%201.avif)

.png)

.png)

How to Scale a Small Business?

To scale a small business, you build the systems, team, financial discipline, and strategy that let revenue grow much faster than costs. Scaling is different from simply growing. Growth means adding revenue while costs rise at the same rate. Scaling means adding revenue while keeping costs flat or growing only slightly, which is the only way a small business creates real wealth for its owner.

In this article, we cover the best way to scale, the 4 pillars that drive successful scaling, the specific steps to follow, the easiest businesses to scale, why most small businesses fail, how much profit owners actually keep, and how to value a business so you know what scaling is really worth.

How to Scale a Small Business

To scale a small business, you build a model where revenue grows faster than costs. That requires four things at once: clean financial systems that give you real-time visibility, a team that can deliver without the owner doing every job, processes that work the same way every time, and a marketing engine that brings in customers predictably. Skip any one of these and the scaling effort stalls.

The data shows why this matters. According to the U.S. Bureau of Labor Statistics, approximately 20% of small businesses fail in the first year, 50% fail by year five, and 65% fail by year ten. The Kaplan Group reports that 478,800 new businesses are forming each month in 2025, the highest rate on record, which means competition for customers and talent is intense. According to Search Logistics 2026 data, 82% of business failures trace back to poor financial management. Scaling without the right financial discipline is how good ideas turn into closed businesses.

The good news is that scaling is not about working harder. It is about working differently. Owners who scale successfully step out of day-to-day operations and into strategic decisions. They put structured strategic planning in place so every department moves in the same direction. They invest in technology, document their processes, and hire ahead of demand instead of behind it. The shift is uncomfortable at first, but it is the only path from a job that owns you to a business that pays you.

What Is the Best Way to Scale a Business

The best way to scale a business is to standardize your operations, invest in repeatable systems, build a team that can run without you, and use data to make every major decision. These four moves create the leverage that separates a scaling business from one that just gets bigger and more chaotic.

Standardizing operations starts with documenting how every important task gets done. Sales calls, onboarding, customer service, fulfillment, billing, and reporting all need written processes that any trained employee can follow. According to a 2025 small business survey reported by the Federal Reserve, 57% of small business owners cite difficulty reaching customers and growing sales as their top operational challenge, up from 53% in 2023. That problem is much easier to solve when your sales process is documented and consistent than when every salesperson does it differently.

Repeatable systems mean software, tools, and workflows that handle work without owner involvement. CRMs, accounting platforms, scheduling tools, marketing automation, and project management software each remove a piece of the owner's daily workload. Building a team that runs without you means hiring people who can make decisions, training them on the systems, and trusting them to execute. Using data means tracking the right KPIs every week and adjusting before small problems compound. Our business consulting work focuses on exactly this kind of structured scaling.

What Are the 4 Pillars of Scaling Up

The 4 pillars of scaling up are People, Strategy, Execution, and Cash. This framework comes from Verne Harnish's book Scaling Up: How a Few Companies Make It and Why the Rest Don't, which has been used by more than 40,000 business leaders worldwide. Each pillar plays a specific role, and weakness in any one of them will limit how far the business can grow.

People

People is the first pillar because nothing else works without the right team in the right seats. According to Harnish's framework, scaling companies focus on attracting, hiring, developing, and retaining people who match the company's values and skills needs. A bad hire at scale costs more than a bad hire at the startup stage because the mistake gets replicated across more customers, more deals, and more team members.

Strong people decisions include clear job descriptions, structured interview processes, defined performance expectations, and regular feedback. According to a 2025 Robert Half hiring survey, 62% of finance and operations leaders struggle to hire qualified talent, which means the businesses that get hiring right pull ahead of competitors who do not.

Strategy

Strategy is the second pillar. A scaling business needs a clear answer to four questions: what do we do, who do we serve, why do they choose us, and where are we going. Without those answers, every department drifts in its own direction. Harnish's research found that companies with a written one-page strategic plan that everyone in the business understands grow faster than those without one.

Good strategy also includes a clear competitive position. According to a 2025 Fidelity Private Shares analysis of mid-stage businesses, capital and customers are flowing toward companies with lasting competitive advantages, not just growth at any cost. Defining where you win and where you do not play is one of the most important strategic decisions a scaling business makes.

Execution

Execution is the third pillar. According to Harnish's framework, sustained high growth comes from disciplined habits, routines, and scorekeeping. That means setting priorities every quarter, holding short daily and weekly meetings to surface bottlenecks, and tracking the KPIs that drive profit and cash. The Rockefeller Habits checklist from Harnish's earlier work outlines ten specific habits that scaling companies follow consistently.

Execution discipline shows up in monthly financial reviews, weekly KPI dashboards, quarterly planning sessions, and clear accountability for results. A 2025 Deloitte CFO Signals survey found that 78% of finance leaders treat scenario modeling as a core part of their monthly work, up from 52% in 2021. That kind of discipline is what scaling demands at every level of the business.

Cash

Cash is the fourth pillar and the one most small businesses get wrong. Growth consumes cash. New hires, more inventory, more marketing, and larger receivables all hit the bank account before the new revenue arrives. According to U.S. Bank research widely cited by industry analysts, 82% of small businesses that fail do so because of poor cash flow management.

Strong cash discipline includes a rolling 13-week cash flow forecast, weekly receivables follow-up, strategic vendor payment timing, and an operating reserve sized for the volatility of the business. The shorter you can make your cash conversion cycle, the faster you can scale without running out of capital. The same kind of cash flow discipline that protects larger companies is exactly what scaling small businesses need most.

The Difference Between Growing and Scaling a Business

The difference between growing and scaling a business is the relationship between revenue and costs. Growing a business means revenue goes up, but costs go up roughly at the same rate, so profit margins stay flat. Scaling a business means revenue goes up while costs stay relatively flat, so profit margins improve as the business gets bigger.

A simple example clarifies the distinction. A service business that grows from $1 million to $2 million in revenue by hiring twice as many employees has grown, but it has not scaled. Margins probably stayed the same. A service business that grows from $1 million to $2 million by adding automation, raising prices, and serving more customers per team member has scaled. Margins improve, the owner's profit increases, and the business becomes more valuable.

According to data from the Federal Reserve's 2025 Small Business Credit Survey, only 46% of small employer firms were profitable in 2024, with another 35% breaking even and 19% operating at a loss. Those numbers reflect a market where most owners are growing but few are actually scaling. The owners who scale almost always have systems, financial discipline, and a clear strategy in place before the growth happens.

Steps to Scale a Small Business

The steps to scale a small business are documenting your processes, building a strong team, strengthening cash flow management, investing in marketing that compounds, and using technology to multiply output. Each step builds on the one before it. Skip a step and the scaling effort gets harder.

Build Systems and Documented Processes

Systems are the foundation of scaling. Every recurring task in the business should have a documented process that any trained team member can follow. Sales scripts, customer onboarding checklists, fulfillment procedures, billing workflows, and reporting templates all reduce dependence on the owner. According to a 2025 small business research report, businesses with documented systems scale 30 to 40% faster than those that rely on tribal knowledge held only in the owner's head.

Systems also make the business more valuable when the owner eventually sells. According to BizBuySell data from 2025 covering 9,500 transactions, businesses with strong operating systems sell for materially higher SDE multiples than owner-dependent businesses. The investment in documentation pays off twice: once during scaling, and again at exit.

Develop and Empower Your Team

A small business cannot scale on the owner's effort alone. Building a team means hiring for specific roles, training them on the systems, and giving them authority to make decisions. According to Robert Half 2025 research, 62% of finance and operations leaders report ongoing talent shortages, which means good hires are harder to find but more valuable when you get them right.

Empowering the team means resisting the urge to micromanage. Owners who scale successfully spend less time in operations and more time on strategy, hiring, and high-level customer relationships. That shift requires trust, training, and clear performance expectations. Our startup advisory work often centers on helping owners make exactly this transition, which is one of the hardest parts of going from a $1 million business to a $5 million business.

Strengthen Cash Flow Management

Cash flow management is the financial discipline that lets you scale without running out of money. The basic tools are a rolling 13-week cash forecast, a clear receivables process, strategic payable timing, and a cash reserve sized for the volatility of the business. According to a Federal Reserve survey cited in Kaplan Group research, 51% of small businesses report uneven cash flows as a top financial challenge.

Strong cash discipline also includes weekly bank reviews, monthly close within 5 business days, and clean financial statements that the owner can actually read. According to Search Logistics 2026 data, 33% of small business owners cite cash flow as their number one challenge. Solving that one problem early is often the single biggest unlock for scaling.

Invest in Marketing That Compounds

Scaling marketing is different from running marketing. Scaling marketing means investing in channels that get more efficient over time, not just bigger. Content marketing, SEO, email lists, referral programs, and brand building all compound. Paid ads can scale, but they do not compound. Most scaling businesses build a mix that includes both, with the compounding channels carrying more of the load over time.

Smart marketing investment also requires measurement. According to a 2025 Federal Reserve small business survey, 57% of small business owners cite difficulty reaching customers and growing sales as their top operational challenge. The owners who solve that problem track customer acquisition cost, lifetime value, and conversion rates by channel every month, then double down on what works and cut what does not.

Use Technology to Multiply Output

Technology is how a small team handles the workload of a much larger team. CRM systems, accounting platforms, marketing automation, scheduling tools, and AI-powered software each remove hours of manual work every week. According to a 2025 Gartner survey, AI adoption in business operations has nearly doubled in two years, and most small businesses now use at least one AI-driven tool to handle work that used to require a full-time employee.

The right technology stack depends on the business. A professional services firm might prioritize CRM, project management, and time tracking. A product business might prioritize inventory management, e-commerce, and supply chain tools. The principle stays the same. Every recurring manual task is a candidate for automation, and every hour the owner spends on manual work is an hour not spent on scaling.

Why Do 90% of Small Businesses Fail

The 90% small business failure statistic is a myth. The actual numbers, according to the U.S. Bureau of Labor Statistics, are that approximately 20% of small businesses fail in the first year, 30% fail by year two, 50% fail by year five, and 65% fail by year ten. The 90% figure usually comes from misquoted statistics about startups in high-risk industries, not small businesses overall.

That said, the real failure rates are still high enough to take seriously. According to Search Logistics 2026 small business data, 82% of business failures are caused by poor financial management. Other top reasons include weak demand for the product or service, undercapitalization, poor team execution, and inability to compete on price or differentiation. According to CB Insights research on broader business failures, 42% of failures are tied to lack of market need and 29% are tied to running out of cash.

The good news is that most of the top failure causes are preventable with the right financial discipline, strategic planning, and operational systems. Owners who treat their business like a business, not a side project, dramatically improve their odds. According to LendingTree's analysis of 2025 BLS data, the information sector has the highest first-year failure rate at 28.4%, while agriculture, forestry, fishing, and hunting have the highest 10-year survival rate at 50.5%. The takeaway is that industry matters, but execution matters more.

What Are the Easiest Businesses to Scale

The easiest businesses to scale are software and SaaS companies, e-commerce brands with strong unit economics, digital service businesses with productized offerings, franchises and licensing models, and content-driven businesses with strong organic distribution. These models share three traits: low marginal cost to serve additional customers, strong recurring or repeat revenue, and a clear path to automate or delegate most of the work.

According to a 2025 valuation analysis from Sundance Financial covering BizBuySell transactions, the highest-multiple small businesses are typically the ones with recurring revenue, low owner dependency, and strong asset bases. Marinas sold at average 6.6x SDE, car washes at 4.7x, storage facilities at 4.6x, medical billing at 4.4x, and laundromats at 4.1x. The lower-multiple businesses tend to be the ones that depend heavily on the owner's daily involvement, like single-owner consulting practices or specialty service businesses.

Industries that are harder to scale include restaurants, traditional retail, single-owner professional services, and businesses with heavy regulatory burdens. These can still grow successfully, but they require more capital, more management bandwidth, and more time per dollar of revenue added. Owners in harder-to-scale industries often choose to scale by multiplying locations or productizing their service rather than trying to scale a single unit beyond a certain size. Strong business formation decisions at the start also affect how easily a business can later add locations or new entities for expansion.

How Much Profit Does a Business Owner Actually Keep

How much profit a business owner actually keeps depends on industry, size, structure, and tax planning, but the typical net profit margin for a small business runs between 5 and 15% of revenue. Some industries push higher, like software at 20 to 30% and specialty services at 15 to 25%. Others run thinner, like restaurants at 3 to 5% and retail at 2 to 6%.

The number that matters most to owners is not net profit margin on the financials. It is what is called Seller's Discretionary Earnings, or SDE. SDE adds back the owner's salary, benefits, and any non-essential expenses to net profit, showing the total economic benefit the owner receives from the business. For a $1 million revenue service business with a 10% reported net margin, SDE might run $150,000 to $200,000 once owner salary and benefits are added back.

The way to keep more profit is twofold. First, optimize the business so margins improve as revenue grows. Higher prices, better cost control, and more efficient delivery all flow directly to the owner's pocket. Second, use proactive tax planning to keep more of what the business earns. The right entity structure, retirement plan contributions, equipment depreciation timing, and qualified business deductions can save tens of thousands of dollars per year for a typical small business owner.

Is a Business Worth 5 Times Profit

A business is sometimes worth 5 times profit, but the typical range is 2 to 5 times profit for small businesses depending on size, industry, growth rate, and owner dependency. According to Sundance Financial 2025 data covering more than 9,500 BizBuySell transactions, the average small business sold for approximately 2.5x SDE in 2025. Multiples above 5x are usually reserved for businesses with recurring revenue, strong systems, minimal owner involvement, or attractive growth trajectories.

The 5x rule of thumb comes from how mid-size businesses are valued using EBITDA multiples. According to Sofer Advisors 2024 to 2025 transaction data, EBITDA multiples for small businesses under $1 million in EBITDA typically run 3x to 5x, with stronger businesses reaching 5x to 7x. Businesses above $10 million in EBITDA often command premium multiples in the 8x to 14x range because they attract institutional buyers and have more sophisticated operations.

The factors that push multiples higher are well documented. Recurring revenue, diversified customer base, strong margins, low owner dependency, clean financial reporting, and a documented growth trajectory all increase the multiple a buyer is willing to pay. The factors that push multiples lower include customer concentration, owner dependency, declining revenue, weak margins, and messy books. Investing in scaling discipline before a sale almost always pays for itself in a higher exit multiple.

How Many Times Is EBITDA a Company Worth

How many times EBITDA a company is worth depends on size, industry, and quality. According to Sofer Advisors data based on 2024 to 2025 transaction analysis, small businesses with under $1 million in EBITDA typically trade at 3x to 5x EBITDA. Mid-market businesses with $2 million to $10 million in EBITDA generally trade at 5x to 9x. Larger businesses above $10 million in EBITDA often see 8x to 14x or higher, especially in technology and other growth sectors.

Industry plays a major role. According to ClearlyAcquired 2025 valuation data, the median EV/EBITDA multiple for industrial sector strategic buyers jumped to 14.7x in 2025 from 8.0x in 2024, driven by demand for automation and infrastructure businesses. Technology and SaaS businesses routinely trade at 8x to 15x EBITDA at the lower middle market, while traditional service businesses trade at 4x to 7x. Restaurants and retail usually trade at lower multiples because of margin volatility and owner dependency.

Owners who scale with a future sale in mind focus on three things. First, getting EBITDA above $2 million, which moves the business from SDE multiples to EBITDA multiples and usually unlocks better pricing. Second, building recurring revenue, which is the single most powerful multiple driver in most industries. Third, reducing owner dependency so the business can run without the founder, which is what institutional buyers require.

How to Quickly Value a Small Business

To quickly value a small business, calculate Seller's Discretionary Earnings or EBITDA, then apply the typical industry multiple to that number. For most small businesses under $5 million in revenue, the SDE method works. For businesses above that, EBITDA multiples are more accurate. A quick estimate uses the formula: business value = SDE x industry multiple, where the industry multiple typically falls between 1.5x and 4.5x for owner-operated businesses.

According to Elite Exit Advisors data covering 2021 through 2025 transactions, the overall market average SDE multiple is 2.57x, with the typical range running 2.0x to 3.6x. According to BizBuySell data cited by Sundance Financial, the 2025 overall average across all industries was approximately 2.5x SDE based on 9,500 reported transactions. Higher-than-average multiples apply when the business has recurring revenue, clean books, low owner dependency, or strong growth. Lower-than-average multiples apply when the business has customer concentration, weak margins, or messy financials.

The quick formula gets you a ballpark. A serious valuation requires a more careful analysis of working capital, deferred revenue, customer concentration, tax structure, real estate, and other adjustments. For owners thinking about scaling toward a sale in the next 3 to 5 years, the most valuable exercise is identifying the gaps between today's business and what a buyer would want to see. Closing those gaps typically adds 1x to 2x to the multiple, which on a $500,000 SDE business is $500,000 to $1 million in additional sale price.

Stages of Business Scaling Compared

Most small businesses move through predictable scaling stages, each with its own challenges, focus areas, and financial profile. Knowing which stage you are in helps prioritize the right work and avoid the common mistakes of trying to skip a stage. The table below outlines the four stages most small businesses go through on the path to a mature, scalable operation.

StageTypical RevenueMain FocusCommon MistakeStartupUnder $250,000Product-market fit, first customersScaling before finding fitEarly Growth$250K to $1MRepeatable sales, first hiresOwner doing every jobScaling$1M to $10MSystems, team, cash disciplineSkipping the financial infrastructureMature Scale$10M and aboveLeadership, strategy, exit prepFounder stays too operational

Sources: U.S. Bureau of Labor Statistics 2025 small business survival data, BizBuySell 2025 transaction analysis, Federal Reserve 2025 Small Business Credit Survey, Verne Harnish Scaling Up methodology.

Most owners we work with hit a wall somewhere between early growth and scaling. The financial infrastructure that worked at $500,000 in revenue cannot handle $3 million. The hiring approach that produced the first few employees breaks down by the time the team reaches 15. Each stage requires its own discipline, and bringing in proper growth planning early often shortens the time to the next stage by months or even years.

Financial Discipline That Makes Scaling Possible

The financial discipline that makes scaling possible includes monthly close within 5 business days, weekly cash flow review, quarterly strategic planning sessions, clean bookkeeping that produces accurate reports, and proactive tax planning that protects margin. Without this foundation, scaling efforts almost always run into surprise tax bills, cash crunches, or financial blind spots that derail the growth plan.

According to Kaplan Group 2025 small business data, 75% of firms cite rising costs of goods, services, or wages as their primary financial challenge. The owners who handle those rising costs without losing margin are the ones who track them monthly, adjust pricing as needed, and use cost control as an active part of their financial management. According to the Federal Reserve's 2025 Small Business Credit Survey, 51% of small businesses face uneven cash flow, which is one of the biggest barriers to scaling because uneven cash makes it hard to invest in growth confidently.

We see this pattern with growing businesses in Miami and across the country. The owners who scale most successfully are the ones who treat financial management like a strategic function, not an afterthought. That usually means working with a CPA or fractional CFO who reviews the numbers monthly, builds forward forecasts, and helps make the big decisions with data rather than gut feel. Our virtual CFO engagements often start exactly at this inflection point, where the owner realizes that scaling further requires financial leadership the bookkeeper alone cannot provide.

When to Bring in Professional Support for Scaling

The clearest signs you need professional support for scaling are revenue growth that is not translating to profit growth, financial data that is too messy or delayed to drive decisions, plans to hire or expand without a clear budget, an upcoming bank loan or investor conversation, and a sense that the business has grown faster than the systems can handle.

Professional support takes several forms. A bookkeeper handles daily transactions and basic reporting. A CPA handles tax compliance and strategic tax planning. A virtual CFO handles financial strategy, cash flow forecasting, and decision support. A business consultant or advisor handles operational and strategic planning. Most growing small businesses need at least two of these, and the more complex the business gets, the more roles become necessary.

According to research from BCL India and other sources, the virtual CFO services market is growing at roughly 15.6% per year as more businesses adopt this model. The reason is simple: scaling without senior financial guidance is risky, and full-time CFOs cost $300,000 or more in total compensation. A fractional or virtual model gives growing businesses the same expertise for $3,000 to $10,000 per month. Strong business planning support at this stage often produces the single biggest improvement in scaling speed and quality.

Common Scaling Pitfalls and How to Avoid Them

The common scaling pitfalls are hiring too fast without revenue to support it, hiring too slow and burning out the existing team, scaling marketing spend before unit economics work, taking on debt at the wrong stage, ignoring tax planning until it becomes an emergency, and trying to scale a business that has not yet found product-market fit. Each of these mistakes can take months or years to recover from once made.

Hiring too fast is the most expensive mistake. A new $80,000-per-year hire actually costs $100,000 to $120,000 once benefits, taxes, equipment, and onboarding are factored in. According to Robert Half 2025 hiring research, the fully loaded cost of a new employee runs 1.25 to 1.4 times the base salary. If revenue does not grow fast enough to cover that cost, the business burns cash quickly and may need to lay off the new hire within 6 to 12 months, which damages morale and reputation.

Scaling marketing before unit economics work is the second biggest mistake. If a business does not yet know its customer acquisition cost and lifetime value, pouring money into ads just produces faster losses. The path forward is to test marketing on a small budget, prove the unit economics, then scale spend only after the math works. Strong startup CFO guidance during this phase often prevents the most expensive scaling mistakes before they happen.

Frequently Asked Questions

How Much Is a Business Worth With $500,000 in Sales

A business with $500,000 in sales is typically worth $100,000 to $500,000, depending on profitability and industry. The value comes from earnings, not revenue. If the business produces $100,000 in SDE on $500,000 in revenue, the typical 2.5x SDE multiple puts the value around $250,000. If the business produces only $50,000 in SDE, the value drops closer to $125,000. According to BizBuySell 2025 transaction data, businesses with strong recurring revenue and clean books sell at the higher end of those ranges.

How Much Is a Business Worth With $100,000 a Year

A business worth $100,000 a year in profit is typically valued at $200,000 to $500,000, applying small business SDE multiples of 2x to 5x. The exact number depends on industry, growth rate, owner involvement, and the quality of the financials. A laundromat or storage facility doing $100,000 in SDE might sell for $400,000 to $450,000 because of low owner dependency and recurring revenue. A consulting practice doing $100,000 in SDE might sell for $150,000 to $250,000 because the value walks out the door with the owner.

How Do I Know If My Business Is Ready to Scale

You know your business is ready to scale when you have a repeatable sales process producing predictable revenue, positive unit economics, documented operations, and at least 3 to 6 months of cash reserves to fund the growth investment. Trying to scale before these foundations are in place usually produces chaos rather than growth. According to Federal Reserve 2025 data, only 46% of small employer firms were profitable in 2024, which suggests most businesses are not yet ready to scale and would benefit from stabilizing first.

How Long Does It Take to Scale a Small Business

Scaling a small business typically takes 3 to 7 years from the early growth stage to a mature scaled operation. The exact timeline depends on industry, capital availability, market conditions, and execution quality. According to BLS data, only 35% of small businesses survive past year ten, but the ones that do typically reach scaled operating maturity by year five to seven. Faster scaling is possible in software and digital businesses, where 18 to 36 months is achievable with the right product-market fit.

Should I Take On Debt to Scale

Whether to take on debt to scale depends on the return on the borrowed capital and the cash flow stability of the business. Debt makes sense when the borrowed money will produce a return higher than the interest cost and the business has predictable cash flow to make the payments. Debt does not make sense when the business is still struggling with unit economics or cash flow timing. According to a 2024 Federal Reserve Small Business Credit Survey, only 31% of small business loan applicants received the full amount they requested, which means lenders are being selective and businesses need to present clean financials to qualify.

When Should I Hire My First Employee

You should hire your first employee when you have consistent revenue covering at least 3 months of the fully loaded employee cost, a clearly defined role they can step into, and documented processes for the work they will do. The fully loaded cost runs 1.25 to 1.4 times base salary once benefits, taxes, and equipment are added, according to Robert Half 2025 research. Hiring too early creates cash pressure. Hiring too late leaves the owner stuck doing low-value work that prevents the business from growing.

What Is the Difference Between Growing and Scaling

The difference between growing and scaling is the relationship between revenue and costs. Growing means revenue and costs go up together, so margins stay flat. Scaling means revenue grows faster than costs, so margins expand. Owners who scale successfully build systems, teams, and technology that allow each additional dollar of revenue to require less additional cost than the dollar before it. This is the financial pattern that turns a small business into a real engine of wealth creation.

Putting It All Together

Scaling a small business is not about working harder or growing faster. It is about building the systems, team, financial discipline, and strategy that let revenue grow much faster than costs. The 4 pillars of people, strategy, execution, and cash give you the framework. The specific steps of documented processes, strong hiring, cash flow management, scalable marketing, and smart technology give you the action plan. The valuation knowledge gives you the long-term goal worth scaling toward.

If you are running a growing business and want financial leadership that supports the kind of scaling discipline most owners never reach on their own, we would be glad to help. At NR CPAs & Business Advisors, we work with small businesses and growing companies to build the financial structure, planning rhythm, and long-term strategy that turns growth into real, lasting value. Reach out to our team at (954) 231-6613 to start the conversation.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

Owe The IRS And Can't Pay? Your Options

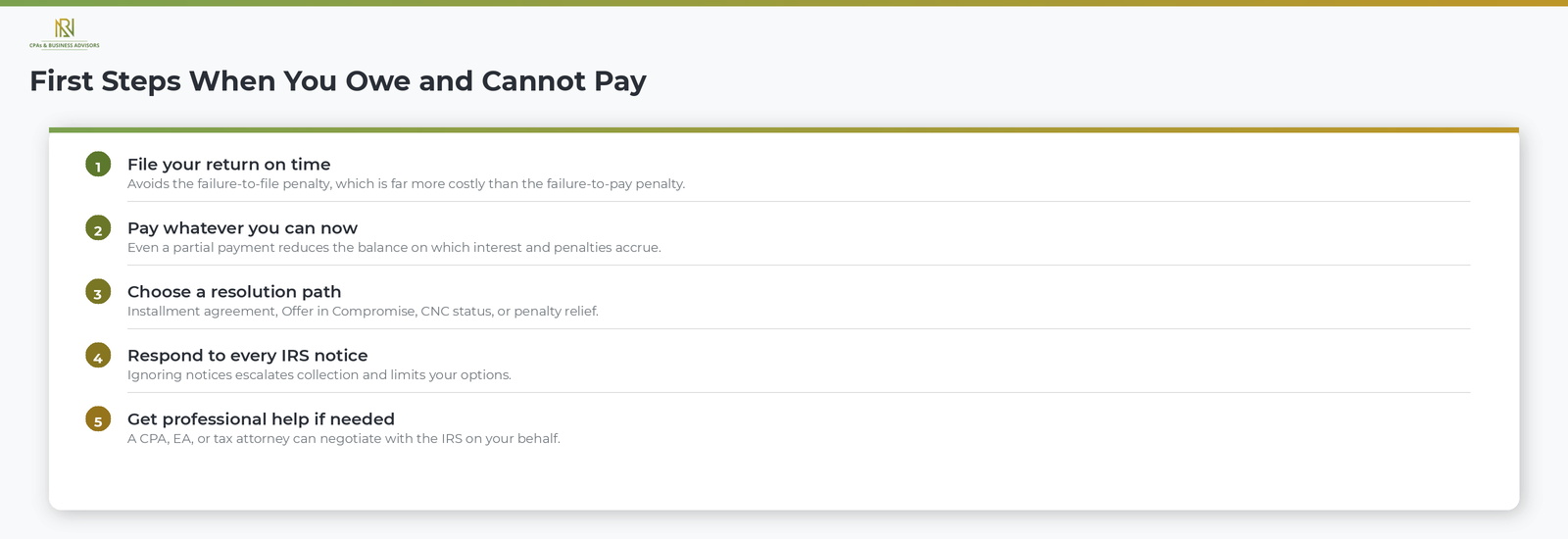

If you owe the IRS and cannot pay the full amount, the most important step you can take is to file your return on time and pay as much as you can, even if that amount is far less than what you owe. According to the IRS, filing on time avoids the failure-to-file penalty, which is significantly more expensive than the failure-to-pay penalty. Paying even a partial amount reduces the balance on which the IRS calculates interest and penalties, which means the total debt grows more slowly than it would if you paid nothing at all.

The IRS does not expect every taxpayer to pay in full on the due date. According to the IRS, the agency offers several programs specifically designed for taxpayers who owe but cannot pay, and most of these options are available whether your debt is recent or has been accumulating for years. The worst action you can take is no action. Ignoring a tax debt does not make it go away. Instead, it triggers an escalating series of IRS collection notices that can eventually result in wage garnishments, bank account levies, property seizures, and federal tax liens that damage your credit. For a full breakdown of how the IRS notice sequence works, our complete guide to IRS correspondence explains every stage from balance due reminders to final enforcement.

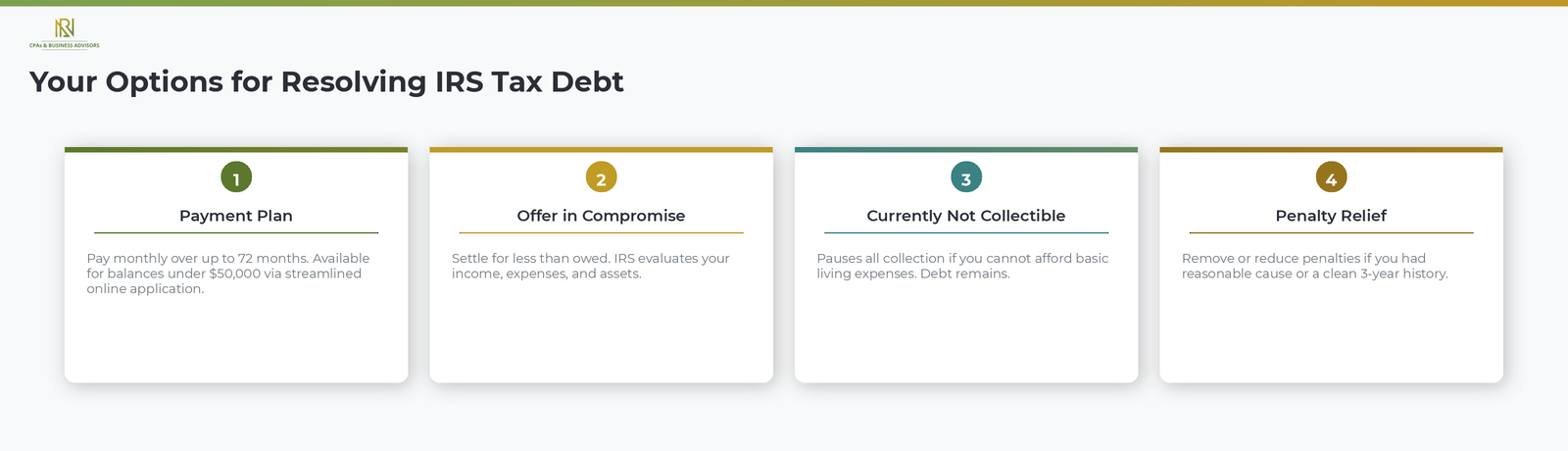

Your Options For Resolving IRS Tax Debt

The IRS provides four primary paths for taxpayers who owe but cannot pay in full: installment agreements, Offers in Compromise, Currently Not Collectible status, and penalty relief. The right option depends on how much you owe, how much you can afford to pay each month, and whether you are experiencing financial hardship.

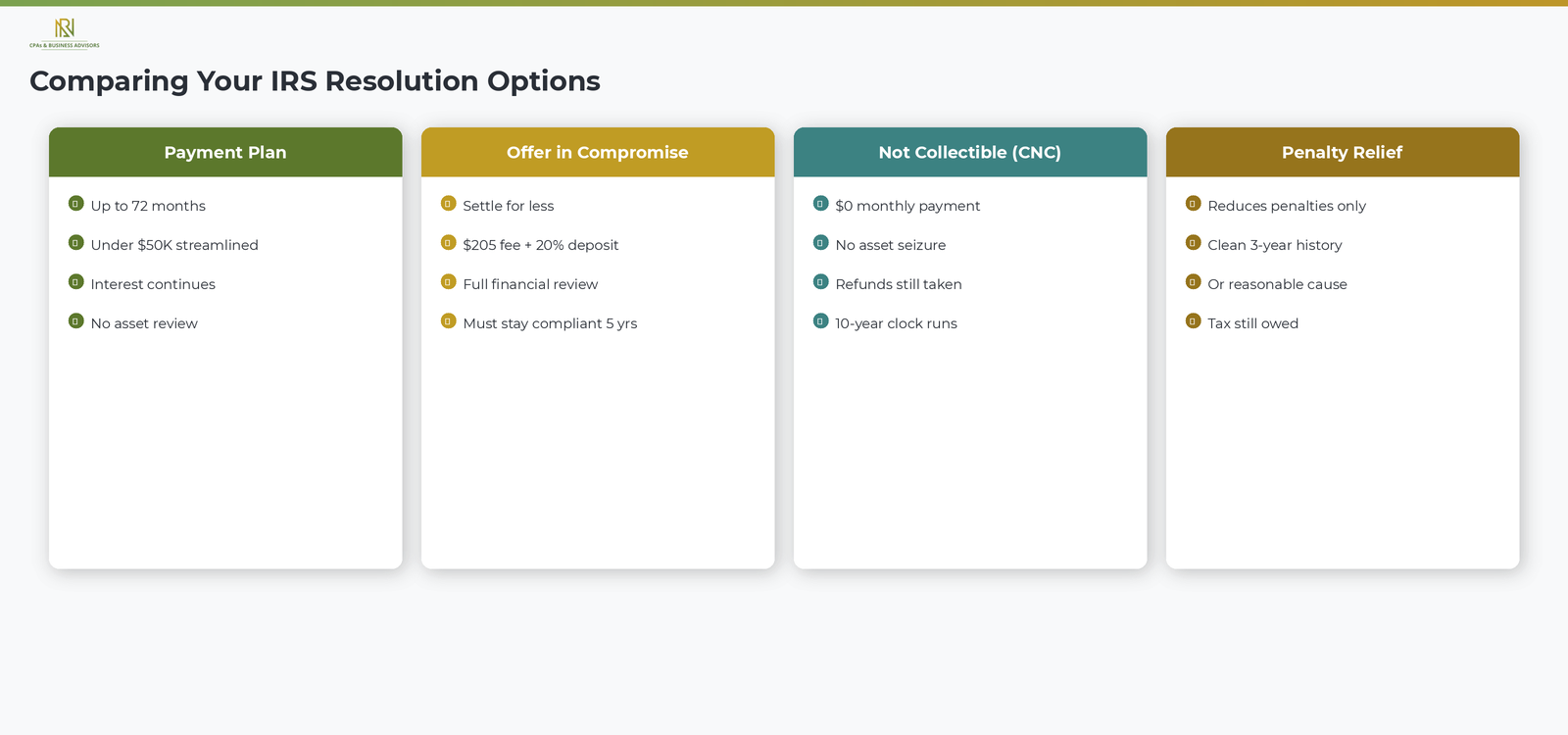

Payment Plans And Installment Agreements

An installment agreement allows you to pay your tax debt in monthly installments over time instead of all at once. According to the IRS, two types of plans are available. A short-term payment plan gives you up to 180 days to pay the full balance, with no setup fee if you apply online. A long-term installment agreement spreads payments across up to 72 months and is available to taxpayers who owe less than $50,000 in combined tax, penalties, and interest. According to the IRS, taxpayers who owe $50,000 or less can apply for a streamlined installment agreement through the IRS Online Payment Agreement tool without providing detailed financial documentation. Our step-by-step guide to installment agreements covers the full application process, balance thresholds, and how interest is calculated on the remaining amount.

Offer In Compromise

An Offer in Compromise allows you to settle your tax debt for less than the full amount you owe. According to the IRS, the agency considers your ability to pay, your income, your expenses, and your asset equity when deciding whether to accept an offer. The IRS generally approves an offer when the amount you propose represents the most the agency can expect to collect within a reasonable period. To apply, you submit Form 656 along with a $205 application fee and an initial payment. Low-income taxpayers who meet the IRS certification guidelines are exempt from both the fee and the initial payment. According to the IRS, you can check your eligibility using the Offer in Compromise Pre-Qualifier tool on IRS.gov before applying.

Currently Not Collectible Status

If your income is so low that you cannot afford to pay anything toward your tax debt without failing to meet basic living expenses, you may qualify for Currently Not Collectible status. According to the IRS, this designation temporarily pauses all collection activity on your account, including levies and garnishments. The tax debt does not go away, and interest and penalties continue to accrue, but the IRS will not take enforcement action while you remain in this status. According to the IRS, the agency will take your future tax refunds and apply them to the balance, and if you owe more than $10,000, the IRS will generally file a Notice of Federal Tax Lien. The IRS reviews your financial situation periodically and may resume collection activity if your income improves.

An important feature of Currently Not Collectible status is that it does not stop the IRS's 10-year statute of limitations on collecting a tax debt. According to the IRS, the agency generally has 10 years from the date a tax debt is assessed to collect it. If the statute expires while your account is in Currently Not Collectible status, the debt is written off permanently.

Penalty Relief

If you owe penalties on top of your tax balance, you may qualify for penalty relief. According to the IRS, the agency can reduce or remove penalties if you tried to comply with the law but were unable to meet your obligations due to circumstances beyond your control, such as a natural disaster, serious illness, or the death of a close family member. First-time penalty abatement is also available to taxpayers who have a clean compliance history for the three prior tax years.

How The IRS Decides Which Option You Qualify For

The IRS evaluates your eligibility for each program based on your total debt, your monthly income and expenses, and the equity in your assets. According to the IRS, the agency uses national and local cost-of-living standards to determine what constitutes a reasonable monthly expense. If your income exceeds your allowable expenses, the IRS expects you to put the difference toward your tax debt through a payment plan. If your allowable expenses equal or exceed your income and you have no significant assets, you may qualify for Currently Not Collectible status or an Offer in Compromise.

Taxpayers facing financial hardship may also qualify for the IRS Fresh Start program, which broadens the eligibility criteria for installment agreements, reduces the threshold for streamlined applications, and makes it easier to qualify for lien withdrawals after meeting certain conditions. The Fresh Start program is not a separate application. It is a set of expanded guidelines the IRS applies to existing resolution options.

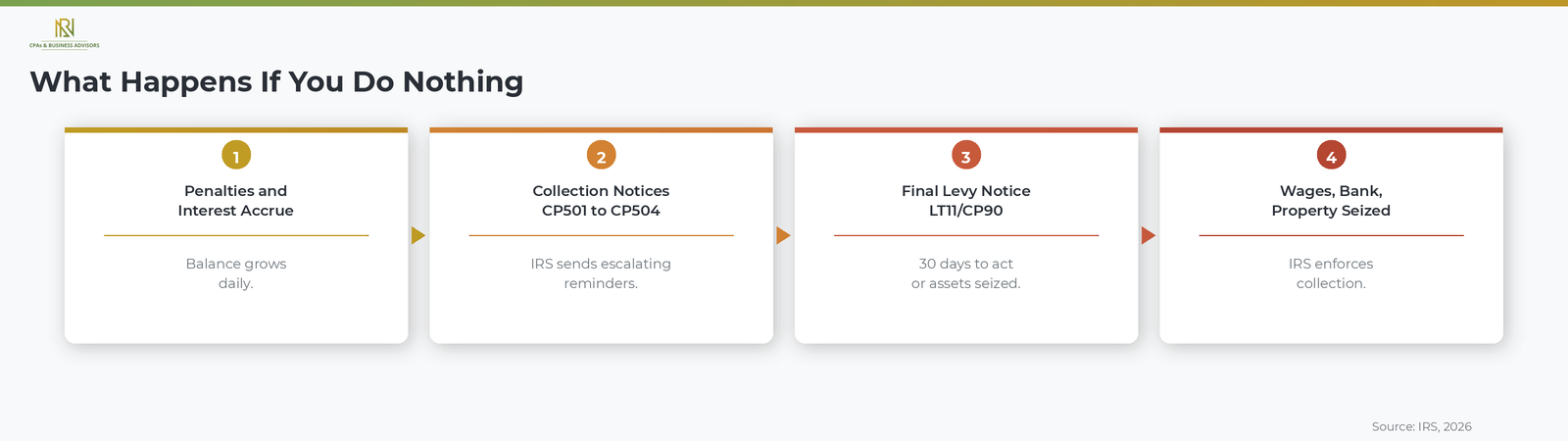

What Happens If You Do Nothing

Doing nothing when you owe the IRS causes penalties and interest to compound daily on your unpaid balance and moves your account through an escalating collection process that can result in the IRS seizing your income and property. According to the IRS, the standard collection sequence begins with a CP14 balance due notice and progresses through CP501 and CP503 reminders, a CP504 Notice of Intent to Levy, and finally an LT11 or CP90 Final Notice of Intent to Levy. At the final notice stage, the IRS is authorized to levy your wages, bank accounts, personal property, and up to 15 percent of your Social Security benefits. Taxpayers who want to understand the full enforcement timeline can review our guide to the LT11 final levy notice.

In addition to levies, the IRS can file a Notice of Federal Tax Lien at any point after a balance remains unpaid. A lien is a public record that establishes the government's legal claim against your assets, can severely damage your credit, and makes it difficult to sell or refinance property. The FAST Act also authorizes the State Department to deny, revoke, or limit your passport if your tax debt meets the threshold for seriously delinquent tax debt.

When To Get Professional Help

Consider working with a CPA, Enrolled Agent, or tax attorney if your tax debt is large, if you are facing active collection action such as a levy or lien, or if you are unsure which resolution option is right for your financial situation. A qualified tax professional can analyze your income, expenses, and assets, determine which IRS program gives you the best outcome, and negotiate directly with the IRS on your behalf. According to the IRS, you can authorize a representative by filing Form 2848, Power of Attorney and Declaration of Representative.

Frequently Asked Questions About Owing The IRS

What Happens If I Owe The IRS More Than $50,000?

You can still set up a payment plan, but you will need to provide detailed financial information to the IRS. According to the IRS, the streamlined installment agreement is only available for balances of $50,000 or less. For larger amounts, you may need to submit Form 433-A (Collection Information Statement) and work directly with the IRS to negotiate terms. An Offer in Compromise may also be an option if the full balance is uncollectible.

Does The IRS Forgive Tax Debt?

The IRS does not automatically forgive tax debt, but it does offer programs that can reduce or eliminate what you owe. An Offer in Compromise allows you to settle for less than the full amount. Currently Not Collectible status pauses collection, and the 10-year statute of limitations on collections means the debt can expire if the IRS does not collect it within that window.

Can I Negotiate With The IRS On My Own?

Yes, you can negotiate directly with the IRS without hiring a representative. According to the IRS, you can apply for payment plans online, submit an Offer in Compromise yourself, and request Currently Not Collectible status by calling the number on your notice. However, taxpayers with complex situations, large balances, or active enforcement actions often benefit from professional representation.

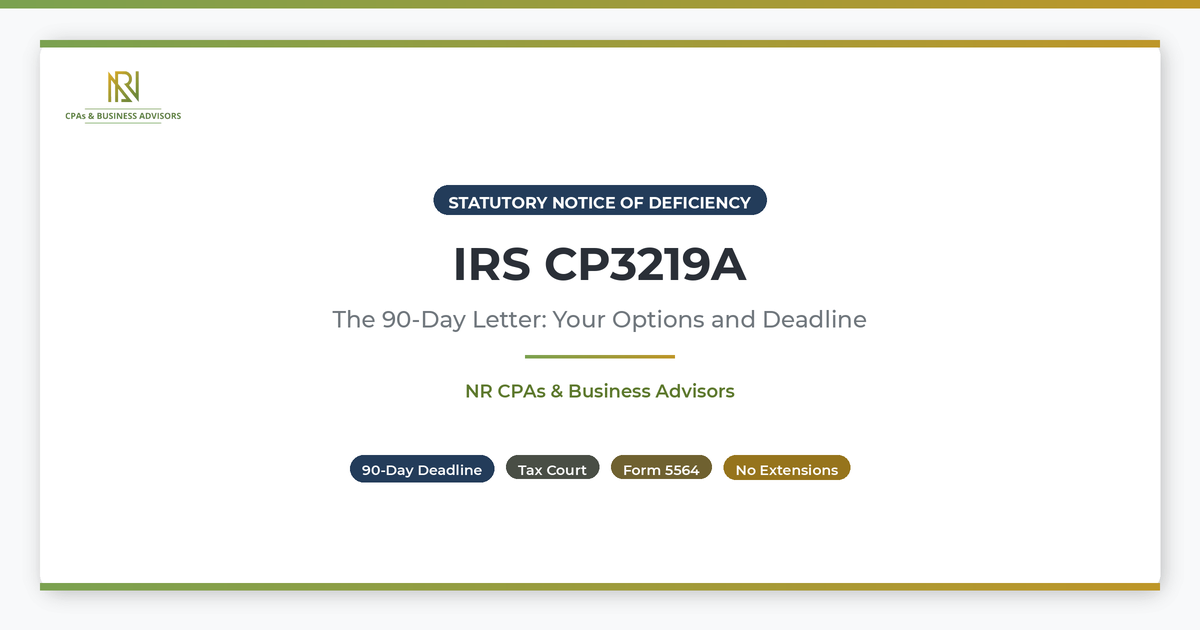

IRS CP3219A: Statutory Notice Of Deficiency (90-Day Letter)

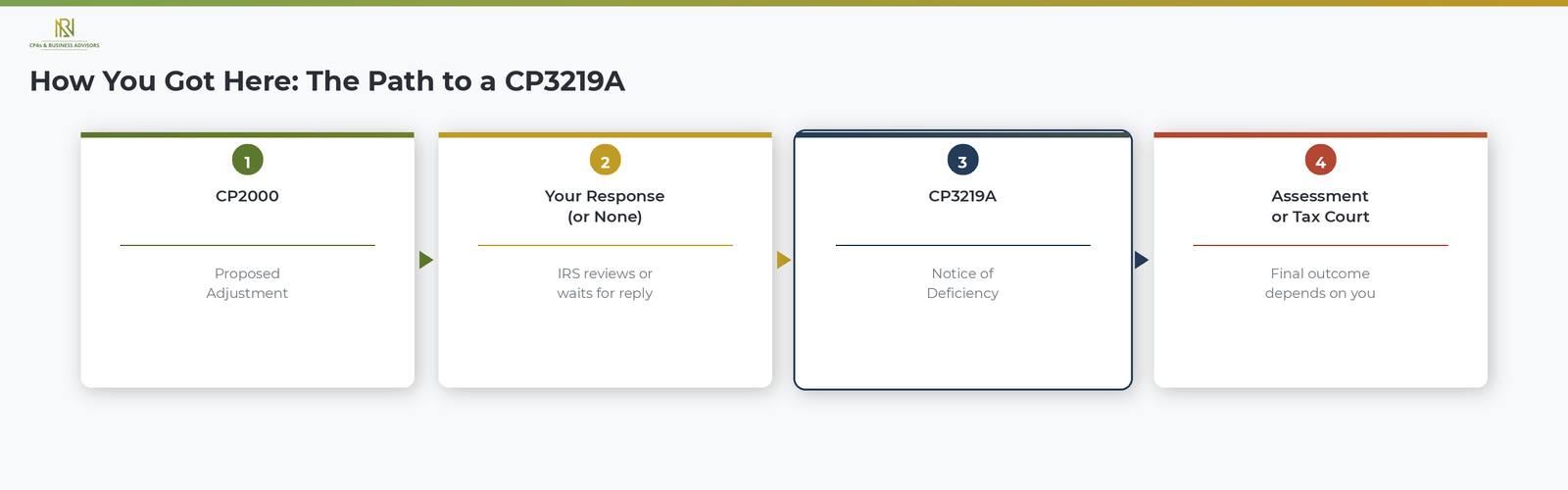

An IRS CP3219A is a Statutory Notice of Deficiency, also known as a 90-day letter, that formally notifies you the IRS is proposing to increase your income tax for a specific tax year. According to the IRS, this notice is issued when the agency found differences between what you reported on your tax return and the information it received from employers, banks, and other third parties. The CP3219A is not a bill and it is not an audit. It is a legal notice that explains the proposed change, how the amount was calculated, and your right to challenge the decision in U.S. Tax Court before the proposed tax becomes an assessed balance.

The CP3219A is one of the most consequential notices the IRS issues because it is the last step before the proposed tax increase is finalized. If you do not respond within the deadline printed on the notice, the IRS will assess the additional tax, add penalties and interest, and send you a bill. At that point, disputing the amount becomes significantly more difficult. For a broader overview of how all IRS notices work and what different types mean, our complete guide to IRS correspondence covers every category from balance due reminders to enforcement actions.

Why You Received A CP3219A

You received a CP3219A because the IRS previously contacted you about an income discrepancy on your tax return and either did not receive a response or was unable to reach an agreement with you. According to the IRS, the CP3219A is typically the final notice in a sequence that begins with a CP2000, which is a proposed adjustment notice the IRS sends when third-party information does not match what you reported. Taxpayers who want to understand the CP2000 and how the IRS identifies income discrepancies can review our full guide to the CP2000 underreporter notice.

The most common reasons the IRS issues a CP3219A include the following.

- No response to prior notices. The IRS sent a CP2000 or related correspondence and did not receive a reply within the response window.

- Unresolved disagreement. You responded to the CP2000 but the IRS did not accept your explanation, and the proposed adjustment remains in dispute.

- Unreported income. Wages, investment earnings, retirement distributions, or other income reported to the IRS by third parties does not appear on your tax return.

- Incorrect credits or deductions. The IRS believes you claimed credits or deductions that the available records do not support.

The 90 Day Deadline And Why It Cannot Be Extended

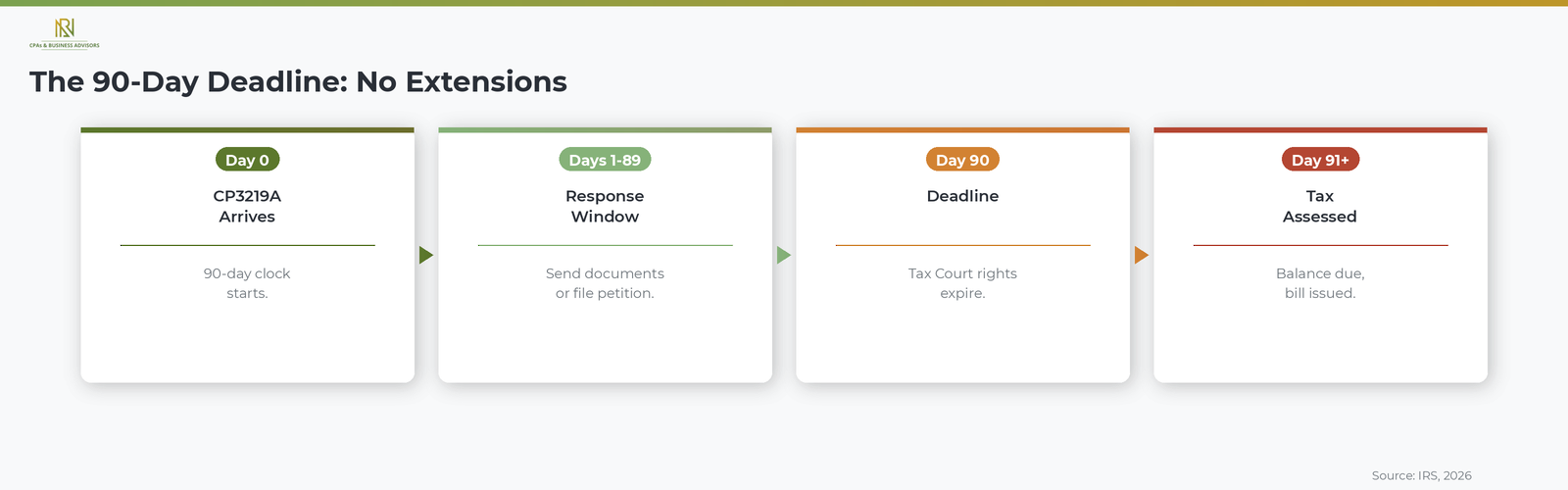

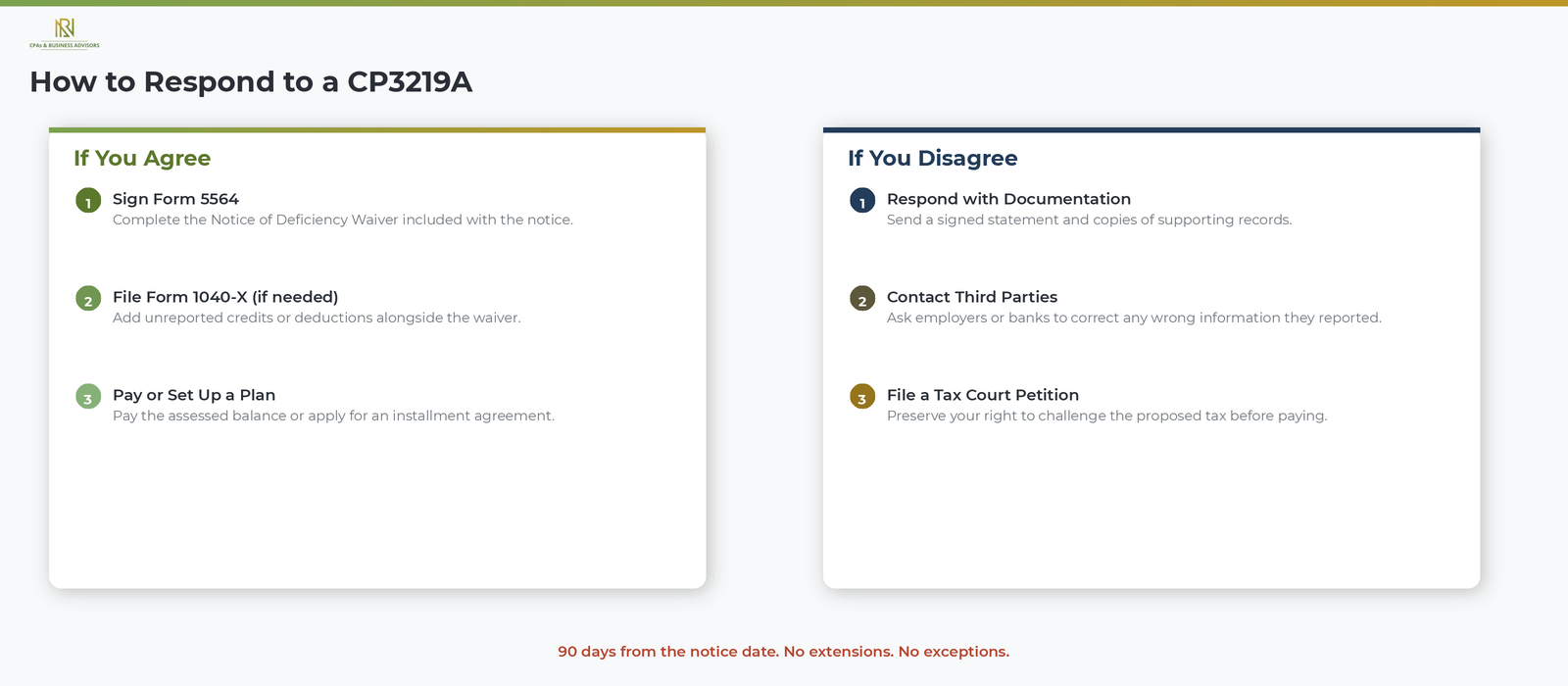

You have exactly 90 days from the date printed on the CP3219A to respond, and this deadline cannot be extended for any reason. According to the IRS, if you are outside the United States when you receive the notice, the deadline is extended to 150 days. This 90-day window is a statutory deadline set by the Internal Revenue Code, which means neither the IRS nor any tax professional can grant additional time.

The 90-day deadline applies to two critical actions: responding to the IRS with documentation that supports your position, and filing a petition with the U.S. Tax Court if you wish to challenge the proposed deficiency. According to the IRS, the Tax Court cannot consider your case if the petition is filed even one day late. For this reason, acting as early as possible within the 90-day window is essential, especially given that IRS processing times for responses can be longer than usual.

How To Respond If You Agree With The Proposed Changes

If you agree that the IRS's proposed tax increase is correct, sign and return the enclosed Form 5564, Notice of Deficiency Waiver, by the deadline. According to the IRS, signing Form 5564 means you accept the proposed changes and waive your right to petition the U.S. Tax Court on those specific items. The IRS will then assess the additional tax along with any applicable penalties and interest.

If the CP3219A is correct but you also have additional income, credits, or deductions that were not included on your original return, you can file Form 1040-X (Amended U.S. Individual Income Tax Return) along with Form 5564. According to the IRS, you should write "CP3219A" on the top of Form 1040-X and submit both forms together. If you owe a balance after the assessment and cannot pay the full amount, you may qualify for a monthly IRS payment plan or installment agreement. Our step-by-step guide to payment plans explains the application process and how interest is calculated on the remaining balance.

How To Respond If You Disagree

If you disagree with the proposed changes, respond to the IRS as soon as possible with documentation that supports your position. According to the IRS, you must include a signed statement explaining why you believe the proposed adjustment is incorrect, along with copies of any supporting records such as corrected W-2s, 1099s, or other income documents.

If the information a third party reported to the IRS is wrong, contact the employer, bank, or institution that filed the incorrect document and ask them to issue a corrected version. According to the IRS, you should notify the agency that you are waiting for the correction so the IRS is aware the issue is being addressed. Keep written records of all communication with the third party in case the correction takes longer than expected.

You can respond by uploading documents through the IRS secure portal (the fastest option), by fax to the number listed on the notice, or by mail to the address on the notice. Regardless of the method you choose, do not wait until the last day. If the IRS has not responded to your submission by the deadline, you may still need to file a Tax Court petition to preserve your rights.

Your Right To Petition The U.S. Tax Court

The CP3219A grants you the legal right to file a petition with the U.S. Tax Court to challenge the proposed deficiency before it becomes an assessed balance. According to the IRS, one of the primary benefits of petitioning the Tax Court is that you can dispute the proposed tax increase without having to pay the amount first. This makes Tax Court the preferred option for taxpayers who disagree with the IRS's calculation but cannot afford to pay and then seek a refund.

To file a petition, visit the U.S. Tax Court website at ustaxcourt.gov and follow the instructions for starting a case. You can file electronically or by mail. The petition must be filed by the date printed on the CP3219A. According to the IRS, the agency will continue to work with you during the 90-day period to resolve the issue, but this does not extend your Tax Court filing deadline.

What Happens If You Miss The 90 Day Deadline

If you do not respond or file a Tax Court petition within 90 days, the IRS will assess the proposed tax increase as a final balance due on your account. According to the IRS, once the assessment is made, the agency will send you a bill for the additional tax, penalties, and interest. At that point, disputing the underlying amount becomes significantly harder because you have lost your right to challenge it in Tax Court without first paying the balance and filing a claim for a refund.

After the assessment, the balance enters the standard IRS collection process. The IRS will send collection notices (CP14, CP501, CP503, CP504) and can eventually pursue enforcement actions including federal tax liens and asset levies if the balance remains unpaid. Acting within the 90-day window is far more protective of your rights and financial options than allowing the deadline to pass.

Frequently Asked Questions About The IRS CP3219A

What Is The Difference Between A CP2000 And A CP3219A?

A CP2000 is a proposed adjustment notice that gives you an opportunity to agree, disagree, or provide additional information before any change is made to your tax. According to the IRS, a CP3219A is the Statutory Notice of Deficiency that the IRS issues if the CP2000 issue remains unresolved. The CP3219A carries legal weight and triggers your right to petition the U.S. Tax Court within 90 days.

Is A CP3219A The Same As An Audit?

No, a CP3219A is not an audit. According to the IRS, the notice is generated by the Automated Underreporter program, which compares the information on your return to data reported by third parties. A formal audit (also called an examination) involves a more detailed review of your return and supporting records.

Can I Get More Time To Respond To A CP3219A?

No, the 90-day deadline on a CP3219A is set by the Internal Revenue Code and cannot be extended. According to the IRS, the only exception is for taxpayers outside the United States, who receive 150 days. There are no other extensions available regardless of the circumstances.