%201.avif)

.png)

.png)

What Does a Fractional CFO Do?

A fractional CFO is an experienced financial executive who provides strategic CFO-level guidance to businesses on a part-time, contract, or retainer basis. They do the same work as a full-time CFO, including cash flow management, financial forecasting, budgeting, fundraising support, risk management, and long-term strategic planning. The difference is that you only pay for the hours your business actually needs.

For most small and mid-sized businesses, the fractional CFO model is the most practical way to get executive-level financial leadership without committing to a salary that can exceed $400,000 per year. According to Strategic Market Research, the global virtual CFO market was valued at $7.8 billion in 2024 and is projected to reach $17.9 billion by 2030, growing at a 12.5% annual rate. That growth reflects a clear shift in how businesses think about financial leadership. This article breaks down exactly what a fractional CFO does, what they cost, who needs one, and how the role compares to other financial professionals.

What a Fractional CFO Does for Your Business

A fractional CFO does everything a full-time CFO does, but on a flexible schedule that fits your business needs and budget. Their work falls into several core areas that directly impact how well your business manages money, plans for growth, and avoids costly financial mistakes.

Cash Flow Forecasting and Management

Cash flow is the number one reason small businesses fail. According to SCORE, 82% of small business failures trace back to cash flow problems. A fractional CFO builds rolling cash flow forecasts, monitors burn rate, tracks working capital, and makes sure you always know your financial position weeks and months in advance. This is not something a bookkeeper or accountant is trained to do. A bookkeeper records what already happened. A fractional CFO tells you what is going to happen and what to do about it.

Financial Modeling and Forecasting

A fractional CFO creates financial models that map out best-case, worst-case, and most-likely scenarios for your business. These models help you answer questions like "Can we afford to hire three people next quarter?" or "What happens to our margins if material costs go up 10%?" According to Gitnux, companies using fractional CFOs achieved forecasting accuracy of 95% with the right tools and systems in place. That level of accuracy replaces guesswork with confidence.

Budgeting and Cost Optimization

A fractional CFO helps you build budgets that align with your actual goals, not just last year's numbers. They also look for waste. According to Preferred CFO, the average company wastes approximately $135,000 per year on unused software subscriptions alone. A fractional CFO identifies those leaks and redirects that money toward growth. Companies using fractional executives see a 15% reduction in wasted operational spending within the first six months, according to data from WifiTalents.

Fundraising and Investor Relations

If your business is raising capital, a fractional CFO is essential. They prepare investor-ready financial models, build data rooms, support due diligence, and help you tell a financial story that investors trust. According to the Kauffman Foundation, 83% of entrepreneurs do not access bank loans or venture capital at the time of startup. A fractional CFO bridges that gap by making your financials clear, credible, and compelling. Our startup advisory work focuses heavily on this kind of support.

Strategic Planning and Growth Advisory

A fractional CFO helps leadership teams make data-driven decisions about expansion, pricing, hiring, and market entry. According to Gartner, 47% of finance leaders cite enterprise growth strategy as a top priority. The CFO takes financial data and turns it into a clear roadmap for where the business should go next. Strategic planning is the layer of financial leadership that most small businesses are missing.

How Much Does a Fractional CFO Cost Per Month?

A fractional CFO costs between $3,000 and $12,000 per month for most small to mid-sized businesses. According to Madras Accountancy's 2026 industry data, typical engagements involve 15 to 40 hours per month depending on company size and complexity. The most common retainer for small to mid-sized companies falls between $5,000 and $7,000 per month, according to The Expert CFO.

Compare that to a full-time CFO. According to Salary.com, the average annual salary for a full-time CFO in the United States is approximately $437,000, with total compensation packages reaching nearly $790,000 when you add benefits, bonuses, and retirement contributions. When you also factor in recruitment fees (which can equal 30% of the first-year salary), payroll taxes (adding 25% to 40% on top of base), and the 90 to 180 days it takes to recruit and onboard a full-time hire, the fractional model saves businesses 60% to 80% in total cost.

For startups in the early stages, the cost is even lower. According to Graphite Financial, early-stage companies need only 8 to 10 hours of support per month, which translates to $1,400 to $2,800 monthly. As the business grows, the engagement scales up. That flexibility is one of the biggest advantages of the fractional model. You pay for exactly what you need, and nothing more. Understanding your financial statements clearly is the first step toward getting the most value out of that engagement.

What Is a Fractional CFO Salary?

A fractional CFO salary depends on whether you are asking what they earn total across all clients or what they charge a single business. According to ZipRecruiter, the average annual pay for a fractional CFO in the United States is $151,302 as of 2026, with top earners making up to $257,500. That is their total income across multiple clients.

From the business owner's perspective, the cost is much lower because you are only paying for your share of their time. Hourly rates typically range from $150 to $450 depending on experience, industry, and geographic location. According to CFO Recruit, entry-level fractional practitioners with 5 to 10 years of experience charge $150 to $250 per hour. Mid-tier CFOs with 10 to 15 years command $250 to $350. Premium CFOs with 15-plus years and specialized expertise in fundraising or mergers charge $350 to $500 per hour.

According to data from The Expert CFO, fractional CFO ROI runs 3 to 10 times the investment through cash flow optimization and cost reduction. The cost typically pays for itself within 3 to 6 months for most businesses. That makes the fractional model not just affordable, but genuinely profitable for the companies that use it.

Is Being a Fractional CFO Worth It?

Yes, being a fractional CFO is worth it both for the CFO and for the businesses they serve. From the business perspective, the value is measurable and immediate. From the CFO's perspective, the model offers flexibility, diverse experience, and strong earning potential.

For businesses, according to Gitnux, clients report 92% satisfaction with fractional CFO providers. Companies saw profit margins expand by 12% to 18% on average in their first year. Investor confidence scores rose 40% after a fractional CFO engagement. Working capital efficiency improved 35% on average. These are not abstract benefits. They translate directly into more cash, better decisions, and faster growth. We see these kinds of results across the businesses we work with in the Miami area and across the country through our virtual CFO services.

For the CFOs themselves, the fractional model allows them to work with multiple companies simultaneously, apply their skills across diverse industries, and earn competitive income without being tied to a single employer. According to ZipRecruiter, top-earning fractional CFOs make over $257,000 per year. Many fractional CFOs are former Big Four alumni or Fortune 500 executives who choose the fractional path for its flexibility and impact. According to NOW CFO, 40% of fractional CFOs come from Big Four accounting backgrounds.

How Many Hours Does a Fractional CFO Work?

A fractional CFO works between 5 and 40 hours per month for a single client, depending on the size and complexity of the business. According to NOW CFO, the typical engagement involves 5 to 20 hours per month. The average engagement lasts between 12 and 18 months during a growth phase.

Early-stage startups with simpler financial needs might use 8 to 10 hours per month. Businesses in the $2 million to $10 million revenue range typically need 20 to 40 hours. Companies approaching fundraising, an acquisition, or a major expansion often scale up temporarily to get through the intensive financial preparation those events require.

Across all clients, a fractional CFO may work 30 to 50 hours per week total. The difference is that those hours are spread across multiple businesses, so each client gets exactly the amount of attention their situation demands. This model works because most growing businesses do not need a CFO sitting in the office 40 hours a week. They need a few hours of high-level strategic thinking each week from someone who has done it hundreds of times before.

How Many Clients Does a Fractional CFO Have?

A fractional CFO typically has 3 to 7 clients at any given time. The exact number depends on how many hours each engagement requires and how complex the work is. A CFO working with several early-stage startups needing 8 to 10 hours each can handle more clients. A CFO supporting one company through a fundraise and another through an acquisition may only take on 3 or 4 at a time.

This multi-client model is actually an advantage for the businesses they serve. Because fractional CFOs work across multiple industries and companies simultaneously, they bring a wider range of experience to every engagement. They have seen more problems, tested more solutions, and built more financial models than a CFO who has spent 10 years at a single company. According to Spendesk, this breadth of experience is one of the most valuable things a virtual CFO offers.

Do I Need a CPA to Be a Fractional CFO?

No, you do not need a CPA to be a fractional CFO. While a CPA license is valuable and common among fractional CFOs, it is not a legal requirement for the role. A CFO's job is strategic financial leadership, which requires strong skills in forecasting, financial modeling, cash flow management, and business strategy. A CPA focuses on accounting, tax compliance, and auditing.

That said, many of the best fractional CFOs do hold a CPA credential. According to NOW CFO, 40% of fractional CFOs are former Big Four accounting alumni, and many of those hold CPA licenses. The CPA adds credibility and signals a deep understanding of tax planning and financial reporting standards. But other credentials like an MBA, CMA (Certified Management Accountant), or years of executive finance experience at high-growth companies can be equally valuable.

For business owners hiring a fractional CFO, the most important thing is not whether they have specific letters after their name. It is whether they have a track record of solving financial problems like yours. Ask about specific results: cash runway extended, funding secured, margins improved, costs reduced. A strong fractional CFO should be able to answer those questions with concrete numbers. Getting the right financial leadership in place early, ideally right from business formation, sets the stage for everything that follows.

Is CFO Higher Than CPA?

Yes, a CFO is higher than a CPA in the organizational hierarchy of a business. A CPA is a professional credential that certifies someone to practice public accounting, prepare taxes, and perform audits. A CFO is a C-suite executive position responsible for the entire financial strategy of a company.

A CPA can be a CFO, and many CFOs hold CPA licenses. But the roles serve different purposes. A CPA is focused on compliance, accuracy, and historical financial reporting. A CFO uses that data to plan the future, manage risk, guide investment decisions, and lead the financial direction of the business. According to Gartner, over 70% of CFOs now handle responsibilities well beyond traditional finance, including technology strategy, data analytics, and enterprise-wide planning.

In most companies, the CPA either works as part of the accounting team or serves as the external tax advisor. The CFO sits at the executive table alongside the CEO. They are the person who takes the numbers the CPA produces and turns them into strategy. Businesses dealing with IRS issues or complex tax situations often benefit most when a CPA and a CFO work together, each doing what they do best.

Fractional CFO vs Bookkeeper vs Accountant vs Full-Time CFO

Choosing the right level of financial support depends on the stage and complexity of your business. Each role builds on the one before it, and hiring the wrong one at the wrong time wastes money or creates dangerous blind spots.

RoleWhat They DoCost RangeBest ForBookkeeperRecords transactions, manages invoices, reconciles bank accounts$20 to $50 per hourBusinesses with simple finances and low transaction volumeAccountant / CPAPrepares taxes, ensures compliance, interprets financial statements$150 to $400 per hourBusinesses needing tax strategy, compliance, and year-end reportingFractional CFOCash flow forecasting, financial modeling, budgeting, fundraising, strategic planning$3,000 to $12,000 per monthBusinesses with $1M to $50M revenue needing strategic financial leadershipFull-Time CFODaily financial leadership, team management, investor relations, complex compliance$300,000 to $500,000+ per yearBusinesses with $50M+ revenue and daily executive-level financial demands

Sources: Salary.com, ZipRecruiter, Graphite Financial, The Expert CFO, Bennett Financials, Robert Half

The key distinction is between looking backward and looking forward. Bookkeepers and accountants look backward. They tell you what happened. A fractional CFO looks forward. They tell you what is going to happen and what you should do about it. If you are making major business decisions without solid financial projections, you have outgrown your current financial setup and need CFO-level support. Businesses that track the right financial metrics are better positioned to know exactly when that shift should happen.

Is a CFO for a Small Company Worth It?

Yes, a CFO is worth it for a small company. The return on investment is measurable and typically exceeds the cost within the first 3 to 6 months. A fractional CFO helps small businesses find money they did not know they were losing, plan taxes proactively instead of reactively, and make growth decisions backed by data instead of instinct.

According to data from Gitnux, companies using fractional CFOs saw profit margins expand by 12% to 18% in their first year. Strategic pricing reviews led to a 5% revenue increase without a single new customer. Investor confidence scores rose 40%. These results are not limited to large companies. They apply to businesses doing $1 million to $10 million in revenue that bring in the right financial leadership at the right time.

The cost of not having a CFO is almost always higher than the cost of having one. According to Gartner's CFO Leadership Vision, profits lost due to financially unsound operating decisions currently equal approximately 3% of EBITDA. For a business doing $5 million in revenue with 15% EBITDA margins, that translates to roughly $22,500 per year in avoidable losses. A fractional CFO engagement at $5,000 per month pays for itself several times over. Smart tax-saving strategies alone can offset the cost in many cases.

Why Are CPAs Declining?

CPAs are declining because fewer people are entering the profession, and the pipeline of new accountants is shrinking. According to data from the American Institute of CPAs (AICPA), the number of students completing accounting degrees has dropped significantly over the past several years. At the same time, a large wave of experienced CPAs is retiring, creating a widening talent gap.

Several factors drive this trend. The 150-credit-hour requirement to sit for the CPA exam adds an extra year of education beyond a typical bachelor's degree, which discourages many students. Starting salaries in public accounting have historically lagged behind other fields like technology and finance. The workload, especially during tax season, is intense. Many young professionals are choosing alternative career paths that offer better pay, more flexibility, or both.

This decline has real consequences for businesses. Fewer CPAs means longer wait times for tax preparation, less availability for audit and compliance work, and higher fees across the board. It also reinforces the value of the fractional CFO model. A fractional CFO who also holds a CPA license brings both strategic and compliance expertise to the table. For businesses that need both business consulting and financial compliance, working with a CPA-led firm that offers CFO-level advisory is the most efficient path forward.

What Degree Do Most CFOs Have?

Most CFOs have a bachelor's degree in accounting, finance, or business administration. Many also hold an MBA or a master's degree in finance. According to Robert Half, a CPA certification remains the gold standard for CFO roles and typically adds 10% to 15% to compensation. MBAs from top-tier schools carry similar premiums.

In practice, what matters more than the degree is the experience. The best fractional CFOs have 10 to 20 or more years of progressive experience in corporate finance, FP&A (financial planning and analysis), or executive leadership. Many started in public accounting at firms like Deloitte, PwC, Ernst & Young, or KPMG, then moved into corporate finance roles before eventually going fractional. According to NOW CFO, 40% of fractional CFOs are alumni of Big Four accounting firms.

For business owners hiring a fractional CFO, the degree on their resume matters far less than their ability to build accurate financial forecasts, manage cash flow, and deliver actionable advice that moves the business forward. Ask about results, not credentials. The right CFO for your company is the one who has solved problems like yours and can prove it with numbers.

Frequently Asked Questions

Is CFO a High Stress Job?

Yes, CFO is a high stress job. The role has expanded beyond traditional finance to include technology strategy, AI adoption, cybersecurity, and enterprise-wide data analytics. According to Russell Reynolds Associates, CFO turnover hit a seven-year high in 2025, with burnout and heavier workloads cited as primary drivers. The average CFO tenure has dropped to 5.8 years. The fractional model reduces some of this stress because the CFO works across multiple clients and can structure their workload more flexibly than a full-time executive tied to a single company.

What Is a Typical CFO Salary?

A typical CFO salary in the United States ranges from $150,000 to over $500,000 depending on company size and industry. According to Robert Half's 2026 data, CFOs with at least 10 years of experience earn $195,500 at the lowest tier, $269,750 at mid-tier, and $321,750 at the top tier. For companies with $1 billion to $5 billion in revenue, average CFO compensation reaches $423,019 per year. Total compensation packages at larger companies can exceed $1 million including bonuses, equity, and benefits.

Which Pays More, CFP or CPA?

A CPA generally pays more than a CFP (Certified Financial Planner) in terms of average salary. CPAs work in accounting, tax, and corporate finance, where compensation tends to be higher. CFPs work in personal financial planning and wealth management. However, earning potential for both depends heavily on specialization, experience, and the type of firm or practice. A CPA working as a CFO or partner at a large firm will significantly outearn a CFP, while a CFP managing high-net-worth clients can also earn substantial income. The paths are different and serve different purposes.

Is AI Replacing Bookkeepers?

AI is automating many routine bookkeeping tasks like transaction categorization, bank reconciliation, and invoice processing, but it is not fully replacing bookkeepers yet. According to a Goldman Sachs survey from 2025, 80% of small business leaders using AI reported increased efficiency and productivity. The bookkeeping tasks most likely to be automated are repetitive and data-entry driven. What AI cannot replace is the judgment, context, and relationship that a human financial professional provides. Businesses still need people to interpret data, catch anomalies, and connect financial information to real business decisions.

How Much Does a CFO Make at a $300 Million Company?

A CFO at a $300 million company typically earns between $350,000 and $600,000 in total compensation, including base salary, bonuses, and equity. According to Bennett Financials, companies with annual revenue between $50 million and $1 billion pay their CFOs an average base salary of $250,000 to $400,000. When you add performance bonuses (typically 30% to 60% of base salary) and equity incentives, the total package can climb substantially higher. Companies at the $300 million level also tend to provide strong benefits, retirement contributions, and sometimes stock options.

What Jobs Pay $500,000 a Year in the US?

Jobs that pay $500,000 a year in the United States include C-suite executives at mid-sized to large companies (CEO, CFO, COO), senior partners at law firms, surgeons and specialist physicians, investment bankers, hedge fund managers, and senior technology executives at major companies. According to Workday's 2026 CFO salary guide, CFOs in the software sector at large companies can earn total compensation packages ranging from $4.2 million to $26.3 million. However, the $500,000 threshold is most commonly reached at companies with $500 million or more in revenue, or in high-compensation industries like finance, technology, and healthcare.

What It All Comes Down To

A fractional CFO gives growing businesses something that a bookkeeper, accountant, or even a controller cannot provide: a clear view of the future and a plan for how to get there. They build the forecasts, manage the cash flow, prepare for fundraising, and make sure every major financial decision is backed by real data. The model works because it delivers full CFO-level expertise at a fraction of the cost, with the flexibility to scale up or down as the business evolves.

If your business is past the startup phase and you are making financial decisions without solid projections, a fractional CFO is the right next step. At NR CPAs & Business Advisors, we provide virtual CFO support built around the real financial challenges growing businesses face every day. Call us at (305) 978-1533 to talk through your situation.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

What to Do When You Receive an IRS Notice?

If you receive an IRS notice, don't panic. Read it carefully, find the notice number to see what it is about, check the deadline, and then either follow the instructions to respond or get a tax professional to help. Most IRS letters deal with one specific issue and are straightforward to handle once you know what they are asking for.

First, Don't Panic (And Don't Ignore It)

A letter from the IRS rarely means trouble, but you should never ignore it. According to the IRS, it sends notices for routine reasons, such as a balance due, a changed refund, or a simple question about your return, and most are resolved by reading the letter and taking the step it asks for. What you cannot do is set it aside. Acting promptly limits interest and penalties, and many notices carry a firm deadline. The calm, timely response is almost always the cheapest one.

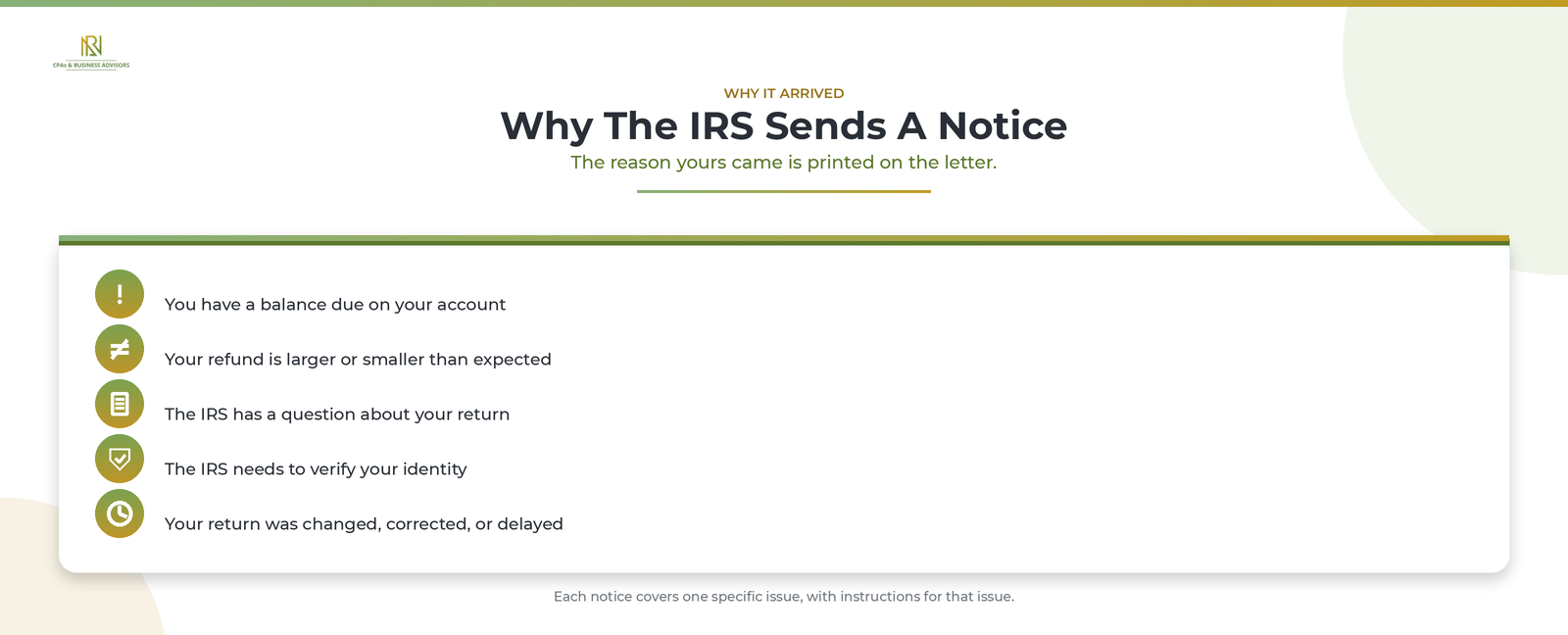

Why Did The IRS Send You A Notice?

The IRS contacts you when something on your account or return needs attention. According to the IRS, the most common reasons are:

- You have a balance due.

- Your refund is larger or smaller than you expected.

- The IRS has a question about your return or needs to verify your identity.

- The IRS changed or corrected your return.

- Your return is delayed in processing.

Each notice covers one specific issue and includes instructions for that issue, so the reason yours arrived is stated right on the letter.

What To Do When You Receive An IRS Notice

Work through the notice in order: read it, identify it, verify it, compare it to your return, note the deadline, respond, and keep a copy. According to the IRS, these steps handle the large majority of letters without a phone call or an office visit:

- Read the entire notice carefully to understand the issue and the action it asks for.

- Find the notice or letter number in the top right corner, such as CP14 or CP2000, and look it up on IRS.gov for a plain-English explanation.

- Verify the notice is genuine before you act or pay anything.

- Compare the notice against your tax return, and check which tax year it covers rather than assuming it is your most recent one.

- Note the response deadline and put it somewhere you will not miss it.

- Respond the way the notice tells you to, and only if it asks you to.

- Keep the notice and a copy of your response with your tax records.

The sections below cover the steps that trip people up most.

How To Tell If The Notice Is Real

A genuine IRS notice arrives by mail, never by text, email, or social media. According to the IRS, its first contact comes through the U.S. Postal Service, and it will never use social media or a text message to ask for personal or financial information. To confirm a letter is real, search the notice number on IRS.gov, where every notice is described. If the letter does not show up in that search or looks suspicious, call the IRS at 800-829-1040 and follow the representative's instructions rather than any contact details printed on a questionable letter.

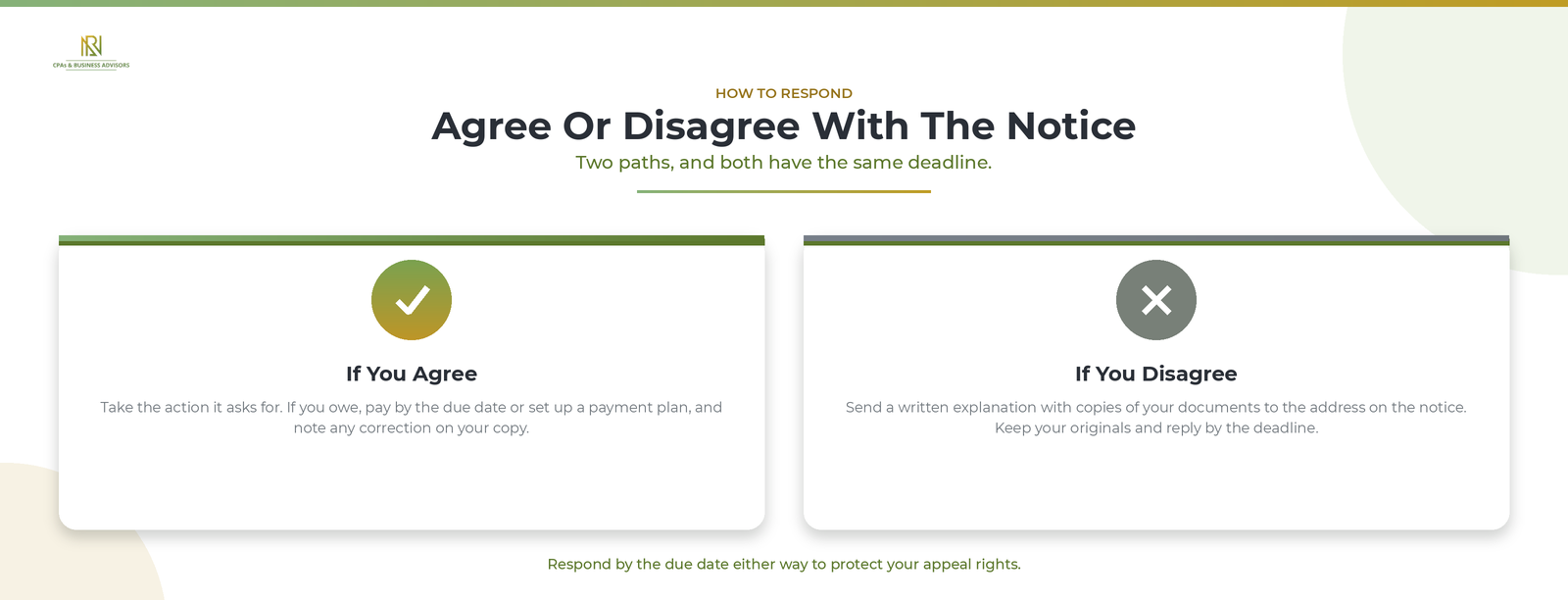

If You Agree With The Notice

If the notice is correct, simply do what it asks. According to the IRS, that usually means taking the requested action and, if you owe, paying by the due date to reduce interest and penalties. If you cannot pay in full, you can arrange to pay the balance over time and still send what you can now, writing the notice's reference number on your payment so the IRS applies it correctly. If the notice corrected your return and you agree, note the change on your own copy and keep it.

If You Disagree With The Notice

If you don't agree, you must respond by the deadline with a written explanation and proof. According to the IRS, you follow the dispute instructions on the notice, send a letter explaining why you disagree, and include copies of any documents that support your position, mailed to the address on the notice. Send copies and keep your originals, and allow at least 30 days for the IRS to reply. Responding by the due date is also what protects your right to appeal later.

How Long Do You Have To Respond?

Most IRS notices give you about 30 days to respond, though the exact window is printed on the letter and varies by notice type. According to the IRS, you should act by the due date shown, because replying on time both limits added interest and penalties and guarantees your appeal rights. If you need more time, call the number in the top right corner of the notice before the deadline passes.

What Happens If You Ignore An IRS Notice?

Ignoring a notice doesn't make it go away; it makes the problem larger. According to the IRS, when you don't respond, interest and penalties keep building and the IRS moves ahead with whatever the letter proposed, which can mean assessing tax you might have disputed or starting collection on a balance. Some letters carry legal deadlines, and missing them costs you options, such as the chance to take a disputed amount to the U.S. Tax Court. Whatever the notice, the safe move is to respond within the window it gives you. If yours is a specific letter like a CP2000 underreported income notice or a CP14 balance due notice, follow the steps for that notice in particular.

Should You Handle It Yourself Or Get Help?

You can resolve most IRS notices on your own, especially simple ones where you agree and just need to pay or send a document. According to the IRS, the majority of correspondence can be handled without calling or visiting an office. Bring in a professional when the amount is large, when you disagree and need to build a documented case, or when the letter signals an examination. A CPA, enrolled agent, or tax attorney can deal with the IRS for you, and a firm offering IRS tax resolution services can manage the whole response. If cost is a concern, a Low Income Taxpayer Clinic may be able to represent you for free or a small fee.

Can You View IRS Notices Online?

Yes, you can see many IRS notices in your online account. According to the IRS, you can view digital copies of select notices and even go paperless for certain letters by signing in to your IRS Online Account. That is also a useful way to confirm a balance or check that a payment has been applied before you respond to a notice about it.

Frequently Asked Questions

How do I respond to an IRS notice? Follow the instructions printed on the notice, and reply only if it asks you to, using the response form or the address provided, within the deadline.

Why would the IRS send me a notice? Usually because you have a balance due, your refund changed, the IRS has a question about your return, or it corrected something on your account.

How long do I have to respond to an IRS notice? Typically about 30 days, but the exact deadline is on the letter and depends on the notice type.

What happens if I ignore an IRS notice? Interest and penalties grow, the IRS proceeds with its proposed change or collection, and you can lose the right to dispute the amount.

Do I need to call the IRS? Usually not. Reply only if the notice instructs you to, and if you must call, use the number in the top right corner with your return and the letter in hand.

An IRS notice is a request to handle one specific thing, not a reason to dread the mailbox. Read it, confirm what it is and that it is genuine, mark the deadline, and respond the way it asks, or hand it to a professional if it is complex. Taken in order and on time, almost every IRS letter is far easier to resolve than it first looks.

IRS CP2000 Notice: What It Means And How To Respond?

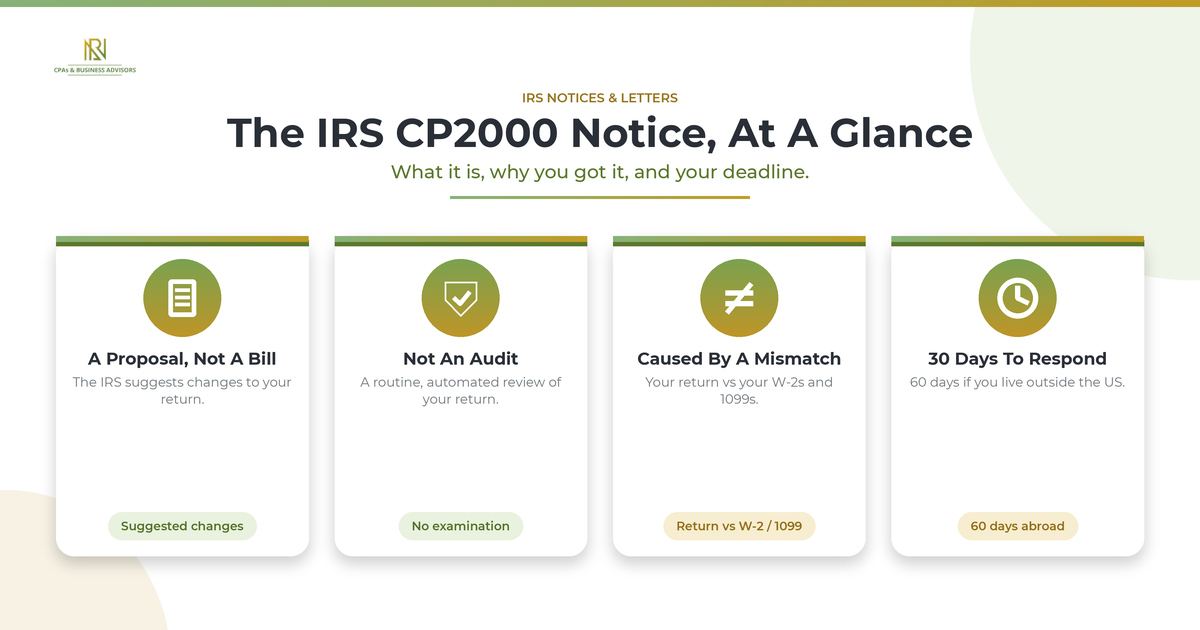

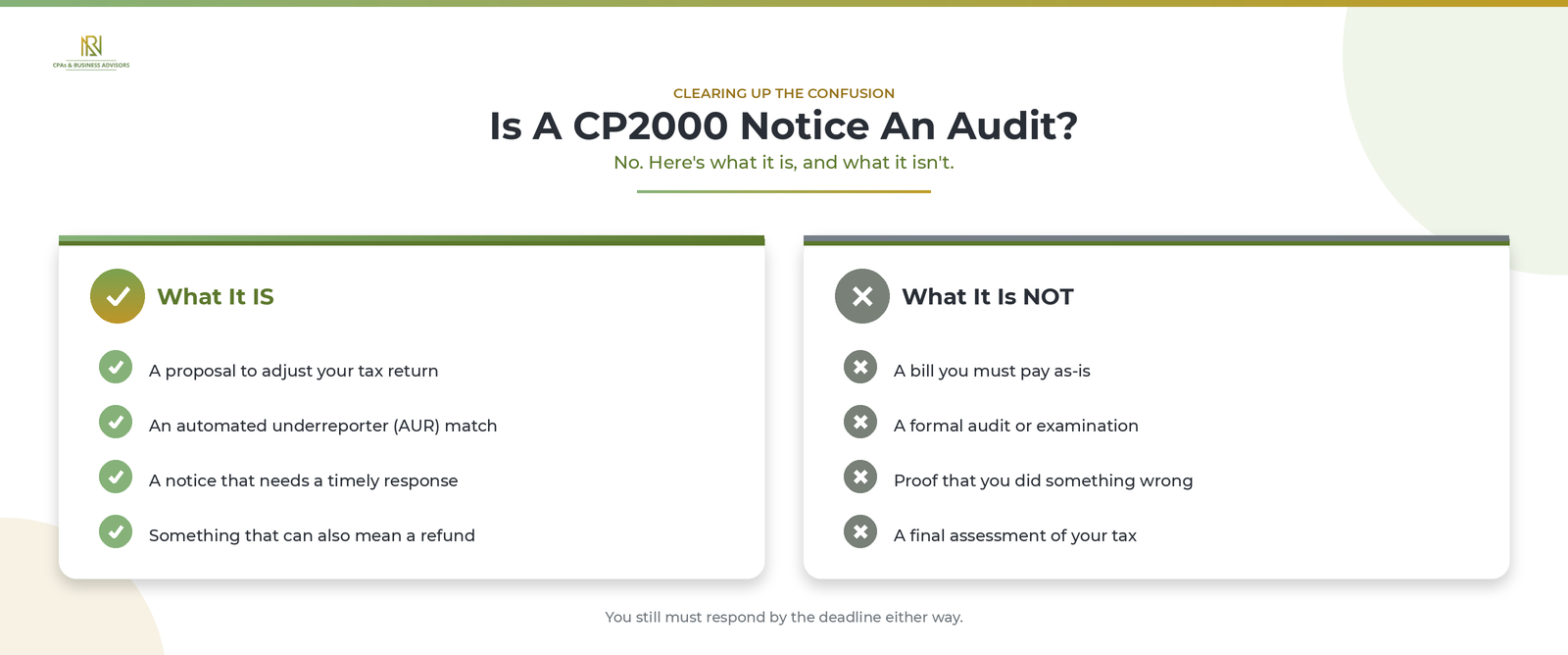

An IRS CP2000 notice is a letter proposing changes to your tax return because the income reported to the IRS by third parties, like employers or banks, does not match what you reported. According to the IRS, it is not a bill and not an audit. It is a proposal, and you generally have 30 days to respond.

What Is An IRS CP2000 Notice?

A CP2000 notice is the IRS's Notice of Underreported Income, a proposal to adjust your return when third-party records don't match what you filed. According to the IRS, its Automated Underreporter system compares the income, payments, credits, and deductions on your return against the Forms W-2, 1098, and 1099 that employers, banks, and other payers send in. When something doesn't line up, a tax examiner reviews it and the IRS issues a CP2000. The proposed change can mean you owe more, but it can also lower your tax or produce a refund.

Why Did You Get A CP2000 Notice?

You received a CP2000 because the IRS's records show income or other items that don't match your return. According to the IRS, the notice comes from its Automated Underreporter program, which flags discrepancies between your return and the information returns filed under your Social Security number. Common triggers are a missing 1099, a forgotten W-2, stock sales reported on a 1099-B, or interest and dividend income left off the return. It does not necessarily mean you did anything wrong. In practice, many CP2000 notices overstate the balance, because the automated match doesn't account for related deductions such as the cost basis of investments you sold.

Is A CP2000 Notice An Audit?

No. A CP2000 notice is not an audit, and it is not a bill. According to the IRS, the CP2000 is a proposal to adjust your income, payments, credits, or deductions, not a formal examination of your records. You still have to respond by the deadline, but receiving one does not mean you are being audited. Staying calm and replying on time is what keeps it from escalating.

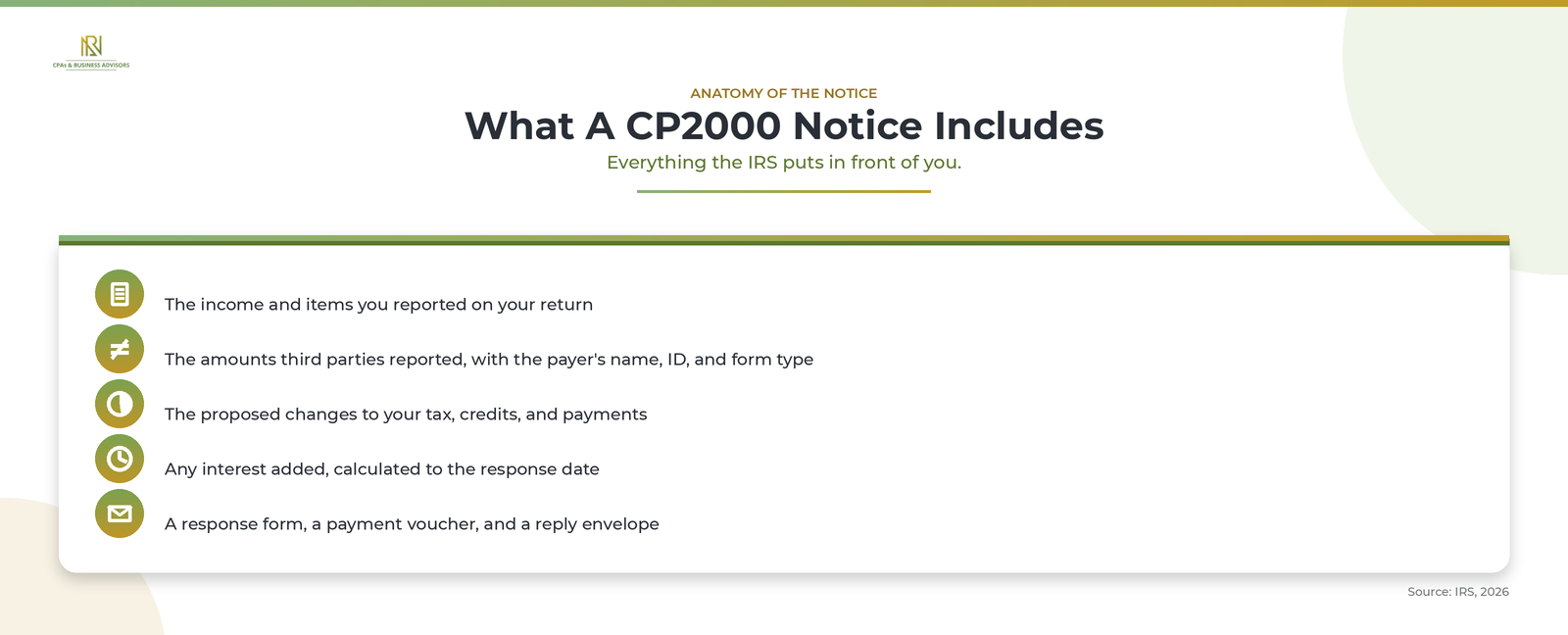

What Does A CP2000 Notice Include?

A CP2000 spells out exactly what the IRS believes is wrong and how to reply. According to the IRS, the notice shows:

- The amounts you reported on your original or amended return.

- The amounts third parties reported paying you.

- The payer's name, ID number, and the type of document filed, such as a W-2 or 1099.

- The proposed changes to your income, tax, credits, and payments, plus any interest.

- A response form, a payment voucher, and a reply envelope.

How To Respond To A CP2000 Notice

The first page summarizes the proposed change and gives a phone number to call, so that is where to start.

How To Respond To A CP2000 Notice

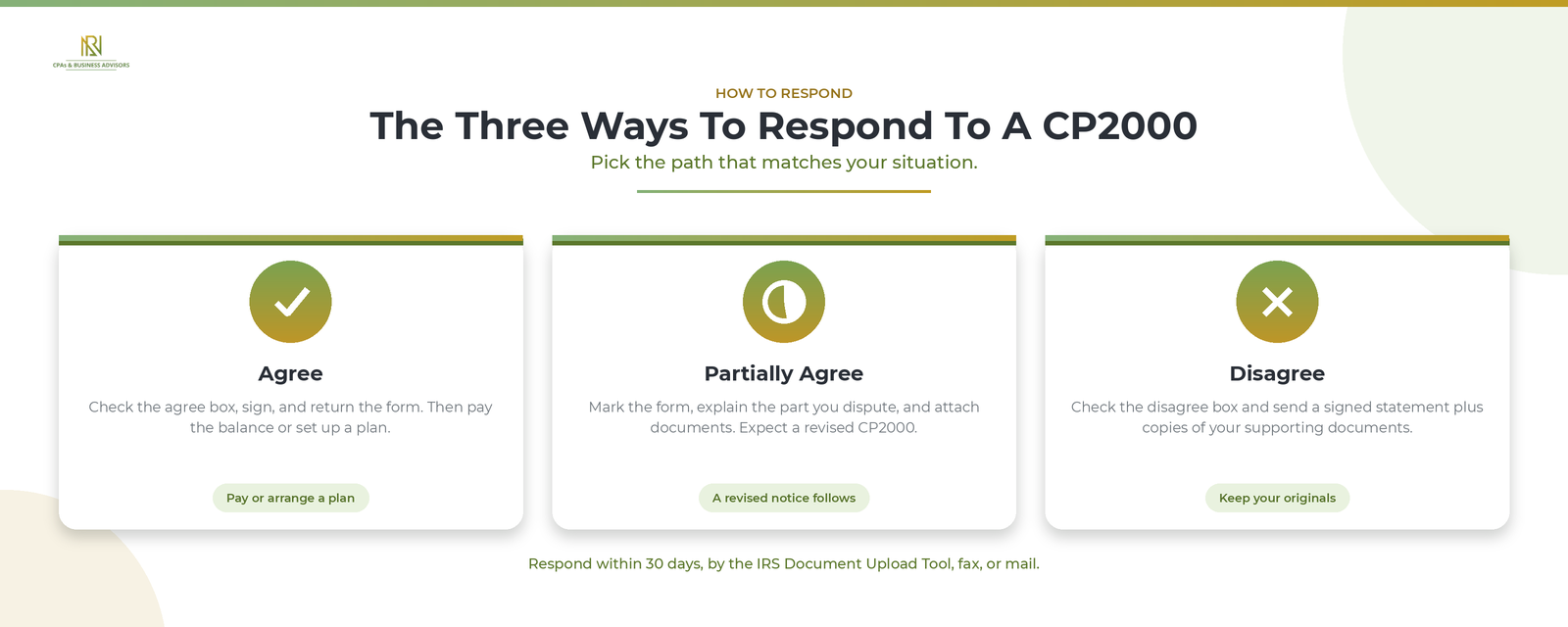

Respond by reviewing the proposed changes, deciding whether you agree, and returning the response form by the deadline. According to the IRS, you can reply through its Document Upload Tool, by fax, or by mail to the address on the notice. The basic steps are:

- Gather every W-2, 1098, and 1099 filed under your Social Security number for that year.

- Compare those forms against the return you filed to see whether the IRS is right.

- Recalculate the tax, factoring in any deductions the automated match missed.

- Decide whether you agree, partially agree, or disagree.

- Complete the response form, sign it (both spouses if you filed jointly), and return it by the due date.

If anything is unclear, call the phone number on the notice, and check your account about eight weeks after you reply to confirm the IRS has resolved it.

If You Agree With The Notice

If the IRS is right, agreeing is simple. According to the IRS, you check the box that says you agree, sign and date the response form, and return it. If you have the money, pay the proposed amount, because paying within 30 days stops additional interest and possibly penalties from building. You do not need to file an amended return unless you have other income, credits, or expenses to report.

If You Disagree With The Notice

If you think the notice is wrong, you must still respond by the deadline, with proof. According to the IRS, you check the box showing you disagree and include a signed statement explaining why, along with copies of any supporting documents, such as corrected forms or records of your cost basis. Send photocopies, never your originals, and keep everything for your records. A clear, documented explanation is what gets the IRS to accept your position and drop the proposed change.

If You Partially Agree

Sometimes part of the notice is right and part is wrong. In that case you mark the response form accordingly and explain, in writing, the specific items you dispute, with documentation for each. According to the IRS, if your explanation resolves some but not all of the discrepancies, it will send a revised CP2000 with a new calculation, which you then review and answer the same way.

Should You File An Amended Return?

Do not send a standalone amended return as your CP2000 response. A Form 1040-X goes to a different IRS unit and may not be matched to your notice, which can cost you the chance to contest penalties or appeal. According to the IRS, if you do have other income, credits, or expenses to report, you complete Form 1040-X, write "CP2000" across the top, and submit it together with your response form. And if you find the same mismatch on another year's return, file an amended return for that year to stop similar penalties from accruing.

What Is The Deadline To Respond?

You generally have 30 days from the date on the notice to respond, or 60 days if you live outside the United States. According to the IRS, that date is also where the interest calculation runs to, so replying and paying promptly limits what you owe. If you need more time, call the phone number on the notice before the deadline; the IRS usually grants a 30-day extension when you ask before it issues the next notice.

What Happens If You Ignore A CP2000 Notice?

If you don't respond, the IRS treats the proposed changes as correct and moves to assess the tax. According to the IRS, when it doesn't hear from you by the response date, it sends a Statutory Notice of Deficiency, also called a CP3219A or 90-day letter. That notice gives you the right to challenge the proposal in U.S. Tax Court, but once it is issued you can no longer settle the matter through the regular CP2000 process or appeal it inside the IRS. Ignoring the letter only adds interest and penalties and removes your easiest options, so responding on time matters.

Can You Contest The Penalties Or Appeal?

Yes. You can dispute the penalties and ask for an appeal, even if you agree with the additional tax. A CP2000 that proposes more tax often carries the 20% accuracy-related penalty, which may not even be shown on the notice. According to the IRS, you have the right to appeal a proposed adjustment through its Independent Office of Appeals, so it is smart to include an appeal request in your response in case the IRS disagrees and the deadline gets close. In your statement, lay out the facts and the reason the penalty shouldn't apply, such as reasonable cause or a first-time penalty abatement. If the IRS later proposes the same amount without addressing your reply, you can ask for CP2000 reconsideration.

What If You Agree But Can't Pay?

If you owe but can't pay it all at once, you still have options. According to the IRS, paying in full by the date on the notice stops additional interest and penalties, but if you can't, you can set up an installment agreement to spread the balance into monthly payments. If paying anything would create real hardship, an offer in compromise or the wider set of relief programs the IRS offers may fit. Request the plan with your response so the IRS knows you intend to pay.

Should You Handle A CP2000 Notice Yourself Or Hire A Professional?

You can handle a straightforward CP2000 yourself, especially when you simply forgot a form and agree with the change. Hiring help earns its cost when the amount is large, when you disagree and need to build a documented case, when stock sales or business income are involved, or when the notice may stem from identity theft. According to the IRS, if someone used your Social Security number, you send a completed Form 14039, Identity Theft Affidavit, with your reply. For complex or high-dollar notices, a firm offering IRS tax resolution services can prepare the response, contest penalties, and deal with the IRS for you. You can also authorize a tax professional to represent you by filing Form 2848.

How To Avoid CP2000 Notices In The Future

The best way to avoid another CP2000 is to make sure your return matches what the IRS already has. According to the IRS, you should wait until you have all your income documents before filing, check each W-2, 1098, and 1099 for accuracy, keep complete records, and report any income document that arrives after you file on an amended return. If you sold investments, confirm your broker reported your cost basis, since missing basis is a common reason the automated match overstates income.

Frequently Asked Questions

What happens if the IRS sends a CP2000 notice? The IRS is proposing a change to your return based on a mismatch with third-party records. You review it, then agree or disagree by the deadline.

Does a CP2000 trigger an audit? No. A CP2000 is not an audit, though it is handled formally and you must respond on time.

What does a CP2000 notice typically indicate? It usually means income reported under your Social Security number, such as a 1099 or W-2, was left off or misstated on your return.

How do I respond to a CP2000 letter? Compare the notice to your records, complete the response form showing whether you agree or disagree, attach a signed statement and documents if you disagree, and return it by fax, mail, or the IRS Document Upload Tool within 30 days.

How do I check the status of my CP2000? Call the phone number on the notice, or review your IRS account about eight weeks after you reply.

A CP2000 notice feels alarming, but it is a routine, fixable proposal, not a verdict. Read it closely, compare it against your own records, and respond by the deadline, agreeing if the IRS is right and documenting your case if it isn't. Handled on time, most CP2000 notices close quickly, often for less than the letter first proposed.