%201.avif)

.png)

.png)

How a Virtual CFO Helps with Fundraising?

A virtual CFO helps with fundraising by preparing investor-ready financial statements, building credible financial models, organizing the data room, managing due diligence, advising on valuation and deal terms, and handling post-close investor reporting. For most founders raising a seed, Series A, or growth round, a virtual CFO is the difference between a fundraise that closes on favorable terms and one that drags on for months or falls apart entirely.

In this article, we cover exactly what a CFO does during fundraising, what financial documents investors expect, how to build a model and a data room, what due diligence looks like, when to bring in a virtual CFO before a raise, how the role supports Series A and later rounds, and what the engagement costs.

How a Virtual CFO Helps with Fundraising

A virtual CFO helps with fundraising by giving founders a senior financial partner who builds the financial story, prepares the materials, and stands behind the numbers during investor conversations. The role spans every phase of the raise, from cleaning up historical financials in the months before fundraising starts, to building a defensible financial model, to running the data room, to handling investor questions during due diligence, to setting up reporting after the round closes.

The data shows why this matters. According to research from NSKT Global, startups with well-prepared financials raise Series A funding 3 times faster than those scrambling to organize their financial house during the fundraising process. Companies that engage a fractional or virtual CFO 6 to 12 months before a raise often close at better valuations because investors can focus on growth potential instead of worrying about whether the books are clean. Our virtual CFO engagements often start exactly at this kind of pre-fundraising stage, when founders realize the bookkeeping that got them this far is not going to survive professional investor scrutiny.

The U.S. fundraising market remains active despite tougher conditions. According to PitchBook data, U.S. startup funding reached $162.8 billion in the first half of 2025, with AI companies pulling in 64% of that capital. According to Q3 2025 venture capital analysis from Eqvista, total quarterly funding hit $97 billion, with 18 mega-rounds capturing one-third of all capital. The bar to raise has gone up, and the quality of financial preparation now plays a much bigger role in whether a deal closes.

What Does a CFO Do During Fundraising

What a CFO does during fundraising is build the financial materials, run the numbers behind every conversation, manage the data room, support due diligence, and help structure the deal terms. The CFO works alongside the CEO, but where the CEO leads the strategic pitch, the CFO guarantees that every number in every document is accurate, defensible, and tied to source data.

Pre-Fundraising Preparation

Pre-fundraising preparation is the most important phase, and most founders underestimate how much time it takes. A virtual CFO starts by cleaning up historical financials, fixing categorization errors, reconciling accounts, and making sure the books match what the pitch deck will eventually claim. According to a 2025 Deloitte CFO Signals report, 78% of finance leaders now treat scenario modeling as a core part of monthly work, up from 52% in 2021. That same discipline gets applied to the fundraising prep, where the CFO builds 3 to 5 years of historical clarity before building the forward model.

The CFO also defines the financial story. What does the business actually do, how does it make money, what does the path to profitability look like, and what will the capital be used for. These are not marketing questions. They are financial questions that need to be answered with numbers, and the answers shape every later document.

Building the Financial Model and Pitch Deck

The financial model is the foundation of every fundraising conversation. A virtual CFO builds a 3 to 5 year model with monthly granularity covering revenue, costs, headcount, capital expenditures, and cash position. The model includes base, upside, and downside scenarios so investors can see what happens under different conditions. According to Crunchbase research, poor financial modeling contributes to unexpected cash shortfalls in 76% of failed startups, which is exactly why investors scrutinize models so carefully.

The pitch deck pulls from the model. According to FD Capital research, a typical fundraising deck covers 12 to 18 slides spanning problem, solution, market, product, traction, business model, unit economics, team, competition, financial projections, use of funds, and the ask. The CFO owns the slides where financial integrity matters most: traction, business model, unit economics, financials, and use of funds. Our strategic planning work for clients leads directly into the kind of model and deck that pass investor scrutiny.

Due Diligence Support

Due diligence is where most deals are won or lost. Investors send long lists of financial, legal, tax, and operational questions, and the speed and quality of the answers signal how well-run the company is. According to First Round Capital partner Josh Kopelman, the time from first conversation to term sheet at top VCs has compressed from 90 days in 2014 to as little as 9 days today. That speed only works if the founder has a CFO who can produce clean, accurate, and complete information on demand.

A virtual CFO populates the data room ahead of time, anticipates the questions investors will ask, and prepares answers with supporting documentation. We pair this with structured financial statements so the numbers in the data room match the numbers in the deck, in the model, and in every spoken claim during a pitch meeting.

Post-Close Investor Reporting

Once the round closes, the CFO sets up the investor reporting cadence. This usually includes monthly or quarterly investor updates, board reporting packages, KPI dashboards, and ad hoc reporting for new investors evaluating future rounds. According to Crunchbase analysis, companies with dynamic financial forecasting and consistent investor reporting are 2.7 times more likely to raise follow-on funding. Strong post-close reporting is not just compliance, it is the foundation of the next round.

Can a Virtual CFO Help with Fundraising

Yes, a virtual CFO can help with fundraising, and for most early-stage and growth-stage companies, a virtual CFO is the right choice over a full-time hire. The work involved in a fundraise is project-based and time-bounded, with peak hours during the active raise and lower hours before and after. A virtual or fractional engagement matches that workflow far better than a permanent six-figure executive hire.

According to industry research, around 80% of startups operate without a CFO in the early stages, which means founders making fundraising decisions usually do not have senior financial guidance in the room. According to Salary.com data for 2025, a full-time CFO in the U.S. earns a median base salary of $437,000, with total compensation often exceeding $500,000 once benefits, bonuses, and equity are factored in. A pre-revenue or early-revenue startup cannot absorb that kind of cost, but it can absorb the $3,000 to $10,000 per month a virtual CFO charges. According to Business Research Insights, the global virtual CFO market was valued at $3.91 billion in 2024 and is projected to reach $8.17 billion by 2032, growing at a 9.6% annual rate, largely because founders raising capital have figured out the model works.

The technology behind virtual CFO work also makes it well-suited for fundraising. Cloud accounting platforms, shared data rooms, video conferencing, and live financial dashboards mean a remote CFO has the same visibility into the numbers as someone sitting in the office. Modern investors expect to see digital data rooms and live models, and a virtual CFO is the person who builds and runs both.

What Financial Documents Do Investors Want to See

The financial documents investors want to see include 3 years of historical financial statements, the current year-to-date financials, a 3 to 5 year financial model, monthly cash flow forecasts, the cap table, recent tax returns, accounts receivable and payable aging reports, payroll summaries, and any customer or revenue concentration analysis. Together these form the core of the financial data room.

The historical financials matter most for proving traction. Investors look for clean monthly profit and loss statements, balance sheets, and cash flow statements that match the company's tax returns and bank records. According to a 2025 Bessemer Venture Partners report, unit economics are now scrutinized more carefully than they were five years ago, with VCs spending more time validating margin trajectory before writing checks. Companies with messy or inconsistent historical books often see deals stall or fall apart during this phase. Solid tax planning records also matter here, because investors compare tax filings to internal financials to confirm everything reconciles.

The forward model is where the CFO tells the growth story. The model has to show realistic revenue assumptions, defensible cost structure, clear use of funds, and a credible path to the next milestone. Investors do not believe hockey-stick projections that come out of nowhere. They believe models grounded in unit economics, sales pipeline data, and historical performance.

What Is a Financial Model for Fundraising

A financial model for fundraising is a spreadsheet that projects revenue, expenses, headcount, cash flow, and key metrics over the next 3 to 5 years. The model serves as the financial backbone of the entire fundraise. Investors use it to assess whether the company's growth plan is realistic, whether the requested capital is enough to reach the next milestone, and whether the unit economics work at scale.

A strong fundraising model has several specific components. Monthly granularity for the first 24 months and quarterly granularity beyond that. Detailed revenue build with assumptions clearly stated. Cost of goods sold tied to revenue with margin trajectory. Operating expenses broken out by department. Headcount plan with timing of hires. Cash flow statement showing burn rate, runway, and the impact of the new round. Sensitivity tables showing what happens if revenue comes in 20% above or below plan. Use of funds breakdown tying directly to the capital ask.

Building the model is one of the most time-consuming parts of fundraising. A virtual CFO who has done this work many times moves faster and avoids the common mistakes that slow down or kill deals, like circular references, mismatched assumptions across tabs, or revenue projections that do not reconcile to the historical run rate. According to Burkland Associates, the model is often the single most-reviewed document in any due diligence process. We see this firsthand with our clients in Miami and across the country, where the quality of the model frequently determines how quickly a term sheet shows up.

What Is a Data Room for Fundraising

A data room for fundraising is an organized digital folder containing all the financial, legal, operational, and corporate documents that investors review during due diligence. The data room is usually hosted on a secure platform like DocSend, Google Drive, Box, or Dropbox, and access is granted to investors who have signed an NDA or LOI.

A typical data room includes financial documents (historical statements, model, tax returns, cap table), legal documents (incorporation, bylaws, shareholder agreements, IP assignments, key contracts), HR documents (employee list, offer letters for key hires, equity grants), customer and revenue data (top customer breakdown, churn analysis, sales pipeline), product and IP documentation, and any prior board materials. Investors expect to find everything they need in the data room within 24 to 48 hours of getting access.

The CFO usually owns the data room. According to Burkland Associates research, building the data room also surfaces gaps in the company's record-keeping, like missing signed contracts, equity grants that were never formally documented, or tax filings that need correction. Fixing these gaps before investors see them prevents awkward back-and-forth that can damage the deal. A well-organized data room signals discipline, which is exactly what investors look for when deciding whether to write a check.

What Is Due Diligence in Fundraising

Due diligence in fundraising is the formal review process where investors examine every aspect of the company before committing capital. It typically covers financial, legal, tax, commercial, and technical diligence, and can take anywhere from 2 weeks to several months depending on the size of the round and the complexity of the business.

Financial due diligence is the most intensive part. Investors review historical financials, validate the model, test key assumptions, examine the cap table, and verify customer concentration. According to research cited by Fidelity Private Shares, due diligence has been getting deeper in 2025, with investors spending more time validating financial discipline, product-market fit, and defensibility before writing checks. Median fundraising timelines have stretched to roughly two years from first investor conversation to close in some cases, which means the discipline that supports the diligence process matters more than ever.

A virtual CFO manages diligence by responding to investor questions quickly, providing supporting documentation, walking investors through the model on live calls, and addressing any concerns that come up. The CFO also coordinates with legal counsel, auditors, and tax advisors to make sure the answers across all functions stay consistent. Strong business consulting support during this phase often saves weeks of back-and-forth and gets the deal to a term sheet faster.

When Should a Startup Hire a Virtual CFO Before Fundraising

A startup should hire a virtual CFO 6 to 12 months before the intended fundraising round, according to industry research from NSKT Global. This gives the CFO enough time to clean up the books, build a credible model, fix any compliance gaps, and prepare the data room before active conversations with investors begin.

The timing matters because most of the work that determines fundraising success happens before the first investor meeting. According to research from NSKT Global, startups that bring on a virtual CFO 6 to 12 months ahead of a Series A raise close their rounds 3 times faster than those who wait until they are already pitching. Common triggers for hiring include monthly burn exceeding $200,000, having raised $2 million or more in prior funding, planning to approach institutional investors for the first time, or hitting revenue milestones that make the business attractive to growth-stage capital. The startup CFO role at this stage is more about preparation than execution, and the preparation takes months, not weeks.

Waiting until the raise is already underway is a common mistake. Founders trying to build the model and clean up the books while also pitching investors get pulled in too many directions, and the quality of both suffers. The model arrives late, due diligence questions sit unanswered, and investor confidence erodes. By the time the round closes, if it closes at all, the company has often given up significant valuation to compensate for the friction.

How a Virtual CFO Builds a Financial Model

A virtual CFO builds a financial model by starting with historical data, layering in unit economics, projecting revenue from the bottom up, mapping costs to growth, modeling cash flow, and stress-testing assumptions through multiple scenarios. The process usually takes 4 to 8 weeks for a first version and continues to evolve through the fundraising process as investor questions sharpen the assumptions.

The bottom-up revenue build is where good models separate from bad ones. Instead of starting with a target revenue number and working backward, the CFO starts with the smallest units of the business and builds up. For a SaaS company, that means modeling new customers per month, average contract value, churn, and expansion revenue. For a services business, it means modeling billable hours, utilization rates, and team capacity. For an e-commerce business, it means modeling conversion rates, average order value, and marketing efficiency. Investors trust models that are built this way because the assumptions can be defended and stress-tested.

The cost side follows revenue. Cost of goods sold scales with revenue based on gross margin. Operating expenses scale with headcount, marketing spend, and infrastructure needs. The CFO models hiring timing carefully, because hiring decisions are usually the biggest near-term cost driver. According to McKinsey research, companies that engage in proactive scenario planning are 33% more likely to recover financially within six months after a disruption. That same scenario discipline shows up in fundraising models, where investors expect to see what happens if revenue comes in slower than planned or costs run higher.

How a Virtual CFO Supports Series A and Beyond

A virtual CFO supports Series A and beyond by managing more complex financial requirements, leading institutional investor conversations, preparing audit-ready financials, and building board-level reporting. Series A is the inflection point where casual financial management stops being good enough, and a virtual CFO can match that step-up without forcing the company to commit to a full-time hire.

At the seed stage, fundraising is more about story and team. By Series A, investors expect real metrics. According to PitchBook data, U.S. Series A activity in July 2025 included $2.03 billion across 124 deals, with investors expecting clear unit economics, defensible growth rates, and detailed financial reporting. The diligence is more rigorous, the documents are longer, and the questions go deeper into things like cohort analysis, LTV to CAC ratios, gross margin trends, and operating efficiency.

By Series B and beyond, the CFO role gets even more important. Larger rounds bring institutional investors who often require GAAP-compliant financials, audited statements, and quarterly board reporting. The cap table grows more complex with multiple share classes, options pools, and SAFE conversions. According to Cowen Partners executive search research, the cost of mistakes at this stage also grows, with valuation differences from poor financial preparation potentially running into millions of dollars. A fractional CFO at this stage usually scales hours up significantly during the raise and back down between rounds, which matches how the work actually flows.

What Is Burn Rate and Why It Matters in Fundraising

Burn rate is how much cash a startup spends each month beyond what it earns, and it matters in fundraising because it directly determines how long the company can operate before running out of money. Investors look at burn rate to assess capital efficiency, runway, and whether the requested capital is enough to reach the next milestone.

There are two types of burn. Gross burn is total monthly cash spend. Net burn is gross burn minus monthly revenue. Most investors care more about net burn because it tells them how fast the company is actually using up capital. According to Sequoia Capital guidance, startups should maintain 18 to 24 months of cash runway in the current funding environment, but Carta data shows the median startup actually operates with closer to 12 months of runway. The gap is one reason fundraising timelines have stretched out and why so many founders feel constant pressure to raise.

A virtual CFO manages burn rate by building rolling forecasts, identifying cost reductions before they become urgent, and timing capital raises so the company never has less than 6 months of runway when actively fundraising. Initiating fundraising with 12 to 15 months of runway positions the company as a growth opportunity, not a distressed situation. Smart cash flow discipline before and during the raise can mean the difference between negotiating from strength and accepting whatever terms come.

How Much Does a Virtual CFO Cost for Fundraising

A virtual CFO costs between $3,000 and $15,000 per month for fundraising support, depending on the size of the raise, the complexity of the business, and the experience of the CFO. According to a 2025 pricing survey from Eagle Rock CFO, most growing companies pay $4,000 to $8,000 per month for ongoing CFO support, with hours scaling up during active fundraising periods.

Project-based pricing is also common for fundraising work. According to industry research, fundraising-specific projects often run as flat fees ranging from $15,000 to $75,000 for the full preparation cycle, including model building, deck financials, data room setup, and due diligence support. Hourly rates for fractional CFOs range from $175 to $450, with most experienced practitioners charging $200 to $350 per hour, according to Bennett Financials and other industry pricing surveys.

The investment usually pays for itself many times over through a better valuation, faster close, and reduced founder time spent on financial work. According to Eagle Rock CFO research, growing companies typically see a 3 to 10 times return on their fractional CFO investment. For a startup raising $5 million at a $20 million pre-money valuation, even a 10% valuation improvement is $500,000 of additional equity preserved, which dwarfs the entire cost of CFO engagement for the year. Strong business formation work and clean entity structure also support the kind of valuation investors are willing to pay.

Fundraising Support Options Compared

Founders raising capital usually weigh several options for financial support, including a full-time CFO, a virtual or fractional CFO, a CPA firm, an investment banker, or trying to handle the financial work themselves. Each option fits a different stage, budget, and complexity level. The table below shows how these compare on the factors that matter most during a raise.

Support OptionTypical CostFundraising StrengthBest ForFull-Time CFO$300,000 to $500,000+/yearVery high, daily availabilitySeries B and laterVirtual or Fractional CFO$36,000 to $120,000/yearHigh, strategic focusSeed through Series BCPA or Accounting Firm$5,000 to $30,000/yearModerate, tax and compliancePre-seed or smaller raisesInvestment Banker3 to 7% of round + retainerHigh, investor introductionsGrowth rounds over $10MFounder SoloFounder time onlyLow to moderate, depends on founderFriends and family rounds

Sources: Salary.com 2025 CFO compensation data, Cowen Partners Executive Search 2025, Eagle Rock CFO 2025 pricing survey, K38 Consulting 2025 fractional CFO guide, Graphite Financial 2025 hourly rate data, Bennett Financials 2025 fractional CFO pricing.

What Investors Look for in a Strong Fundraising Process

What investors look for in a strong fundraising process is preparation, discipline, accuracy, and speed. Preparation means clean financials, a credible model, and an organized data room before pitching starts. Discipline means consistent assumptions across the deck, model, and conversations. Accuracy means every number reconciles to source data. Speed means quick, complete responses to diligence questions.

According to a 2025 Fidelity Private Shares analysis, investors are spending more time on financial discipline and defensibility than ever before. Capital is flowing toward startups with solid fundamentals, not just growth at any cost. According to CB Insights research, 42% of startups fail because they built a product nobody wanted, and 29% fail because they ran out of money. Investors know these numbers, and they look for evidence that the founders in front of them understand and have planned around the financial risks. A virtual CFO is the person who provides that evidence in concrete form.

The best CFOs also help with what investors do not say directly. They notice when an investor's questions signal a concern about gross margin trajectory, customer concentration, or the realism of the hiring plan, and they prepare follow-up materials to address those concerns before they harden into objections. Our startup advisory work centers around this kind of preparation, where the goal is not just answering questions but anticipating them.

Common Fundraising Mistakes a Virtual CFO Helps Founders Avoid

The common fundraising mistakes a virtual CFO helps founders avoid are unrealistic projections, inconsistent numbers across documents, missing supporting evidence, cap table errors, weak unit economics analysis, and starting the raise too late with too little runway. Each of these mistakes is easy to make when a founder is running the whole process alone, and each one can kill an otherwise promising deal.

Unrealistic projections are the most common red flag. Investors see thousands of pitch decks, and they know what realistic growth looks like for a given stage and industry. A model that shows 10x revenue growth with flat headcount and stable margins gets dismissed quickly. A CFO grounds the projections in unit economics, sales velocity, and historical data so the numbers feel earned, not invented.

Inconsistent numbers between the deck, the model, and the verbal pitch is the second most common problem. According to FD Capital research, the CFO's main job during fundraising is to make sure every number in every document ties back to source data. When investors notice mismatched figures, even small ones, trust erodes fast and the deal slows down. The cap table is another frequent source of errors. SAFE notes, option grants, and prior round terms all need to be modeled accurately so post-close ownership is clear before the term sheet is even signed.

Starting the raise with insufficient runway is the most expensive mistake. Founders who begin fundraising with less than 6 months of cash give up leverage in negotiations because investors know the company is running out of options. According to Sequoia Capital and Carta data, the recommended approach is to start with 12 to 15 months of runway and aim to close before runway drops below 6 months. Our CFO services are built around exactly this kind of timing discipline.

Frequently Asked Questions

What Is a Cap Table

A cap table, or capitalization table, is a spreadsheet that lists every shareholder in a company and the equity they own. It shows founders, employees with options, prior investors, and any debt holders with conversion rights like SAFEs or convertible notes. A clean, accurate cap table is one of the first things any investor will ask to see, and any errors can delay or derail a fundraise.

How Long Does Fundraising Take

Fundraising typically takes 3 to 12 months from first investor conversation to close, depending on the stage, sector, and market conditions. According to Fidelity Private Shares 2025 research, median fundraising timelines have stretched to nearly two years in some cases, particularly outside the Bay Area. Companies with strong preparation, clean financials, and an experienced virtual CFO often close materially faster than companies that go in unprepared.

What Is Investor Reporting

Investor reporting is the regular communication between a company and its investors after a fundraise closes. It usually includes monthly or quarterly updates covering financial results, KPI performance, key wins and losses, and any major changes in strategy or team. According to Crunchbase analysis, companies with consistent investor reporting are 2.7 times more likely to raise follow-on funding, which is why a virtual CFO usually sets up the reporting cadence and templates within the first 30 days after a round closes.

How Early Should You Hire a CFO Before Fundraising

You should hire a CFO 6 to 12 months before fundraising, according to research from NSKT Global. This gives the CFO time to clean up historical financials, build the model, organize the data room, and fix any compliance gaps before investors start reviewing materials. Founders who wait until they are already pitching usually pay for the delay through slower closes, lower valuations, or deals that fall apart in diligence.

What Is the Difference Between a CFO and a Virtual CFO

The difference between a CFO and a virtual CFO is the engagement model, not the expertise. A traditional CFO is a full-time in-house executive who manages the entire finance function. A virtual CFO provides the same strategic guidance on a part-time, remote, or project basis, which fits the workflow of fundraising and the budget of most growing companies.

Is a Fractional CFO Worth It for Fundraising

Yes, a fractional CFO is worth it for fundraising. The return usually shows up through a faster close, a higher valuation, and significantly less founder time spent on financial work. According to Eagle Rock CFO research, growing companies see a 3 to 10 times return on fractional CFO investment, and during a fundraise that ROI often arrives within the first 90 days through avoided mistakes and stronger investor confidence.

Do You Need a CFO to Raise Money

You do not technically need a CFO to raise money, but having one significantly improves the odds of a successful close. Many seed-stage companies raise small rounds without senior financial support, often from friends, family, or angel investors who are betting more on the founder than on the financials. For institutional rounds, including most Series A raises and beyond, a virtual CFO is essentially required because investors expect to see professional financial materials and a financial leader who can answer their questions.

What It All Comes Down To

A virtual CFO turns fundraising from a stressful, time-consuming distraction into a structured process with a clear timeline and a much higher chance of success. From clean historical financials and credible models to organized data rooms and disciplined investor reporting, the right virtual CFO gives founders the financial backbone every successful raise requires. The data is consistent across multiple industry sources. Companies with senior financial guidance close faster, at better valuations, and with less friction than those that go in unprepared.

If you are planning to raise capital in the next 6 to 12 months and want to bring in financial leadership that knows what investors expect, we are here to help. At NR CPAs & Business Advisors, we work with founders and growing companies to build the financial foundation a successful fundraise requires. Reach out to our team at (954) 231-6613 to start the conversation.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

IRS LT11 / Letter 1058: Final Notice Of Intent To Levy

What Is An IRS LT11 Notice Or Letter 1058

The IRS LT11 and Letter 1058 are the agency's final notice before it begins seizing your wages, bank accounts, and other property to collect an unpaid tax debt. According to the IRS, both notices serve the same legal purpose: they formally notify you of the IRS's intent to levy your assets under Internal Revenue Code Section 6331 and inform you of your right to request a Collection Due Process hearing before that levy occurs. Receiving either notice means the IRS has exhausted its standard collection reminders and is now authorized to take enforcement action.

The LT11 and Letter 1058 are alternative forms of the same final notice. The LT11 is generated by the IRS Automated Collection System and is typically the version most individual taxpayers receive. Letter 1058 is usually issued by an IRS Revenue Officer who has been assigned to your case directly. Regardless of which version you receive, the legal weight and response deadline are identical. For a broader overview of how all IRS notices work and where this notice fits in the system, our complete guide to IRS correspondence covers every notice category.

Why You Received An LT11 Or Letter 1058

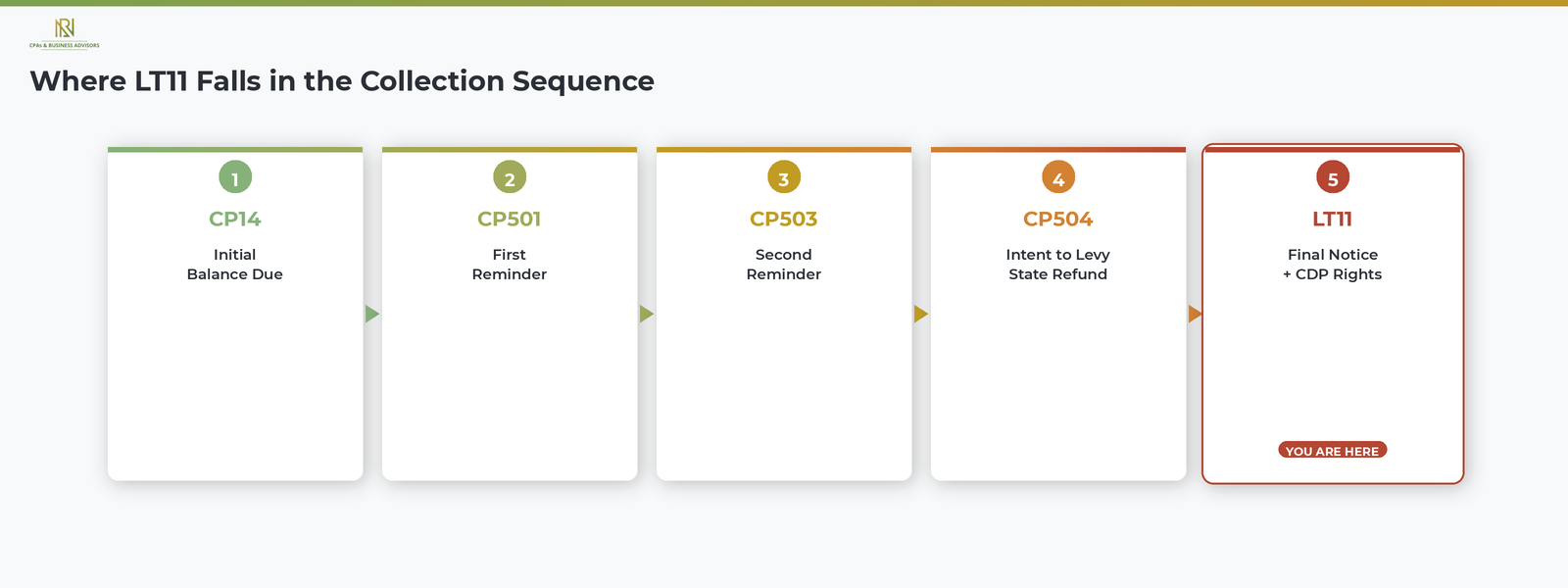

You received an LT11 or Letter 1058 because the IRS sent you multiple prior notices about an unpaid tax balance and did not receive payment or a response. According to the IRS, this final notice comes at the end of a collection sequence that typically includes four earlier notices.

- CP14: the initial notice that your return has an unpaid balance.

- CP501: a first reminder that the balance remains unpaid.

- CP503: a second reminder with stronger language.

- CP504: a Notice of Intent to Levy, warning that the IRS will begin seizing your state tax refund. Taxpayers who received a CP504 notice and want to understand that step in the process can review our full explanation of the CP504 and its response options.

- LT11 or Letter 1058: the final notice, authorizing the IRS to levy wages, bank accounts, and all other property.

The LT11 prominently displays the heading "Notice of Intent to Levy and Your Collection Due Process Right to a Hearing" on the first page. Letter 1058 uses similar language: "Final Notice, Notice of Intent to Levy and Notice of Your Rights to a Hearing." Both make clear that the IRS will proceed with enforcement unless you act within the deadline.

The 30 Day Deadline And Your Right To A CDP Hearing

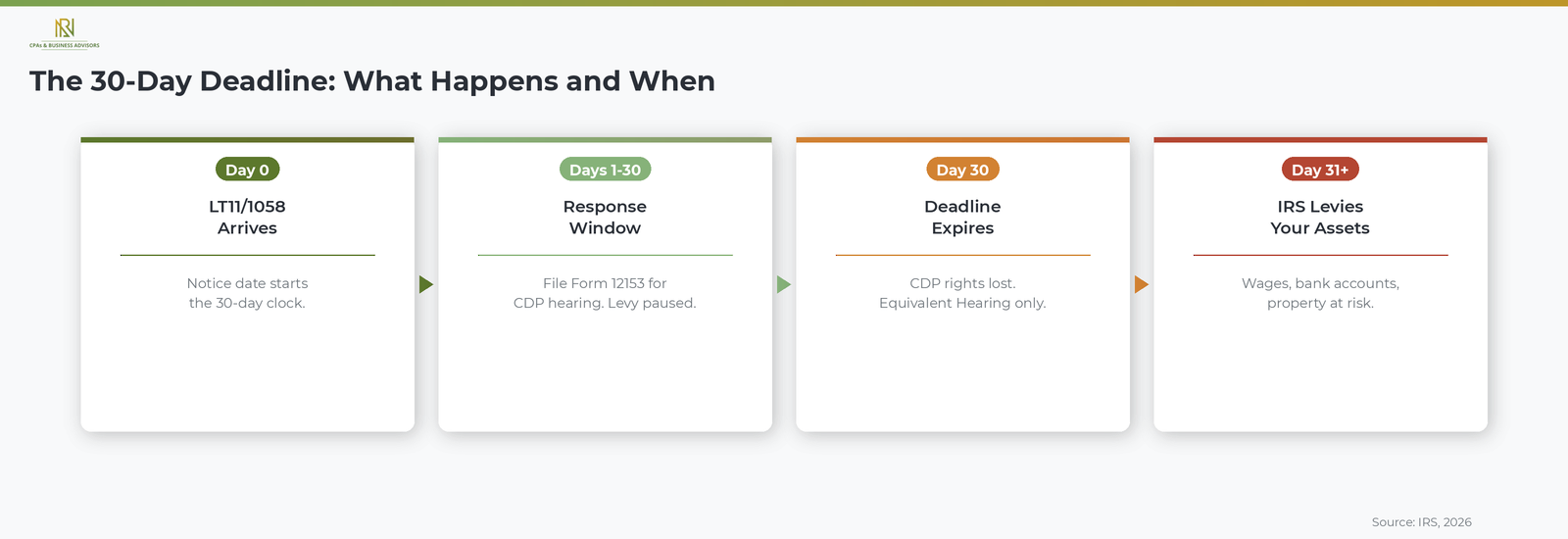

You have exactly 30 days from the date printed on the LT11 or Letter 1058 to respond, and filing within that window is critical because it preserves your right to a Collection Due Process hearing and temporarily stops all levy action. According to the IRS, a Collection Due Process hearing is conducted by the IRS Independent Office of Appeals, which is separate from the division that issued the notice.

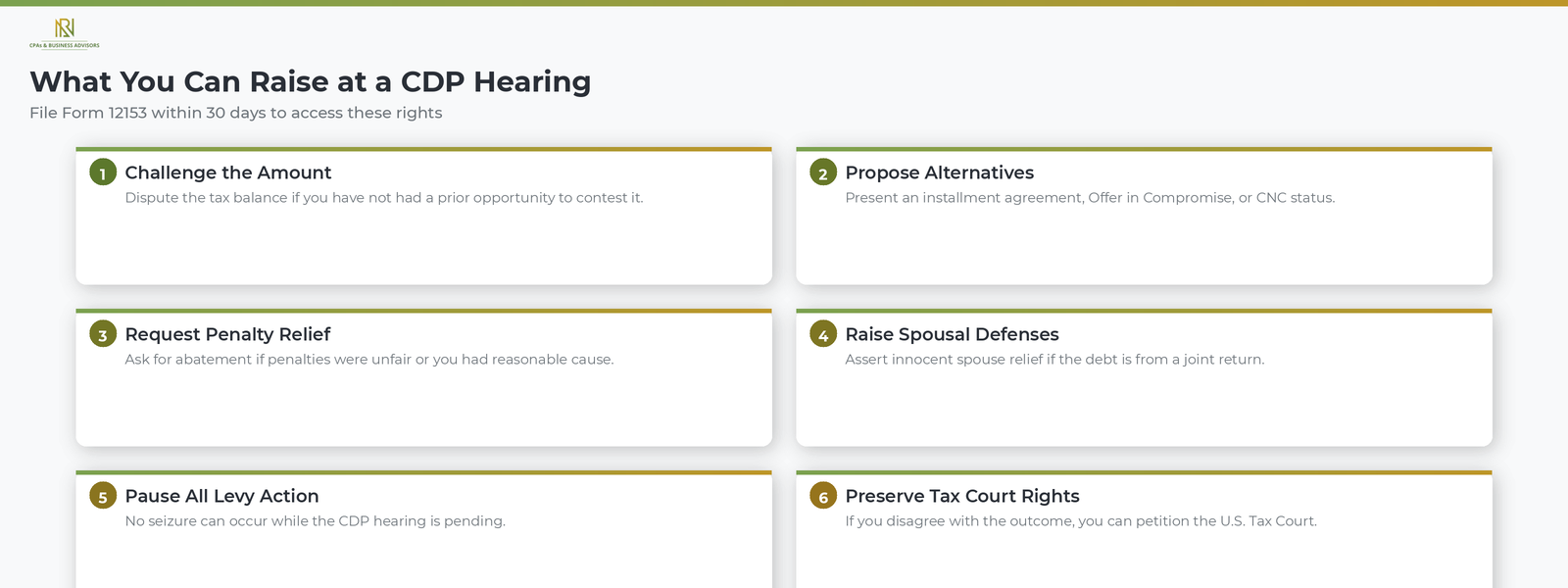

To request a CDP hearing, file Form 12153, Request for a Collection Due Process or Equivalent Hearing, within 30 days of the notice date. During the hearing, you can raise the following issues.

- Challenge the amount owed. If you believe the tax balance is incorrect and have not had a prior opportunity to dispute it, you can contest the underlying liability.

- Propose collection alternatives. You can present options such as an installment agreement, an Offer in Compromise, or Currently Not Collectible status as alternatives to a levy.

- Request penalty abatement. If penalties were applied unfairly or you had reasonable cause for late payment, you can ask for penalty relief.

- Argue spousal defenses. If the debt relates to a joint return and you qualify, you can raise innocent spouse relief.

According to the IRS, no levy action can occur while a CDP hearing request is pending, which makes filing within the 30-day window one of the most effective ways to stop or delay enforcement. A CDP hearing also preserves your right to petition the U.S. Tax Court if you disagree with the Appeals Office decision.

What The IRS Can Levy After Sending An LT11

After the 30-day response window on an LT11 or Letter 1058 expires without action, the IRS is authorized to levy virtually any asset or income stream you have. According to the IRS, property subject to levy includes the following.

- Wages, salaries, and commissions. The IRS can contact your employer and require a portion of each paycheck to be withheld until the debt is satisfied.

- Bank accounts. The IRS can freeze and seize funds in your checking and savings accounts up to the full balance owed.

- State tax refunds. Any state income tax refund you are entitled to can be intercepted.

- Business assets. Equipment, inventory, and accounts receivable can be seized.

- Personal property. According to the IRS, the agency can seize your vehicle, your home, and other real or personal property.

- Social Security benefits. The IRS can levy up to 15 percent of your monthly Social Security payments.

- Retirement accounts. The IRS can levy 401(k) and IRA funds. According to the IRS, amounts withdrawn through a levy are treated as taxable income but are not subject to the 10 percent early withdrawal penalty that normally applies to distributions taken before age 59 and a half.

In addition to levies, the IRS can file a Notice of Federal Tax Lien, which publicly establishes the government's claim against your current and future assets and can damage your credit. The FAST Act also authorizes the State Department to deny, revoke, or limit your passport if your balance meets the seriously delinquent tax debt threshold.

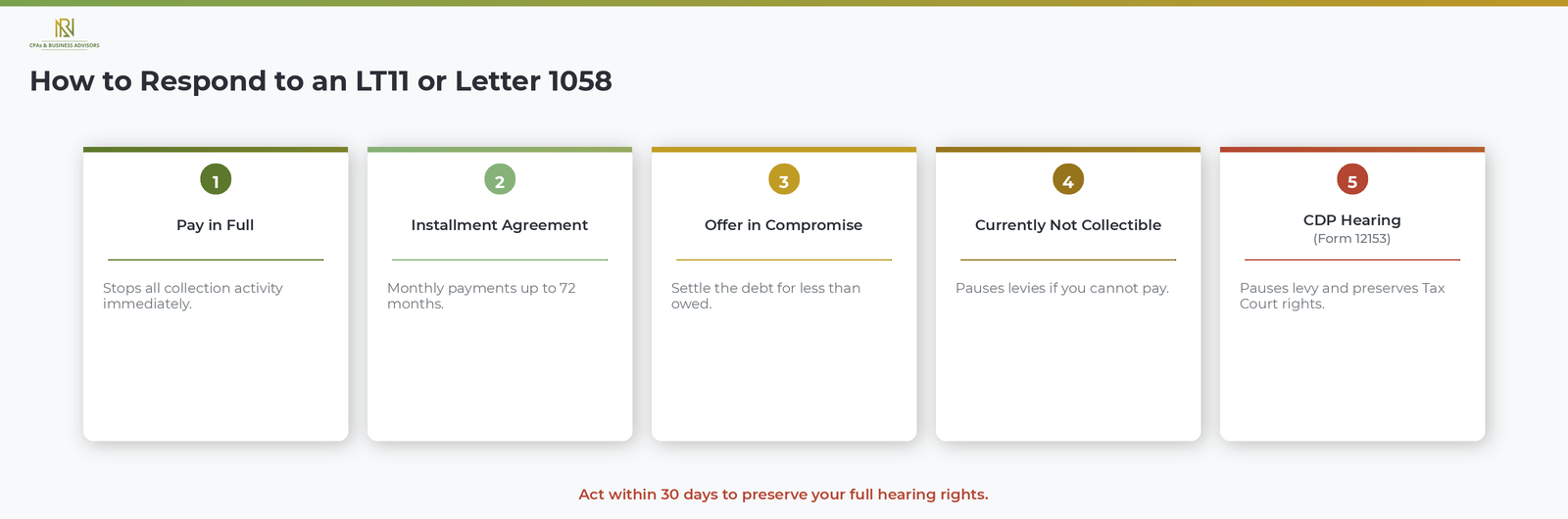

How To Respond To An LT11 Or Letter 1058

The best response depends on your financial situation and whether you agree with the balance the IRS says you owe, but in every case responding before the 30-day deadline is essential.

- Pay the balance in full. The fastest way to stop all collection activity. You can pay online at IRS.gov, by phone, or by mailing a check with the payment voucher from the notice.

- Set up an installment agreement. If you cannot pay in full, you may qualify for a monthly IRS payment plan or installment agreement. Taxpayers who owe less than $50,000 can apply for a streamlined agreement online. Our step-by-step guide to payment plans covers the full application process and balance thresholds.

- Submit an Offer in Compromise. If your financial circumstances make the full debt unlikely to be collected, you may be able to settle for less than you owe.

- Request Currently Not Collectible status. If you have no ability to pay anything, the IRS may temporarily suspend collection activity. The debt remains, but levies stop while you remain unable to pay.

- Request a CDP hearing. File Form 12153 within 30 days to pause the levy and present your case to an independent Appeals officer.

Taxpayers facing significant hardship may also qualify for the IRS Fresh Start program, which broadens eligibility for installment agreements and penalty relief for individuals and businesses with qualifying balances.

What Happens If You Miss The 30 Day Deadline

If you do not respond within 30 days of the date on the LT11 or Letter 1058, the IRS can immediately begin levying your assets, and your hearing rights are reduced. According to the IRS, you can still request what is called an Equivalent Hearing after the 30-day window closes, but an Equivalent Hearing does not stop levy action while it is pending and does not give you the right to petition the U.S. Tax Court if you disagree with the outcome. For this reason, filing Form 12153 within the 30-day window is significantly more protective than waiting.

Even after the deadline passes, you can still pursue collection alternatives such as installment agreements or an Offer in Compromise by contacting the IRS directly. However, the IRS is not required to pause enforcement while those requests are being reviewed unless a formal CDP hearing is pending.

Frequently Asked Questions About The IRS LT11 And Letter 1058

What Is The Difference Between An LT11 And Letter 1058?

Both are the IRS's final notice of intent to levy and carry the same legal authority. The LT11 is generated by the IRS Automated Collection System, while Letter 1058 is typically issued by an IRS Revenue Officer assigned to your case. The response deadline and your rights are identical regardless of which version you receive.

How Long Do I Have To Respond To An LT11?

You have 30 days from the date printed on the notice to respond. According to the IRS, filing a CDP hearing request (Form 12153) within that window pauses all levy action and preserves your right to petition the U.S. Tax Court.

What Is The Difference Between A CP504 And An LT11?

The CP504 is the notice before the LT11 in the IRS collection sequence. According to the IRS, the CP504 authorizes the IRS to levy your state tax refund, while the LT11 authorizes levies on all other assets including wages, bank accounts, and personal property. The LT11 also grants you Collection Due Process hearing rights, which the CP504 does not.

IRS CP504 Notice: Intent To Levy — What To Do Now

What Is An IRS CP504 Notice

An IRS CP504 is a Notice of Intent to Levy, meaning the IRS is informing you that it will seize your state tax refund, wages, bank accounts, or other property if you do not pay your unpaid tax balance or make payment arrangements immediately. According to the IRS, the CP504 is issued under Internal Revenue Code Section 6331(d) and represents the final automated balance due reminder before the agency begins active enforcement. If you have received this notice, the IRS has already sent prior correspondence about the same unpaid balance and has not received payment or a response.

The CP504 includes your Social Security number, the date of the notice, and the specific tax year and form the balance relates to. It breaks the total amount owed into original tax, assessed penalties, and accrued interest. The notice also provides payment instructions, explains your right to appeal under the Collection Appeals Program, and describes the consequences of not responding. For a broader overview of how all IRS notices work and what different notice types mean, our complete guide to IRS correspondence covers every category from adjustments to enforcement.

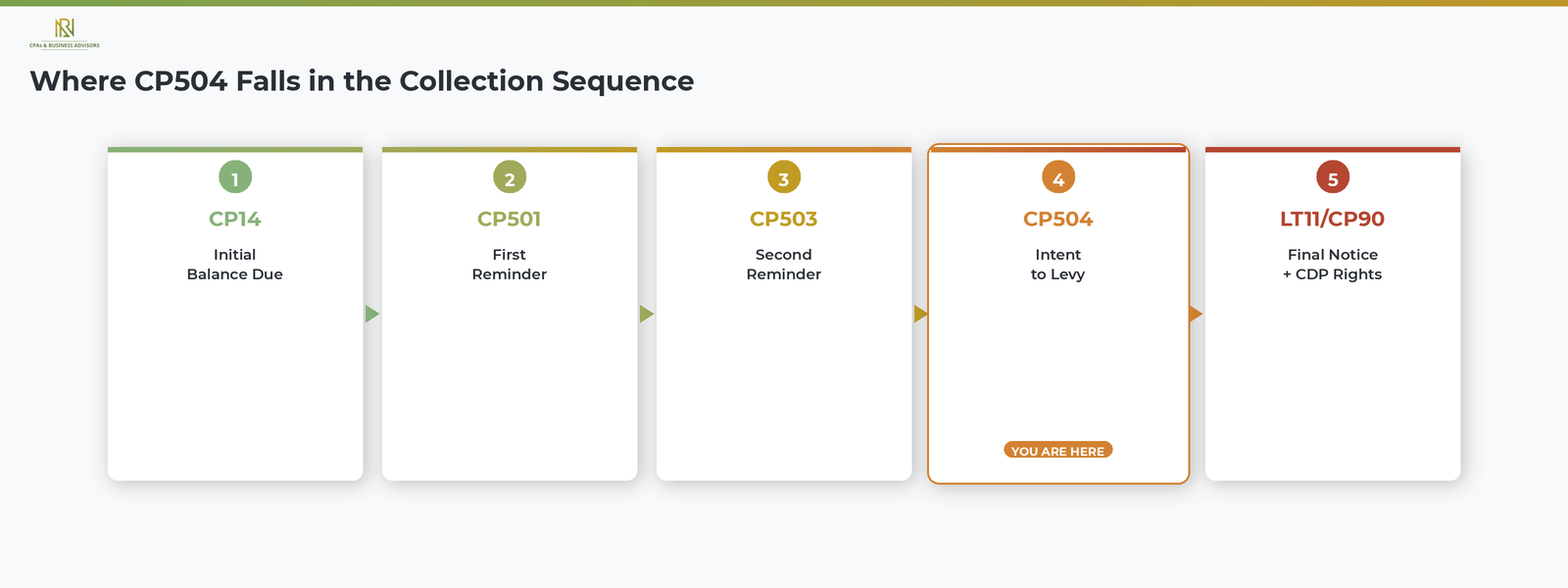

Where CP504 Falls In The IRS Collection Sequence

The CP504 is the fourth notice in a five-step collection sequence that the IRS follows when an individual taxpayer has an unpaid balance. Each notice in this sequence carries more urgency than the last, and the CP504 marks the transition point from automated reminders to active enforcement. According to the IRS, the standard progression works as follows.

- CP14: the initial notice that your tax return has an unpaid balance. Taxpayers who want to understand this first notice in the collection sequence can review our full guide to the CP14 balance due letter.

- CP501: a first reminder that the balance remains unpaid.

- CP503: a second reminder with stronger language, noting that the IRS has still not received payment.

- CP504: the Notice of Intent to Levy, warning that the IRS will begin seizing assets if you do not act.

- LT11 or CP90: the Final Notice of Intent to Levy, which grants you the right to request a Collection Due Process hearing within 30 days before the IRS proceeds.

The critical difference between the CP504 and the notices that came before it is that the CP504 authorizes the IRS to levy your state income tax refund without further notice. The final notices that follow, LT11 and CP90, authorize the IRS to levy everything else, including wages, bank accounts, and personal property.

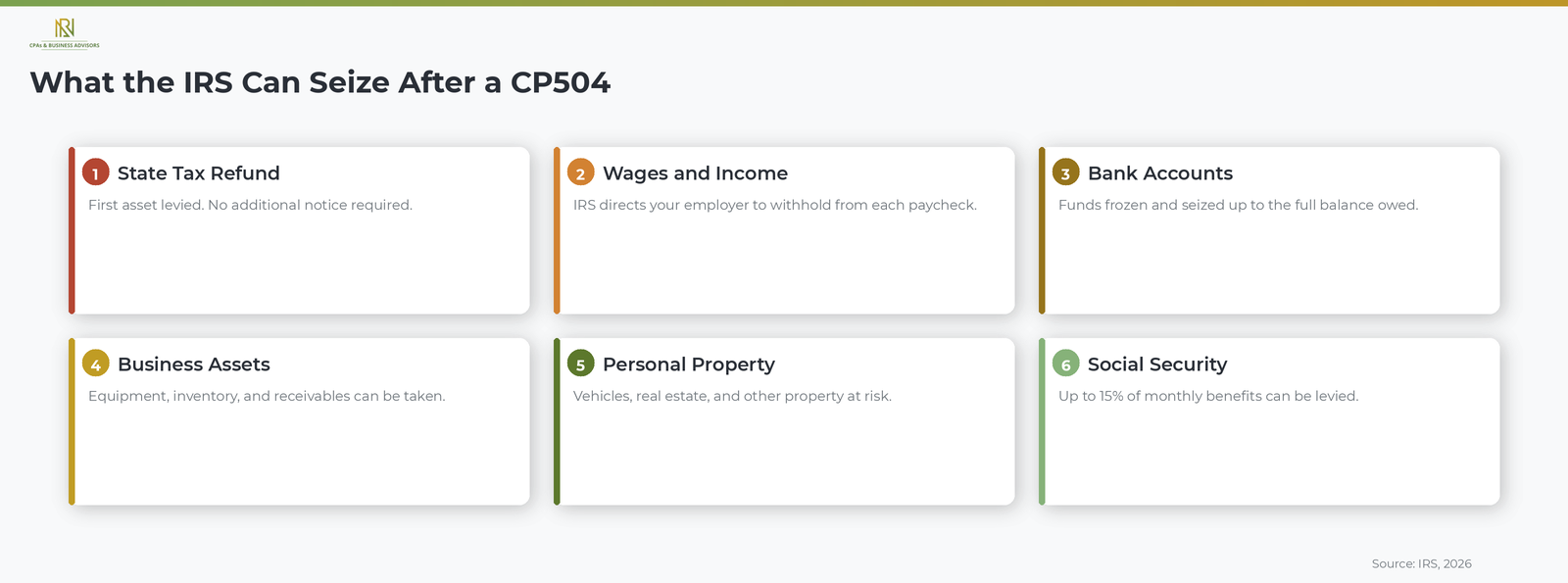

What The IRS Can Seize After A CP504 Notice

After sending a CP504, the IRS can immediately intercept your state income tax refund, and after issuing a subsequent final notice, it can seize virtually any other asset or income stream you have. According to the IRS, property subject to levy includes the following.

- State income tax refunds. According to the IRS, this is typically the first asset levied after a CP504 because the agency can intercept it without issuing an additional notice.

- Wages, salaries, and commissions. The IRS can direct your employer to withhold a portion of each paycheck until the debt is satisfied.

- Bank accounts. The IRS can freeze funds in your checking and savings accounts and seize the balance up to the total amount owed.

- Business assets. Equipment, inventory, and accounts receivable can all be seized to satisfy a business or individual tax debt.

- Personal property. According to the IRS, the agency can seize your vehicle, your home, and other real or personal property. The IRS is one of the few creditors authorized to take a personal residence despite state homestead protections.

- Social Security benefits. The IRS can levy up to 15 percent of your monthly Social Security payments.

In addition to levies, the IRS can file a Notice of Federal Tax Lien, which is a public claim against your current and future assets. According to the IRS, a lien can damage your credit, make it difficult to sell or refinance property, and establish the government's legal priority over other creditors. The FAST Act also authorizes the State Department to deny, revoke, or limit your passport if your tax debt meets the threshold for seriously delinquent tax debt.

How To Respond To An IRS CP504 Notice

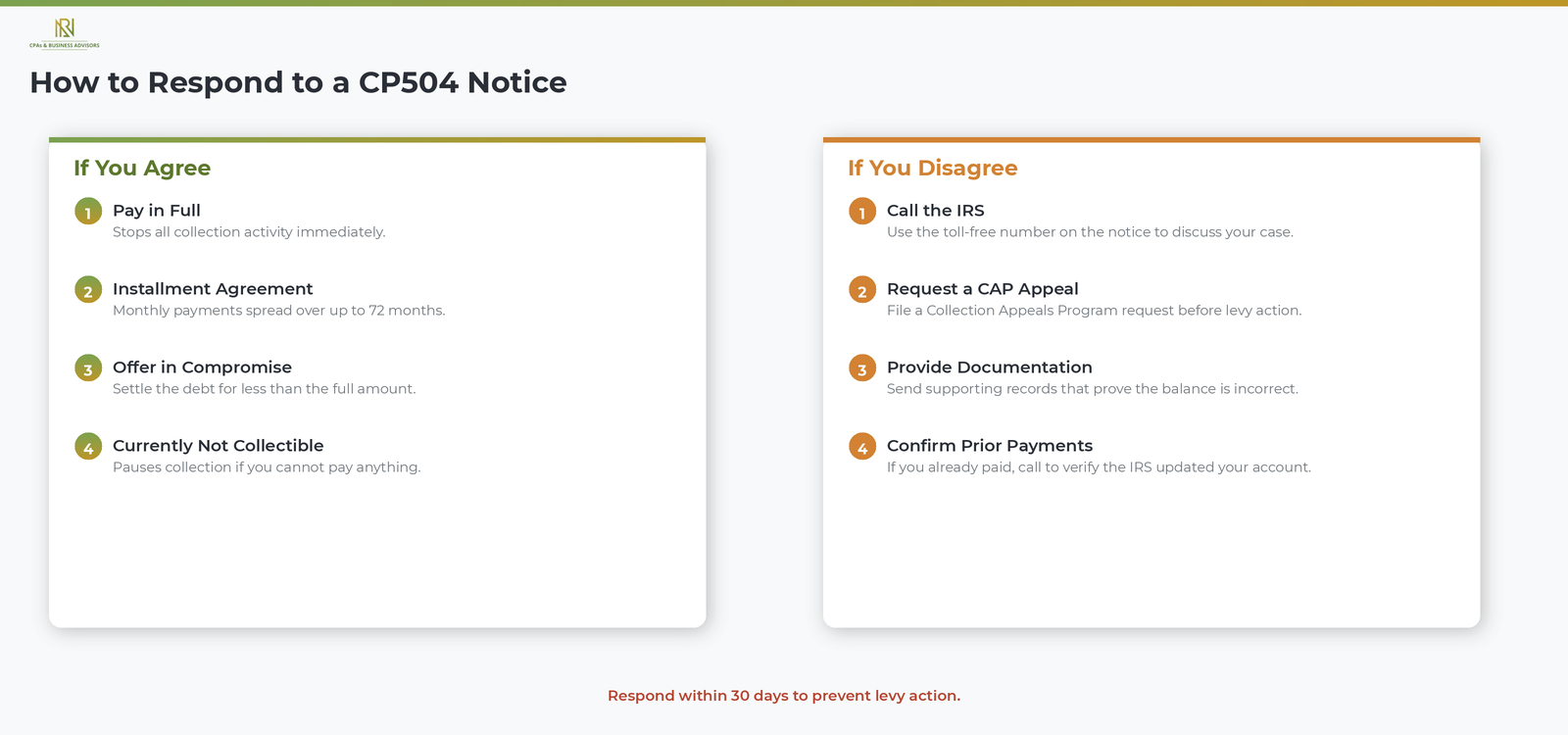

Respond to a CP504 as quickly as possible, ideally well within the 30-day window the IRS provides before taking levy action. Your best course of action depends on whether you agree or disagree with the amount the notice says you owe.

If You Agree With The Amount Owed

According to the IRS, you have several options for resolving the balance.

- Pay in full. The fastest way to stop collection activity is to pay the entire balance shown on the notice. You can pay online at IRS.gov, by phone, or by mailing a check with the payment voucher included in the notice.

- Set up an installment agreement. If you cannot pay the full amount at once, you may qualify for a monthly IRS payment plan or installment agreement. Our step-by-step guide to setting up structured payments covers the application process, balance thresholds, and how interest is calculated on the remaining amount.

- Submit an Offer in Compromise. If your financial situation makes it unlikely you can pay the full debt even with a payment plan, you may be able to settle for less than you owe through a formal Offer in Compromise.

- Request Currently Not Collectible status. If you have no ability to pay anything toward the debt, the IRS may temporarily pause collection activity by placing your account in Currently Not Collectible status. This does not eliminate the debt, but it stops levies while you remain unable to pay.

Taxpayers facing significant financial hardship may also qualify for the IRS Fresh Start program, which expands access to installment agreements and eases qualification thresholds for eligible individuals and businesses.

If You Disagree With The Amount Owed

If you believe the balance on the CP504 is incorrect, call the toll-free number printed on the notice immediately. According to the IRS, you can also request an appeal under the Collection Appeals Program before collection action takes place by following the instructions included in the notice. If you have already paid the balance or set up an installment agreement, contact the IRS at the number on the notice to confirm that your account reflects the payment or arrangement.

For general guidance on responding to any IRS correspondence, including how to organize supporting documentation and meet response deadlines, our guide on what to do when you receive an IRS notice provides a step-by-step walkthrough of the full response process.

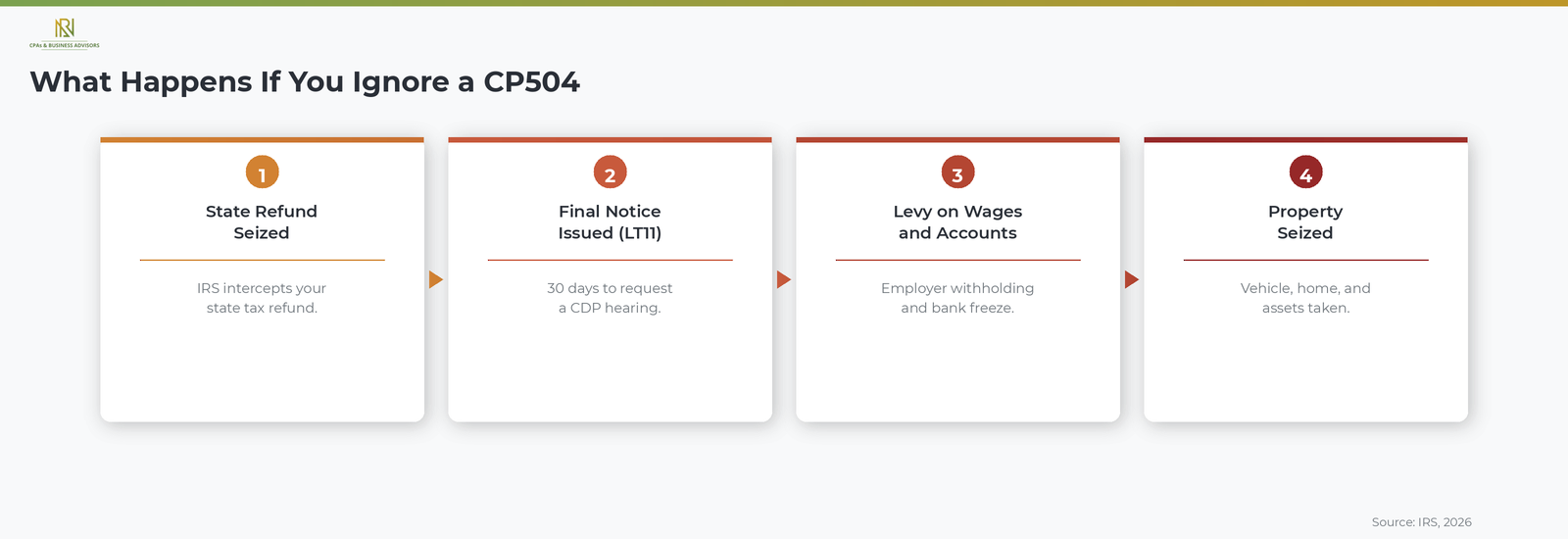

What Happens If You Ignore A CP504 Notice

Ignoring a CP504 causes the IRS to escalate to its final enforcement steps, beginning with the seizure of your state tax refund and progressing to levies on your wages, bank accounts, and personal property. According to the IRS, the next notice after the CP504 is typically the LT11 or Letter 1058, labeled "Final Notice of Intent to Levy and Notice of Your Right to a Hearing." This notice grants you the right to request a Collection Due Process hearing within 30 days, which is your last formal opportunity to challenge the proposed levy or present an alternative resolution before the IRS takes action.

If you do not respond to that final notice, the IRS can proceed with levying all available assets, filing a federal tax lien that becomes part of the public record and affects your credit, and, for balances meeting the seriously delinquent threshold, certifying your debt to the State Department for passport denial or revocation. Penalties and interest continue to accrue on the unpaid balance throughout this process, increasing the total amount owed with each month that passes.

Difference Between CP504 And CP504B

The CP504 is issued to individual taxpayers for unpaid personal income tax, while the CP504B is issued to businesses for unpaid business tax obligations such as employment taxes or excise taxes. According to the IRS, both notices carry the same intent to levy warning and the same level of urgency. If you received a CP504B for a business tax account, the response options and deadlines are the same as those described above for the standard CP504.

Frequently Asked Questions About The IRS CP504 Notice

How Serious Is A CP504 Notice?

A CP504 is one of the most urgent notices the IRS issues. According to the IRS, it is a formal Notice of Intent to Levy that authorizes the agency to begin seizing your state tax refund immediately and signals that levies on wages, bank accounts, and property will follow if you do not respond.

What Comes After A CP504 Notice?

The next step after a CP504 is typically the LT11 or Letter 1058, the Final Notice of Intent to Levy. According to the IRS, this final notice grants you 30 days to request a Collection Due Process hearing. If you do not respond, the IRS can proceed with levying your assets.

Is A CP504 Sent By Certified Mail?

The CP504 is typically sent by regular U.S. mail, not certified mail. According to the IRS, the subsequent final notice (LT11 or CP90) may arrive by certified mail because it triggers Collection Due Process hearing rights and the IRS must document delivery.

Can I Set Up A Payment Plan After Receiving A CP504?

Yes, you can still apply for an installment agreement after receiving a CP504. According to the IRS, you can apply online through the IRS Online Payment Agreement tool at IRS.gov or by calling the toll-free number printed on the notice. Setting up a payment plan stops the escalation toward active levy action as long as you remain current on your payments.