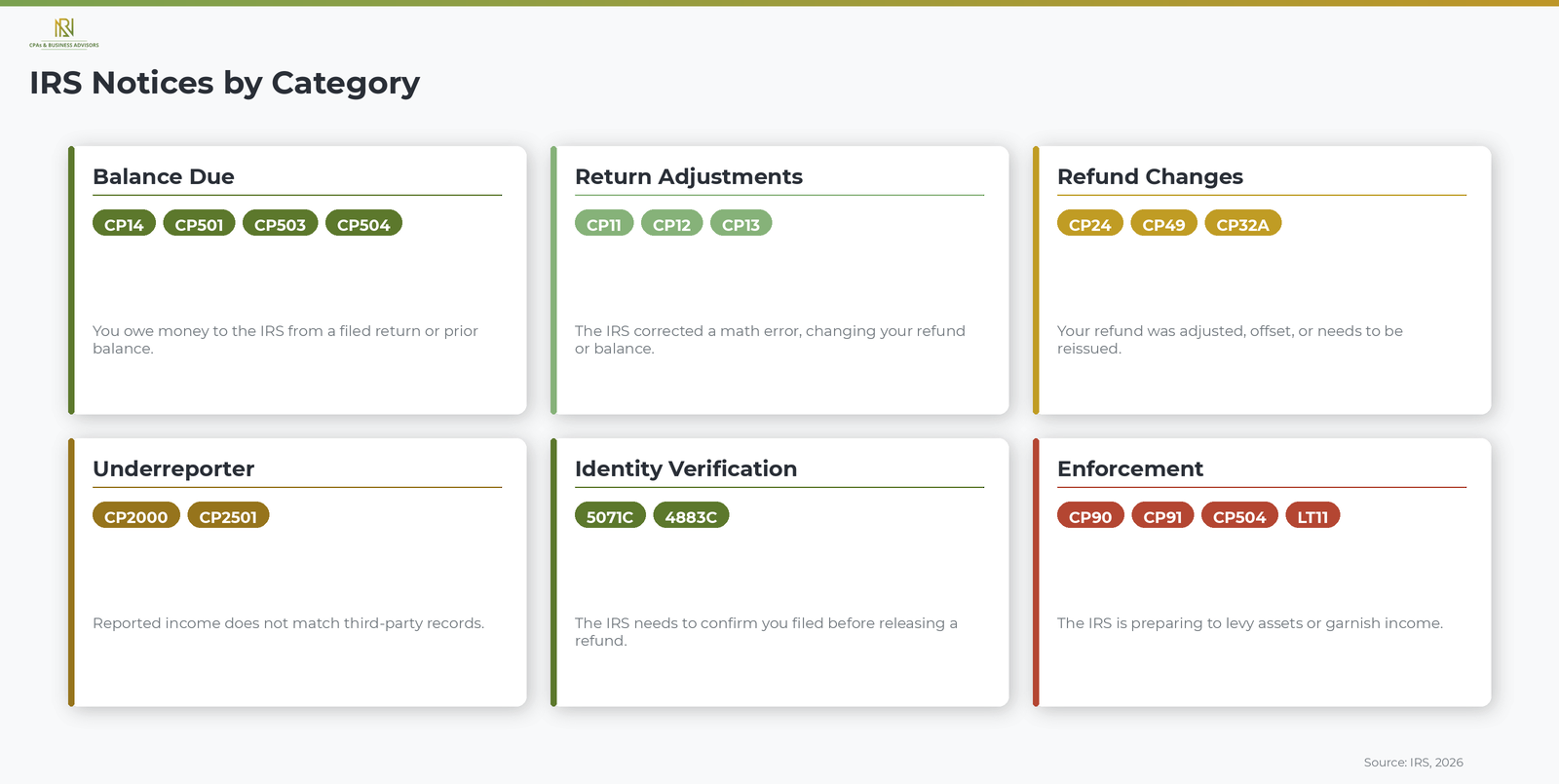

Balance Due Notices

Balance due notices inform you that you owe money to the IRS. The most common is the CP14, which is the initial notice the agency sends when a filed return shows an unpaid amount. If you received a CP14 notice, our complete guide to this balance due letter explains the specific charges, deadlines, and response options. Subsequent reminders in the collection sequence include the CP501, CP503, and CP504, each carrying increased urgency.

Return Adjustment Notices

The IRS sends adjustment notices when it corrects an error on your return. A CP11 means the correction resulted in a balance you now owe. A CP12 means the correction resulted in a larger refund or a change to the amount you expected. A CP13 means the correction left your balance at zero with no additional amount owed and no refund due. According to the IRS, each of these notices explains exactly what changed and how the recalculated amount was determined.

Refund-Related Notices

These notices address changes to the amount or timing of your refund. A CP24 notifies you that the IRS found a difference between your estimated tax payments and the amount posted to your account, resulting in a potential overpayment credit. A CP49 notifies you that the IRS applied all or part of your refund to a prior tax debt. A CP32A asks you to contact the IRS so the agency can reissue a refund check.

Underreporter Notices

An underreporter notice means the income or payment information the IRS received from third parties does not match what you reported. The CP2000 is the primary notice in this category and one of the most frequently issued IRS letters. According to the IRS, a CP2000 is not a bill but a proposed adjustment that explains how the recalculated tax was determined. Taxpayers who receive a CP2000 notice can review our full guide to this underreporter letter for response steps and dispute options.

Identity Verification Notices

Identity verification notices ask you to confirm that you filed the return in question before the IRS will release a refund. Common examples include Letter 5071C and Letter 4883C. According to the IRS, these letters are part of the agency's efforts to prevent tax-related identity theft and typically require you to verify your identity online at IRS.gov or by calling the toll-free number printed on the letter.

Enforcement And Collection Notices

Enforcement notices signal that the IRS is preparing to take collection action against your assets. A CP504 warns that the IRS intends to levy your state tax refund. A CP90 or LT11 is a final notice of intent to levy bank accounts, wages, and other property, and it grants you the right to request a Collection Due Process hearing within 30 days. Certain enforcement notices, such as the CP90, may arrive as certified mail requiring your signature. A CP91 warns that the IRS intends to levy up to 15 percent of your Social Security benefits.

How IRS Notices Escalate From Reminder To Enforcement

IRS collection notices follow a specific sequence that grows more urgent at each stage, and each notice includes a deadline that starts the clock on the next escalation step. According to the IRS, the standard progression for an unpaid individual tax balance works as follows.

- CP14: the initial balance due notice, sent shortly after you file a return with an unpaid amount.

- CP501: a first reminder that your balance remains unpaid.

- CP503: a second reminder with stronger language, noting that the IRS still has not received your payment or a response.

- CP504: a notice of intent to levy your state income tax refund if you do not pay or contact the IRS to arrange a resolution.

- CP90 or LT11: the final notice of intent to levy your wages, bank accounts, and other assets. This notice also informs you of your right to a Collection Due Process hearing, which you must request within 30 days.

Responding at any point in this sequence can slow or stop the escalation. Taxpayers who cannot pay the full amount may qualify for a structured IRS payment plan or installment agreement. Our guide to these structured repayment options covers the application process, payment thresholds, and how interest is calculated on the remaining balance. Those facing significant financial hardship may also qualify for the IRS Fresh Start program, which provides expanded installment terms and penalty relief for eligible individuals and businesses.

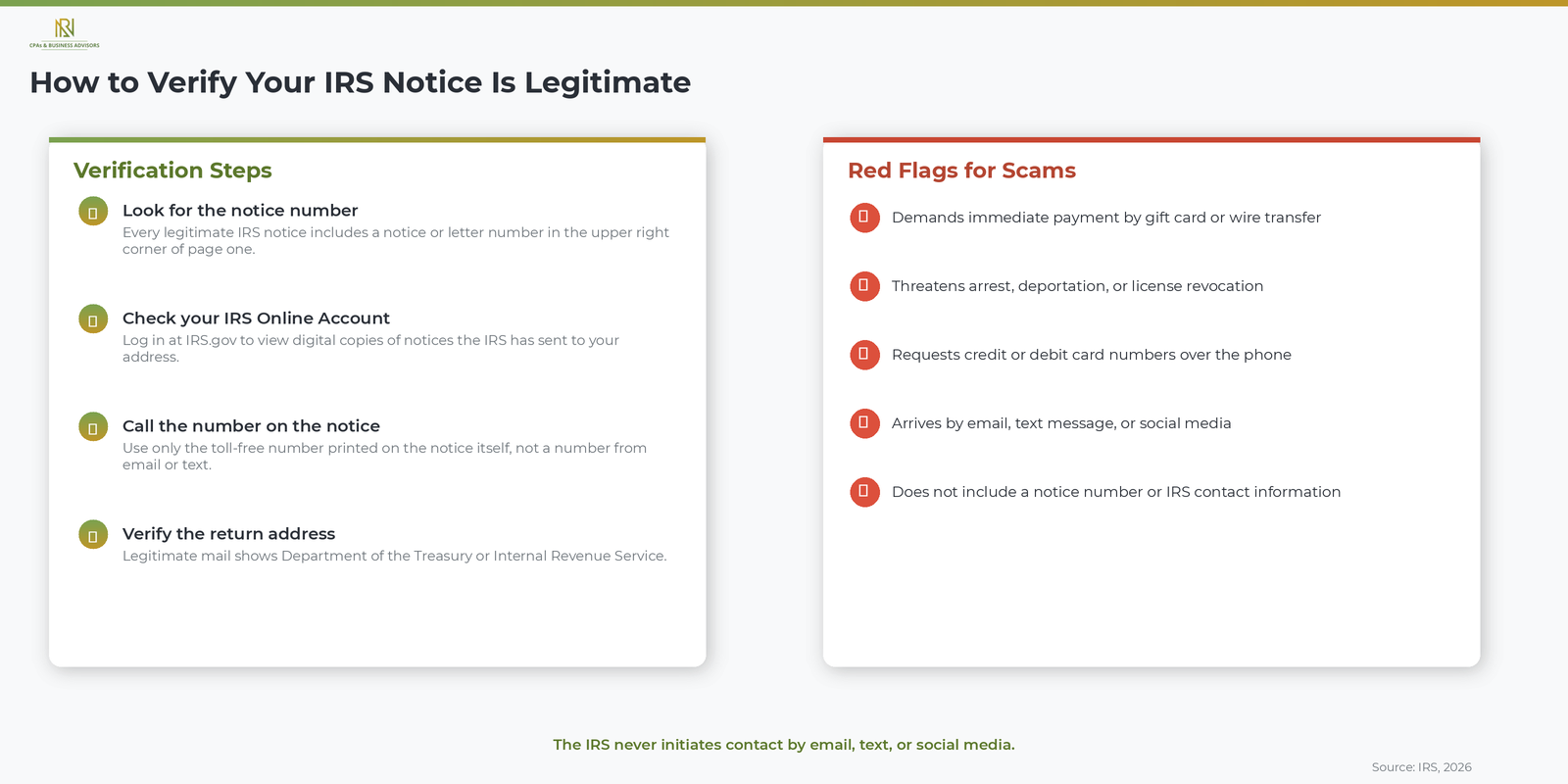

How To Verify Your IRS Notice Is Legitimate

A legitimate IRS notice arrives by U.S. mail, references a specific tax year and notice number, and never asks you to click a link or provide personal information through email or text. According to the IRS, the agency does not initiate contact with taxpayers by email, text message, or social media to request personal or financial information. Any communication that does so is a scam.

To confirm that a notice you received is genuine, take the following steps.

- Look for the notice or letter number in the upper right corner of the first page. Every legitimate IRS notice includes one.

- Log in to your IRS Online Account at IRS.gov. According to the IRS, many notices are viewable in your online account, which allows you to verify the correspondence directly against what the agency has on file.

- Call the toll-free number printed on the notice itself, not a number from an email, a text, or a website you found through a search.

- Check the return address. Legitimate IRS mail comes from a recognized IRS processing center, and the envelope typically includes "Department of the Treasury" or "Internal Revenue Service" in the return address.

According to the IRS, common red flags for fraudulent correspondence include demands for immediate payment by gift card or wire transfer, threats of arrest or deportation, and requests for credit or debit card numbers over the phone.

What To Do When You Receive An IRS Notice

Read the notice carefully, compare the information to your own tax records, and respond by the deadline printed on the document. Most IRS notices explain exactly what changed, why it changed, and what action you need to take. If you agree with the notice, follow the payment or documentation instructions provided. If you disagree, the notice will explain how to dispute the changes, which typically involves mailing a written response with supporting documents to the address on the notice.

The most critical step is acting before the deadline. Late responses can limit your options for disputing proposed changes or requesting a hearing. For a complete walkthrough of what to do when you receive an IRS notice, including what documentation to gather and how to organize your reply, our step-by-step response guide covers every stage from opening the envelope to confirming the issue is resolved.

When To Get Professional Help With An IRS Notice

Consider working with a CPA, Enrolled Agent, or tax attorney when your notice involves a large balance due, a proposed audit, an enforcement action such as a levy or lien, or a situation you do not fully understand. A qualified tax professional can communicate directly with the IRS on your behalf, identify resolution options you may not be aware of, and ensure your rights as a taxpayer are protected throughout the process. According to the IRS, you can authorize a representative by filing Form 2848, Power of Attorney and Declaration of Representative. Simple notices confirming a small refund adjustment or a zero-balance correction typically do not require professional assistance.

Frequently Asked Questions About IRS Notices

What Is The Most Common IRS Notice?

The CP14 is the most commonly issued IRS notice. According to the IRS, a CP14 is sent when a filed tax return shows an unpaid balance. The notice lists the amount owed, the payment due date, and the options available for resolving the balance.

How Do I Know If My IRS Notice Is Real?

A real IRS notice arrives by U.S. mail, includes a notice number in the upper right corner, and references a tax year tied to your account. According to the IRS, the agency never initiates contact by email, text, or social media. You can verify any notice by logging in to your IRS Online Account at IRS.gov.

What Happens If I Ignore An IRS Notice?

Ignoring an IRS notice allows penalties and interest to accumulate and moves your case further along the collection process. According to the IRS, unresolved balances can eventually lead to a federal tax lien on your property, levies on your bank accounts and wages, and garnishment of up to 15 percent of your Social Security benefits.

Can I View My IRS Notices Online?

Yes, many IRS notices are available through your IRS Online Account. According to the IRS, you can log in at IRS.gov to view digital copies of notices the agency has sent to your address on file, which provides a convenient way to review your correspondence without waiting for mail delivery.