%201.avif)

.png)

.png)

Owe The IRS And Can't Pay? Your Options

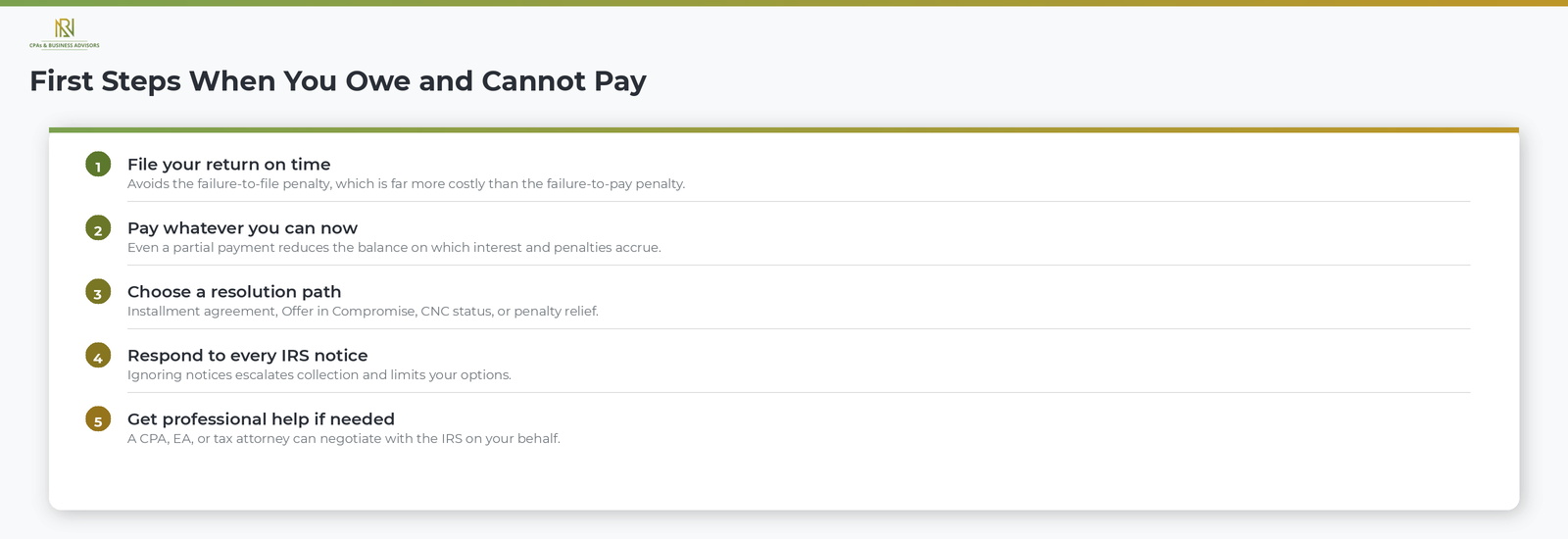

If you owe the IRS and cannot pay the full amount, the most important step you can take is to file your return on time and pay as much as you can, even if that amount is far less than what you owe. According to the IRS, filing on time avoids the failure-to-file penalty, which is significantly more expensive than the failure-to-pay penalty. Paying even a partial amount reduces the balance on which the IRS calculates interest and penalties, which means the total debt grows more slowly than it would if you paid nothing at all.

The IRS does not expect every taxpayer to pay in full on the due date. According to the IRS, the agency offers several programs specifically designed for taxpayers who owe but cannot pay, and most of these options are available whether your debt is recent or has been accumulating for years. The worst action you can take is no action. Ignoring a tax debt does not make it go away. Instead, it triggers an escalating series of IRS collection notices that can eventually result in wage garnishments, bank account levies, property seizures, and federal tax liens that damage your credit. For a full breakdown of how the IRS notice sequence works, our complete guide to IRS correspondence explains every stage from balance due reminders to final enforcement.

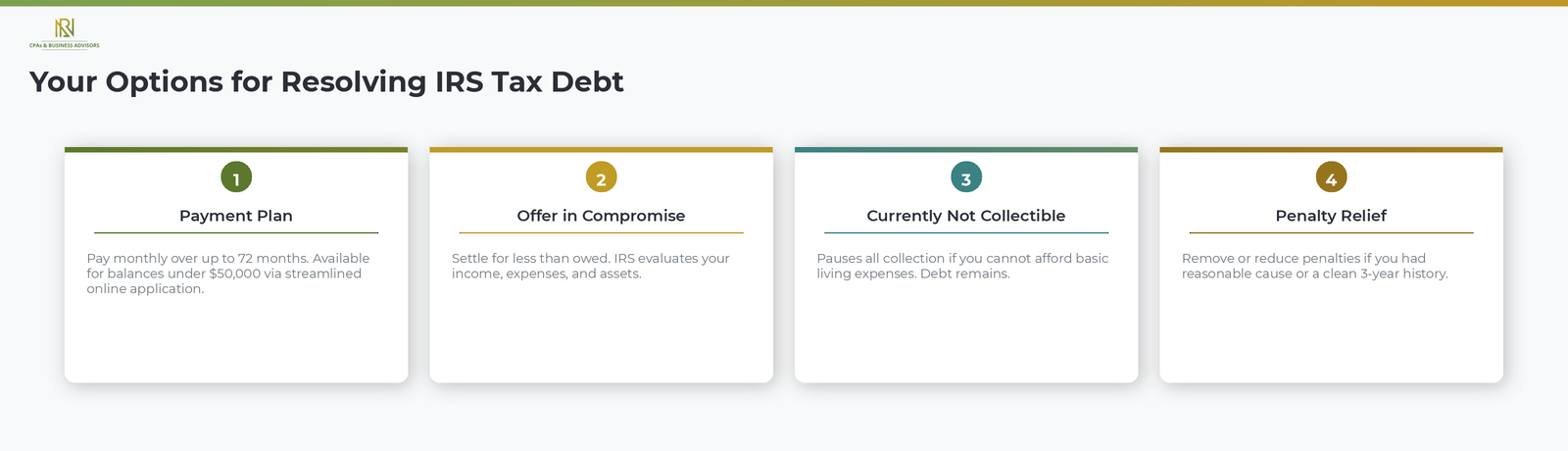

Your Options For Resolving IRS Tax Debt

The IRS provides four primary paths for taxpayers who owe but cannot pay in full: installment agreements, Offers in Compromise, Currently Not Collectible status, and penalty relief. The right option depends on how much you owe, how much you can afford to pay each month, and whether you are experiencing financial hardship.

Payment Plans And Installment Agreements

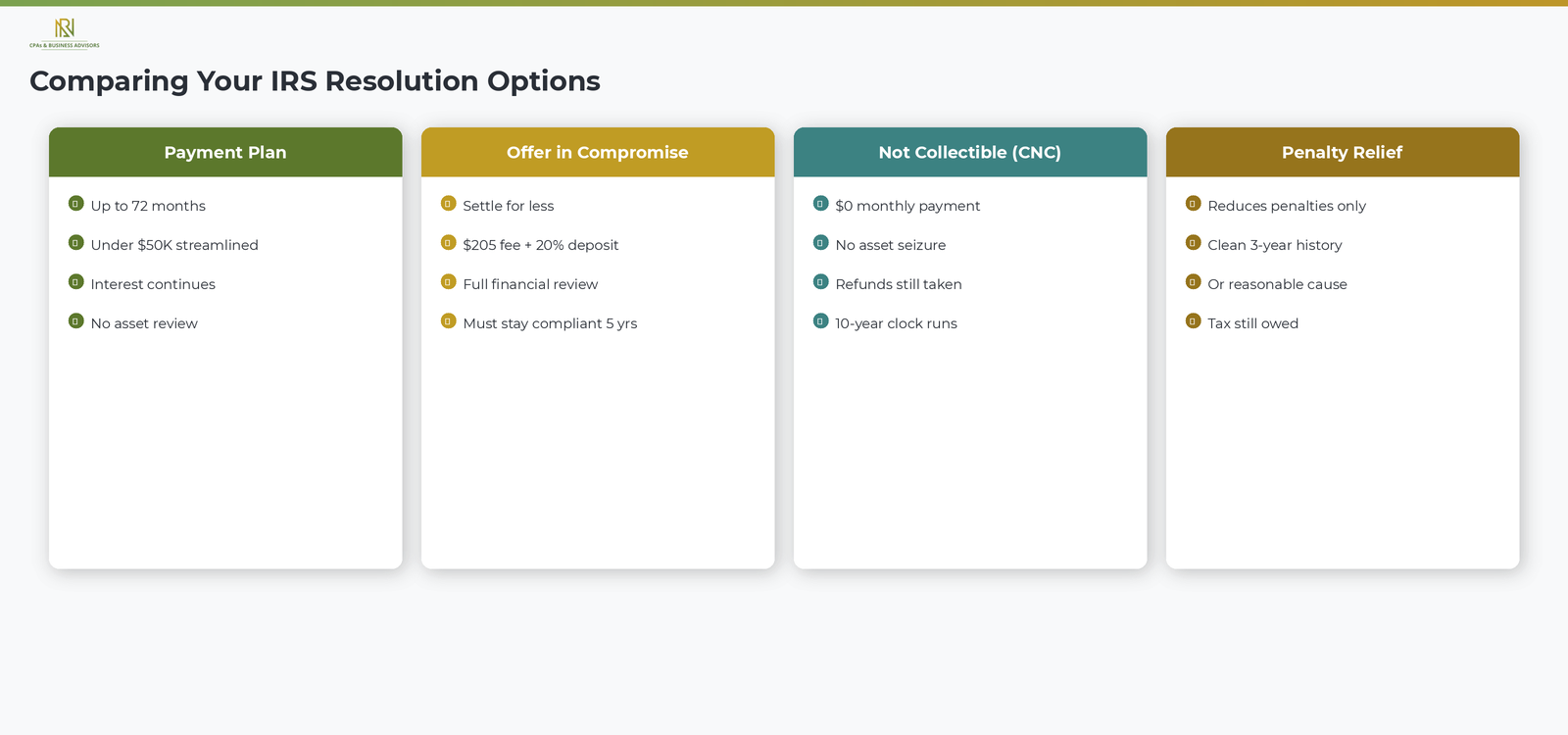

An installment agreement allows you to pay your tax debt in monthly installments over time instead of all at once. According to the IRS, two types of plans are available. A short-term payment plan gives you up to 180 days to pay the full balance, with no setup fee if you apply online. A long-term installment agreement spreads payments across up to 72 months and is available to taxpayers who owe less than $50,000 in combined tax, penalties, and interest. According to the IRS, taxpayers who owe $50,000 or less can apply for a streamlined installment agreement through the IRS Online Payment Agreement tool without providing detailed financial documentation. Our step-by-step guide to installment agreements covers the full application process, balance thresholds, and how interest is calculated on the remaining amount.

Offer In Compromise

An Offer in Compromise allows you to settle your tax debt for less than the full amount you owe. According to the IRS, the agency considers your ability to pay, your income, your expenses, and your asset equity when deciding whether to accept an offer. The IRS generally approves an offer when the amount you propose represents the most the agency can expect to collect within a reasonable period. To apply, you submit Form 656 along with a $205 application fee and an initial payment. Low-income taxpayers who meet the IRS certification guidelines are exempt from both the fee and the initial payment. According to the IRS, you can check your eligibility using the Offer in Compromise Pre-Qualifier tool on IRS.gov before applying.

Currently Not Collectible Status

If your income is so low that you cannot afford to pay anything toward your tax debt without failing to meet basic living expenses, you may qualify for Currently Not Collectible status. According to the IRS, this designation temporarily pauses all collection activity on your account, including levies and garnishments. The tax debt does not go away, and interest and penalties continue to accrue, but the IRS will not take enforcement action while you remain in this status. According to the IRS, the agency will take your future tax refunds and apply them to the balance, and if you owe more than $10,000, the IRS will generally file a Notice of Federal Tax Lien. The IRS reviews your financial situation periodically and may resume collection activity if your income improves.

An important feature of Currently Not Collectible status is that it does not stop the IRS's 10-year statute of limitations on collecting a tax debt. According to the IRS, the agency generally has 10 years from the date a tax debt is assessed to collect it. If the statute expires while your account is in Currently Not Collectible status, the debt is written off permanently.

Penalty Relief

If you owe penalties on top of your tax balance, you may qualify for penalty relief. According to the IRS, the agency can reduce or remove penalties if you tried to comply with the law but were unable to meet your obligations due to circumstances beyond your control, such as a natural disaster, serious illness, or the death of a close family member. First-time penalty abatement is also available to taxpayers who have a clean compliance history for the three prior tax years.

How The IRS Decides Which Option You Qualify For

The IRS evaluates your eligibility for each program based on your total debt, your monthly income and expenses, and the equity in your assets. According to the IRS, the agency uses national and local cost-of-living standards to determine what constitutes a reasonable monthly expense. If your income exceeds your allowable expenses, the IRS expects you to put the difference toward your tax debt through a payment plan. If your allowable expenses equal or exceed your income and you have no significant assets, you may qualify for Currently Not Collectible status or an Offer in Compromise.

Taxpayers facing financial hardship may also qualify for the IRS Fresh Start program, which broadens the eligibility criteria for installment agreements, reduces the threshold for streamlined applications, and makes it easier to qualify for lien withdrawals after meeting certain conditions. The Fresh Start program is not a separate application. It is a set of expanded guidelines the IRS applies to existing resolution options.

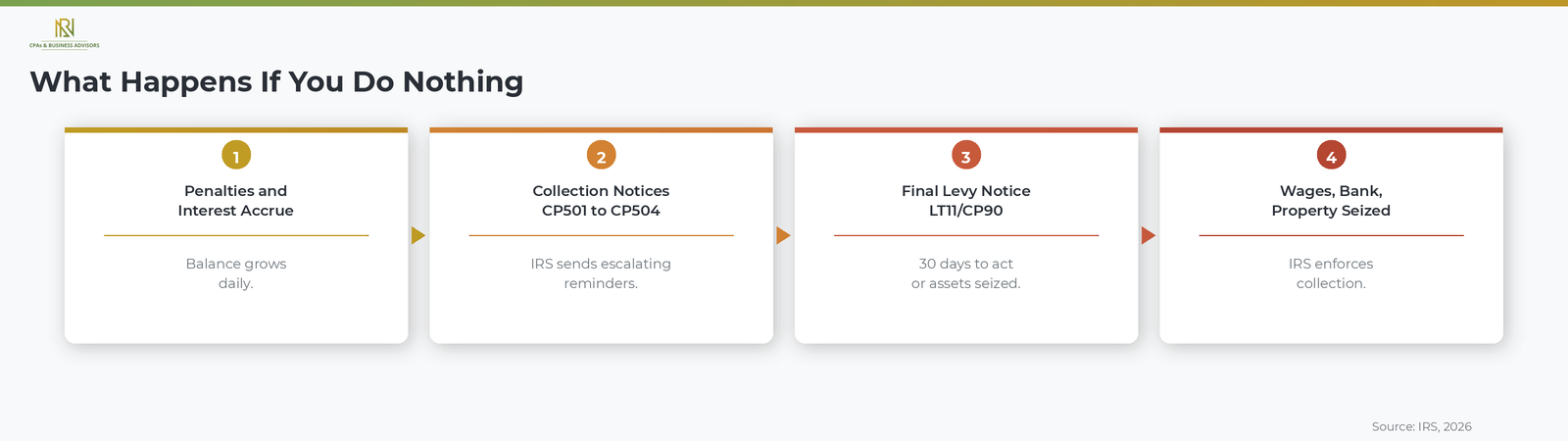

What Happens If You Do Nothing

Doing nothing when you owe the IRS causes penalties and interest to compound daily on your unpaid balance and moves your account through an escalating collection process that can result in the IRS seizing your income and property. According to the IRS, the standard collection sequence begins with a CP14 balance due notice and progresses through CP501 and CP503 reminders, a CP504 Notice of Intent to Levy, and finally an LT11 or CP90 Final Notice of Intent to Levy. At the final notice stage, the IRS is authorized to levy your wages, bank accounts, personal property, and up to 15 percent of your Social Security benefits. Taxpayers who want to understand the full enforcement timeline can review our guide to the LT11 final levy notice.

In addition to levies, the IRS can file a Notice of Federal Tax Lien at any point after a balance remains unpaid. A lien is a public record that establishes the government's legal claim against your assets, can severely damage your credit, and makes it difficult to sell or refinance property. The FAST Act also authorizes the State Department to deny, revoke, or limit your passport if your tax debt meets the threshold for seriously delinquent tax debt.

When To Get Professional Help

Consider working with a CPA, Enrolled Agent, or tax attorney if your tax debt is large, if you are facing active collection action such as a levy or lien, or if you are unsure which resolution option is right for your financial situation. A qualified tax professional can analyze your income, expenses, and assets, determine which IRS program gives you the best outcome, and negotiate directly with the IRS on your behalf. According to the IRS, you can authorize a representative by filing Form 2848, Power of Attorney and Declaration of Representative.

Frequently Asked Questions About Owing The IRS

What Happens If I Owe The IRS More Than $50,000?

You can still set up a payment plan, but you will need to provide detailed financial information to the IRS. According to the IRS, the streamlined installment agreement is only available for balances of $50,000 or less. For larger amounts, you may need to submit Form 433-A (Collection Information Statement) and work directly with the IRS to negotiate terms. An Offer in Compromise may also be an option if the full balance is uncollectible.

Does The IRS Forgive Tax Debt?

The IRS does not automatically forgive tax debt, but it does offer programs that can reduce or eliminate what you owe. An Offer in Compromise allows you to settle for less than the full amount. Currently Not Collectible status pauses collection, and the 10-year statute of limitations on collections means the debt can expire if the IRS does not collect it within that window.

Can I Negotiate With The IRS On My Own?

Yes, you can negotiate directly with the IRS without hiring a representative. According to the IRS, you can apply for payment plans online, submit an Offer in Compromise yourself, and request Currently Not Collectible status by calling the number on your notice. However, taxpayers with complex situations, large balances, or active enforcement actions often benefit from professional representation.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

Owe The IRS And Can't Pay? Your Options

If you owe the IRS and cannot pay the full amount, the most important step you can take is to file your return on time and pay as much as you can, even if that amount is far less than what you owe. According to the IRS, filing on time avoids the failure-to-file penalty, which is significantly more expensive than the failure-to-pay penalty. Paying even a partial amount reduces the balance on which the IRS calculates interest and penalties, which means the total debt grows more slowly than it would if you paid nothing at all.

The IRS does not expect every taxpayer to pay in full on the due date. According to the IRS, the agency offers several programs specifically designed for taxpayers who owe but cannot pay, and most of these options are available whether your debt is recent or has been accumulating for years. The worst action you can take is no action. Ignoring a tax debt does not make it go away. Instead, it triggers an escalating series of IRS collection notices that can eventually result in wage garnishments, bank account levies, property seizures, and federal tax liens that damage your credit. For a full breakdown of how the IRS notice sequence works, our complete guide to IRS correspondence explains every stage from balance due reminders to final enforcement.

Your Options For Resolving IRS Tax Debt

The IRS provides four primary paths for taxpayers who owe but cannot pay in full: installment agreements, Offers in Compromise, Currently Not Collectible status, and penalty relief. The right option depends on how much you owe, how much you can afford to pay each month, and whether you are experiencing financial hardship.

Payment Plans And Installment Agreements

An installment agreement allows you to pay your tax debt in monthly installments over time instead of all at once. According to the IRS, two types of plans are available. A short-term payment plan gives you up to 180 days to pay the full balance, with no setup fee if you apply online. A long-term installment agreement spreads payments across up to 72 months and is available to taxpayers who owe less than $50,000 in combined tax, penalties, and interest. According to the IRS, taxpayers who owe $50,000 or less can apply for a streamlined installment agreement through the IRS Online Payment Agreement tool without providing detailed financial documentation. Our step-by-step guide to installment agreements covers the full application process, balance thresholds, and how interest is calculated on the remaining amount.

Offer In Compromise

An Offer in Compromise allows you to settle your tax debt for less than the full amount you owe. According to the IRS, the agency considers your ability to pay, your income, your expenses, and your asset equity when deciding whether to accept an offer. The IRS generally approves an offer when the amount you propose represents the most the agency can expect to collect within a reasonable period. To apply, you submit Form 656 along with a $205 application fee and an initial payment. Low-income taxpayers who meet the IRS certification guidelines are exempt from both the fee and the initial payment. According to the IRS, you can check your eligibility using the Offer in Compromise Pre-Qualifier tool on IRS.gov before applying.

Currently Not Collectible Status

If your income is so low that you cannot afford to pay anything toward your tax debt without failing to meet basic living expenses, you may qualify for Currently Not Collectible status. According to the IRS, this designation temporarily pauses all collection activity on your account, including levies and garnishments. The tax debt does not go away, and interest and penalties continue to accrue, but the IRS will not take enforcement action while you remain in this status. According to the IRS, the agency will take your future tax refunds and apply them to the balance, and if you owe more than $10,000, the IRS will generally file a Notice of Federal Tax Lien. The IRS reviews your financial situation periodically and may resume collection activity if your income improves.

An important feature of Currently Not Collectible status is that it does not stop the IRS's 10-year statute of limitations on collecting a tax debt. According to the IRS, the agency generally has 10 years from the date a tax debt is assessed to collect it. If the statute expires while your account is in Currently Not Collectible status, the debt is written off permanently.

Penalty Relief

If you owe penalties on top of your tax balance, you may qualify for penalty relief. According to the IRS, the agency can reduce or remove penalties if you tried to comply with the law but were unable to meet your obligations due to circumstances beyond your control, such as a natural disaster, serious illness, or the death of a close family member. First-time penalty abatement is also available to taxpayers who have a clean compliance history for the three prior tax years.

How The IRS Decides Which Option You Qualify For

The IRS evaluates your eligibility for each program based on your total debt, your monthly income and expenses, and the equity in your assets. According to the IRS, the agency uses national and local cost-of-living standards to determine what constitutes a reasonable monthly expense. If your income exceeds your allowable expenses, the IRS expects you to put the difference toward your tax debt through a payment plan. If your allowable expenses equal or exceed your income and you have no significant assets, you may qualify for Currently Not Collectible status or an Offer in Compromise.

Taxpayers facing financial hardship may also qualify for the IRS Fresh Start program, which broadens the eligibility criteria for installment agreements, reduces the threshold for streamlined applications, and makes it easier to qualify for lien withdrawals after meeting certain conditions. The Fresh Start program is not a separate application. It is a set of expanded guidelines the IRS applies to existing resolution options.

What Happens If You Do Nothing

Doing nothing when you owe the IRS causes penalties and interest to compound daily on your unpaid balance and moves your account through an escalating collection process that can result in the IRS seizing your income and property. According to the IRS, the standard collection sequence begins with a CP14 balance due notice and progresses through CP501 and CP503 reminders, a CP504 Notice of Intent to Levy, and finally an LT11 or CP90 Final Notice of Intent to Levy. At the final notice stage, the IRS is authorized to levy your wages, bank accounts, personal property, and up to 15 percent of your Social Security benefits. Taxpayers who want to understand the full enforcement timeline can review our guide to the LT11 final levy notice.

In addition to levies, the IRS can file a Notice of Federal Tax Lien at any point after a balance remains unpaid. A lien is a public record that establishes the government's legal claim against your assets, can severely damage your credit, and makes it difficult to sell or refinance property. The FAST Act also authorizes the State Department to deny, revoke, or limit your passport if your tax debt meets the threshold for seriously delinquent tax debt.

When To Get Professional Help

Consider working with a CPA, Enrolled Agent, or tax attorney if your tax debt is large, if you are facing active collection action such as a levy or lien, or if you are unsure which resolution option is right for your financial situation. A qualified tax professional can analyze your income, expenses, and assets, determine which IRS program gives you the best outcome, and negotiate directly with the IRS on your behalf. According to the IRS, you can authorize a representative by filing Form 2848, Power of Attorney and Declaration of Representative.

Frequently Asked Questions About Owing The IRS

What Happens If I Owe The IRS More Than $50,000?

You can still set up a payment plan, but you will need to provide detailed financial information to the IRS. According to the IRS, the streamlined installment agreement is only available for balances of $50,000 or less. For larger amounts, you may need to submit Form 433-A (Collection Information Statement) and work directly with the IRS to negotiate terms. An Offer in Compromise may also be an option if the full balance is uncollectible.

Does The IRS Forgive Tax Debt?

The IRS does not automatically forgive tax debt, but it does offer programs that can reduce or eliminate what you owe. An Offer in Compromise allows you to settle for less than the full amount. Currently Not Collectible status pauses collection, and the 10-year statute of limitations on collections means the debt can expire if the IRS does not collect it within that window.

Can I Negotiate With The IRS On My Own?

Yes, you can negotiate directly with the IRS without hiring a representative. According to the IRS, you can apply for payment plans online, submit an Offer in Compromise yourself, and request Currently Not Collectible status by calling the number on your notice. However, taxpayers with complex situations, large balances, or active enforcement actions often benefit from professional representation.

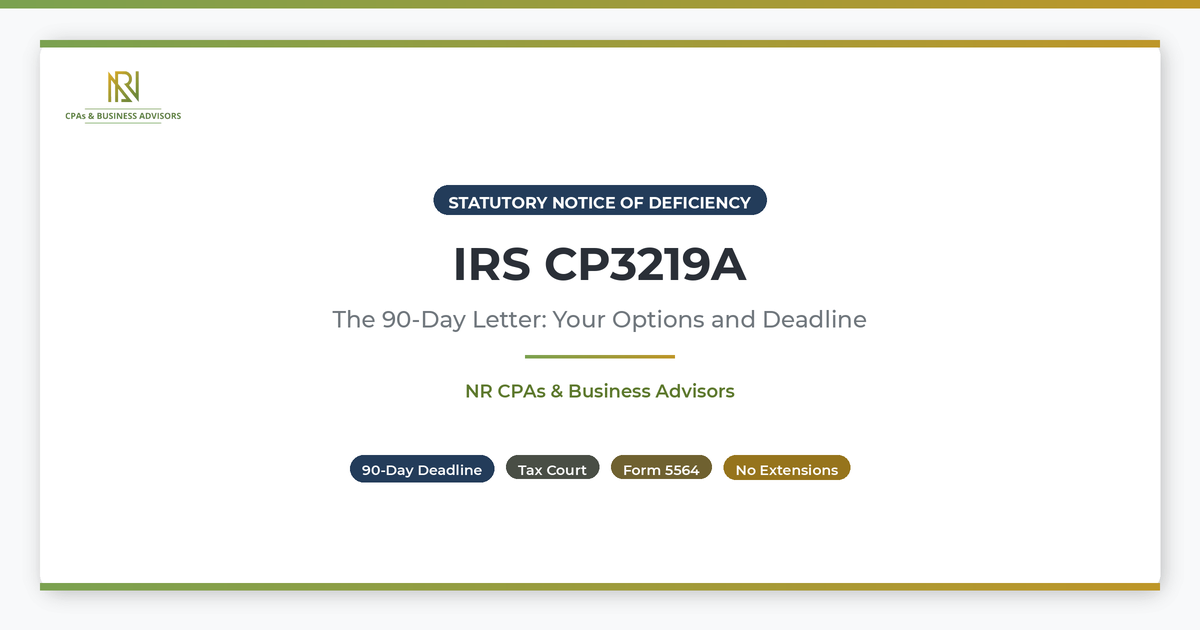

IRS CP3219A: Statutory Notice Of Deficiency (90-Day Letter)

An IRS CP3219A is a Statutory Notice of Deficiency, also known as a 90-day letter, that formally notifies you the IRS is proposing to increase your income tax for a specific tax year. According to the IRS, this notice is issued when the agency found differences between what you reported on your tax return and the information it received from employers, banks, and other third parties. The CP3219A is not a bill and it is not an audit. It is a legal notice that explains the proposed change, how the amount was calculated, and your right to challenge the decision in U.S. Tax Court before the proposed tax becomes an assessed balance.

The CP3219A is one of the most consequential notices the IRS issues because it is the last step before the proposed tax increase is finalized. If you do not respond within the deadline printed on the notice, the IRS will assess the additional tax, add penalties and interest, and send you a bill. At that point, disputing the amount becomes significantly more difficult. For a broader overview of how all IRS notices work and what different types mean, our complete guide to IRS correspondence covers every category from balance due reminders to enforcement actions.

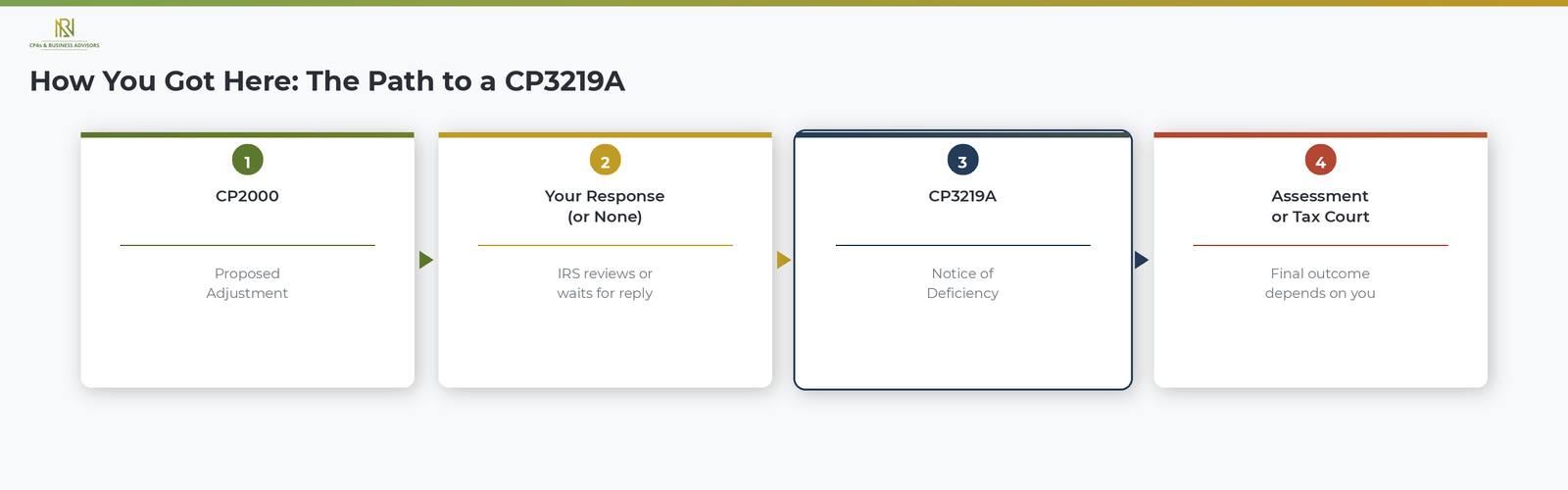

Why You Received A CP3219A

You received a CP3219A because the IRS previously contacted you about an income discrepancy on your tax return and either did not receive a response or was unable to reach an agreement with you. According to the IRS, the CP3219A is typically the final notice in a sequence that begins with a CP2000, which is a proposed adjustment notice the IRS sends when third-party information does not match what you reported. Taxpayers who want to understand the CP2000 and how the IRS identifies income discrepancies can review our full guide to the CP2000 underreporter notice.

The most common reasons the IRS issues a CP3219A include the following.

- No response to prior notices. The IRS sent a CP2000 or related correspondence and did not receive a reply within the response window.

- Unresolved disagreement. You responded to the CP2000 but the IRS did not accept your explanation, and the proposed adjustment remains in dispute.

- Unreported income. Wages, investment earnings, retirement distributions, or other income reported to the IRS by third parties does not appear on your tax return.

- Incorrect credits or deductions. The IRS believes you claimed credits or deductions that the available records do not support.

The 90 Day Deadline And Why It Cannot Be Extended

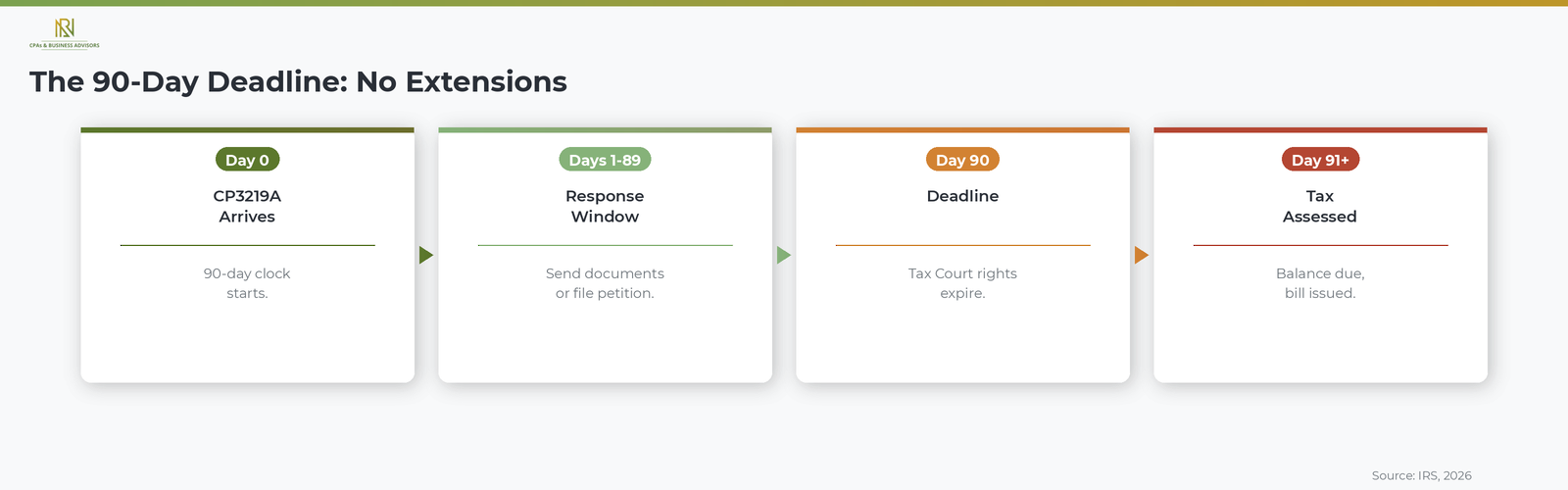

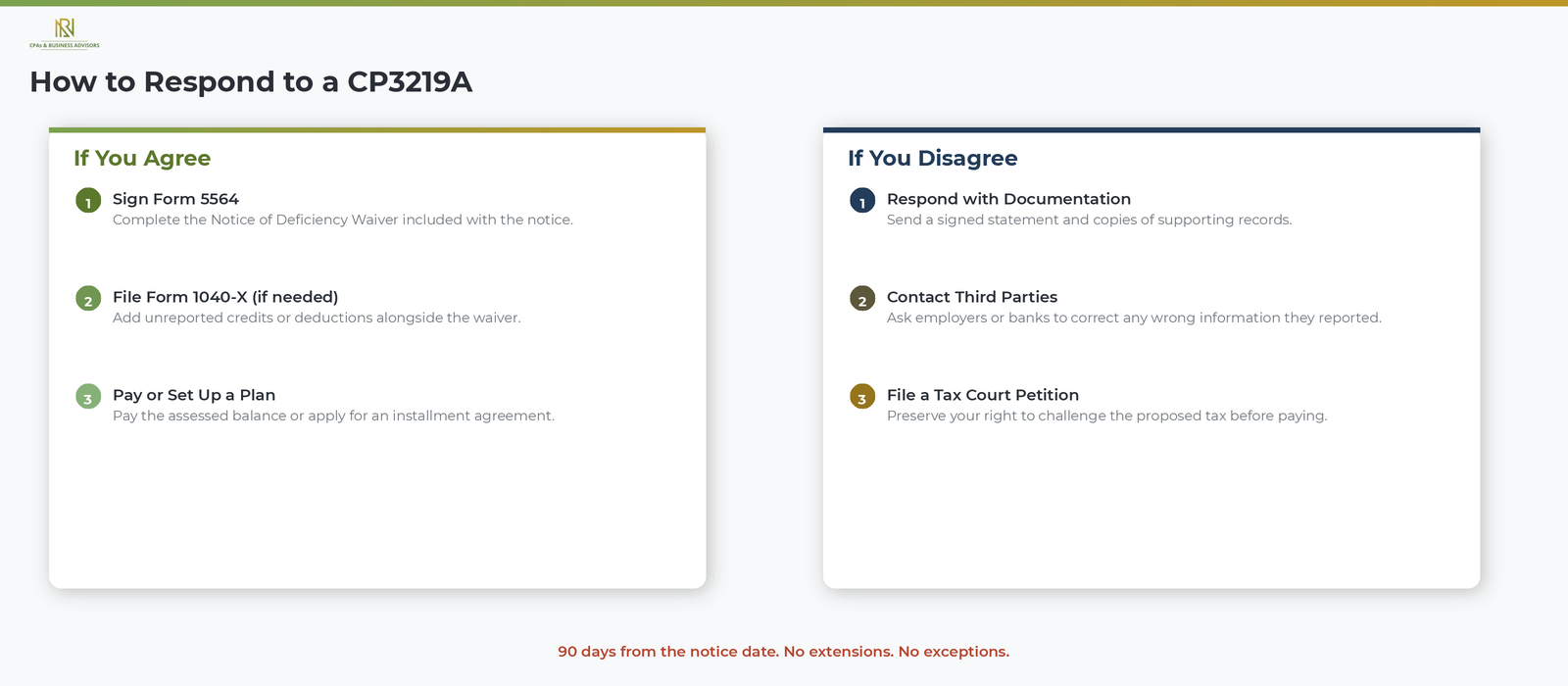

You have exactly 90 days from the date printed on the CP3219A to respond, and this deadline cannot be extended for any reason. According to the IRS, if you are outside the United States when you receive the notice, the deadline is extended to 150 days. This 90-day window is a statutory deadline set by the Internal Revenue Code, which means neither the IRS nor any tax professional can grant additional time.

The 90-day deadline applies to two critical actions: responding to the IRS with documentation that supports your position, and filing a petition with the U.S. Tax Court if you wish to challenge the proposed deficiency. According to the IRS, the Tax Court cannot consider your case if the petition is filed even one day late. For this reason, acting as early as possible within the 90-day window is essential, especially given that IRS processing times for responses can be longer than usual.

How To Respond If You Agree With The Proposed Changes

If you agree that the IRS's proposed tax increase is correct, sign and return the enclosed Form 5564, Notice of Deficiency Waiver, by the deadline. According to the IRS, signing Form 5564 means you accept the proposed changes and waive your right to petition the U.S. Tax Court on those specific items. The IRS will then assess the additional tax along with any applicable penalties and interest.

If the CP3219A is correct but you also have additional income, credits, or deductions that were not included on your original return, you can file Form 1040-X (Amended U.S. Individual Income Tax Return) along with Form 5564. According to the IRS, you should write "CP3219A" on the top of Form 1040-X and submit both forms together. If you owe a balance after the assessment and cannot pay the full amount, you may qualify for a monthly IRS payment plan or installment agreement. Our step-by-step guide to payment plans explains the application process and how interest is calculated on the remaining balance.

How To Respond If You Disagree

If you disagree with the proposed changes, respond to the IRS as soon as possible with documentation that supports your position. According to the IRS, you must include a signed statement explaining why you believe the proposed adjustment is incorrect, along with copies of any supporting records such as corrected W-2s, 1099s, or other income documents.

If the information a third party reported to the IRS is wrong, contact the employer, bank, or institution that filed the incorrect document and ask them to issue a corrected version. According to the IRS, you should notify the agency that you are waiting for the correction so the IRS is aware the issue is being addressed. Keep written records of all communication with the third party in case the correction takes longer than expected.

You can respond by uploading documents through the IRS secure portal (the fastest option), by fax to the number listed on the notice, or by mail to the address on the notice. Regardless of the method you choose, do not wait until the last day. If the IRS has not responded to your submission by the deadline, you may still need to file a Tax Court petition to preserve your rights.

Your Right To Petition The U.S. Tax Court

The CP3219A grants you the legal right to file a petition with the U.S. Tax Court to challenge the proposed deficiency before it becomes an assessed balance. According to the IRS, one of the primary benefits of petitioning the Tax Court is that you can dispute the proposed tax increase without having to pay the amount first. This makes Tax Court the preferred option for taxpayers who disagree with the IRS's calculation but cannot afford to pay and then seek a refund.

To file a petition, visit the U.S. Tax Court website at ustaxcourt.gov and follow the instructions for starting a case. You can file electronically or by mail. The petition must be filed by the date printed on the CP3219A. According to the IRS, the agency will continue to work with you during the 90-day period to resolve the issue, but this does not extend your Tax Court filing deadline.

What Happens If You Miss The 90 Day Deadline

If you do not respond or file a Tax Court petition within 90 days, the IRS will assess the proposed tax increase as a final balance due on your account. According to the IRS, once the assessment is made, the agency will send you a bill for the additional tax, penalties, and interest. At that point, disputing the underlying amount becomes significantly harder because you have lost your right to challenge it in Tax Court without first paying the balance and filing a claim for a refund.

After the assessment, the balance enters the standard IRS collection process. The IRS will send collection notices (CP14, CP501, CP503, CP504) and can eventually pursue enforcement actions including federal tax liens and asset levies if the balance remains unpaid. Acting within the 90-day window is far more protective of your rights and financial options than allowing the deadline to pass.

Frequently Asked Questions About The IRS CP3219A

What Is The Difference Between A CP2000 And A CP3219A?

A CP2000 is a proposed adjustment notice that gives you an opportunity to agree, disagree, or provide additional information before any change is made to your tax. According to the IRS, a CP3219A is the Statutory Notice of Deficiency that the IRS issues if the CP2000 issue remains unresolved. The CP3219A carries legal weight and triggers your right to petition the U.S. Tax Court within 90 days.

Is A CP3219A The Same As An Audit?

No, a CP3219A is not an audit. According to the IRS, the notice is generated by the Automated Underreporter program, which compares the information on your return to data reported by third parties. A formal audit (also called an examination) involves a more detailed review of your return and supporting records.

Can I Get More Time To Respond To A CP3219A?

No, the 90-day deadline on a CP3219A is set by the Internal Revenue Code and cannot be extended. According to the IRS, the only exception is for taxpayers outside the United States, who receive 150 days. There are no other extensions available regardless of the circumstances.