%201.avif)

.png)

.png)

How to Create a Strategic Business Plan

A strategic business plan is a structured document that defines your company's long-term goals, outlines the strategies you will use to reach those goals, and maps the financial projections and action steps required to get there. Unlike a basic business plan that focuses on day-to-day operations, a strategic plan connects your mission to measurable outcomes over a one-year, three-year, or five-year horizon. According to SBA-cited research, businesses with formal plans grow 30% faster than those without clear objectives. This article walks through what a strategic business plan includes, how it differs from a standard business plan, and the step-by-step process for building one that keeps your company focused, funded, and growing.

What Is a Strategic Business Plan?

A strategic business plan is a forward-looking document that defines where your business is headed, how it will get there, and how you will measure progress along the way. A strategic business plan typically covers a one-to-five-year period and includes your company's mission statement, a SWOT analysis, specific goals with timelines, the strategies and action plans to achieve those goals, financial projections, key performance indicators (KPIs), and an executive summary. Each section builds on the one before it, creating a single reference point for every major decision the business makes.

Strategic business plans serve both internal and external purposes. Internally, the plan aligns your team around shared goals and prevents scattered effort. Externally, the plan demonstrates to lenders, investors, and partners that your business operates with structure and discipline. According to research cited by Forbes, 71% of successful small businesses have a documented business plan. Strategic planning turns that documentation into a living framework that evolves as the business grows.

What Is the Difference Between a Business Plan and a Strategic Plan?

The difference between a business plan and a strategic plan is that a business plan focuses on how the company operates day to day, while a strategic plan focuses on where the company is going over the long term and how it will get there. A business plan covers operational details: what the company sells, who it serves, how it markets, and how it generates revenue. A strategic plan sits above those details and defines the broader direction, the goals that guide those operations, and the metrics that measure whether the business is on track.

Both documents are valuable, and most growing businesses need both. A business plan answers "what do we do and how do we do it?" A strategic plan answers "where are we going and how will we know we got there?" For companies that are already past the startup phase, the strategic plan often becomes the more important document because the operational systems are already in place. The strategic plan determines whether those systems are pointed in the right direction. Companies that separate the two documents and review each on its own cadence tend to make clearer decisions than those that combine everything into one sprawling file.

According to the U.S. Bureau of Labor Statistics, 49.4% of new businesses fail within five years. Many of those failures trace back to a lack of direction, not a lack of effort. A business formation that starts with a strong structural foundation and a strategic plan is better positioned to survive those critical early years.

What Are the Key Components of a Strategic Business Plan?

The key components of a strategic business plan are a mission and vision statement, a SWOT analysis, goals and objectives, strategies and action plans, a financial plan, key performance indicators, and an executive summary. Each component serves a specific function, and skipping any one of them weakens the overall plan.

The mission statement explains why the company exists and what it does. The vision statement describes where the company is heading. The SWOT analysis evaluates internal strengths and weaknesses alongside external opportunities and threats. Goals and objectives translate the vision into specific, measurable targets. Strategies and action plans describe the steps the company will take to reach those targets. The financial plan projects revenue, expenses, cash flow, and profitability. Key performance indicators track progress. The executive summary condenses everything into a brief overview that stakeholders can review quickly.

Together, these components form a single planning architecture. The mission drives the goals. The goals drive the strategies. The strategies drive the financial projections. The financial projections produce the KPIs. The KPIs tell you whether the plan is working. Business consulting support often helps owners build these components in sequence so nothing gets skipped or built out of order.

How Do You Write a Strategic Business Plan Step by Step?

You write a strategic business plan step by step by defining your mission and vision, conducting a SWOT analysis, setting SMART goals, developing strategies and action plans, building the financial plan, identifying KPIs, and writing the executive summary last. The sequence matters because each step depends on the output of the step before it. Writing the executive summary first, for example, produces a vague overview that does not reflect real analysis. Writing it last produces a summary grounded in the actual plan.

According to University of Oregon research cited across multiple industry publications, entrepreneurs with business plans are 152% more likely to launch their ventures compared to those without plans. The planning process itself produces clarity, even before the plan is finished. Follow these seven steps to build each section:

- Define your mission and vision statements

- Conduct a SWOT analysis

- Set SMART goals and objectives

- Develop your strategies and action plans

- Build the financial plan

- Identify key performance indicators

- Write the executive summary

Step 1: Define Your Mission and Vision Statements

Your mission statement defines what your company does, who it serves, and why it exists. A strong mission statement is one to three sentences long and specific enough that someone outside the company could read it and understand the business. "We help small business owners reduce tax liability and make better financial decisions" is specific. "We provide world-class solutions" is not.

Your vision statement describes what the company will look like in three to five years. The vision provides a destination the team can work toward. According to research from Upmetrics, only 13% of U.S. employees strongly believe their leaders communicate effectively with the organization, which makes a clear, written vision statement even more important for alignment. The mission and vision together create the foundation every other section of the strategic plan builds on.

Step 2: Conduct a SWOT Analysis

A SWOT analysis evaluates your company's Strengths, Weaknesses, Opportunities, and Threats to give you a clear picture of your current position before you set goals. Strengths and weaknesses are internal factors you control: your team's expertise, your cash reserves, your customer retention rate. Opportunities and threats are external factors you cannot control: market trends, new competitors, regulatory changes. Approximately 80% of businesses use SWOT analysis as a standard part of their strategic planning process, according to industry data compiled by PlanArmory.

The goal of the SWOT is not to produce a long list. Limit each quadrant to three to five critical items ranked by impact. A SWOT with 15 strengths is not strategic; it is unfocused. The output of the SWOT analysis feeds directly into the goal-setting step, because the most valuable goals address the intersection of your strengths and your opportunities while protecting against your most significant threats.

Step 3: Set SMART Goals and Objectives

SMART goals are Specific, Measurable, Achievable, Relevant, and Time-based targets that translate your vision into concrete outcomes. "Grow revenue" is not a SMART goal. "Increase annual revenue from $800,000 to $1 million by December 31, 2027" is a SMART goal because it specifies the target, the metric, the timeline, and the starting point. Every goal in the strategic plan should follow this format.

Break annual goals into quarterly and monthly milestones so the plan produces accountability throughout the year. According to research cited by Statista, 65% of businesses that stick to their plans achieve their strategic objectives. The businesses that fall short typically set goals without milestones, review them once, and then let the plan sit in a drawer until the next annual cycle. Startup advisory work often focuses heavily on this step because early-stage businesses set either too many goals or goals that are not measurable.

Step 4: Develop Your Strategies and Action Plans

Strategies describe the broad approach you will take to reach each goal, and action plans break those strategies into specific tasks with owners, deadlines, and resources. A strategy might be "increase customer acquisition through referral partnerships." The action plan under that strategy might include: identify 10 potential referral partners by March 15, contact each partner by April 1, formalize three agreements by May 1, and launch the referral program by June 1.

The action plan is where most strategic plans fail. Many businesses produce strong goals and then skip the action plan entirely, leaving the team with a destination but no map. According to Upmetrics industry research, 64% of companies that successfully implement initiatives integrate them into their budgets and limit the number of initiatives they pursue. Focus on three to five core strategies per year rather than 15 underfunded initiatives.

Step 5: Build the Financial Plan

The financial plan translates your strategies and goals into projected revenue, expenses, cash flow, and profitability over the planning period. At a minimum, the financial section should include a 12-month cash flow projection, a projected income statement (profit and loss), a projected balance sheet, and a break-even analysis. For businesses seeking financing, lenders and investors scrutinize the financial plan more closely than any other section. According to research cited by Forbes, 75% of investors prioritize financial projections when evaluating a business plan.

The financial plan should also include a monthly operating budget that aligns spending with the strategies outlined in Step 4. A strategy to launch a referral program, for example, needs a budget line for partner incentives, marketing materials, and tracking software. If the strategy does not have a budget, it does not have a plan. Accurate financial statements from prior periods form the baseline for all projections, which is why clean books and up-to-date records are a prerequisite, not an afterthought.

Step 6: Identify Key Performance Indicators

Key performance indicators (KPIs) are the specific metrics you will track to measure whether your strategies are producing the expected results. Each goal should have at least one primary KPI and one or two secondary KPIs. A revenue growth goal might use monthly recurring revenue as the primary KPI and customer acquisition cost as a secondary KPI. A profitability goal might track gross margin as the primary KPI and operating expense ratio as the secondary.

KPIs produce the data that makes quarterly plan reviews productive. Without KPIs, review meetings become opinion-driven conversations about what feels like it is working. With KPIs, the conversation shifts to what the data shows is actually working. Tracking the right financial metrics turns the strategic plan from a static document into an active management tool.

Step 7: Write the Executive Summary

The executive summary is a one-to-two-page overview of the entire strategic plan, and it should be written last because it summarizes everything the other sections contain. The executive summary includes the company's mission, its primary goals, the top strategies, key financial projections, and the expected outcomes. For plans shared with lenders or investors, the executive summary is often the only section that gets read in full, which makes its clarity and accuracy critical.

Keep the executive summary concise. A strong executive summary states the company's direction, the financial targets, and the timeline in clear, specific language. According to Harvard Business Review-cited research, companies with business plans are 2.5 times more likely to secure loans than those without. The executive summary is the front door of the plan, and a weak front door discourages further reading.

What Is a SWOT Analysis and How Does It Fit into a Strategic Plan?

A SWOT analysis is a strategic planning framework that evaluates a company's Strengths, Weaknesses, Opportunities, and Threats to inform goal-setting and strategy development. The SWOT analysis fits into the strategic plan between the mission/vision section and the goal-setting section because it provides the situational awareness that makes goals realistic and strategies effective. Setting goals without a SWOT is like planning a route without knowing the starting point.

CategoryTypeDefinitionExampleStrengthsInternalAdvantages your business controlsStrong cash reserves, experienced team, loyal customer baseWeaknessesInternalDisadvantages your business controlsOutdated technology, high employee turnover, thin profit marginsOpportunitiesExternalFavorable conditions in the marketGrowing demand in your sector, new tax credits, competitor exitThreatsExternalUnfavorable conditions in the marketRising material costs, new regulations, economic downturn

Sources: SBA Business Guide; Business Development Bank of Canada SWOT framework; Bank of America small business planning resources.

The most effective SWOT analyses focus on the 3-5 most impactful items in each quadrant rather than producing exhaustive lists. According to Bank of America research, owners who complete business plans that include a SWOT analysis are twice as likely to grow their business or obtain capital compared to those who skip the exercise. A virtual CFO or financial advisor can help quantify the SWOT findings by attaching revenue estimates to opportunities and cost projections to threats, which makes the analysis actionable rather than theoretical.

What Should the Financial Section of a Strategic Plan Include?

The financial section of a strategic plan should include a cash flow projection, a projected income statement, a projected balance sheet, a break-even analysis, a monthly operating budget, and capital expenditure estimates. Each of these documents serves a different purpose, and together they give you a complete picture of where the business stands financially and where it is heading.

The financial section should include the following components:

- A 12-month cash flow projection showing when money comes in and when it goes out, month by month

- A projected income statement (profit and loss) covering the full planning period, typically one to three years

- A projected balance sheet showing expected assets, liabilities, and equity at the end of each year

- A break-even analysis identifying the revenue threshold at which the business covers all fixed and variable costs

- A monthly operating budget that ties spending directly to the strategies and action plans in the plan

- Capital expenditure estimates for any major purchases, technology investments, or facility upgrades planned during the period

According to a U.S. Bank study, 82% of small businesses that fail do so because of poor cash flow management. The cash flow projection is the single most important financial document in the plan because it reveals timing gaps between income and expenses before they become emergencies. Many small business owners skip this step because they assume profitability equals solvency. Profitability measures whether revenue exceeds expenses over time. Solvency measures whether you have enough cash on hand to pay this month's bills. A company can be profitable and still run out of cash. Owners dealing with recurring cash flow problems often discover that the root cause was a missing projection, not a missing customer.

What Are Common Mistakes in Strategic Business Planning?

The most common mistakes in strategic business planning are setting too many goals, overestimating revenue projections, ignoring cash flow in the financial plan, writing the plan once and never reviewing it, and planning in isolation without input from advisors or team members. Each of these mistakes reduces the plan's effectiveness and increases the risk that the business drifts off course.

Setting too many goals is the most frequent pitfall. A strategic plan with 15 goals spreads resources too thin and creates confusion about priorities. The most effective plans focus on three to five core goals per year with clear milestones. Overestimating revenue is the second most common mistake. Projections should be based on historical data, market research, and realistic assumptions, not on best-case scenarios. According to the 2026 Federal Reserve Small Business Credit Survey, 60% of small businesses applied for financing in the prior 12 months, and lenders scrutinize projections that appear inflated or unsupported by data.

Planning in isolation is a subtler problem. The owner writes the plan alone, shares it with no one, and then wonders why the team is not aligned. Strategic plans produce better results when key team members contribute to the SWOT analysis, the goal-setting, and the action planning. For businesses across South Florida and nationwide, bringing in outside advisory support, whether a CPA, a structured planning consultant, or a fractional CFO, introduces objectivity and financial rigor that internal teams often lack.

How Often Should a Small Business Update Its Strategic Plan?

A small business should update its strategic plan at least once per year, with quarterly reviews to track progress against KPIs and make adjustments as conditions change. The annual update involves revisiting the SWOT analysis, reassessing goals, and revising financial projections based on actual performance. Quarterly reviews are shorter check-ins that compare KPI data to the plan's milestones and determine whether strategies need adjustment.

According to Upmetrics industry research, 70% of business leaders dedicate approximately one day each month to reviewing business strategy. That level of review produces better outcomes than annual-only reviews because it catches problems early and allows course corrections before small issues become large ones. Trigger-based updates are also important. Major events, including a significant revenue change, a new competitor, a regulatory shift, or a major hire, should prompt a plan review regardless of the scheduled cadence.

The strategic plan is not a one-time document. It is a management tool that produces value only when it is used, reviewed, and updated. According to Statista-cited research, 65% of businesses that consistently follow their plans achieve their strategic objectives. The businesses that treat the plan as a living document outperform those that file it away after creation.

How Does a CPA Help with Strategic Business Planning?

A CPA helps with strategic business planning by building accurate financial projections, stress-testing assumptions, identifying tax-efficient structures, and providing the objective financial analysis that separates a strong plan from a wishful one. Many of the plan's most critical components, including the cash flow projection, the income statement, the break-even analysis, and the budget, require accounting expertise to build accurately.

Beyond the numbers, a CPA or Enrolled Agent brings tax planning into the strategic planning process. Entity structure decisions (S-corp vs. C-corp vs. LLC), retirement plan design, estimated tax obligations, and deduction strategies all affect the financial projections in the plan. A strategic plan that ignores tax implications produces projections that overstate after-tax income and understate the true cost of growth.

Owners interested in year-round tax strategies that align with their strategic plan can explore additional tax-saving strategies to capture savings before year-end. The earlier tax planning enters the strategic planning process, the more accurately the financial projections reflect the business's real after-tax position.

Working with a financial professional also introduces accountability. A CPA who reviews the plan quarterly can flag variances, identify emerging risks, and recommend adjustments before small problems become expensive ones. According to research cited by Harvard Business Review, companies with business plans are 2.5 times more likely to secure loans. A CPA-prepared financial section carries more credibility with lenders than a self-prepared projection, which is why the advisory relationship often pays for itself during the first funding application.

Frequently Asked Questions

Why Do Small Businesses Need a Strategic Plan?

Small businesses need a strategic plan because it creates a clear direction for growth, aligns the team around shared goals, and provides a framework for making financial and operational decisions. According to SBA-cited data, businesses with formal plans grow 30% faster than those without. A strategic plan also improves the chances of securing financing, because lenders and investors require documented projections and goals before approving funding.

How Long Should a Strategic Business Plan Be?

A strategic business plan should be 15 to 30 pages for most small businesses, depending on the complexity of the operation and the intended audience. Plans submitted to lenders or investors typically need more detail in the financial projections section. Internal-only plans can be shorter and more focused. The goal is completeness without filler: every page should contain information that drives a decision or measures a result.

Can You Use a Strategic Plan to Secure a Business Loan?

Yes, you can use a strategic plan to secure a business loan. Lenders evaluate the financial projections, market analysis, and management strategy sections of the plan to determine whether the business can generate enough revenue to repay the loan. According to Harvard Business Review research, companies with business plans are 2.5 times more likely to secure loans. A plan prepared with professional strategic business planning support typically carries more credibility with lenders than a self-prepared document.

What Are the 7 Elements of a Strategic Plan?

The 7 elements of a strategic plan are a mission statement, a vision statement, a SWOT analysis, goals and objectives, strategies and action plans, a financial plan, and key performance indicators. Some frameworks add an executive summary as an eighth element. Each element builds on the previous one to create a cohesive planning document that guides long-term business decisions.

What Are the 5 Key Components of a Strategic Plan?

The 5 key components of a strategic plan are a mission/vision statement, a situational analysis (typically a SWOT), strategic goals, action plans with timelines, and a financial plan with projections. These five components cover the minimum requirements for a functional strategic plan. More detailed plans expand each component with KPIs, market research, and an executive summary.

How Do You Measure the Success of a Strategic Plan?

You measure the success of a strategic plan by tracking the key performance indicators (KPIs) defined in the plan against the goals and milestones you set. Quarterly reviews compare actual performance to projected performance across revenue, profitability, cash flow, customer acquisition, and other metrics specific to your business. According to Statista-cited research, 65% of businesses that consistently follow and measure their plans achieve their strategic objectives.

The Takeaway

A strategic business plan gives your company a clear direction, a financial roadmap, and a measurement system that keeps every decision aligned with your long-term goals. The data supports this consistently: businesses with documented plans grow faster, secure financing more often, and achieve their objectives at significantly higher rates than businesses that operate without one. The process itself, from defining your mission through building financial projections and setting KPIs, produces clarity that pays dividends long before the plan is finished. According to the OnDeck/Ocrolus Small Business Report, 94% of small business owners project growth in 2026. The businesses most likely to capture that growth are the ones with a plan that tells them exactly how to get there.

If you are ready to build or update a strategic business plan with the financial rigor and tax-aware projections that lenders, investors, and your own team will trust, we would welcome the conversation. At NR CPAs & Business Advisors, we help small business owners create structured plans grounded in accurate financial data and real growth strategy.

Reach out to our team at (954) 231-6613 to get started.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

IRS Currently Not Collectible (CNC) Status: How It Works

Currently Not Collectible (CNC) is an IRS designation that temporarily pauses all collection activity on your account when you cannot afford to pay anything toward your tax debt without failing to cover basic living expenses. According to the IRS, CNC status means the agency has determined that requiring any payment would cause you financial hardship. While your account is in CNC, the IRS will not levy your wages, seize your bank accounts, or garnish your income.

CNC status does not eliminate your tax debt. According to the IRS, you still owe the full balance, and penalties and interest continue to accrue while your account is in this status. The IRS may also file a Notice of Federal Tax Lien to protect the government's interest in your property, and it will apply any future federal tax refunds to your outstanding balance. CNC is a temporary measure, not a permanent resolution, but it can provide critical breathing room for taxpayers in severe financial hardship.

Who Qualifies For CNC Status

You may qualify for CNC status if your monthly income, after allowable living expenses, leaves you unable to make even a small payment toward your tax debt. According to the IRS, the agency uses national and local cost-of-living standards to evaluate your expenses, including housing, utilities, food, transportation, health insurance, and out-of-pocket medical costs. If your allowable expenses equal or exceed your income, and you have no significant assets the IRS could use to satisfy the debt, CNC status is typically approved.

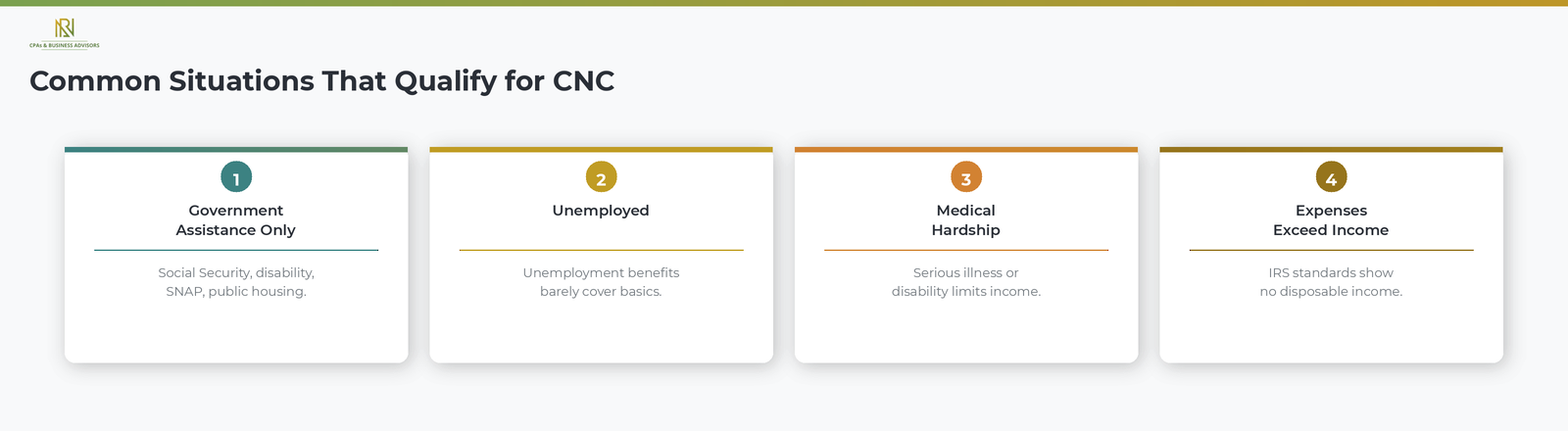

Common situations that support CNC eligibility include the following.

- Your only income is from government assistance. Social Security, disability benefits, unemployment compensation, or public assistance programs.

- You are unemployed with no other income. Especially when unemployment benefits barely cover basic expenses.

- You have a serious medical condition or disability. Particularly conditions that permanently limit your earning capacity.

- Your expenses exceed your income. Even after the IRS applies its own expense standards, there is no disposable income available for tax payments.

How To Request Currently Not Collectible Status

To request CNC status, call the IRS at 800-829-1040 or the phone number on your most recent notice and explain that you cannot afford to make any payments toward your tax debt. According to the IRS, the agent will ask you to provide financial information to verify your hardship. In most cases, you will need to complete Form 433-F, Collection Information Statement, which is a two-page form that documents your income, monthly expenses, debts, and assets.

For more complex financial situations, the IRS may require Form 433-A (for wage earners and self-employed individuals) or Form 433-B (for businesses). According to the IRS, you should be prepared to provide supporting documentation including pay stubs, bank statements, utility bills, rent or mortgage statements, and medical records if applicable. The IRS compares your reported expenses against its allowable expense standards to determine whether any payment is feasible.

When speaking with the IRS, be clear that you cannot afford any monthly payment, not just that you cannot pay the full amount. According to the IRS, if you can afford a small monthly payment, the agency will typically direct you toward an installment agreement or partial payment plan instead of CNC status.

What Happens While Your Account Is In CNC

While your account is in CNC status, the IRS suspends most active collection efforts but retains the right to take certain actions that protect the government's interest. According to the IRS, the following applies during CNC.

- No levies or garnishments. The IRS will not levy your wages, bank accounts, or other property.

- Tax refunds are still taken. The IRS will intercept and apply any federal tax refund you receive to the outstanding balance.

- A federal tax lien may be filed. According to the IRS, if you owe more than $10,000, the agency will generally file a Notice of Federal Tax Lien, which is a public record that can affect your credit and your ability to sell or refinance property.

- Penalties and interest continue. The balance grows while you are in CNC because the IRS does not stop charging penalties or interest during this period.

- Periodic reviews. The IRS may review your financial situation later and resume collection if your income improves.

When The IRS Can Remove CNC Status

The IRS can remove your account from CNC status and resume collection activity if your financial situation improves. According to the IRS, the agency assigns a closing code to each CNC account that corresponds to an income threshold. If your reported income exceeds that threshold, as indicated by W-2s, 1099s, or tax returns filed in subsequent years, the IRS may contact you to reassess your ability to pay.

If the IRS determines you can now afford payments, it will typically offer you the option to set up an installment agreement or pursue another resolution. If your income remains below the threshold indefinitely, your CNC status continues until the 10-year Collection Statute Expiration Date (CSED) expires, at which point the remaining debt is written off permanently.

How CNC Interacts With The 10 Year Collection Statute

One of the most important features of CNC status is that it does not pause or extend the IRS's 10-year collection clock. According to the IRS, the CSED continues to run while your account is in CNC. This means that if your income does not improve before the statute expires, the IRS loses its legal authority to collect the debt, and the balance is permanently written off.

This is a key distinction from other resolution options. Requesting an Offer in Compromise or an installment agreement suspends the CSED while the IRS evaluates your application, effectively giving the agency more time to collect. CNC status does not. For taxpayers with older tax debts and limited income prospects, CNC can be strategically advantageous because the clock keeps running in your favor.

However, CNC is not always the best long-term strategy. If your income is likely to improve, the IRS will remove you from CNC and resume collection, potentially with a larger balance due to accumulated penalties and interest. Taxpayers weighing CNC against other options like payment plans, Offers in Compromise, or penalty relief can compare all available paths in the IRS tax debt resolution overview.

Frequently Asked Questions About CNC Status

Does CNC Status Forgive My Tax Debt?

No, CNC status does not forgive or cancel your tax debt. According to the IRS, you still owe the full balance, and penalties and interest continue to accrue. The debt is only eliminated if the 10-year CSED expires while your account remains in CNC.

Will The IRS Take My Tax Refund While I Am In CNC?

Yes, the IRS will intercept and apply your federal tax refund to the outstanding balance even while your account is in CNC status. According to the IRS, refund offsets are one of the collection actions the agency continues during CNC.

How Long Can I Stay In CNC Status?

There is no fixed time limit on CNC status. According to the IRS, your account remains in CNC as long as your financial situation does not improve beyond the threshold the agency sets. The IRS may review your finances periodically, but CNC can last for years if your income remains at hardship levels.

IRS Penalty Abatement: How To Remove IRS Penalties

IRS penalty abatement is the removal or reduction of penalties the IRS has assessed against you for failing to file a return, failing to pay taxes owed, or failing to make required tax deposits on time. According to the IRS, abating a penalty does not eliminate the underlying tax you owe, but it removes the additional charges the IRS added on top of that balance. Because penalties often represent a significant portion of a taxpayer's total debt, a successful abatement can substantially reduce the amount you need to pay.

According to the IRS, when penalties are removed, the interest charged on those penalties is also automatically eliminated. However, interest on the unpaid tax itself continues to accrue until the balance is paid in full. Penalty abatement is available for individual taxpayers, businesses, and employers, though the eligibility criteria and process differ depending on the type of penalty and the relief program you qualify for.

Types Of IRS Penalty Relief

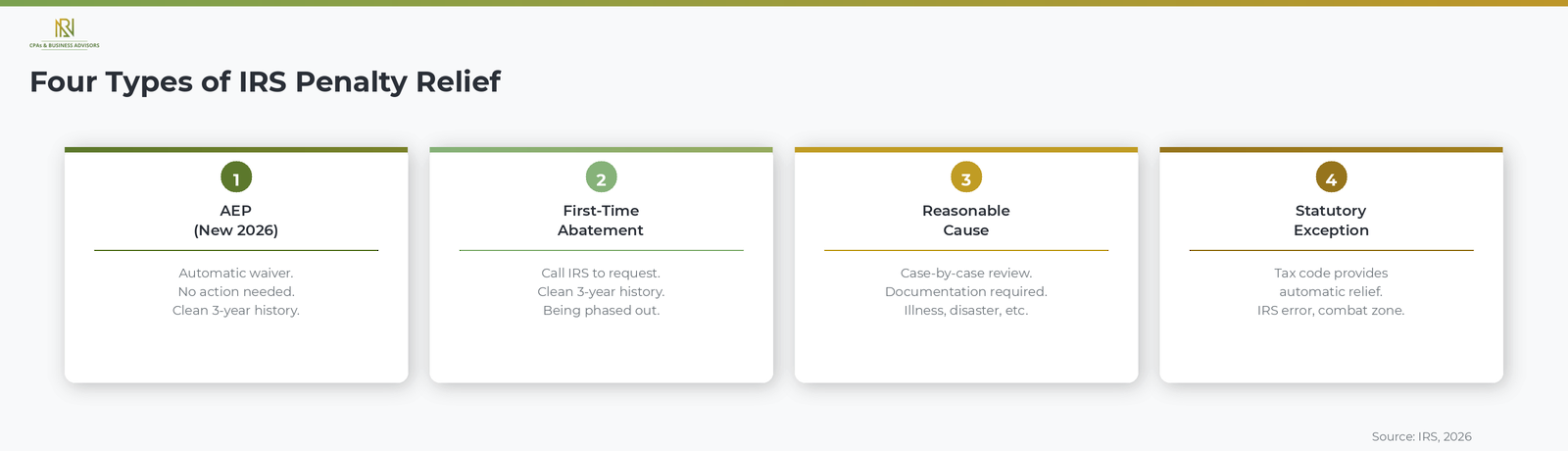

The IRS offers four main types of penalty relief: the Automatic Exemption from Penalty program, first-time penalty abatement, reasonable cause relief, and statutory exceptions. Each program has its own eligibility requirements and applies to different situations.

Automatic Exemption From Penalty Program

Starting in 2026, the IRS is phasing in the Automatic Exemption from Penalty (AEP) program, which automatically waives failure-to-file, failure-to-pay, and failure-to-deposit penalties for qualifying taxpayers without requiring any action on your part. According to the IRS, you qualify for AEP relief if you filed the same type of return on time for each of the previous three years and had no penalties assessed (other than estimated tax penalties) or any prior penalties were waived for reasonable cause. Unlike other programs, you do not need to call the IRS or submit paperwork. The IRS simply does not assess the penalty, and sends you a letter confirming the relief was applied.

According to the IRS, the AEP program applies to individual 1040 returns filed for tax year 2025 and later, and to certain quarterly business returns for tax year 2026 and later. The AEP program will fully replace the First-Time Penalty Abatement program for penalties related to returns originally due on or after January 1, 2027.

First-Time Penalty Abatement

First-Time Penalty Abatement (FTA) is an administrative waiver that removes failure-to-file, failure-to-pay, or failure-to-deposit penalties for taxpayers with a clean compliance history over the prior three years. According to the IRS, you qualify if you filed all required returns (or filed valid extensions), had no penalties assessed for the three preceding tax years, and have paid or arranged to pay any tax due. Unlike the AEP program, FTA is not automatic. You must contact the IRS by phone or submit Form 843, Claim for Refund and Request for Abatement, to request it.

According to the IRS, the FTA program is being phased out as the AEP program rolls in. FTA will be fully replaced for penalties associated with returns originally due on or after January 1, 2027. For penalties on returns due before that date, FTA remains available.

Reasonable Cause Relief

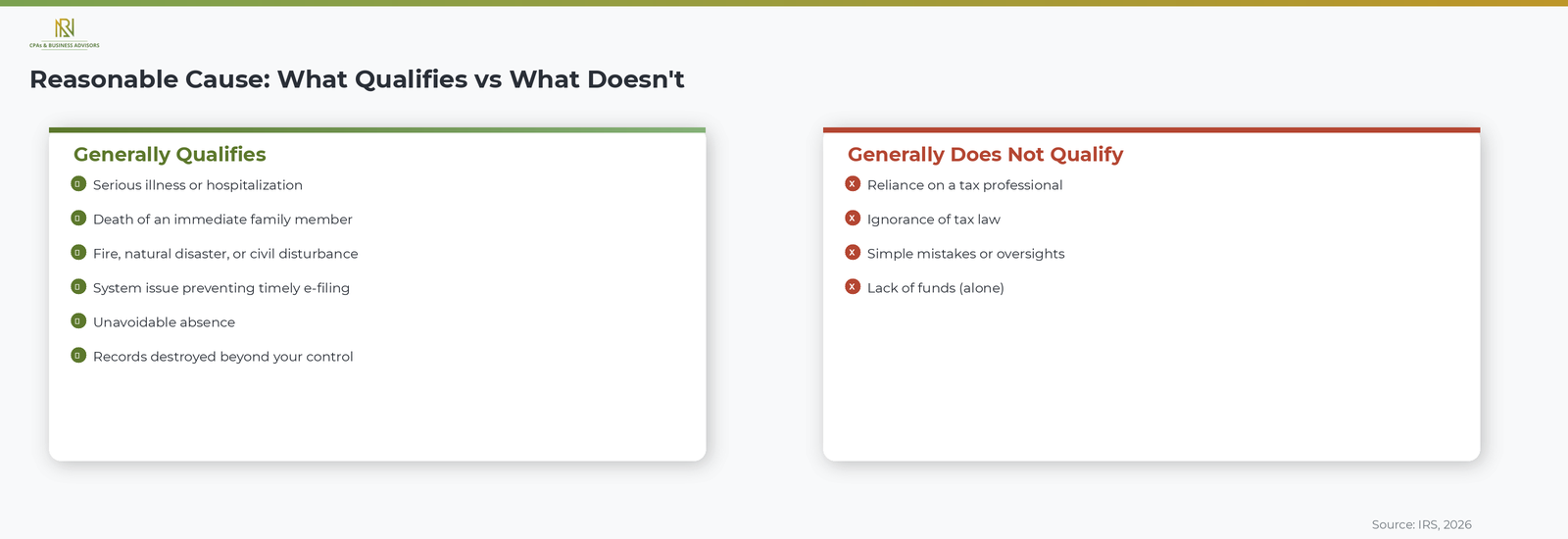

If you do not qualify for AEP or first-time abatement, the IRS can still remove penalties if you demonstrate that your failure to comply was due to reasonable cause and good faith. According to the IRS, reasonable cause is evaluated on a case-by-case basis considering all the facts and circumstances. Valid reasons include serious illness or death of an immediate family member, fires or natural disasters that destroyed records, system issues that prevented timely electronic filing or payment, and unavoidable absences.

According to the IRS, the following reasons generally do not qualify as reasonable cause on their own: reliance on a tax professional, ignorance of the law, simple mistakes or oversights, and lack of funds. However, lack of funds combined with other circumstances showing good-faith effort to comply may support a reasonable cause claim. You must provide supporting documentation such as medical records, court records, or correspondence that demonstrates the circumstances that prevented you from meeting your obligations.

Statutory Exceptions

In certain situations, the tax code itself provides an automatic exception that eliminates a penalty. According to the IRS, statutory exceptions include receiving incorrect written advice from the IRS that you reasonably relied on, being able to prove that your return or payment was mailed or e-filed before the deadline, being impacted by a federally declared disaster, and serving in a military combat zone.

Which Penalties Can Be Removed

The most common penalties eligible for abatement are the failure-to-file penalty, the failure-to-pay penalty, and the failure-to-deposit penalty. The failure-to-file penalty is 5 percent of the unpaid tax per month up to 25 percent. The failure-to-pay penalty is 0.5 percent per month up to 25 percent. Both penalties can be removed through AEP, FTA, or reasonable cause relief.

Accuracy-related penalties, which the IRS assesses when you underpay taxes due to negligence or a substantial understatement of income, can be removed through reasonable cause relief but are not eligible for AEP or first-time abatement. According to the IRS, the estimated tax penalty (for individuals who do not make sufficient quarterly payments) generally cannot be removed through any of the standard relief programs.

How To Request Penalty Abatement

The process for requesting penalty abatement depends on the type of relief you are seeking.

- AEP: No action required. The IRS applies the waiver automatically and sends you a confirmation letter.

- First-time abatement: Call the toll-free number on your IRS notice and request the abatement over the phone. If approved, the IRS sends a confirmation letter within 30 days.

- Reasonable cause: Call the IRS or submit Form 843 with a written explanation of your circumstances and supporting documentation. According to the IRS, phone requests are sometimes granted immediately, but complex cases may require a written submission.

- Statutory exception: Follow the instructions on your IRS notice or submit Form 843 with evidence of the exception (such as proof of timely mailing or a FEMA disaster declaration).

If you owe a balance beyond the penalties and cannot pay in full, you can set up an installment agreement to pay the remaining tax over time while your penalty abatement request is processed.

What To Do If Your Request Is Denied

If the IRS denies your penalty abatement request, you have 30 days from the date on the denial letter to appeal the decision to the IRS Independent Office of Appeals. According to the IRS, you must submit a written letter stating that you are appealing, include a copy of the denial notice, and provide any additional documentation or explanation you want the Appeals office to consider. Appeals officers review your case independently from the unit that issued the original denial.

If Appeals also denies your request, you can take the matter to court. According to the IRS, you can file a petition with the U.S. Tax Court before paying the disputed amount, or pay the penalty and file for a refund through the U.S. District Court or the U.S. Court of Federal Claims. Taxpayers who need to explore other ways to reduce their total IRS debt beyond penalty abatement, including Offers in Compromise and hardship status, can review the full range of IRS resolution options.

Frequently Asked Questions About Penalty Abatement

How Long Does It Take To Get Penalty Abatement?

It depends on the type of relief and how you request it. According to the IRS, first-time abatement requests made by phone can be approved immediately during the call. Written requests for reasonable cause relief may take several weeks to several months. The AEP program requires no wait time because the penalty is never assessed in the first place.

Can I Get Penalties Removed For Multiple Years?

First-time abatement and AEP apply to one tax period at a time. According to the IRS, you must have a clean three-year compliance history for each period you are requesting relief for. Reasonable cause relief can apply to multiple years if the same qualifying circumstance affected your ability to comply across those years, but you must demonstrate reasonable cause separately for each period.

Does Penalty Abatement Remove Interest Too?

Penalty abatement automatically removes the interest that was charged on the abated penalties, but it does not remove interest on the underlying tax. According to the IRS, interest on unpaid tax continues to accrue until the balance is paid in full, regardless of whether penalties are removed.