%201.avif)

.png)

.png)

IRS CP3219A: Statutory Notice Of Deficiency (90-Day Letter)

An IRS CP3219A is a Statutory Notice of Deficiency, also known as a 90-day letter, that formally notifies you the IRS is proposing to increase your income tax for a specific tax year. According to the IRS, this notice is issued when the agency found differences between what you reported on your tax return and the information it received from employers, banks, and other third parties. The CP3219A is not a bill and it is not an audit. It is a legal notice that explains the proposed change, how the amount was calculated, and your right to challenge the decision in U.S. Tax Court before the proposed tax becomes an assessed balance.

The CP3219A is one of the most consequential notices the IRS issues because it is the last step before the proposed tax increase is finalized. If you do not respond within the deadline printed on the notice, the IRS will assess the additional tax, add penalties and interest, and send you a bill. At that point, disputing the amount becomes significantly more difficult. For a broader overview of how all IRS notices work and what different types mean, our complete guide to IRS correspondence covers every category from balance due reminders to enforcement actions.

Why You Received A CP3219A

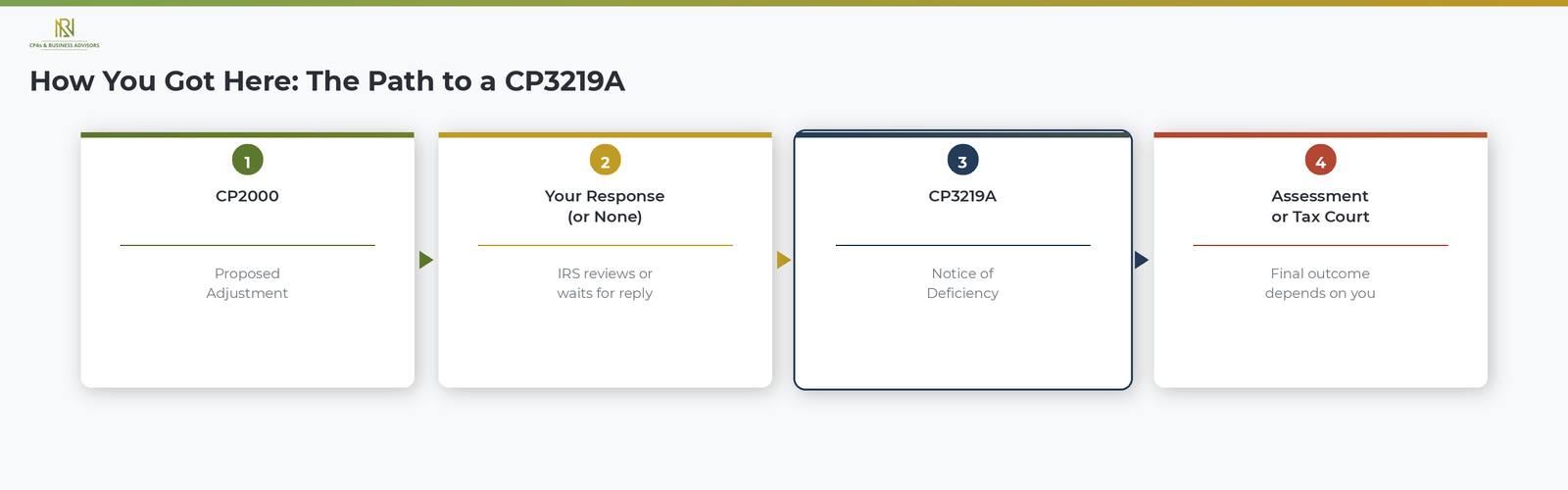

You received a CP3219A because the IRS previously contacted you about an income discrepancy on your tax return and either did not receive a response or was unable to reach an agreement with you. According to the IRS, the CP3219A is typically the final notice in a sequence that begins with a CP2000, which is a proposed adjustment notice the IRS sends when third-party information does not match what you reported. Taxpayers who want to understand the CP2000 and how the IRS identifies income discrepancies can review our full guide to the CP2000 underreporter notice.

The most common reasons the IRS issues a CP3219A include the following.

- No response to prior notices. The IRS sent a CP2000 or related correspondence and did not receive a reply within the response window.

- Unresolved disagreement. You responded to the CP2000 but the IRS did not accept your explanation, and the proposed adjustment remains in dispute.

- Unreported income. Wages, investment earnings, retirement distributions, or other income reported to the IRS by third parties does not appear on your tax return.

- Incorrect credits or deductions. The IRS believes you claimed credits or deductions that the available records do not support.

The 90 Day Deadline And Why It Cannot Be Extended

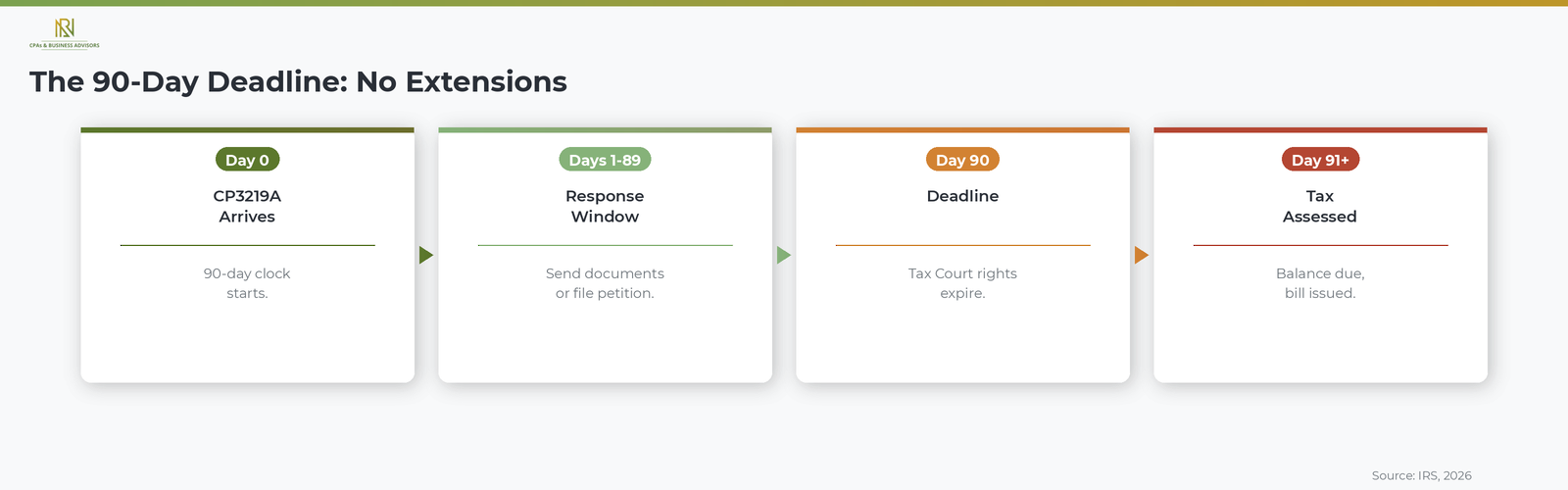

You have exactly 90 days from the date printed on the CP3219A to respond, and this deadline cannot be extended for any reason. According to the IRS, if you are outside the United States when you receive the notice, the deadline is extended to 150 days. This 90-day window is a statutory deadline set by the Internal Revenue Code, which means neither the IRS nor any tax professional can grant additional time.

The 90-day deadline applies to two critical actions: responding to the IRS with documentation that supports your position, and filing a petition with the U.S. Tax Court if you wish to challenge the proposed deficiency. According to the IRS, the Tax Court cannot consider your case if the petition is filed even one day late. For this reason, acting as early as possible within the 90-day window is essential, especially given that IRS processing times for responses can be longer than usual.

How To Respond If You Agree With The Proposed Changes

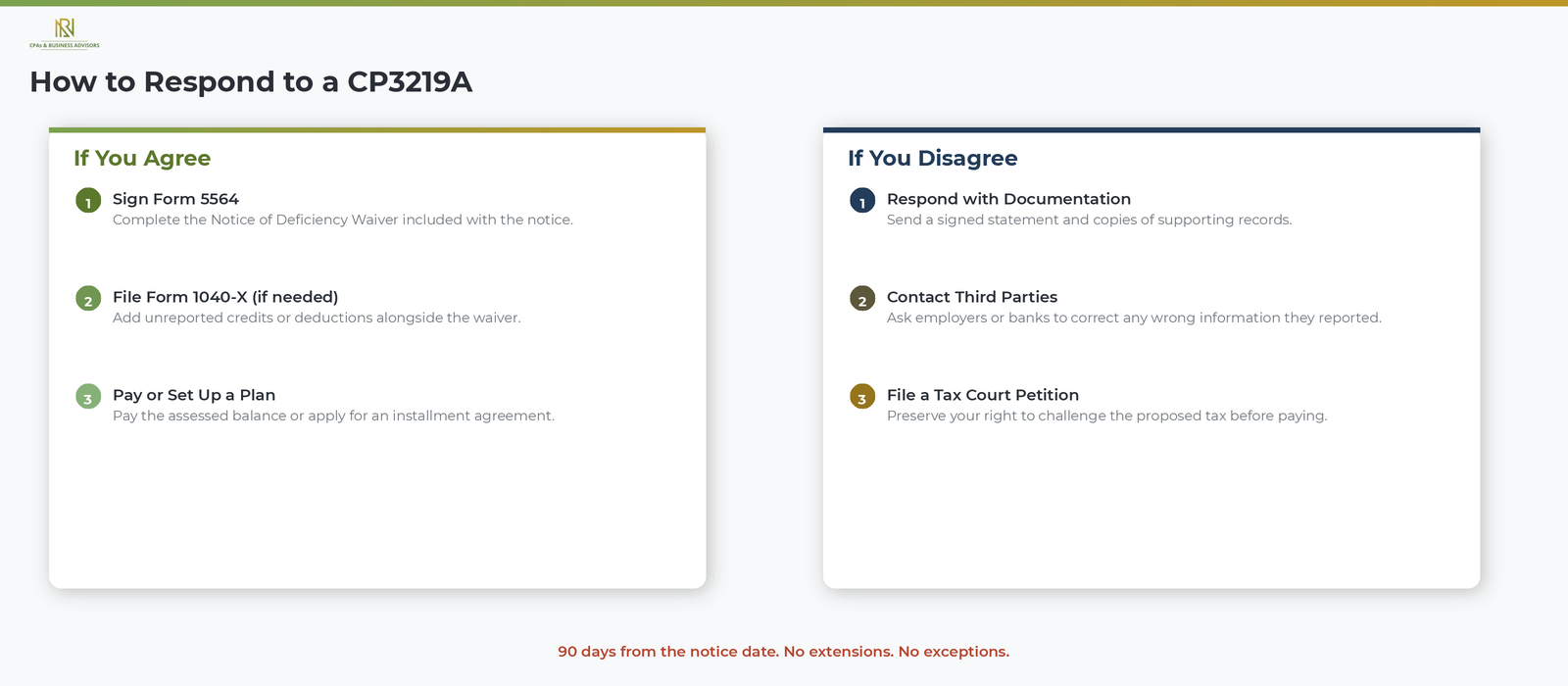

If you agree that the IRS's proposed tax increase is correct, sign and return the enclosed Form 5564, Notice of Deficiency Waiver, by the deadline. According to the IRS, signing Form 5564 means you accept the proposed changes and waive your right to petition the U.S. Tax Court on those specific items. The IRS will then assess the additional tax along with any applicable penalties and interest.

If the CP3219A is correct but you also have additional income, credits, or deductions that were not included on your original return, you can file Form 1040-X (Amended U.S. Individual Income Tax Return) along with Form 5564. According to the IRS, you should write "CP3219A" on the top of Form 1040-X and submit both forms together. If you owe a balance after the assessment and cannot pay the full amount, you may qualify for a monthly IRS payment plan or installment agreement. Our step-by-step guide to payment plans explains the application process and how interest is calculated on the remaining balance.

How To Respond If You Disagree

If you disagree with the proposed changes, respond to the IRS as soon as possible with documentation that supports your position. According to the IRS, you must include a signed statement explaining why you believe the proposed adjustment is incorrect, along with copies of any supporting records such as corrected W-2s, 1099s, or other income documents.

If the information a third party reported to the IRS is wrong, contact the employer, bank, or institution that filed the incorrect document and ask them to issue a corrected version. According to the IRS, you should notify the agency that you are waiting for the correction so the IRS is aware the issue is being addressed. Keep written records of all communication with the third party in case the correction takes longer than expected.

You can respond by uploading documents through the IRS secure portal (the fastest option), by fax to the number listed on the notice, or by mail to the address on the notice. Regardless of the method you choose, do not wait until the last day. If the IRS has not responded to your submission by the deadline, you may still need to file a Tax Court petition to preserve your rights.

Your Right To Petition The U.S. Tax Court

The CP3219A grants you the legal right to file a petition with the U.S. Tax Court to challenge the proposed deficiency before it becomes an assessed balance. According to the IRS, one of the primary benefits of petitioning the Tax Court is that you can dispute the proposed tax increase without having to pay the amount first. This makes Tax Court the preferred option for taxpayers who disagree with the IRS's calculation but cannot afford to pay and then seek a refund.

To file a petition, visit the U.S. Tax Court website at ustaxcourt.gov and follow the instructions for starting a case. You can file electronically or by mail. The petition must be filed by the date printed on the CP3219A. According to the IRS, the agency will continue to work with you during the 90-day period to resolve the issue, but this does not extend your Tax Court filing deadline.

What Happens If You Miss The 90 Day Deadline

If you do not respond or file a Tax Court petition within 90 days, the IRS will assess the proposed tax increase as a final balance due on your account. According to the IRS, once the assessment is made, the agency will send you a bill for the additional tax, penalties, and interest. At that point, disputing the underlying amount becomes significantly harder because you have lost your right to challenge it in Tax Court without first paying the balance and filing a claim for a refund.

After the assessment, the balance enters the standard IRS collection process. The IRS will send collection notices (CP14, CP501, CP503, CP504) and can eventually pursue enforcement actions including federal tax liens and asset levies if the balance remains unpaid. Acting within the 90-day window is far more protective of your rights and financial options than allowing the deadline to pass.

Frequently Asked Questions About The IRS CP3219A

What Is The Difference Between A CP2000 And A CP3219A?

A CP2000 is a proposed adjustment notice that gives you an opportunity to agree, disagree, or provide additional information before any change is made to your tax. According to the IRS, a CP3219A is the Statutory Notice of Deficiency that the IRS issues if the CP2000 issue remains unresolved. The CP3219A carries legal weight and triggers your right to petition the U.S. Tax Court within 90 days.

Is A CP3219A The Same As An Audit?

No, a CP3219A is not an audit. According to the IRS, the notice is generated by the Automated Underreporter program, which compares the information on your return to data reported by third parties. A formal audit (also called an examination) involves a more detailed review of your return and supporting records.

Can I Get More Time To Respond To A CP3219A?

No, the 90-day deadline on a CP3219A is set by the Internal Revenue Code and cannot be extended. According to the IRS, the only exception is for taxpayers outside the United States, who receive 150 days. There are no other extensions available regardless of the circumstances.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

IRS CP3219A: Statutory Notice Of Deficiency (90-Day Letter)

An IRS CP3219A is a Statutory Notice of Deficiency, also known as a 90-day letter, that formally notifies you the IRS is proposing to increase your income tax for a specific tax year. According to the IRS, this notice is issued when the agency found differences between what you reported on your tax return and the information it received from employers, banks, and other third parties. The CP3219A is not a bill and it is not an audit. It is a legal notice that explains the proposed change, how the amount was calculated, and your right to challenge the decision in U.S. Tax Court before the proposed tax becomes an assessed balance.

The CP3219A is one of the most consequential notices the IRS issues because it is the last step before the proposed tax increase is finalized. If you do not respond within the deadline printed on the notice, the IRS will assess the additional tax, add penalties and interest, and send you a bill. At that point, disputing the amount becomes significantly more difficult. For a broader overview of how all IRS notices work and what different types mean, our complete guide to IRS correspondence covers every category from balance due reminders to enforcement actions.

Why You Received A CP3219A

You received a CP3219A because the IRS previously contacted you about an income discrepancy on your tax return and either did not receive a response or was unable to reach an agreement with you. According to the IRS, the CP3219A is typically the final notice in a sequence that begins with a CP2000, which is a proposed adjustment notice the IRS sends when third-party information does not match what you reported. Taxpayers who want to understand the CP2000 and how the IRS identifies income discrepancies can review our full guide to the CP2000 underreporter notice.

The most common reasons the IRS issues a CP3219A include the following.

- No response to prior notices. The IRS sent a CP2000 or related correspondence and did not receive a reply within the response window.

- Unresolved disagreement. You responded to the CP2000 but the IRS did not accept your explanation, and the proposed adjustment remains in dispute.

- Unreported income. Wages, investment earnings, retirement distributions, or other income reported to the IRS by third parties does not appear on your tax return.

- Incorrect credits or deductions. The IRS believes you claimed credits or deductions that the available records do not support.

The 90 Day Deadline And Why It Cannot Be Extended

You have exactly 90 days from the date printed on the CP3219A to respond, and this deadline cannot be extended for any reason. According to the IRS, if you are outside the United States when you receive the notice, the deadline is extended to 150 days. This 90-day window is a statutory deadline set by the Internal Revenue Code, which means neither the IRS nor any tax professional can grant additional time.

The 90-day deadline applies to two critical actions: responding to the IRS with documentation that supports your position, and filing a petition with the U.S. Tax Court if you wish to challenge the proposed deficiency. According to the IRS, the Tax Court cannot consider your case if the petition is filed even one day late. For this reason, acting as early as possible within the 90-day window is essential, especially given that IRS processing times for responses can be longer than usual.

How To Respond If You Agree With The Proposed Changes

If you agree that the IRS's proposed tax increase is correct, sign and return the enclosed Form 5564, Notice of Deficiency Waiver, by the deadline. According to the IRS, signing Form 5564 means you accept the proposed changes and waive your right to petition the U.S. Tax Court on those specific items. The IRS will then assess the additional tax along with any applicable penalties and interest.

If the CP3219A is correct but you also have additional income, credits, or deductions that were not included on your original return, you can file Form 1040-X (Amended U.S. Individual Income Tax Return) along with Form 5564. According to the IRS, you should write "CP3219A" on the top of Form 1040-X and submit both forms together. If you owe a balance after the assessment and cannot pay the full amount, you may qualify for a monthly IRS payment plan or installment agreement. Our step-by-step guide to payment plans explains the application process and how interest is calculated on the remaining balance.

How To Respond If You Disagree

If you disagree with the proposed changes, respond to the IRS as soon as possible with documentation that supports your position. According to the IRS, you must include a signed statement explaining why you believe the proposed adjustment is incorrect, along with copies of any supporting records such as corrected W-2s, 1099s, or other income documents.

If the information a third party reported to the IRS is wrong, contact the employer, bank, or institution that filed the incorrect document and ask them to issue a corrected version. According to the IRS, you should notify the agency that you are waiting for the correction so the IRS is aware the issue is being addressed. Keep written records of all communication with the third party in case the correction takes longer than expected.

You can respond by uploading documents through the IRS secure portal (the fastest option), by fax to the number listed on the notice, or by mail to the address on the notice. Regardless of the method you choose, do not wait until the last day. If the IRS has not responded to your submission by the deadline, you may still need to file a Tax Court petition to preserve your rights.

Your Right To Petition The U.S. Tax Court

The CP3219A grants you the legal right to file a petition with the U.S. Tax Court to challenge the proposed deficiency before it becomes an assessed balance. According to the IRS, one of the primary benefits of petitioning the Tax Court is that you can dispute the proposed tax increase without having to pay the amount first. This makes Tax Court the preferred option for taxpayers who disagree with the IRS's calculation but cannot afford to pay and then seek a refund.

To file a petition, visit the U.S. Tax Court website at ustaxcourt.gov and follow the instructions for starting a case. You can file electronically or by mail. The petition must be filed by the date printed on the CP3219A. According to the IRS, the agency will continue to work with you during the 90-day period to resolve the issue, but this does not extend your Tax Court filing deadline.

What Happens If You Miss The 90 Day Deadline

If you do not respond or file a Tax Court petition within 90 days, the IRS will assess the proposed tax increase as a final balance due on your account. According to the IRS, once the assessment is made, the agency will send you a bill for the additional tax, penalties, and interest. At that point, disputing the underlying amount becomes significantly harder because you have lost your right to challenge it in Tax Court without first paying the balance and filing a claim for a refund.

After the assessment, the balance enters the standard IRS collection process. The IRS will send collection notices (CP14, CP501, CP503, CP504) and can eventually pursue enforcement actions including federal tax liens and asset levies if the balance remains unpaid. Acting within the 90-day window is far more protective of your rights and financial options than allowing the deadline to pass.

Frequently Asked Questions About The IRS CP3219A

What Is The Difference Between A CP2000 And A CP3219A?

A CP2000 is a proposed adjustment notice that gives you an opportunity to agree, disagree, or provide additional information before any change is made to your tax. According to the IRS, a CP3219A is the Statutory Notice of Deficiency that the IRS issues if the CP2000 issue remains unresolved. The CP3219A carries legal weight and triggers your right to petition the U.S. Tax Court within 90 days.

Is A CP3219A The Same As An Audit?

No, a CP3219A is not an audit. According to the IRS, the notice is generated by the Automated Underreporter program, which compares the information on your return to data reported by third parties. A formal audit (also called an examination) involves a more detailed review of your return and supporting records.

Can I Get More Time To Respond To A CP3219A?

No, the 90-day deadline on a CP3219A is set by the Internal Revenue Code and cannot be extended. According to the IRS, the only exception is for taxpayers outside the United States, who receive 150 days. There are no other extensions available regardless of the circumstances.

IRS CP501 & CP503: Balance Reminder Notices

The CP501 and CP503 are IRS balance due reminder notices that the agency sends when you have an unpaid tax balance and have not responded to earlier correspondence. According to the IRS, the CP501 is the first reminder and the CP503 is the second, and both restate the original amount owed plus any additional penalties and interest that have accrued since the initial notice was issued. Neither the CP501 nor the CP503 is a final notice or a threat of immediate enforcement, but ignoring them moves your account closer to active collection actions including levies and liens.

Both notices include the total balance owed, the due date for payment, and the payment options available to you. They also include a toll-free phone number you can call to discuss your account or arrange a resolution. For a broader overview of how all IRS notices work and where these reminders fit in the larger system, our complete guide to IRS correspondence covers every notice category from adjustments to enforcement.

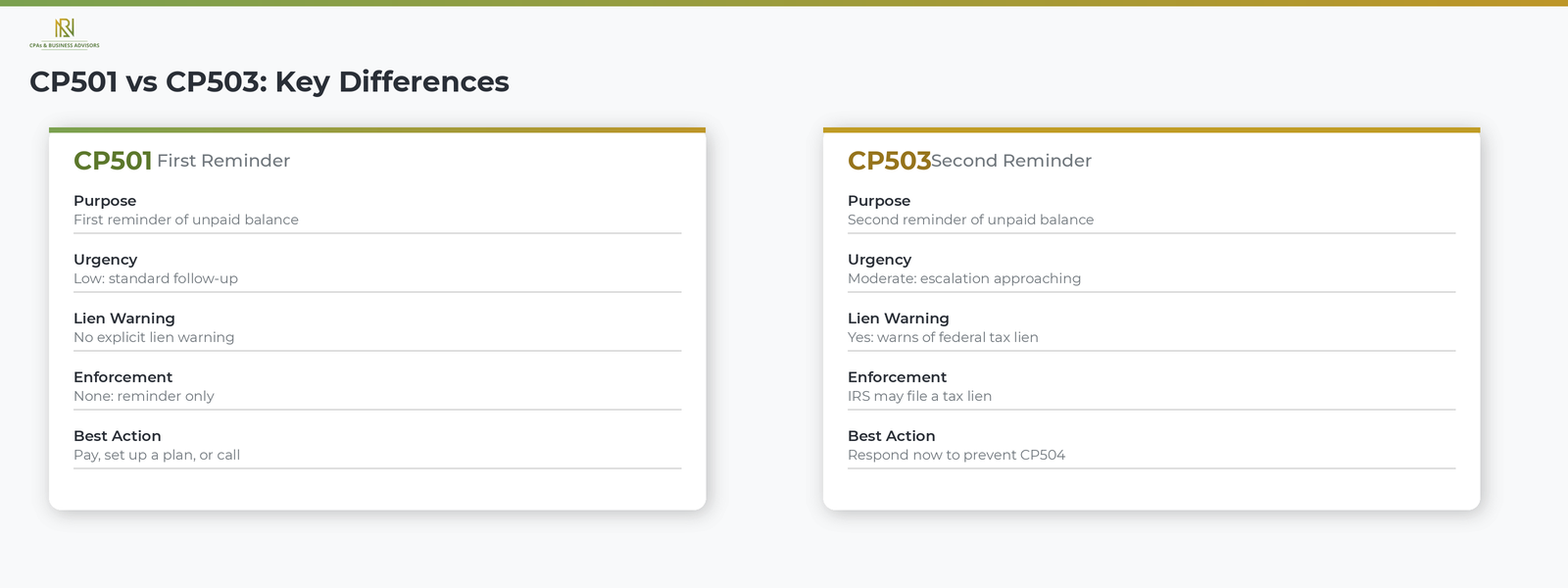

What The CP501 Notice Means

The CP501 is the first reminder the IRS sends after the initial CP14 balance due notice goes unpaid. According to the IRS, you receive a CP501 because the agency has a balance due on one of your tax accounts and has not received payment or a response. The notice restates the amount you owe, including the original tax, any assessed penalties, and interest that has continued to accrue since the CP14 was issued.

The CP501 is not a new assessment or a correction to your return. It is a follow-up to the CP14, which is the first notice the IRS sends when a filed return shows an unpaid balance. Taxpayers who want to understand that initial balance due notice in detail can review our full guide to the CP14 and its response options. At the CP501 stage, you still have the full range of resolution options available, including paying in full, setting up an installment agreement, or disputing the balance if you believe it is incorrect.

What The CP503 Notice Means

The CP503 is the second reminder the IRS sends when the balance from the CP501 remains unpaid and the agency has still not heard from you. According to the IRS, the CP503 carries stronger language than the CP501 and explicitly warns that continued inaction may result in the IRS filing a Notice of Federal Tax Lien. A federal tax lien is a public claim against your current and future assets that can damage your credit, make it difficult to sell or refinance property, and establish the government's legal priority over other creditors.

The structure of the CP503 is nearly identical to the CP501. It lists the total balance owed, the payment due date, available payment options, and the toll-free number for contacting the IRS. The key difference is the escalation in urgency: while the CP501 is a straightforward reminder, the CP503 signals that the IRS is preparing to take more aggressive action if you continue to not respond.

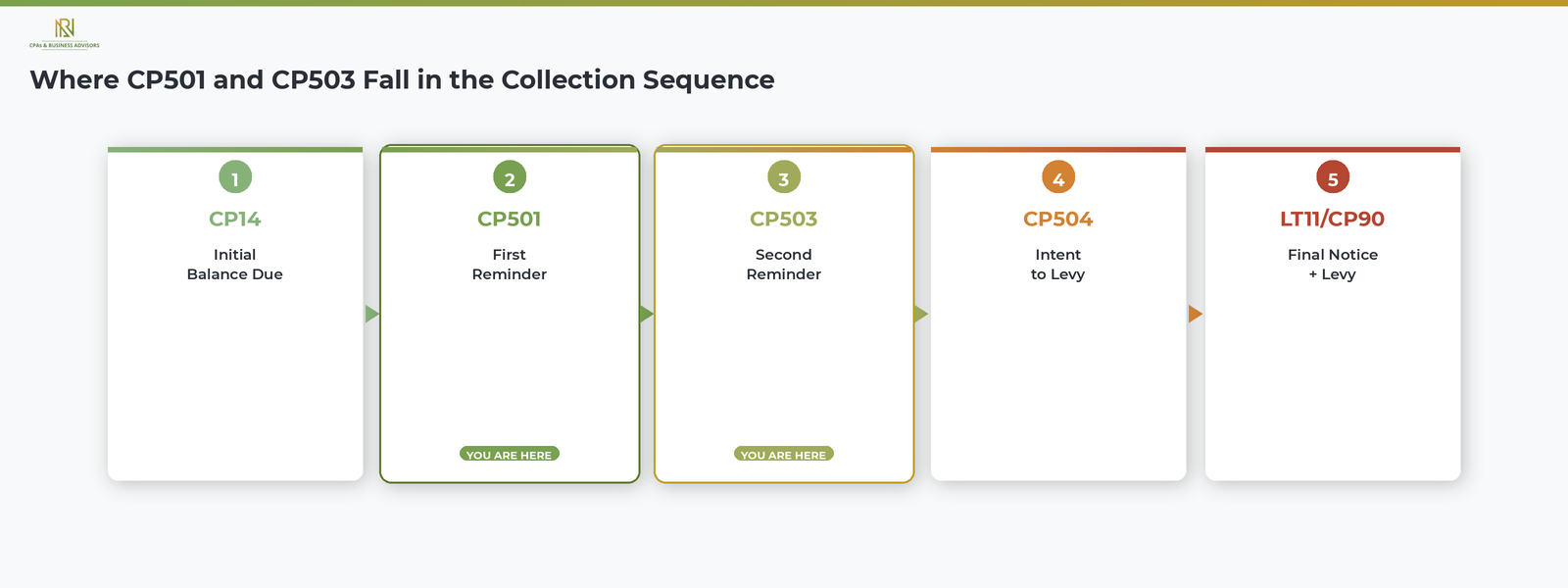

How CP501 And CP503 Fit In The IRS Collection Sequence

The CP501 and CP503 are the second and third steps in a five-step IRS collection sequence that begins with a balance due notice and ends with asset seizure. According to the IRS, the standard progression for an unpaid individual tax balance works as follows.

- CP14: the initial balance due notice, sent after you file a return with an unpaid amount.

- CP501: the first reminder that the balance remains unpaid.

- CP503: the second reminder, with a warning about a potential federal tax lien.

- CP504: the Notice of Intent to Levy, authorizing the IRS to seize your state tax refund. Taxpayers who reach this stage can review our full explanation of the CP504 and how to respond.

- LT11 or CP90: the Final Notice of Intent to Levy, authorizing the IRS to seize wages, bank accounts, and other property.

The CP501 and CP503 represent the window where you have the most options and the least pressure. Penalties and interest continue to accrue at every stage, but no enforcement action, such as a levy or lien, has been initiated yet. Responding at this point is significantly less stressful and more flexible than waiting until the IRS issues a CP504 or final levy notice.

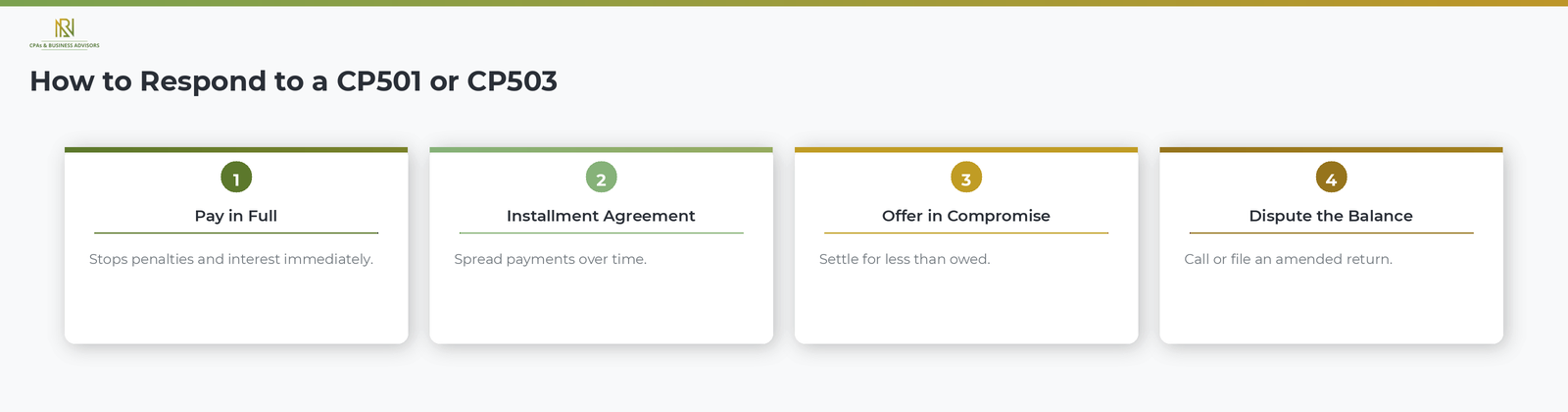

How To Respond To A CP501 Or CP503 Notice

The response process is the same for both the CP501 and the CP503: pay the balance, set up a payment arrangement, or contact the IRS to dispute the amount if you believe it is wrong. Your best option depends on your financial situation.

- Pay the balance in full. The fastest way to stop penalties and interest from continuing to grow. You can pay online at IRS.gov through IRS Direct Pay, by phone, or by mailing a check with the payment voucher from the notice.

- Set up an installment agreement. If you cannot pay the full amount at once, you may qualify for a monthly IRS payment plan or installment agreement that spreads payments over time. Our step-by-step guide to structured payment options covers the application process, balance thresholds, and how interest is calculated.

- Submit an Offer in Compromise. If your financial circumstances make the full balance unlikely to be collected, you may be able to settle for less than you owe.

- Dispute the balance. If you believe the amount is incorrect, call the toll-free number on the notice to discuss your account. If the error relates to income exclusions or credits you did not claim, you may need to file an amended return (Form 1040-X) with the correct information.

Taxpayers experiencing financial hardship may also qualify for the IRS Fresh Start program, which eases the qualification requirements for installment agreements and expands access to penalty relief for eligible individuals and businesses.

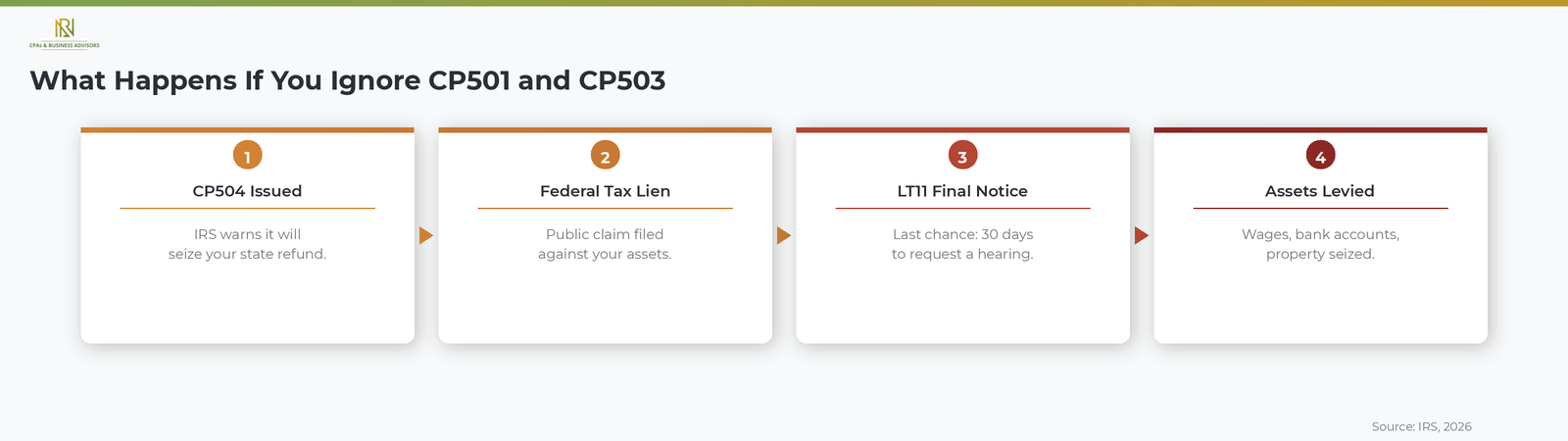

What Happens If You Ignore A CP501 Or CP503

Ignoring a CP501 or CP503 does not make the balance go away. It causes the IRS to escalate to the next stage of collection, where the consequences become significantly more severe. According to the IRS, the next notice after the CP503 is the CP504, which is a formal Notice of Intent to Levy. The CP504 authorizes the IRS to seize your state income tax refund and warns that further enforcement, including levies on wages, bank accounts, and personal property, will follow.

Beyond the CP504, the IRS issues a final notice (LT11 or CP90) that authorizes levies on virtually all of your assets and triggers your right to a Collection Due Process hearing. The IRS can also file a Notice of Federal Tax Lien at any point in this process, which becomes a public record and can affect your credit for years. Penalties and interest continue to accrue throughout the entire sequence, increasing the total amount owed with each month that passes without resolution.

Frequently Asked Questions About CP501 And CP503 Notices

What Is The Difference Between A CP501 And A CP503?

The CP501 is the first reminder and the CP503 is the second. According to the IRS, both notices restate your unpaid balance with updated penalties and interest. The CP503 carries stronger language and explicitly warns that the IRS may file a federal tax lien if you do not respond, while the CP501 does not include that warning.

How Long Do I Have To Respond To A CP501 Or CP503?

Both notices include a specific due date printed on the document, and you should respond by that date to avoid further penalties and escalation. According to the IRS, paying or contacting the agency before the due date on the notice is the most effective way to prevent the next notice in the collection sequence from being issued.

Can The IRS Levy My Assets After A CP501 Or CP503?

No, the IRS cannot levy your assets based on a CP501 or CP503 alone. According to the IRS, the agency must first issue a CP504 (Notice of Intent to Levy) and then a final notice (LT11 or CP90) with Collection Due Process hearing rights before it can proceed with seizing your property. However, the IRS can file a federal tax lien after the CP503 stage without issuing additional notice.