%201.avif)

.png)

.png)

Business Consulting Services for Small Business

Business consulting services for small business give owners outside expertise to solve specific problems, improve operations, and drive measurable growth. A consultant brings tested frameworks, industry experience, and an objective perspective that owners and employees often cannot provide. For most small businesses, the right consultant pays for the engagement many times over through better decisions, stronger systems, and improved financial results.

In this article, we cover what a small business consultant does, the five main types of consulting, the standard 7 C's and 7 steps of the consulting process, the four principles every good consultant follows, what consulting costs, what a fair hourly rate looks like, which types of consultants are most in demand right now, and how AI is changing the profession.

Business Consulting Services for Small Business

Business consulting services for small business are professional advisory engagements that help owners diagnose problems, design solutions, and execute changes that drive growth and profitability. Consultants work across nearly every functional area, including strategy, finance, marketing, operations, technology, and human resources, and they deliver value through expertise the small business does not have internally.

The consulting industry is large and growing fast. According to Grand View Research, the global management consulting market reached $367 billion in 2024 and is projected to grow at a 7.3% annual rate through 2030. According to a 2025 Federal Reserve Small Business Credit Survey, 57% of small business owners cite difficulty reaching customers and growing sales as their top operational challenge, while 75% report rising costs as their primary financial challenge. Both of those problems are exactly the kind of work consultants help solve.

Small business owners turn to consultants for several specific reasons. They face a problem they have not solved before, they want an outside perspective on a major decision, they need help building systems or processes, or they want to accelerate a specific initiative like fundraising, marketing, or operational change. Our business consulting work centers on financial and operational consulting for growing companies, and we see the same patterns across nearly every client we work with.

What Does a Small Business Consultant Do

A small business consultant analyzes the client's business, identifies the highest-impact opportunities and problems, recommends specific actions, and often helps execute the changes. The consultant brings expertise the client lacks, an objective perspective free from internal politics, and proven frameworks that shorten the time to results.

The work itself varies by specialty. A financial consultant might rebuild the cash flow forecast, fix the chart of accounts, and find tax savings. A marketing consultant might audit the website, redesign the sales funnel, and build a content strategy. An operations consultant might map current processes, eliminate bottlenecks, and implement new software. According to a 2025 Robert Half survey, 62% of finance and operations leaders report ongoing talent shortages, which is one of the biggest reasons small businesses bring in consultants instead of trying to hire full-time experts.

The best consultants do not just deliver a report and leave. They work alongside the owner and team to make the changes stick. This usually involves training internal staff, building systems the business can run on its own, and documenting decisions so the value remains after the engagement ends. Without structured follow-through, even great recommendations sit in a binder and never produce results.

What Are the 5 Types of Consulting

The 5 types of consulting most relevant to small business owners are strategy consulting, financial consulting, marketing consulting, operations consulting, and human resources consulting. Each addresses a different part of the business, and most small businesses need at least two of these at some point during their growth.

Strategy Consulting

Strategy consulting helps owners answer the big questions about where the business is going. This includes market positioning, competitive strategy, growth planning, pricing strategy, and decisions about new products, services, or locations. According to Grand View Research, strategy consulting accounts for a significant share of the global consulting market because every business eventually faces decisions that benefit from outside strategic perspective. For small businesses, this kind of work often gets paired with structured strategic planning to keep the strategy from sitting on a shelf.

Financial and CFO Consulting

Financial consulting covers cash flow management, financial reporting, budgeting and forecasting, financial systems, fundraising support, and CFO-level strategic guidance. According to U.S. Bank research widely cited in small business analysis, 82% of small businesses that fail do so because of poor cash flow management. That single statistic explains why financial consulting is one of the most common engagements for small businesses. Our virtual CFO work falls into this category, providing financial leadership without the cost of a full-time hire.

Marketing Consulting

Marketing consulting helps small businesses grow revenue through better positioning, messaging, brand development, content marketing, paid advertising, SEO, sales funnel design, and customer retention programs. According to the 2025 Federal Reserve Small Business Credit Survey, 57% of owners say reaching customers and growing sales is their top operational challenge, up from 53% in 2023. A skilled marketing consultant addresses the root causes, not just the symptoms, and builds systems that compound over time.

Operations Consulting

Operations consulting focuses on the day-to-day workings of the business. This includes process mapping, eliminating bottlenecks, implementing new software, supply chain optimization, vendor management, and productivity improvement. According to McKinsey research, companies that focus on operational efficiency are 33% more likely to recover financially within six months after a disruption. Small businesses with weak operations often have margins 5 to 10 percentage points lower than industry peers, which is exactly the gap operations consulting can close.

HR and People Consulting

HR consulting helps small businesses with hiring, compensation, performance management, employee handbooks, compliance, and culture building. As small businesses grow past 10 to 15 employees, the people side gets more complex fast. According to a 2025 Robert Half hiring report, the fully loaded cost of a new hire runs 1.25 to 1.4 times base salary once benefits, taxes, and equipment are factored in. Getting hiring right at this stage matters more than almost any other operational decision.

What Are the 7 C's of Consulting

The 7 C's of consulting are Client, Clarify, Create, Change, Confirm, Continue, and Close. The framework comes from Mick Cope's book The Seven C's of Consulting, which has been used as a standard consulting process model for more than two decades. Each C represents a phase of the engagement, and together they describe how a professional consultant moves from first contact with a client to successful project completion.

Client is the first phase, focused on understanding who the client is, what they need, and what success will look like. Clarify deepens the understanding through analysis and data gathering, defining the real problem rather than just the surface symptom. Create is the solution design phase, where the consultant builds the plan, framework, or system that will address the diagnosed problem. Change is the implementation phase, where the work actually happens, often with active consultant involvement to keep things on track.

Confirm is the validation phase, where the consultant measures whether the change produced the intended result. Continue is about sustaining the change after the active engagement ends, often through training, documentation, and ongoing support. Close is the formal end of the engagement, including final reporting, knowledge transfer, and setting up the relationship for future work. According to Cope's research with 15 years of consulting experience, projects that follow all 7 phases produce significantly better results than projects that skip steps in the middle.

What Are the 7 Steps of the Consulting Process

The 7 steps of the consulting process are entry, diagnosis, planning, implementation, evaluation, knowledge transfer, and closure. This sequence is the standard consulting engagement model used by professional services firms and is closely related to the 7 C's framework.

Entry is the initial conversation and proposal phase. The consultant and the client get to know each other, the consultant scopes the project, and both sides agree on objectives, deliverables, timeline, and fees. Diagnosis is the deep analysis phase. The consultant gathers data, interviews team members, reviews systems and processes, and develops a clear picture of the current state. According to industry data, this phase typically takes 2 to 4 weeks for a mid-size consulting engagement, and it is where most of the eventual value gets created.

Planning is the solution design phase, where the consultant builds the action plan based on the diagnosis. Implementation is where the plan gets executed, often with consultant involvement to manage change and remove obstacles. Evaluation measures whether the changes produced the expected results. Knowledge transfer makes sure the client team can sustain the changes after the consultant leaves. Closure formalizes the end of the engagement and often sets up future work. Each step builds on the previous one, and skipping any of them usually undermines the final result.

What Are the 4 Principles of Consulting

The 4 principles of consulting are independence, confidentiality, objectivity, and competence. These principles form the ethical foundation of professional consulting and are reflected in the codes of conduct used by major industry bodies like the Institute of Management Consultants USA.

Independence means the consultant is free from conflicts of interest that would compromise the advice given. They are not selling a product the client must buy and they are not financially tied to the outcome in a way that biases the recommendation. Confidentiality means everything the consultant learns about the client business stays private, including financial information, strategic plans, and internal challenges. Objectivity means the consultant gives advice based on data and analysis, not on what the client wants to hear. Competence means the consultant has the actual expertise to do the work and is honest about the limits of that expertise.

These principles matter because consulting relationships involve a lot of trust. A small business owner is letting an outsider see the inner workings of the business, including the parts that are not going well. Without strong ethical principles, the consulting relationship breaks down. According to a 2025 survey of small business owners cited in industry research, 64% say trust in the consultant is the single most important factor in choosing who to work with, ranking above price, brand, or specific expertise.

How Much Does Consulting Cost for a Small Business

Consulting costs for a small business typically range from $100 to $400 per hour for hourly engagements, or $3,000 to $25,000 per month for ongoing retainers, depending on the scope of work and the experience of the consultant. Project-based fees usually run between $5,000 and $75,000 for a defined engagement, with complex projects sometimes reaching six figures.

According to a 2025 consulting industry pricing analysis, small business consulting rates break down by experience level. Junior consultants and generalists charge $75 to $150 per hour. Experienced specialists charge $150 to $300 per hour. Senior consultants with deep industry expertise charge $300 to $600 per hour. Boutique firms with proven track records often bill at the higher end of these ranges, while individual practitioners are usually less expensive.

The cost should be evaluated against the return, not in isolation. A $15,000 consulting engagement that produces $100,000 in annual margin improvement pays for itself in less than 8 weeks. Proactive tax planning is one of the most common areas where small business consulting more than pays for itself through measurable savings every year. According to research from consulting industry sources, well-scoped small business consulting engagements typically generate a 3 to 10 times return on investment within the first year. For owners weighing the cost, the better question is not whether to spend the money, but whether the proposed work will produce returns large enough to justify the investment.

What Is a Fair Consulting Fee

A fair consulting fee for small business work usually falls between $125 and $350 per hour, or $5,000 to $15,000 per month on retainer, based on industry benchmarks for experienced specialists working with companies in the $1 million to $50 million revenue range. According to 2025 industry pricing surveys, this range covers roughly 70% of all small business consulting engagements.

What makes a fee fair depends on three factors. First, the experience and track record of the consultant. A consultant with 20 years of relevant experience and a portfolio of successful engagements commands more than someone newer to the field. Second, the complexity and stakes of the work. A consulting project that could affect $500,000 of annual revenue is worth paying more for than one that could improve a single process by 5%. Third, the form of engagement. Hourly work is usually cheaper per hour but less predictable in total cost. Retainer work creates more predictable fees but requires a longer commitment.

The fairest fee structure for both sides usually combines a defined scope with clear deliverables and a fixed price for that scope. This protects the client from runaway hourly billing and gives the consultant predictable revenue. Hourly work makes sense for advisory engagements with uncertain scope, and retainer work makes sense for ongoing relationships where the client wants continuous access to the consultant.

Is $100 an Hour Good for Consulting

$100 an hour is on the lower end of professional consulting rates but can be reasonable for junior consultants, narrowly specialized work, or generalists serving very small businesses. According to 2025 consulting industry pricing data, $100 per hour roughly translates to $200,000 per year in annual revenue at 2,000 billable hours, which is in the entry-level range for most consulting firms.

For experienced specialists, $100 per hour is usually below market. Senior strategy, financial, or operations consultants typically charge $200 to $500 per hour, reflecting both deeper experience and the higher value of their advice. For small business owners trying to evaluate whether $100 per hour is good, the answer depends on the consultant's experience level, the type of work, and the value the engagement will deliver.

The hourly rate alone is not the most important number to focus on. A consultant charging $100 per hour who takes 40 hours to solve a problem costs $4,000. A consultant charging $300 per hour who solves the same problem in 8 hours costs $2,400. The second consultant is actually less expensive and probably better, even though the hourly rate sounds higher. For most small businesses, experience and results-per-hour matter more than the headline rate.

What Types of Consultants Are in Demand

The types of consultants in highest demand in 2025 are AI and digital transformation consultants, cybersecurity consultants, financial and CFO consultants, sustainability consultants, and HR and talent consultants. According to Grand View Research and other industry analyses, these five areas are growing fastest because they address the most pressing concerns facing small and mid-size businesses today.

AI and digital transformation consulting has exploded in the last two years. According to a 2025 Gartner CFO survey, AI adoption in business operations has nearly doubled in two years, and 76% of finance leaders have already deployed AI in at least one part of their operation. Small businesses turn to consultants for help choosing the right tools, integrating them with existing systems, and training employees to use them effectively. Cybersecurity consulting is growing for similar reasons, as small businesses become targets for ransomware and data breaches more often than ever.

Financial and CFO consulting remains in steady demand because cash flow problems and tax complexity continue to challenge most growing businesses. According to Business Research Insights, the global virtual CFO market is projected to grow from $3.91 billion in 2024 to $8.17 billion by 2032 at a 9.6% annual rate. Sustainability consulting and HR consulting round out the top five, both driven by regulatory and workforce pressures that small businesses cannot ignore. Strong consulting services across these areas often produce the biggest immediate impact for growing companies.

Will AI Replace Consultants

AI will not replace consultants, but it is changing the profession quickly. AI tools are automating data analysis, drafting reports, summarizing research, and generating frameworks faster than human consultants ever could. What AI cannot do is exercise judgment, manage relationships, understand context, and navigate the political and emotional dynamics of a business. Those remain firmly human skills.

According to a 2025 Gartner finance survey, 76% of finance leaders have deployed AI in at least one part of their operation, but only 12% report that AI has replaced any specific human role. According to McKinsey research, the consultants and finance professionals who use AI tools effectively are 25 to 40% more productive than peers who do not. The shift is from doing the work to directing the work. AI handles the heavy data lifting, and the consultant focuses on diagnosis, strategy, and execution.

For small business owners, the practical implication is that consulting is becoming more affordable and more valuable at the same time. AI lets consultants deliver more in fewer hours, which can lower total project costs. At the same time, the strategic judgment a consultant provides matters even more in a world where data and reports are easy to generate. Our cash flow work for clients uses AI-powered forecasting tools, but the recommendations and strategy come from experienced humans who know what the numbers actually mean.

Types of Small Business Consulting Engagements Compared

Small business consulting engagements come in several common formats, each suited to different needs and budgets. The table below compares the most common engagement types, what they cost, and when each one makes sense.

Engagement TypeTypical CostTime CommitmentBest ForOne-Time Project$5,000 to $50,0002 to 12 weeksSpecific problem with clear scopeMonthly Retainer$3,000 to $15,000 / monthOngoing, 6+ monthsContinuous advisory needsHourly Advisory$125 to $400 / hourAs neededUnpredictable or short questionsFractional Executive$5,000 to $15,000 / monthOngoing, often 1+ yearNeed for senior leadership role

Sources: 2025 consulting industry pricing surveys, Eagle Rock CFO 2025 pricing survey, K38 Consulting fractional pricing guide, Grand View Research consulting market analysis.

When to Hire a Business Consultant for Your Small Business

You should hire a business consultant when you face a problem you cannot solve internally, a decision that is too big to make without outside perspective, or an opportunity that requires expertise your team does not have. The clearer the trigger, the more value a consultant typically delivers.

Common triggers include planning a major change like opening a new location, entering a new market, or launching a new product. Persistent problems that have not responded to internal efforts, like declining margins, customer churn, or hiring failures. Upcoming financial decisions like applying for a loan, raising capital, or preparing the business for sale. Compliance or risk issues that require specialized knowledge, like new tax laws, employment regulations, or industry standards. According to a 2025 industry consulting report, growing businesses that work with experienced consultants during these triggers reach their goals 40 to 60% faster than those that try to handle the work internally.

We see this pattern often with growing businesses in Miami and across the country. The owner has scaled the business to a point where the next step is bigger than what the existing team can handle alone. Bringing in the right outside expertise at that moment, whether through ongoing small business consulting or a defined project engagement, often accelerates the result by months and protects the owner from expensive mistakes along the way.

What Small Business Consulting Typically Delivers

What small business consulting typically delivers is a measurable improvement in financial performance, operational efficiency, or strategic positioning, often within the first 6 to 12 months of the engagement. The exact deliverables depend on the scope, but most engagements produce both tangible outputs and lasting capability for the client team.

Tangible outputs include things like a written strategic plan, a rebuilt financial model, a documented sales process, an implemented software system, a hiring plan, clean financial statements that owners can actually use, or a tax strategy that produces measurable savings. According to industry research, well-executed consulting engagements typically produce 3 to 10 times return on the fees paid within the first year, with the return showing up in higher revenue, lower costs, better cash flow, or some combination of all three.

Lasting capability is the harder-to-measure but often more valuable outcome. A good consultant does not just solve the immediate problem. They train the team, document the systems, and leave the business better positioned to handle similar challenges in the future. According to research from professional services firms, clients who experience significant lasting capability gains from consulting engagements work with the same firm again at a rate 4 to 5 times higher than clients who only received short-term solutions. This long-term relationship is also where ongoing advisory work tends to multiply value over time.

How to Choose the Right Small Business Consultant

How to choose the right small business consultant comes down to expertise fit, references, communication style, fee structure, and chemistry. The wrong consultant can waste months and a meaningful chunk of capital. The right consultant can transform the business.

Expertise fit means the consultant has done this exact kind of work before, ideally for businesses similar to yours. A marketing consultant who has worked with restaurants is more valuable for a restaurant client than one who has worked only with SaaS companies. References matter because consulting is hard to evaluate based on a proposal alone. Talking to two or three former clients gives a much clearer picture of what working with the consultant is actually like.

Communication style is often underestimated. Some consultants are very directive and tell you what to do. Others are collaborative and work alongside the team. Both approaches can work, but the style needs to match the owner's preference. Fee structure should be clear, predictable, and tied to deliverables when possible. Chemistry comes last but matters because consulting engagements involve a lot of communication and trust. If the first few conversations feel uncomfortable, the engagement will probably be uncomfortable too. Solid startup advisory work also depends heavily on this kind of cultural fit between consultant and founder.

Frequently Asked Questions

What Are the 4 C's in Consulting

The 4 C's in consulting are typically Client, Communication, Clarity, and Commitment. Some practitioners use a different version including Capability, Capacity, Communication, and Commitment. Either set of 4 C's emphasizes the relational and execution side of consulting, focusing on understanding the client, communicating clearly, maintaining clarity throughout the project, and committing to results.

What Are the 5 C's of a Consult

The 5 C's of a consult are commonly Client, Context, Content, Conclusion, and Close. This framework outlines the structure of a consulting conversation or engagement. Client means understanding who you are advising. Context means understanding the situation. Content is the substance of the recommendation. Conclusion ties the analysis to a specific recommendation. Close formalizes next steps and commitments.

How Much Is $70,000 a Year Per Hour

$70,000 a year per hour is approximately $33.65 per hour based on a standard 2,080 work-hour year, which is a 40-hour week multiplied by 52 weeks. If you account for two weeks of vacation, the hourly rate works out closer to $35 per hour. This is a useful benchmark when evaluating consulting fees because it shows how much an internal employee actually costs per hour of productive time, before benefits and overhead are added.

Who Are the Big 4 Business Consultants

The Big 4 business consultants in the broader professional services world are Deloitte, PricewaterhouseCoopers (PwC), Ernst & Young (EY), and KPMG, all of which combine accounting, tax, audit, and consulting work. In pure strategy consulting, the MBB firms (McKinsey, Boston Consulting Group, and Bain) are usually considered the top tier. Big 4 firms primarily serve large enterprises, while small businesses typically work with regional CPA firms, boutique consultancies, and fractional executives.

Is a CFO Higher Than a CPA

A CFO is generally higher than a CPA in terms of seniority within a company, though the two roles serve different functions. A CPA, or Certified Public Accountant, is a licensed professional who specializes in accounting, tax, and audit work. A CFO is an executive-level position responsible for the financial direction of a company. Many CFOs hold the CPA license, but not all CPAs are CFOs.

How Long Does a Consulting Engagement Usually Last

A consulting engagement usually lasts between 4 weeks and 12 months, depending on the scope and complexity of the work. Short diagnostic projects often run 4 to 8 weeks. Standard implementation projects run 3 to 6 months. Ongoing advisory or fractional executive engagements often last a year or more, with the client and consultant renewing the relationship periodically based on results.

Should a Small Business Hire a Generalist or a Specialist Consultant

A small business should hire a specialist consultant when the problem is well-defined and a generalist when the problem is broad or unclear. Specialists deliver deeper expertise in their narrow area, while generalists are better at diagnosing what the actual problem is across multiple business functions. Many small businesses start with a generalist for the initial diagnosis and then bring in specialists to execute specific parts of the resulting plan.

The Bottom Line

Business consulting services for small business deliver outside expertise, fresh perspective, and proven frameworks that owners and internal teams often cannot provide on their own. From strategy and finance to marketing, operations, and HR, the right consultant pays for the engagement many times over through better decisions, stronger systems, and measurable improvement in performance. The data is consistent across industries. Small businesses that work with experienced consultants reach their goals faster, avoid expensive mistakes, and build the kind of operational discipline that supports long-term growth.

If you are running a growing business and looking for the kind of financial and strategic consulting that produces real results, we would be glad to help. At NR CPAs & Business Advisors, we work with small businesses and growing companies across the country to bring clarity, structure, and measurable improvement to their finances and operations. Reach out to our team at (954) 231-6613 to start the conversation.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

How To File Unfiled (Back) Tax Returns?

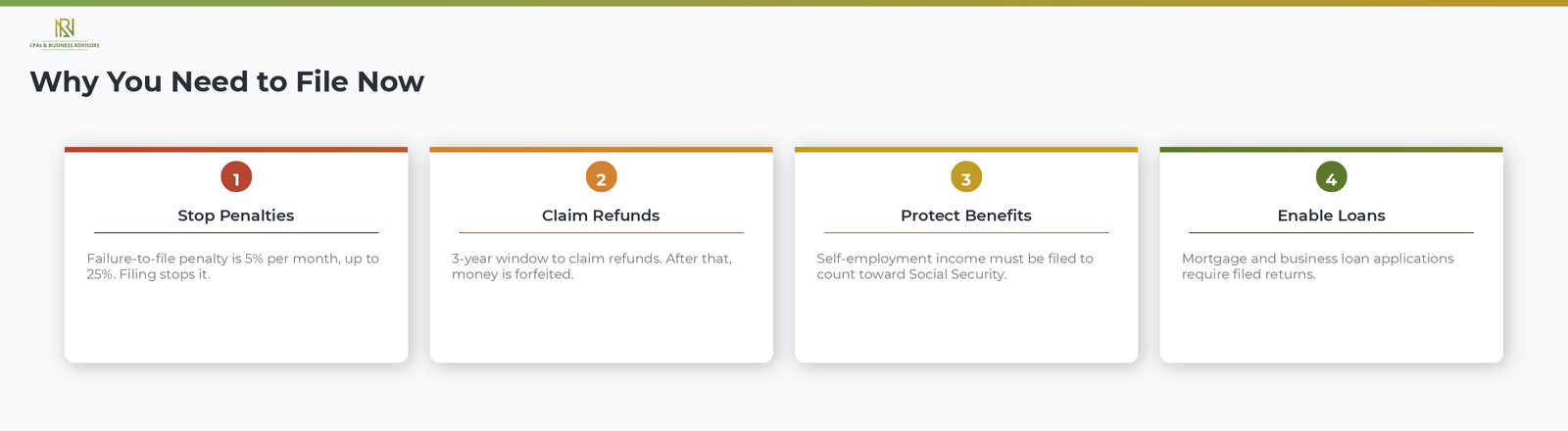

Filing unfiled tax returns, even if they are years late, stops the IRS from increasing your penalties, preserves your right to claim refunds and credits, and prevents the agency from filing a return on your behalf that gives you none of the deductions or credits you may be entitled to. According to the IRS, the failure-to-file penalty is 5 percent of the unpaid tax for each month or part of a month that a return is late, up to a maximum of 25 percent. This penalty is separate from and more expensive than the failure-to-pay penalty, which is 0.5 percent per month. Filing, even when you cannot pay the balance, stops the larger penalty from growing.

Beyond penalties, unfiled returns create problems that extend into other areas of your financial life. According to the IRS, the agency holds income tax refunds when its records show that one or more returns are past due. Self-employed individuals who do not file will not have their earnings reported to the Social Security Administration, which means lost credits toward retirement and disability benefits. Mortgage lenders, business loan providers, and federal financial aid programs all require copies of filed tax returns as part of the approval process.

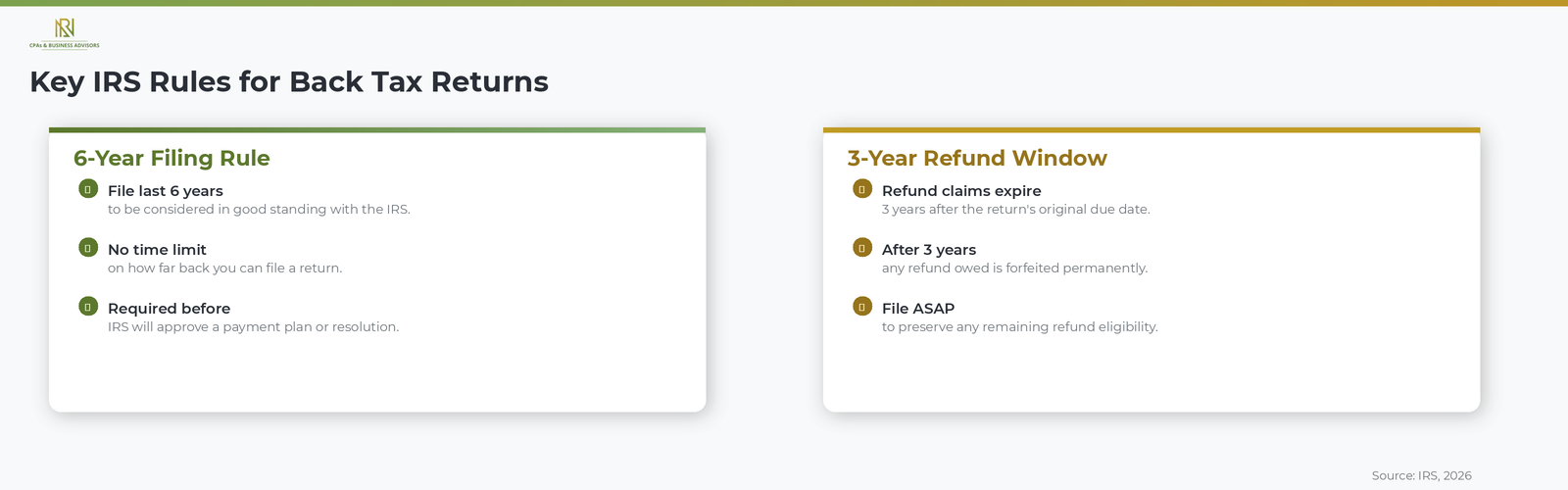

How Many Years Of Back Taxes Do You Need To File

The IRS generally requires you to file the last six years of unfiled tax returns to be considered in compliance, though the agency prefers that you file all outstanding returns. According to the IRS, there is no statute of limitations on filing a past-due return, meaning you can file a return for any prior year regardless of how long ago it was due. However, the IRS only allows you to claim a refund within three years of the return's original due date. After that three-year window closes, any refund you would have been owed is forfeited permanently.

If you have multiple years of unfiled returns, the IRS typically asks you to start with the oldest unfiled year and work forward. Filing all six years brings your account into good standing and is usually required before the IRS will approve a payment plan or other resolution for any balance you owe. For a full overview of the resolution options available once you have filed, our guide to handling a tax balance you cannot pay covers installment agreements, Offers in Compromise, and hardship status.

How To Reconstruct Tax Records For Past Years

If you no longer have the W-2s, 1099s, or other income documents you need to prepare a past-due return, the IRS can provide transcripts of the income information it has on file for you. According to the IRS, you can request wage and income transcripts by filing Form 4506-T, Request for Transcript of Tax Return. These transcripts cover the last 10 tax years and include the information reported to the IRS by your employers, banks, and other payers.

Wage and income transcripts show the data from forms such as W-2s, 1099s, and 1098s, but they do not include information about deductions or credits you may qualify for. To fill in those gaps, gather any records you still have, including bank and brokerage statements, mortgage interest statements, property tax records, charitable donation receipts, and documentation of business expenses if you were self-employed. If you cannot locate certain records, your bank or financial institution may be able to provide duplicate statements for prior years.

Step By Step Guide To Filing Back Tax Returns

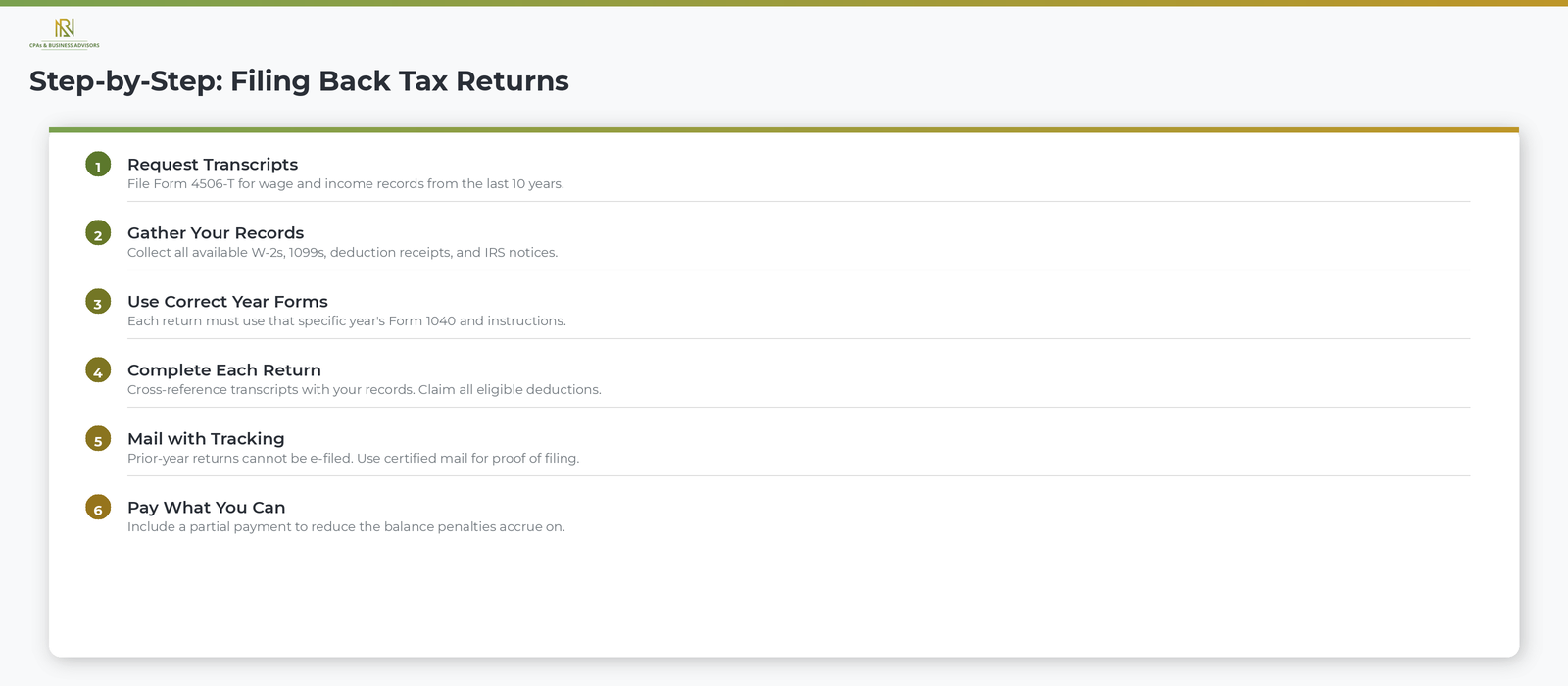

Filing a back tax return follows the same general process as filing a current-year return, with a few important differences in the forms and filing method you use. Follow these steps to file each unfiled return.

- Request your transcripts. File Form 4506-T with the IRS to get wage and income transcripts for each unfiled year. You can request transcripts online through your IRS Online Account, by mail, or by calling 800-829-1040.

- Gather your records. Collect all available income documents, deduction and credit documentation, and any IRS notices you have received for each unfiled year.

- Use the correct year's tax forms. According to the IRS, you must file each return using the tax forms and instructions for the specific year the return covers. A 2021 return must be filed on 2021 forms, a 2022 return on 2022 forms, and so on. Prior-year forms are available on the IRS website under "Prior Year Products."

- Complete the return carefully. Cross-reference the information on your transcript with the documents you gathered to make sure all income is reported and all eligible deductions and credits are claimed. Review each return against the transcript before filing.

- Mail the return. According to the IRS, prior-year returns generally cannot be e-filed and must be mailed to the address listed in the instructions for that year's Form 1040. Use certified mail or a trackable delivery service so you have proof of filing.

- Pay what you can. If the return shows a balance due, include a payment for as much as you can afford. Even a partial payment reduces the balance on which penalties and interest accrue.

According to the IRS, it takes approximately six weeks to process an accurately completed past-due return. If you received a notice about unfiled returns, send the completed return to the address indicated on the notice rather than the standard filing address.

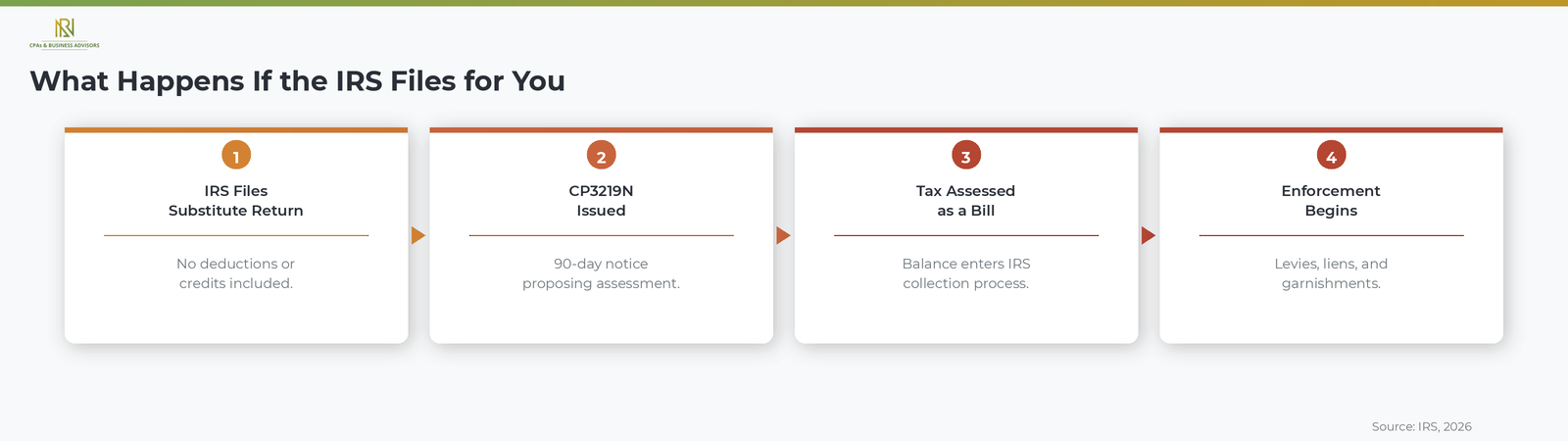

What Happens If The IRS Files A Return For You

If you do not file voluntarily, the IRS can file a substitute return on your behalf, and this substitute return will not include deductions, credits, or exemptions you may be entitled to claim. According to the IRS, a substitute return is based solely on the income information the agency received from third parties such as employers and banks. Because it does not account for deductions like business expenses, itemized deductions, or tax credits such as the Earned Income Credit, the substitute return almost always results in a higher tax bill than the return you would have filed yourself.

After preparing a substitute return, the IRS sends a CP3219N, which is a Notice of Deficiency (also called a 90-day letter) proposing the tax assessment. You have 90 days to either file your own return or petition the U.S. Tax Court. Taxpayers who want to understand the CP3219A Notice of Deficiency in detail, including the 90-day deadline and Tax Court options, can review our full guide to the statutory notice of deficiency. If you do neither, the IRS proceeds with the assessment, and the balance enters the standard collection process.

How To Handle The Balance After Filing

Filing back tax returns often results in a balance due, and the IRS expects you to address that balance even if you cannot pay it in full. According to the IRS, you have several options for resolving the amount owed.

- Pay in full. The fastest way to stop penalties and interest from accruing further.

- Short-term payment extension. According to the IRS, you can request an additional 60 to 120 days to pay your balance in full through the IRS Online Payment Agreement tool or by calling 800-829-1040, with no setup fee.

- Installment agreement. A monthly payment plan that spreads the balance over time. Our step-by-step guide to installment agreements explains the application process and balance thresholds.

- Offer in Compromise. If the full balance is unlikely to be collected, you may be able to settle for less than you owe.

- Currently Not Collectible status. If you cannot afford to pay anything, the IRS may temporarily pause collection.

Taxpayers who are filing multiple years of back returns and facing a combined balance may also qualify for the IRS Fresh Start program, which expands eligibility for installment agreements and eases lien thresholds for individuals and businesses working to get back into compliance.

Frequently Asked Questions About Filing Back Taxes

How Far Back Can You File Taxes?

You can file a tax return for any prior year with no time limit on how far back you go. According to the IRS, there is no statute of limitations on filing a past-due return. However, refund claims must be filed within three years of the return's original due date, and the IRS generally requires the last six years of returns to consider you in compliance.

Can You File Back Taxes Online?

Most prior-year returns cannot be e-filed and must be printed and mailed to the IRS. According to the IRS, e-filing is generally only available for the current tax year and the two most recent prior years. Returns for earlier years must be completed on the appropriate year's forms and mailed to the address in the instructions.

What Happens If You Have Not Filed Taxes In Several Years?

The IRS tracks unfiled returns and can take enforcement action including filing a substitute return, assessing penalties, holding your refunds, and eventually pursuing levies and liens. According to the IRS, the best course of action is to file all outstanding returns as soon as possible, pay what you can, and contact the IRS to discuss resolution options for any remaining balance.

Owe The IRS And Can't Pay? Your Options

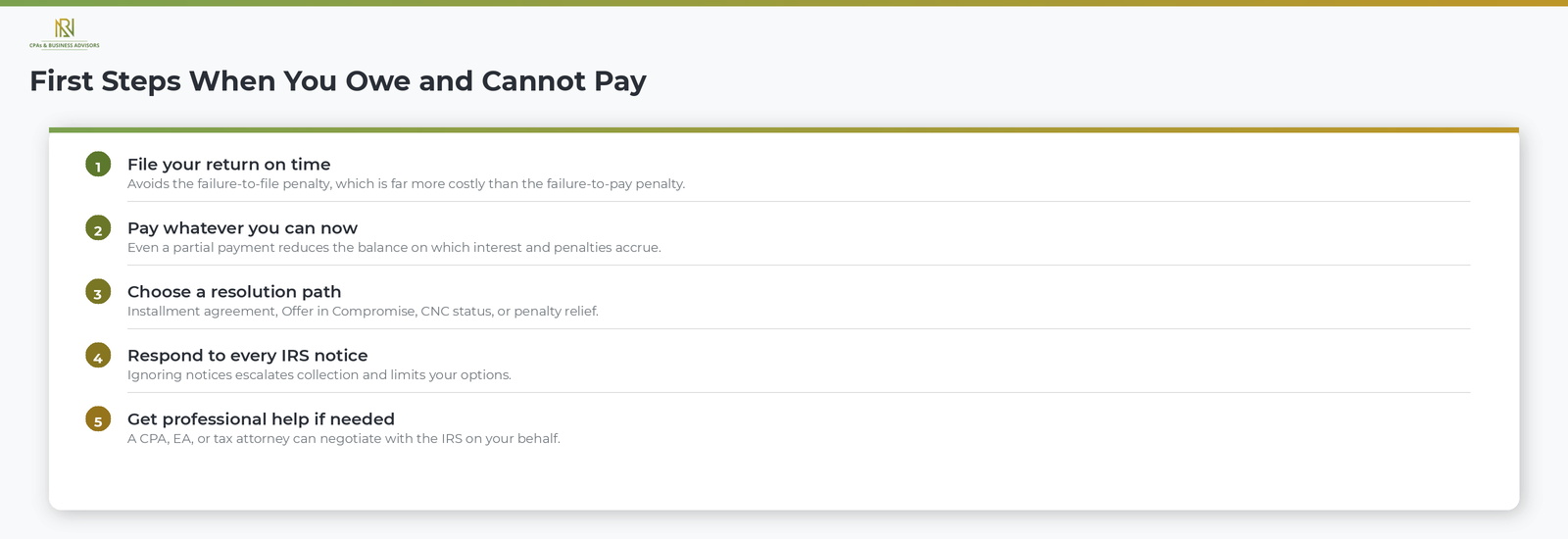

If you owe the IRS and cannot pay the full amount, the most important step you can take is to file your return on time and pay as much as you can, even if that amount is far less than what you owe. According to the IRS, filing on time avoids the failure-to-file penalty, which is significantly more expensive than the failure-to-pay penalty. Paying even a partial amount reduces the balance on which the IRS calculates interest and penalties, which means the total debt grows more slowly than it would if you paid nothing at all.

The IRS does not expect every taxpayer to pay in full on the due date. According to the IRS, the agency offers several programs specifically designed for taxpayers who owe but cannot pay, and most of these options are available whether your debt is recent or has been accumulating for years. The worst action you can take is no action. Ignoring a tax debt does not make it go away. Instead, it triggers an escalating series of IRS collection notices that can eventually result in wage garnishments, bank account levies, property seizures, and federal tax liens that damage your credit. For a full breakdown of how the IRS notice sequence works, our complete guide to IRS correspondence explains every stage from balance due reminders to final enforcement.

Your Options For Resolving IRS Tax Debt

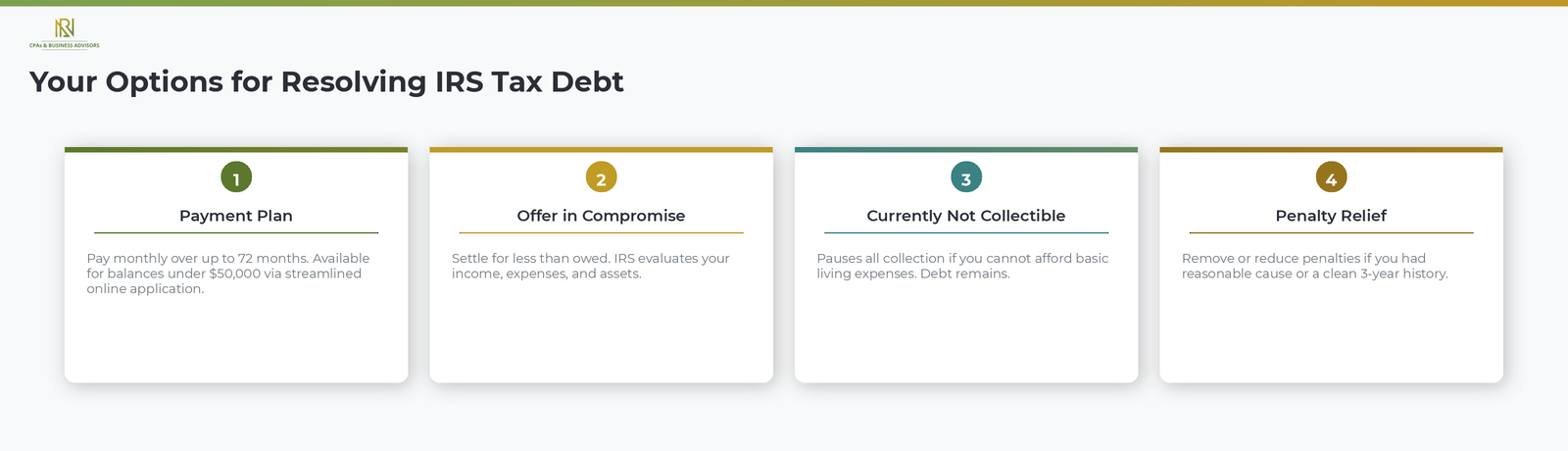

The IRS provides four primary paths for taxpayers who owe but cannot pay in full: installment agreements, Offers in Compromise, Currently Not Collectible status, and penalty relief. The right option depends on how much you owe, how much you can afford to pay each month, and whether you are experiencing financial hardship.

Payment Plans And Installment Agreements

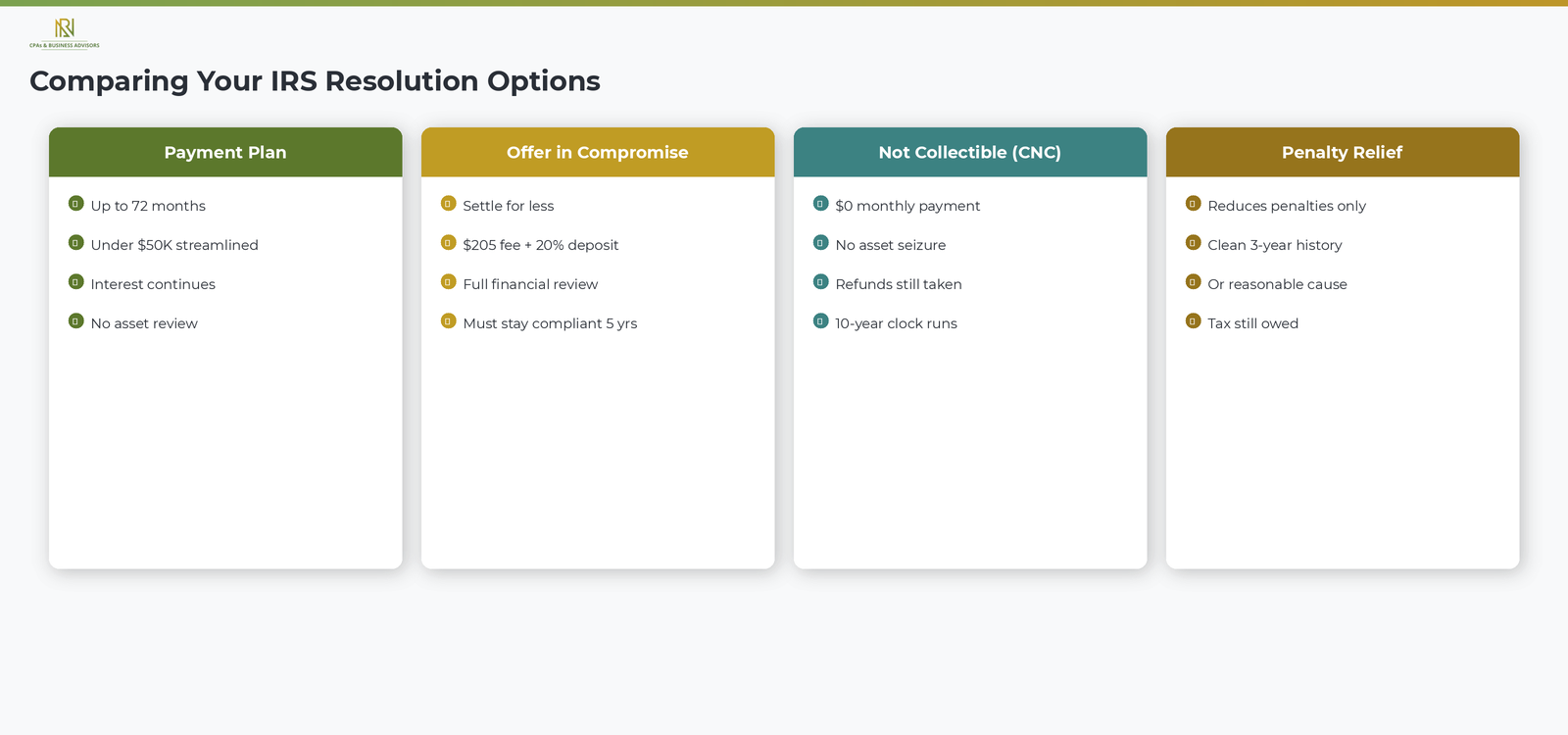

An installment agreement allows you to pay your tax debt in monthly installments over time instead of all at once. According to the IRS, two types of plans are available. A short-term payment plan gives you up to 180 days to pay the full balance, with no setup fee if you apply online. A long-term installment agreement spreads payments across up to 72 months and is available to taxpayers who owe less than $50,000 in combined tax, penalties, and interest. According to the IRS, taxpayers who owe $50,000 or less can apply for a streamlined installment agreement through the IRS Online Payment Agreement tool without providing detailed financial documentation. Our step-by-step guide to installment agreements covers the full application process, balance thresholds, and how interest is calculated on the remaining amount.

Offer In Compromise

An Offer in Compromise allows you to settle your tax debt for less than the full amount you owe. According to the IRS, the agency considers your ability to pay, your income, your expenses, and your asset equity when deciding whether to accept an offer. The IRS generally approves an offer when the amount you propose represents the most the agency can expect to collect within a reasonable period. To apply, you submit Form 656 along with a $205 application fee and an initial payment. Low-income taxpayers who meet the IRS certification guidelines are exempt from both the fee and the initial payment. According to the IRS, you can check your eligibility using the Offer in Compromise Pre-Qualifier tool on IRS.gov before applying.

Currently Not Collectible Status

If your income is so low that you cannot afford to pay anything toward your tax debt without failing to meet basic living expenses, you may qualify for Currently Not Collectible status. According to the IRS, this designation temporarily pauses all collection activity on your account, including levies and garnishments. The tax debt does not go away, and interest and penalties continue to accrue, but the IRS will not take enforcement action while you remain in this status. According to the IRS, the agency will take your future tax refunds and apply them to the balance, and if you owe more than $10,000, the IRS will generally file a Notice of Federal Tax Lien. The IRS reviews your financial situation periodically and may resume collection activity if your income improves.

An important feature of Currently Not Collectible status is that it does not stop the IRS's 10-year statute of limitations on collecting a tax debt. According to the IRS, the agency generally has 10 years from the date a tax debt is assessed to collect it. If the statute expires while your account is in Currently Not Collectible status, the debt is written off permanently.

Penalty Relief

If you owe penalties on top of your tax balance, you may qualify for penalty relief. According to the IRS, the agency can reduce or remove penalties if you tried to comply with the law but were unable to meet your obligations due to circumstances beyond your control, such as a natural disaster, serious illness, or the death of a close family member. First-time penalty abatement is also available to taxpayers who have a clean compliance history for the three prior tax years.

How The IRS Decides Which Option You Qualify For

The IRS evaluates your eligibility for each program based on your total debt, your monthly income and expenses, and the equity in your assets. According to the IRS, the agency uses national and local cost-of-living standards to determine what constitutes a reasonable monthly expense. If your income exceeds your allowable expenses, the IRS expects you to put the difference toward your tax debt through a payment plan. If your allowable expenses equal or exceed your income and you have no significant assets, you may qualify for Currently Not Collectible status or an Offer in Compromise.

Taxpayers facing financial hardship may also qualify for the IRS Fresh Start program, which broadens the eligibility criteria for installment agreements, reduces the threshold for streamlined applications, and makes it easier to qualify for lien withdrawals after meeting certain conditions. The Fresh Start program is not a separate application. It is a set of expanded guidelines the IRS applies to existing resolution options.

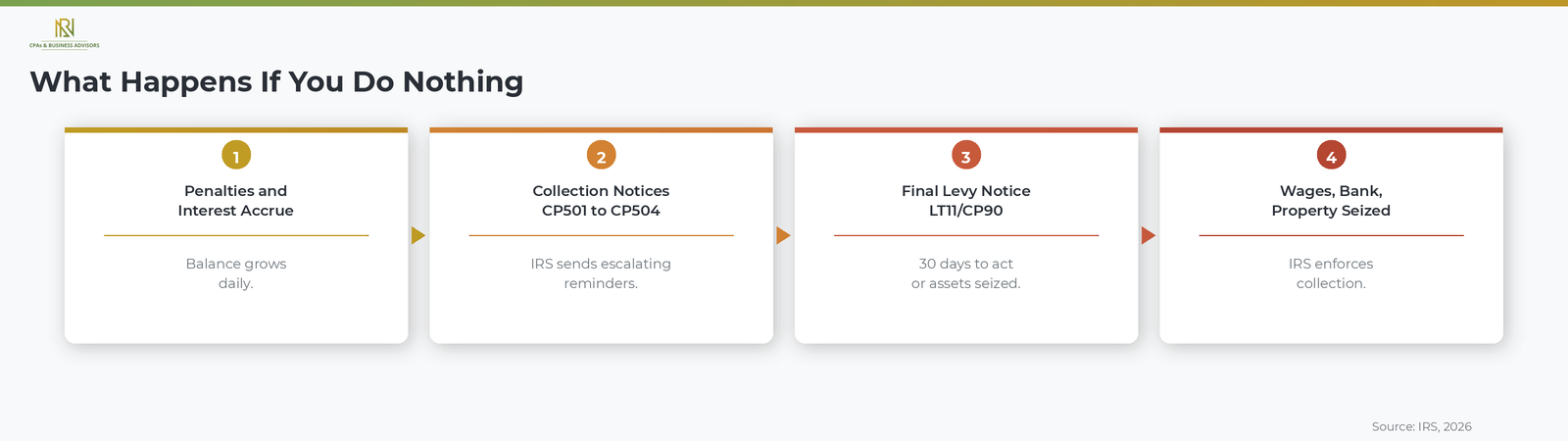

What Happens If You Do Nothing

Doing nothing when you owe the IRS causes penalties and interest to compound daily on your unpaid balance and moves your account through an escalating collection process that can result in the IRS seizing your income and property. According to the IRS, the standard collection sequence begins with a CP14 balance due notice and progresses through CP501 and CP503 reminders, a CP504 Notice of Intent to Levy, and finally an LT11 or CP90 Final Notice of Intent to Levy. At the final notice stage, the IRS is authorized to levy your wages, bank accounts, personal property, and up to 15 percent of your Social Security benefits. Taxpayers who want to understand the full enforcement timeline can review our guide to the LT11 final levy notice.

In addition to levies, the IRS can file a Notice of Federal Tax Lien at any point after a balance remains unpaid. A lien is a public record that establishes the government's legal claim against your assets, can severely damage your credit, and makes it difficult to sell or refinance property. The FAST Act also authorizes the State Department to deny, revoke, or limit your passport if your tax debt meets the threshold for seriously delinquent tax debt.

When To Get Professional Help

Consider working with a CPA, Enrolled Agent, or tax attorney if your tax debt is large, if you are facing active collection action such as a levy or lien, or if you are unsure which resolution option is right for your financial situation. A qualified tax professional can analyze your income, expenses, and assets, determine which IRS program gives you the best outcome, and negotiate directly with the IRS on your behalf. According to the IRS, you can authorize a representative by filing Form 2848, Power of Attorney and Declaration of Representative.

Frequently Asked Questions About Owing The IRS

What Happens If I Owe The IRS More Than $50,000?

You can still set up a payment plan, but you will need to provide detailed financial information to the IRS. According to the IRS, the streamlined installment agreement is only available for balances of $50,000 or less. For larger amounts, you may need to submit Form 433-A (Collection Information Statement) and work directly with the IRS to negotiate terms. An Offer in Compromise may also be an option if the full balance is uncollectible.

Does The IRS Forgive Tax Debt?

The IRS does not automatically forgive tax debt, but it does offer programs that can reduce or eliminate what you owe. An Offer in Compromise allows you to settle for less than the full amount. Currently Not Collectible status pauses collection, and the 10-year statute of limitations on collections means the debt can expire if the IRS does not collect it within that window.

Can I Negotiate With The IRS On My Own?

Yes, you can negotiate directly with the IRS without hiring a representative. According to the IRS, you can apply for payment plans online, submit an Offer in Compromise yourself, and request Currently Not Collectible status by calling the number on your notice. However, taxpayers with complex situations, large balances, or active enforcement actions often benefit from professional representation.