%201.avif)

.png)

.png)

IRS LT11 / Letter 1058: Final Notice Of Intent To Levy

What Is An IRS LT11 Notice Or Letter 1058

The IRS LT11 and Letter 1058 are the agency's final notice before it begins seizing your wages, bank accounts, and other property to collect an unpaid tax debt. According to the IRS, both notices serve the same legal purpose: they formally notify you of the IRS's intent to levy your assets under Internal Revenue Code Section 6331 and inform you of your right to request a Collection Due Process hearing before that levy occurs. Receiving either notice means the IRS has exhausted its standard collection reminders and is now authorized to take enforcement action.

The LT11 and Letter 1058 are alternative forms of the same final notice. The LT11 is generated by the IRS Automated Collection System and is typically the version most individual taxpayers receive. Letter 1058 is usually issued by an IRS Revenue Officer who has been assigned to your case directly. Regardless of which version you receive, the legal weight and response deadline are identical. For a broader overview of how all IRS notices work and where this notice fits in the system, our complete guide to IRS correspondence covers every notice category.

Why You Received An LT11 Or Letter 1058

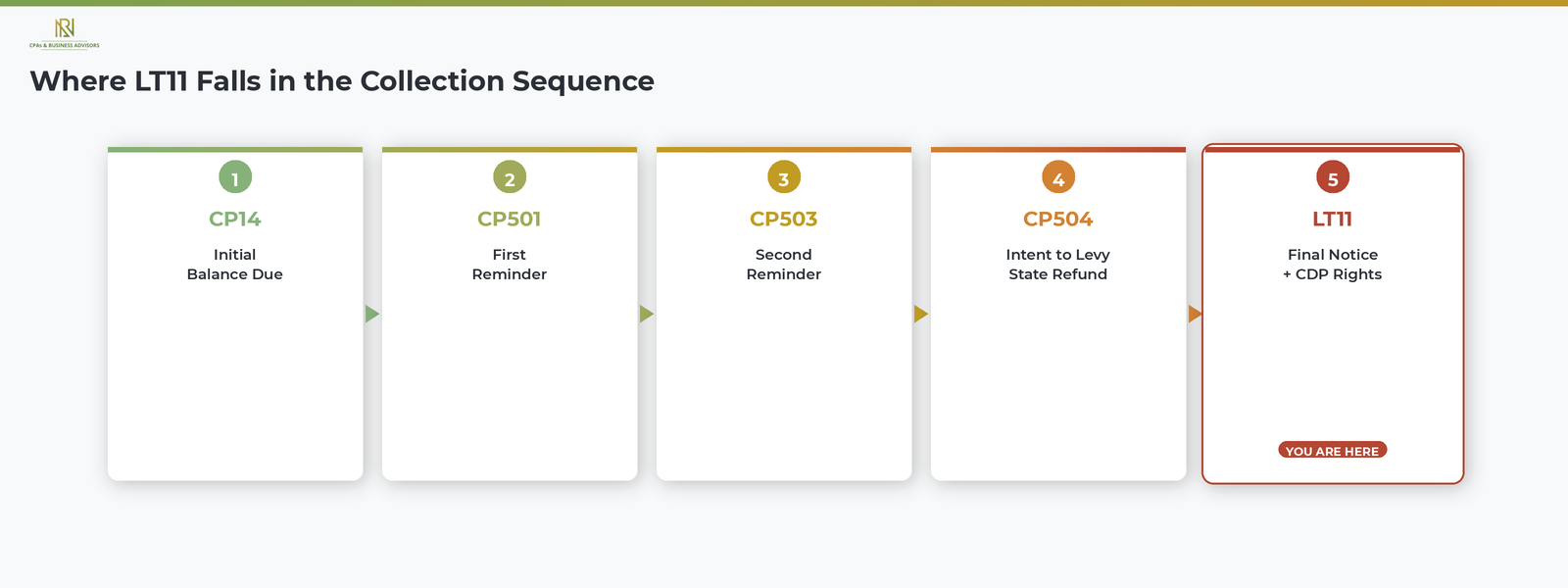

You received an LT11 or Letter 1058 because the IRS sent you multiple prior notices about an unpaid tax balance and did not receive payment or a response. According to the IRS, this final notice comes at the end of a collection sequence that typically includes four earlier notices.

- CP14: the initial notice that your return has an unpaid balance.

- CP501: a first reminder that the balance remains unpaid.

- CP503: a second reminder with stronger language.

- CP504: a Notice of Intent to Levy, warning that the IRS will begin seizing your state tax refund. Taxpayers who received a CP504 notice and want to understand that step in the process can review our full explanation of the CP504 and its response options.

- LT11 or Letter 1058: the final notice, authorizing the IRS to levy wages, bank accounts, and all other property.

The LT11 prominently displays the heading "Notice of Intent to Levy and Your Collection Due Process Right to a Hearing" on the first page. Letter 1058 uses similar language: "Final Notice, Notice of Intent to Levy and Notice of Your Rights to a Hearing." Both make clear that the IRS will proceed with enforcement unless you act within the deadline.

The 30 Day Deadline And Your Right To A CDP Hearing

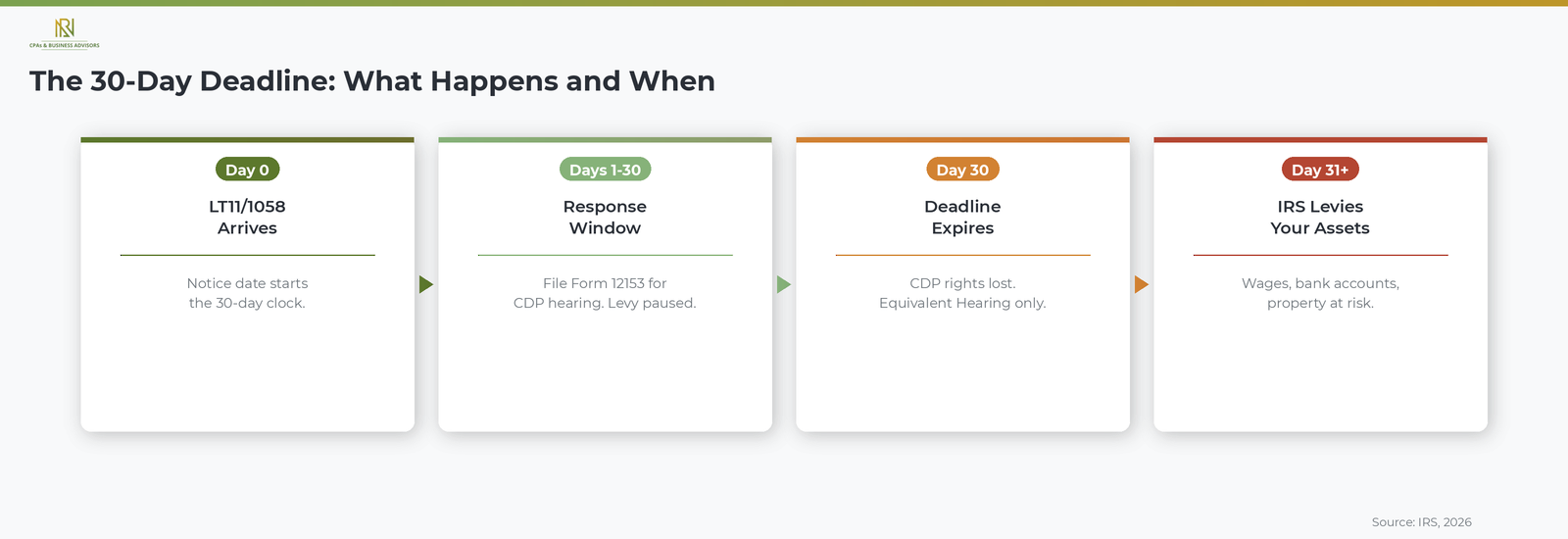

You have exactly 30 days from the date printed on the LT11 or Letter 1058 to respond, and filing within that window is critical because it preserves your right to a Collection Due Process hearing and temporarily stops all levy action. According to the IRS, a Collection Due Process hearing is conducted by the IRS Independent Office of Appeals, which is separate from the division that issued the notice.

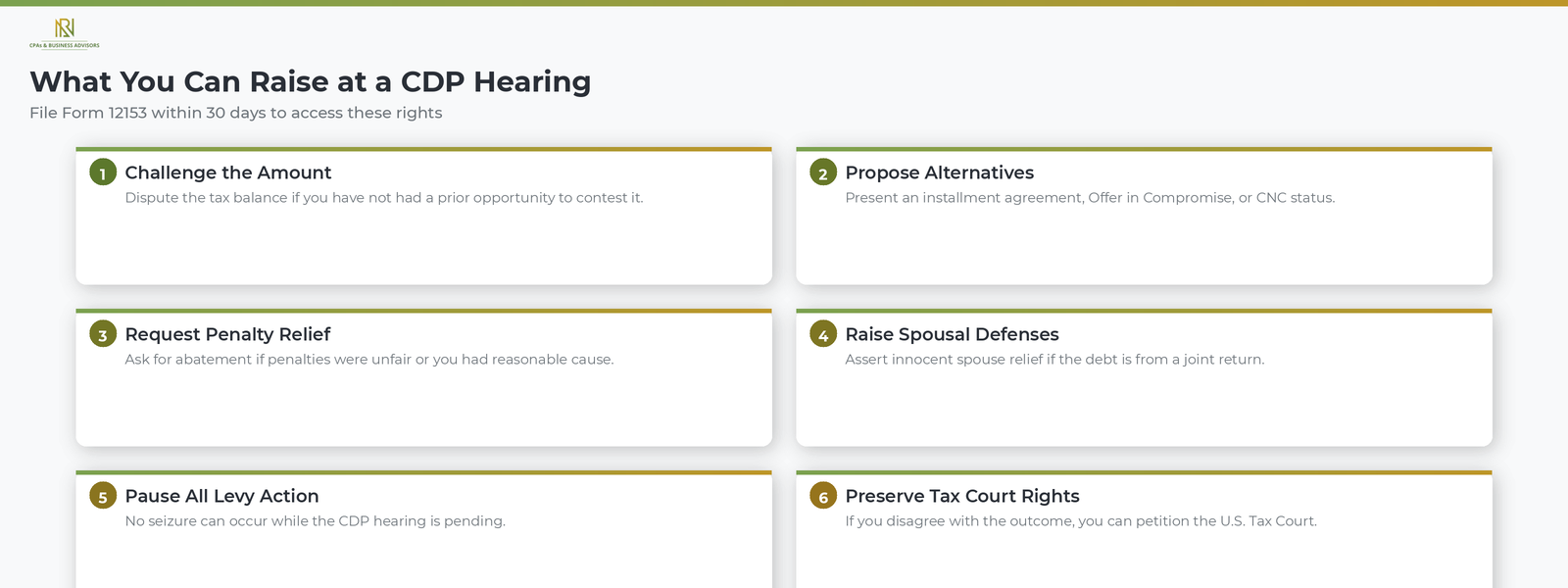

To request a CDP hearing, file Form 12153, Request for a Collection Due Process or Equivalent Hearing, within 30 days of the notice date. During the hearing, you can raise the following issues.

- Challenge the amount owed. If you believe the tax balance is incorrect and have not had a prior opportunity to dispute it, you can contest the underlying liability.

- Propose collection alternatives. You can present options such as an installment agreement, an Offer in Compromise, or Currently Not Collectible status as alternatives to a levy.

- Request penalty abatement. If penalties were applied unfairly or you had reasonable cause for late payment, you can ask for penalty relief.

- Argue spousal defenses. If the debt relates to a joint return and you qualify, you can raise innocent spouse relief.

According to the IRS, no levy action can occur while a CDP hearing request is pending, which makes filing within the 30-day window one of the most effective ways to stop or delay enforcement. A CDP hearing also preserves your right to petition the U.S. Tax Court if you disagree with the Appeals Office decision.

What The IRS Can Levy After Sending An LT11

After the 30-day response window on an LT11 or Letter 1058 expires without action, the IRS is authorized to levy virtually any asset or income stream you have. According to the IRS, property subject to levy includes the following.

- Wages, salaries, and commissions. The IRS can contact your employer and require a portion of each paycheck to be withheld until the debt is satisfied.

- Bank accounts. The IRS can freeze and seize funds in your checking and savings accounts up to the full balance owed.

- State tax refunds. Any state income tax refund you are entitled to can be intercepted.

- Business assets. Equipment, inventory, and accounts receivable can be seized.

- Personal property. According to the IRS, the agency can seize your vehicle, your home, and other real or personal property.

- Social Security benefits. The IRS can levy up to 15 percent of your monthly Social Security payments.

- Retirement accounts. The IRS can levy 401(k) and IRA funds. According to the IRS, amounts withdrawn through a levy are treated as taxable income but are not subject to the 10 percent early withdrawal penalty that normally applies to distributions taken before age 59 and a half.

In addition to levies, the IRS can file a Notice of Federal Tax Lien, which publicly establishes the government's claim against your current and future assets and can damage your credit. The FAST Act also authorizes the State Department to deny, revoke, or limit your passport if your balance meets the seriously delinquent tax debt threshold.

How To Respond To An LT11 Or Letter 1058

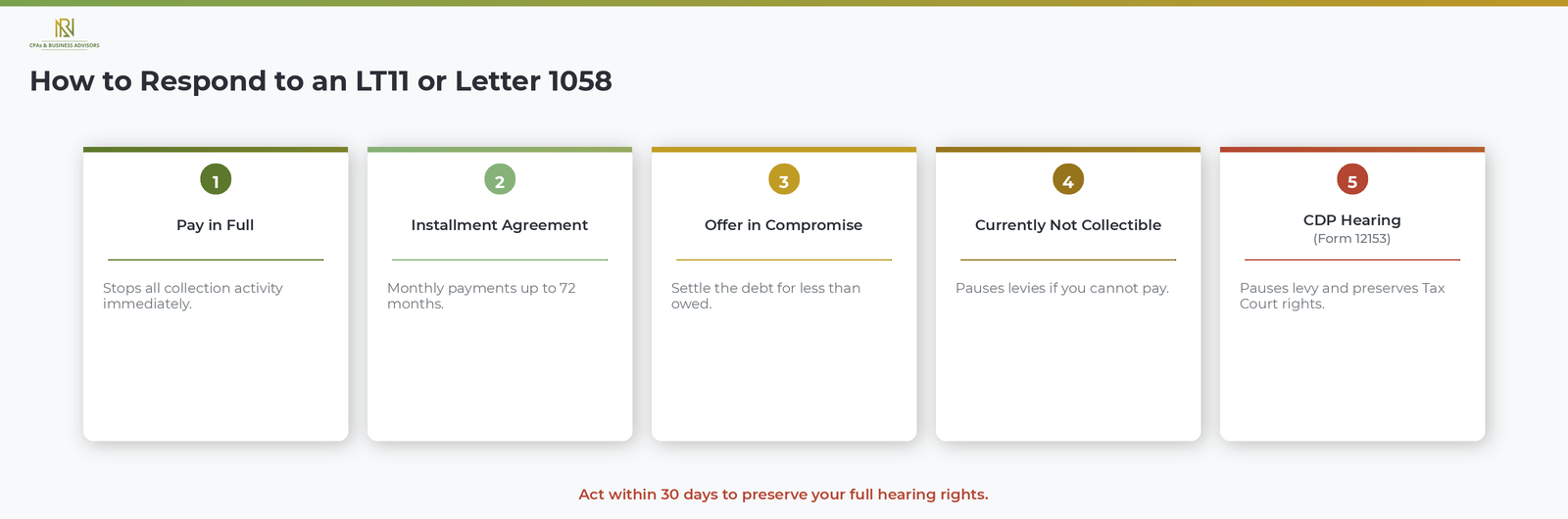

The best response depends on your financial situation and whether you agree with the balance the IRS says you owe, but in every case responding before the 30-day deadline is essential.

- Pay the balance in full. The fastest way to stop all collection activity. You can pay online at IRS.gov, by phone, or by mailing a check with the payment voucher from the notice.

- Set up an installment agreement. If you cannot pay in full, you may qualify for a monthly IRS payment plan or installment agreement. Taxpayers who owe less than $50,000 can apply for a streamlined agreement online. Our step-by-step guide to payment plans covers the full application process and balance thresholds.

- Submit an Offer in Compromise. If your financial circumstances make the full debt unlikely to be collected, you may be able to settle for less than you owe.

- Request Currently Not Collectible status. If you have no ability to pay anything, the IRS may temporarily suspend collection activity. The debt remains, but levies stop while you remain unable to pay.

- Request a CDP hearing. File Form 12153 within 30 days to pause the levy and present your case to an independent Appeals officer.

Taxpayers facing significant hardship may also qualify for the IRS Fresh Start program, which broadens eligibility for installment agreements and penalty relief for individuals and businesses with qualifying balances.

What Happens If You Miss The 30 Day Deadline

If you do not respond within 30 days of the date on the LT11 or Letter 1058, the IRS can immediately begin levying your assets, and your hearing rights are reduced. According to the IRS, you can still request what is called an Equivalent Hearing after the 30-day window closes, but an Equivalent Hearing does not stop levy action while it is pending and does not give you the right to petition the U.S. Tax Court if you disagree with the outcome. For this reason, filing Form 12153 within the 30-day window is significantly more protective than waiting.

Even after the deadline passes, you can still pursue collection alternatives such as installment agreements or an Offer in Compromise by contacting the IRS directly. However, the IRS is not required to pause enforcement while those requests are being reviewed unless a formal CDP hearing is pending.

Frequently Asked Questions About The IRS LT11 And Letter 1058

What Is The Difference Between An LT11 And Letter 1058?

Both are the IRS's final notice of intent to levy and carry the same legal authority. The LT11 is generated by the IRS Automated Collection System, while Letter 1058 is typically issued by an IRS Revenue Officer assigned to your case. The response deadline and your rights are identical regardless of which version you receive.

How Long Do I Have To Respond To An LT11?

You have 30 days from the date printed on the notice to respond. According to the IRS, filing a CDP hearing request (Form 12153) within that window pauses all levy action and preserves your right to petition the U.S. Tax Court.

What Is The Difference Between A CP504 And An LT11?

The CP504 is the notice before the LT11 in the IRS collection sequence. According to the IRS, the CP504 authorizes the IRS to levy your state tax refund, while the LT11 authorizes levies on all other assets including wages, bank accounts, and personal property. The LT11 also grants you Collection Due Process hearing rights, which the CP504 does not.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

IRS LT11 / Letter 1058: Final Notice Of Intent To Levy

What Is An IRS LT11 Notice Or Letter 1058

The IRS LT11 and Letter 1058 are the agency's final notice before it begins seizing your wages, bank accounts, and other property to collect an unpaid tax debt. According to the IRS, both notices serve the same legal purpose: they formally notify you of the IRS's intent to levy your assets under Internal Revenue Code Section 6331 and inform you of your right to request a Collection Due Process hearing before that levy occurs. Receiving either notice means the IRS has exhausted its standard collection reminders and is now authorized to take enforcement action.

The LT11 and Letter 1058 are alternative forms of the same final notice. The LT11 is generated by the IRS Automated Collection System and is typically the version most individual taxpayers receive. Letter 1058 is usually issued by an IRS Revenue Officer who has been assigned to your case directly. Regardless of which version you receive, the legal weight and response deadline are identical. For a broader overview of how all IRS notices work and where this notice fits in the system, our complete guide to IRS correspondence covers every notice category.

Why You Received An LT11 Or Letter 1058

You received an LT11 or Letter 1058 because the IRS sent you multiple prior notices about an unpaid tax balance and did not receive payment or a response. According to the IRS, this final notice comes at the end of a collection sequence that typically includes four earlier notices.

- CP14: the initial notice that your return has an unpaid balance.

- CP501: a first reminder that the balance remains unpaid.

- CP503: a second reminder with stronger language.

- CP504: a Notice of Intent to Levy, warning that the IRS will begin seizing your state tax refund. Taxpayers who received a CP504 notice and want to understand that step in the process can review our full explanation of the CP504 and its response options.

- LT11 or Letter 1058: the final notice, authorizing the IRS to levy wages, bank accounts, and all other property.

The LT11 prominently displays the heading "Notice of Intent to Levy and Your Collection Due Process Right to a Hearing" on the first page. Letter 1058 uses similar language: "Final Notice, Notice of Intent to Levy and Notice of Your Rights to a Hearing." Both make clear that the IRS will proceed with enforcement unless you act within the deadline.

The 30 Day Deadline And Your Right To A CDP Hearing

You have exactly 30 days from the date printed on the LT11 or Letter 1058 to respond, and filing within that window is critical because it preserves your right to a Collection Due Process hearing and temporarily stops all levy action. According to the IRS, a Collection Due Process hearing is conducted by the IRS Independent Office of Appeals, which is separate from the division that issued the notice.

To request a CDP hearing, file Form 12153, Request for a Collection Due Process or Equivalent Hearing, within 30 days of the notice date. During the hearing, you can raise the following issues.

- Challenge the amount owed. If you believe the tax balance is incorrect and have not had a prior opportunity to dispute it, you can contest the underlying liability.

- Propose collection alternatives. You can present options such as an installment agreement, an Offer in Compromise, or Currently Not Collectible status as alternatives to a levy.

- Request penalty abatement. If penalties were applied unfairly or you had reasonable cause for late payment, you can ask for penalty relief.

- Argue spousal defenses. If the debt relates to a joint return and you qualify, you can raise innocent spouse relief.

According to the IRS, no levy action can occur while a CDP hearing request is pending, which makes filing within the 30-day window one of the most effective ways to stop or delay enforcement. A CDP hearing also preserves your right to petition the U.S. Tax Court if you disagree with the Appeals Office decision.

What The IRS Can Levy After Sending An LT11

After the 30-day response window on an LT11 or Letter 1058 expires without action, the IRS is authorized to levy virtually any asset or income stream you have. According to the IRS, property subject to levy includes the following.

- Wages, salaries, and commissions. The IRS can contact your employer and require a portion of each paycheck to be withheld until the debt is satisfied.

- Bank accounts. The IRS can freeze and seize funds in your checking and savings accounts up to the full balance owed.

- State tax refunds. Any state income tax refund you are entitled to can be intercepted.

- Business assets. Equipment, inventory, and accounts receivable can be seized.

- Personal property. According to the IRS, the agency can seize your vehicle, your home, and other real or personal property.

- Social Security benefits. The IRS can levy up to 15 percent of your monthly Social Security payments.

- Retirement accounts. The IRS can levy 401(k) and IRA funds. According to the IRS, amounts withdrawn through a levy are treated as taxable income but are not subject to the 10 percent early withdrawal penalty that normally applies to distributions taken before age 59 and a half.

In addition to levies, the IRS can file a Notice of Federal Tax Lien, which publicly establishes the government's claim against your current and future assets and can damage your credit. The FAST Act also authorizes the State Department to deny, revoke, or limit your passport if your balance meets the seriously delinquent tax debt threshold.

How To Respond To An LT11 Or Letter 1058

The best response depends on your financial situation and whether you agree with the balance the IRS says you owe, but in every case responding before the 30-day deadline is essential.

- Pay the balance in full. The fastest way to stop all collection activity. You can pay online at IRS.gov, by phone, or by mailing a check with the payment voucher from the notice.

- Set up an installment agreement. If you cannot pay in full, you may qualify for a monthly IRS payment plan or installment agreement. Taxpayers who owe less than $50,000 can apply for a streamlined agreement online. Our step-by-step guide to payment plans covers the full application process and balance thresholds.

- Submit an Offer in Compromise. If your financial circumstances make the full debt unlikely to be collected, you may be able to settle for less than you owe.

- Request Currently Not Collectible status. If you have no ability to pay anything, the IRS may temporarily suspend collection activity. The debt remains, but levies stop while you remain unable to pay.

- Request a CDP hearing. File Form 12153 within 30 days to pause the levy and present your case to an independent Appeals officer.

Taxpayers facing significant hardship may also qualify for the IRS Fresh Start program, which broadens eligibility for installment agreements and penalty relief for individuals and businesses with qualifying balances.

What Happens If You Miss The 30 Day Deadline

If you do not respond within 30 days of the date on the LT11 or Letter 1058, the IRS can immediately begin levying your assets, and your hearing rights are reduced. According to the IRS, you can still request what is called an Equivalent Hearing after the 30-day window closes, but an Equivalent Hearing does not stop levy action while it is pending and does not give you the right to petition the U.S. Tax Court if you disagree with the outcome. For this reason, filing Form 12153 within the 30-day window is significantly more protective than waiting.

Even after the deadline passes, you can still pursue collection alternatives such as installment agreements or an Offer in Compromise by contacting the IRS directly. However, the IRS is not required to pause enforcement while those requests are being reviewed unless a formal CDP hearing is pending.

Frequently Asked Questions About The IRS LT11 And Letter 1058

What Is The Difference Between An LT11 And Letter 1058?

Both are the IRS's final notice of intent to levy and carry the same legal authority. The LT11 is generated by the IRS Automated Collection System, while Letter 1058 is typically issued by an IRS Revenue Officer assigned to your case. The response deadline and your rights are identical regardless of which version you receive.

How Long Do I Have To Respond To An LT11?

You have 30 days from the date printed on the notice to respond. According to the IRS, filing a CDP hearing request (Form 12153) within that window pauses all levy action and preserves your right to petition the U.S. Tax Court.

What Is The Difference Between A CP504 And An LT11?

The CP504 is the notice before the LT11 in the IRS collection sequence. According to the IRS, the CP504 authorizes the IRS to levy your state tax refund, while the LT11 authorizes levies on all other assets including wages, bank accounts, and personal property. The LT11 also grants you Collection Due Process hearing rights, which the CP504 does not.

IRS CP504 Notice: Intent To Levy — What To Do Now

What Is An IRS CP504 Notice

An IRS CP504 is a Notice of Intent to Levy, meaning the IRS is informing you that it will seize your state tax refund, wages, bank accounts, or other property if you do not pay your unpaid tax balance or make payment arrangements immediately. According to the IRS, the CP504 is issued under Internal Revenue Code Section 6331(d) and represents the final automated balance due reminder before the agency begins active enforcement. If you have received this notice, the IRS has already sent prior correspondence about the same unpaid balance and has not received payment or a response.

The CP504 includes your Social Security number, the date of the notice, and the specific tax year and form the balance relates to. It breaks the total amount owed into original tax, assessed penalties, and accrued interest. The notice also provides payment instructions, explains your right to appeal under the Collection Appeals Program, and describes the consequences of not responding. For a broader overview of how all IRS notices work and what different notice types mean, our complete guide to IRS correspondence covers every category from adjustments to enforcement.

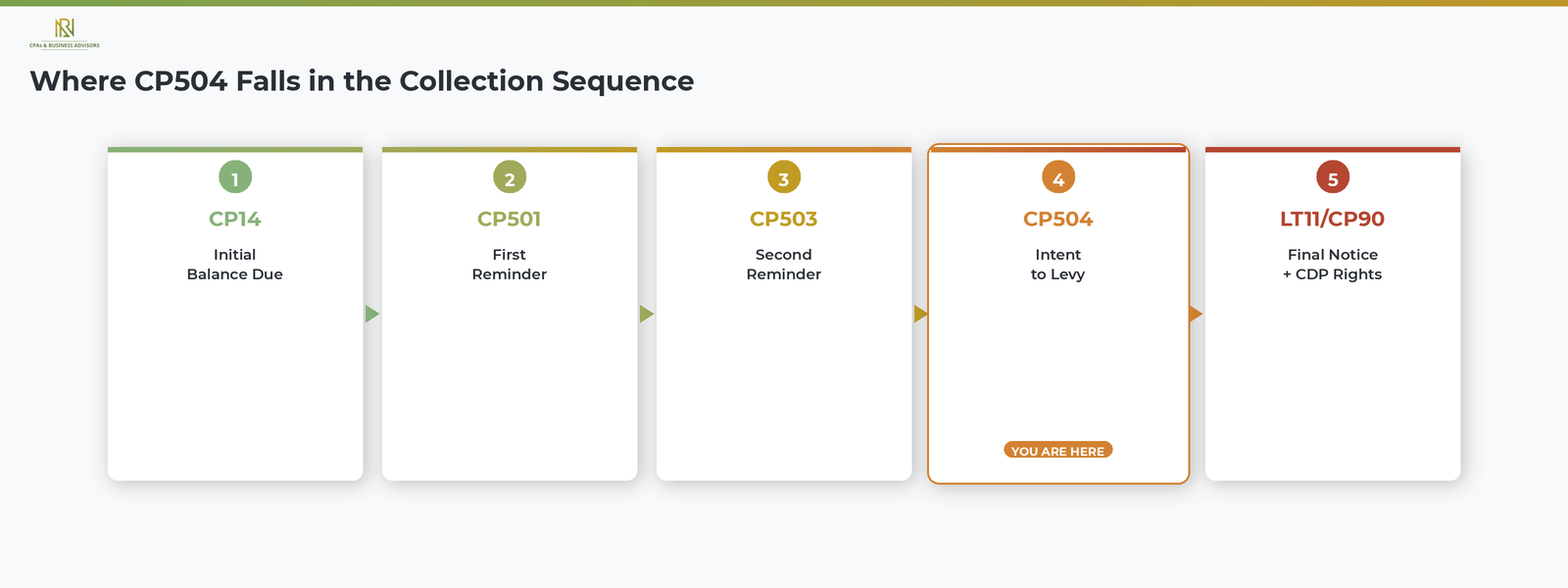

Where CP504 Falls In The IRS Collection Sequence

The CP504 is the fourth notice in a five-step collection sequence that the IRS follows when an individual taxpayer has an unpaid balance. Each notice in this sequence carries more urgency than the last, and the CP504 marks the transition point from automated reminders to active enforcement. According to the IRS, the standard progression works as follows.

- CP14: the initial notice that your tax return has an unpaid balance. Taxpayers who want to understand this first notice in the collection sequence can review our full guide to the CP14 balance due letter.

- CP501: a first reminder that the balance remains unpaid.

- CP503: a second reminder with stronger language, noting that the IRS has still not received payment.

- CP504: the Notice of Intent to Levy, warning that the IRS will begin seizing assets if you do not act.

- LT11 or CP90: the Final Notice of Intent to Levy, which grants you the right to request a Collection Due Process hearing within 30 days before the IRS proceeds.

The critical difference between the CP504 and the notices that came before it is that the CP504 authorizes the IRS to levy your state income tax refund without further notice. The final notices that follow, LT11 and CP90, authorize the IRS to levy everything else, including wages, bank accounts, and personal property.

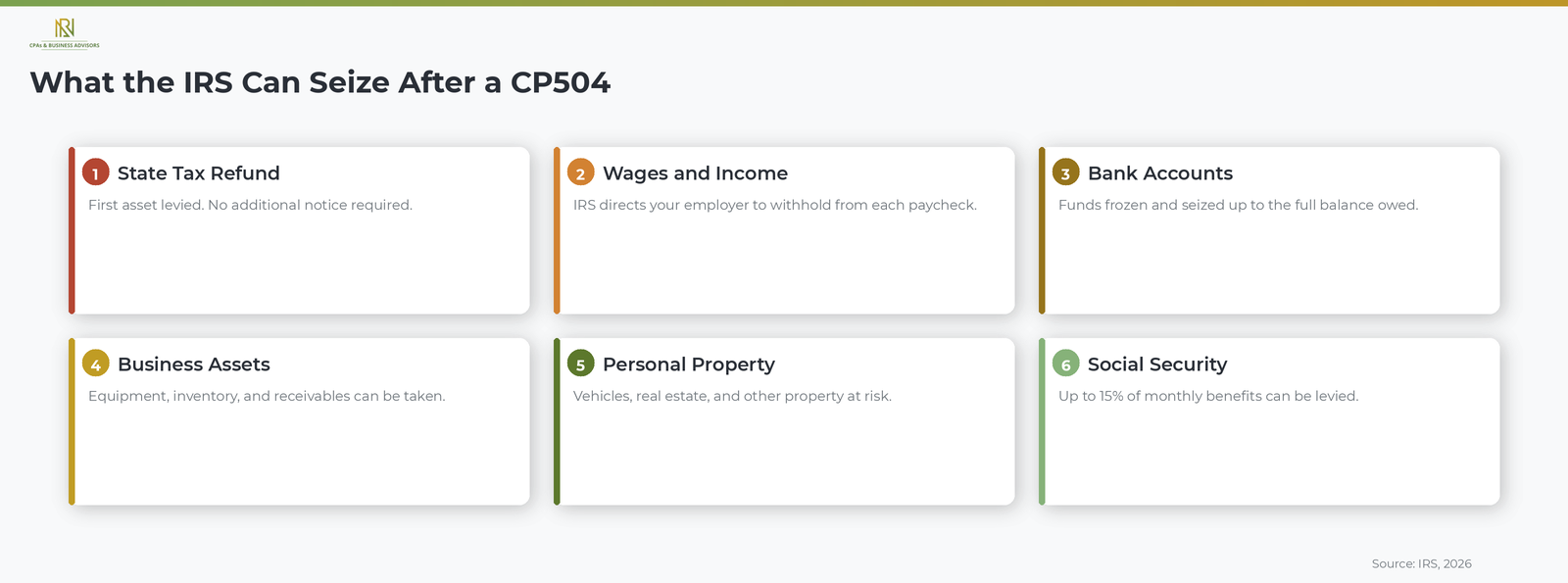

What The IRS Can Seize After A CP504 Notice

After sending a CP504, the IRS can immediately intercept your state income tax refund, and after issuing a subsequent final notice, it can seize virtually any other asset or income stream you have. According to the IRS, property subject to levy includes the following.

- State income tax refunds. According to the IRS, this is typically the first asset levied after a CP504 because the agency can intercept it without issuing an additional notice.

- Wages, salaries, and commissions. The IRS can direct your employer to withhold a portion of each paycheck until the debt is satisfied.

- Bank accounts. The IRS can freeze funds in your checking and savings accounts and seize the balance up to the total amount owed.

- Business assets. Equipment, inventory, and accounts receivable can all be seized to satisfy a business or individual tax debt.

- Personal property. According to the IRS, the agency can seize your vehicle, your home, and other real or personal property. The IRS is one of the few creditors authorized to take a personal residence despite state homestead protections.

- Social Security benefits. The IRS can levy up to 15 percent of your monthly Social Security payments.

In addition to levies, the IRS can file a Notice of Federal Tax Lien, which is a public claim against your current and future assets. According to the IRS, a lien can damage your credit, make it difficult to sell or refinance property, and establish the government's legal priority over other creditors. The FAST Act also authorizes the State Department to deny, revoke, or limit your passport if your tax debt meets the threshold for seriously delinquent tax debt.

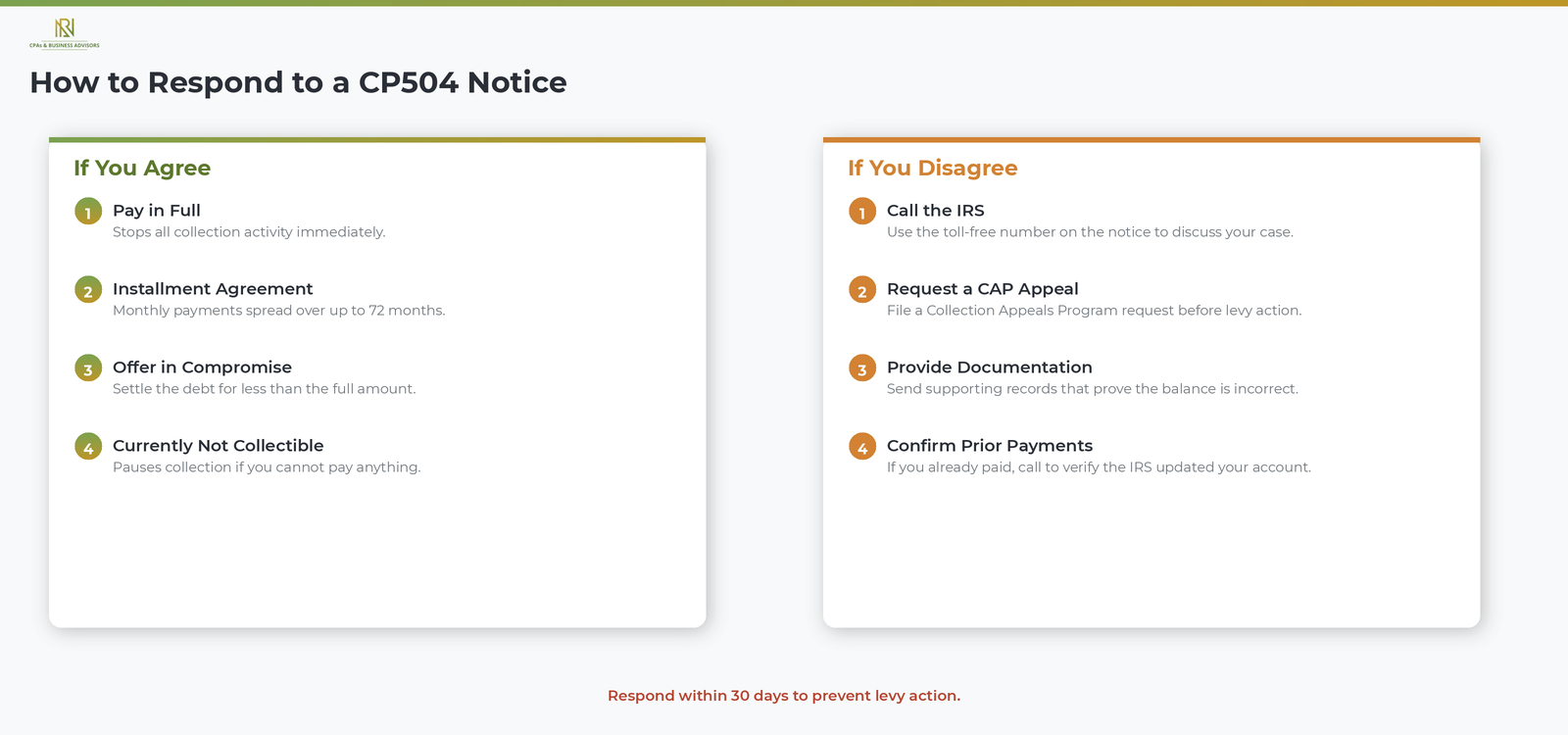

How To Respond To An IRS CP504 Notice

Respond to a CP504 as quickly as possible, ideally well within the 30-day window the IRS provides before taking levy action. Your best course of action depends on whether you agree or disagree with the amount the notice says you owe.

If You Agree With The Amount Owed

According to the IRS, you have several options for resolving the balance.

- Pay in full. The fastest way to stop collection activity is to pay the entire balance shown on the notice. You can pay online at IRS.gov, by phone, or by mailing a check with the payment voucher included in the notice.

- Set up an installment agreement. If you cannot pay the full amount at once, you may qualify for a monthly IRS payment plan or installment agreement. Our step-by-step guide to setting up structured payments covers the application process, balance thresholds, and how interest is calculated on the remaining amount.

- Submit an Offer in Compromise. If your financial situation makes it unlikely you can pay the full debt even with a payment plan, you may be able to settle for less than you owe through a formal Offer in Compromise.

- Request Currently Not Collectible status. If you have no ability to pay anything toward the debt, the IRS may temporarily pause collection activity by placing your account in Currently Not Collectible status. This does not eliminate the debt, but it stops levies while you remain unable to pay.

Taxpayers facing significant financial hardship may also qualify for the IRS Fresh Start program, which expands access to installment agreements and eases qualification thresholds for eligible individuals and businesses.

If You Disagree With The Amount Owed

If you believe the balance on the CP504 is incorrect, call the toll-free number printed on the notice immediately. According to the IRS, you can also request an appeal under the Collection Appeals Program before collection action takes place by following the instructions included in the notice. If you have already paid the balance or set up an installment agreement, contact the IRS at the number on the notice to confirm that your account reflects the payment or arrangement.

For general guidance on responding to any IRS correspondence, including how to organize supporting documentation and meet response deadlines, our guide on what to do when you receive an IRS notice provides a step-by-step walkthrough of the full response process.

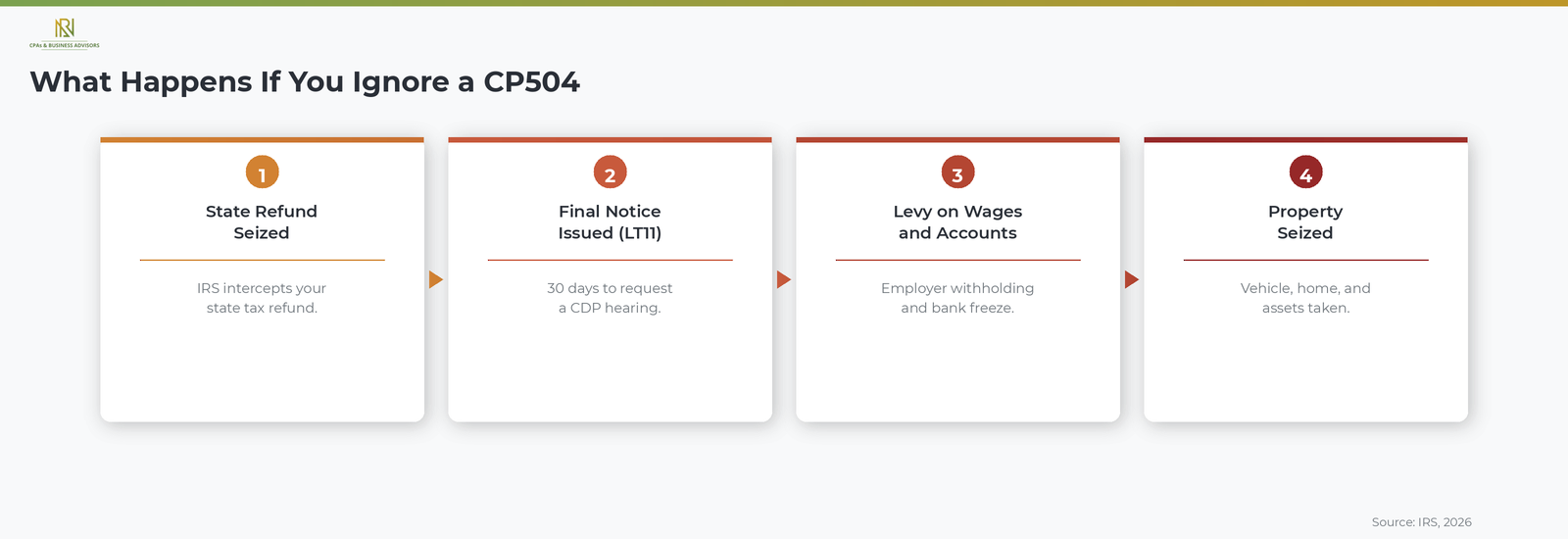

What Happens If You Ignore A CP504 Notice

Ignoring a CP504 causes the IRS to escalate to its final enforcement steps, beginning with the seizure of your state tax refund and progressing to levies on your wages, bank accounts, and personal property. According to the IRS, the next notice after the CP504 is typically the LT11 or Letter 1058, labeled "Final Notice of Intent to Levy and Notice of Your Right to a Hearing." This notice grants you the right to request a Collection Due Process hearing within 30 days, which is your last formal opportunity to challenge the proposed levy or present an alternative resolution before the IRS takes action.

If you do not respond to that final notice, the IRS can proceed with levying all available assets, filing a federal tax lien that becomes part of the public record and affects your credit, and, for balances meeting the seriously delinquent threshold, certifying your debt to the State Department for passport denial or revocation. Penalties and interest continue to accrue on the unpaid balance throughout this process, increasing the total amount owed with each month that passes.

Difference Between CP504 And CP504B

The CP504 is issued to individual taxpayers for unpaid personal income tax, while the CP504B is issued to businesses for unpaid business tax obligations such as employment taxes or excise taxes. According to the IRS, both notices carry the same intent to levy warning and the same level of urgency. If you received a CP504B for a business tax account, the response options and deadlines are the same as those described above for the standard CP504.

Frequently Asked Questions About The IRS CP504 Notice

How Serious Is A CP504 Notice?

A CP504 is one of the most urgent notices the IRS issues. According to the IRS, it is a formal Notice of Intent to Levy that authorizes the agency to begin seizing your state tax refund immediately and signals that levies on wages, bank accounts, and property will follow if you do not respond.

What Comes After A CP504 Notice?

The next step after a CP504 is typically the LT11 or Letter 1058, the Final Notice of Intent to Levy. According to the IRS, this final notice grants you 30 days to request a Collection Due Process hearing. If you do not respond, the IRS can proceed with levying your assets.

Is A CP504 Sent By Certified Mail?

The CP504 is typically sent by regular U.S. mail, not certified mail. According to the IRS, the subsequent final notice (LT11 or CP90) may arrive by certified mail because it triggers Collection Due Process hearing rights and the IRS must document delivery.

Can I Set Up A Payment Plan After Receiving A CP504?

Yes, you can still apply for an installment agreement after receiving a CP504. According to the IRS, you can apply online through the IRS Online Payment Agreement tool at IRS.gov or by calling the toll-free number printed on the notice. Setting up a payment plan stops the escalation toward active levy action as long as you remain current on your payments.