%201.avif)

.png)

.png)

IRS Offer In Compromise: Settle Tax Debt For Less

An Offer in Compromise (OIC) is an IRS program that allows you to settle your federal tax debt for less than the full amount you owe. According to the IRS, the agency considers your income, expenses, asset equity, and ability to pay when deciding whether to accept an offer. The IRS generally approves an OIC when the proposed amount represents the most the agency can reasonably expect to collect within the remaining time on your account.

An OIC is not automatic debt forgiveness. It is a formal agreement between you and the IRS in which you propose a specific dollar amount, and the IRS evaluates whether accepting that amount is in the government's best interest compared to pursuing the full balance through other collection methods. According to the IRS, three legal grounds can support an OIC: doubt as to liability (you dispute that you owe the amount), doubt as to collectibility (your assets and income are less than the full balance), and effective tax administration (you can pay but doing so would create an unfair economic hardship).

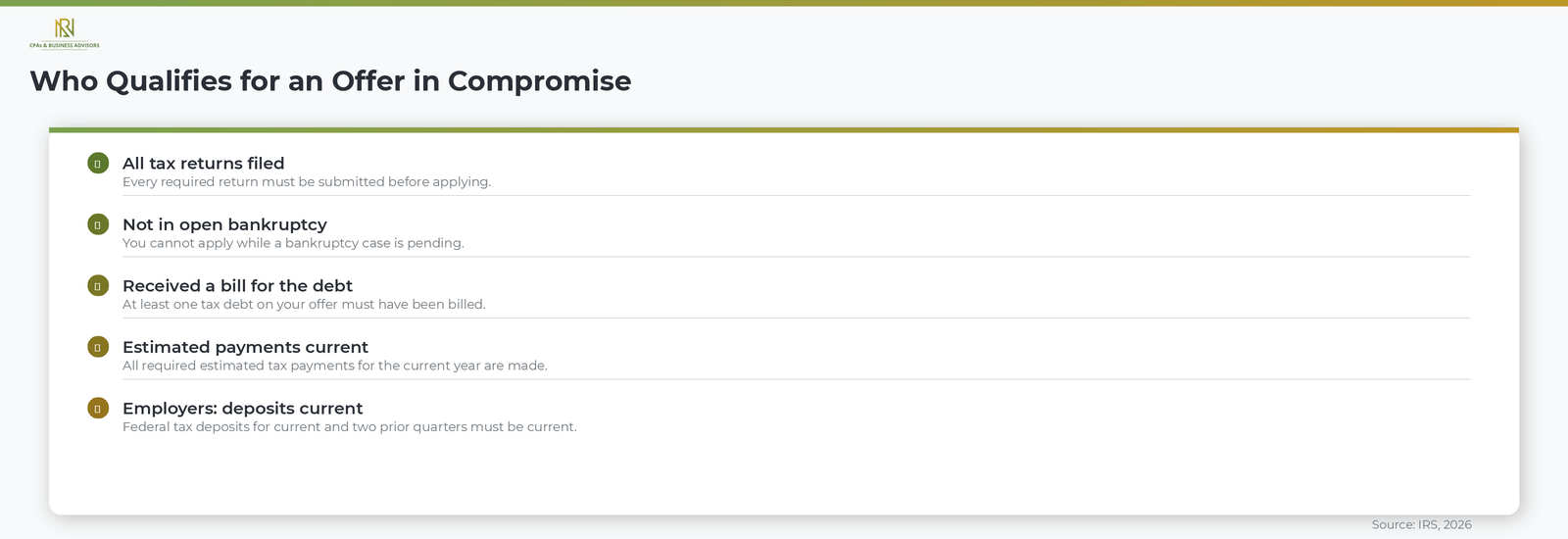

Who Qualifies For An Offer In Compromise

To be eligible for an OIC, you must have filed all required tax returns, made all required estimated tax payments for the current year, and not be in an open bankruptcy proceeding. According to the IRS, you must also have received a bill for at least one tax debt included in your offer. Business owners with employees must be current on federal tax deposits for the current quarter and the two preceding quarters.

Beyond the basic eligibility requirements, qualifying for an accepted OIC depends on your financial picture. The IRS uses national and local expense standards to determine what it considers reasonable monthly living costs. If your income minus allowable expenses leaves little or nothing for tax payments, and your assets have limited equity, you are more likely to have an offer accepted. The IRS provides a free Offer in Compromise Pre-Qualifier tool on its website that helps you check basic eligibility and estimate a preliminary offer amount before you invest time in the full application.

How The IRS Calculates Your Offer Amount

The IRS determines the minimum acceptable offer by calculating your Reasonable Collection Potential (RCP), which is the total of your net asset equity plus your future income the IRS expects to collect. According to the IRS, the RCP formula works as follows.

- Net asset equity. The fair market value of your assets (bank accounts, investments, real estate, vehicles) minus what you owe on them, with a quick-sale discount applied to certain assets.

- Future income. Your monthly disposable income (gross income minus allowable expenses) multiplied by a set number of months. For a lump-sum offer, the IRS multiplies by 12 months. For a periodic payment offer, the multiplier increases to 24 months.

Your offer must equal or exceed your RCP for the IRS to consider it. If the IRS determines your offer is too low, it will typically give you an opportunity to increase the amount before rejecting the application outright.

How To Apply For An Offer In Compromise

Applying for an OIC requires submitting Form 656 (Offer in Compromise), Form 433-A (OIC) for individuals or Form 433-B (OIC) for businesses, a $205 non-refundable application fee, and an initial payment. According to the IRS, the application fee and initial payment are waived for taxpayers who meet the low-income certification guidelines on Form 656.

The application process requires full financial disclosure, including detailed information about your employment, income, monthly expenses, bank accounts, investments, real estate, and vehicles. According to the IRS, you can now check eligibility, make payments, and file your OIC through your Individual Online Account on IRS.gov. You can also mail the completed package to the address listed on Form 656-B, the Offer in Compromise Booklet, which contains step-by-step instructions for the entire process.

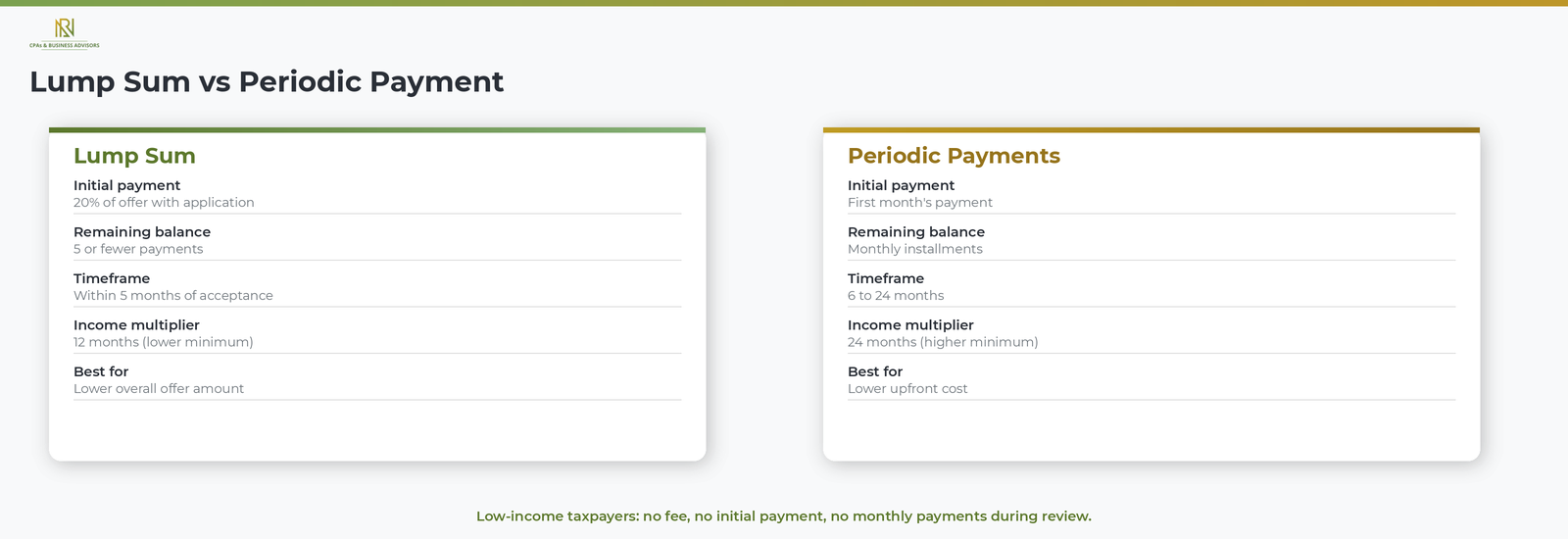

Lump Sum vs Periodic Payment Options

The IRS offers two payment structures for an accepted Offer in Compromise: a lump-sum payment or periodic payments spread over time.

- Lump sum. Submit 20 percent of your total offer amount with the application. If accepted, pay the remaining balance in five or fewer payments within five months.

- Periodic payments. Submit your first monthly payment with the application, then continue making monthly payments while the IRS evaluates your offer. If accepted, pay the remaining balance within 6 to 24 months according to your proposed terms.

According to the IRS, taxpayers who qualify for low-income certification do not need to submit an initial payment with either option and do not need to make monthly payments during the evaluation period. Choosing between lump sum and periodic payments affects how the IRS calculates your RCP. A lump-sum offer uses a 12-month future income multiplier, while a periodic payment offer uses 24 months, which means the minimum acceptable offer is typically higher under the periodic option.

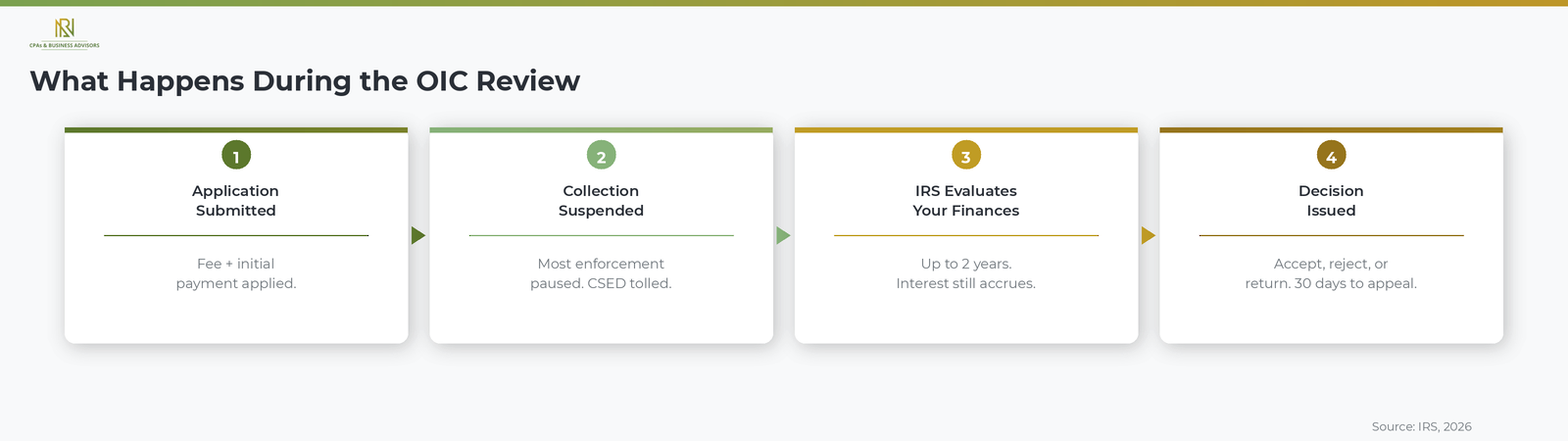

What Happens While The IRS Reviews Your Offer

The IRS can take up to two years to evaluate an OIC application, and several important things happen to your account during that period. According to the IRS, while your offer is under review, the agency suspends most collection activity on your account, including levies and garnishments. However, the IRS may still file a Notice of Federal Tax Lien, and interest continues to accrue on the unpaid balance.

One critical detail: submitting an OIC suspends the 10-year Collection Statute Expiration Date (CSED) while the IRS evaluates your offer, plus 30 additional days if the offer is rejected and through any appeal. This means the total time the IRS has to collect your debt extends beyond the standard 10 years. If your CSED is approaching expiration, this suspension is an important factor to weigh before applying.

According to the IRS, if the agency does not make a determination within two years of receiving your application (excluding any appeal period), your offer is automatically accepted.

What To Do If Your Offer Is Rejected

If the IRS rejects your OIC, you have 30 days to appeal the decision by filing Form 13711, Request for Appeal of Offer in Compromise. According to the IRS, the appeal is reviewed by the Independent Office of Appeals, which is separate from the unit that evaluated your original offer. If the appeal is unsuccessful, the IRS will resume collection activity on your account.

An OIC is not the only path to resolving tax debt you cannot pay in full. Installment agreements allow you to pay over time in monthly installments. Currently Not Collectible status pauses all collection if you cannot afford basic living expenses. Penalty abatement can reduce the penalties on your balance even if the underlying tax remains. Taxpayers evaluating which resolution path fits their situation can compare all four options in the IRS tax debt resolution overview.

Frequently Asked Questions About Offer In Compromise

How Much Will The IRS Settle For?

The IRS will generally accept the lowest amount it believes it can collect based on your Reasonable Collection Potential. According to the IRS, this calculation considers your net asset equity plus your projected disposable income over 12 or 24 months, depending on the payment option you choose. There is no fixed percentage or formula that applies to every taxpayer.

Can I Apply For An OIC On My Own?

Yes, individuals can apply without hiring a representative. According to the IRS, all required forms and instructions are available in Form 656-B, the Offer in Compromise Booklet, and the IRS Pre-Qualifier tool can help you estimate whether your offer is likely to be accepted. However, taxpayers with complex financial situations or large balances often benefit from working with a CPA, Enrolled Agent, or tax attorney.

What Happens If I Don't Follow The OIC Terms After Acceptance?

If you fail to comply with the terms of an accepted OIC, the IRS can terminate the agreement and reinstate the original tax debt minus any payments already made. According to the IRS, OIC terms require you to file all tax returns and pay all taxes on time for the five years following acceptance. Missing a filing or payment deadline during this period puts the entire agreement at risk.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

IRS Currently Not Collectible (CNC) Status: How It Works

Currently Not Collectible (CNC) is an IRS designation that temporarily pauses all collection activity on your account when you cannot afford to pay anything toward your tax debt without failing to cover basic living expenses. According to the IRS, CNC status means the agency has determined that requiring any payment would cause you financial hardship. While your account is in CNC, the IRS will not levy your wages, seize your bank accounts, or garnish your income.

CNC status does not eliminate your tax debt. According to the IRS, you still owe the full balance, and penalties and interest continue to accrue while your account is in this status. The IRS may also file a Notice of Federal Tax Lien to protect the government's interest in your property, and it will apply any future federal tax refunds to your outstanding balance. CNC is a temporary measure, not a permanent resolution, but it can provide critical breathing room for taxpayers in severe financial hardship.

Who Qualifies For CNC Status

You may qualify for CNC status if your monthly income, after allowable living expenses, leaves you unable to make even a small payment toward your tax debt. According to the IRS, the agency uses national and local cost-of-living standards to evaluate your expenses, including housing, utilities, food, transportation, health insurance, and out-of-pocket medical costs. If your allowable expenses equal or exceed your income, and you have no significant assets the IRS could use to satisfy the debt, CNC status is typically approved.

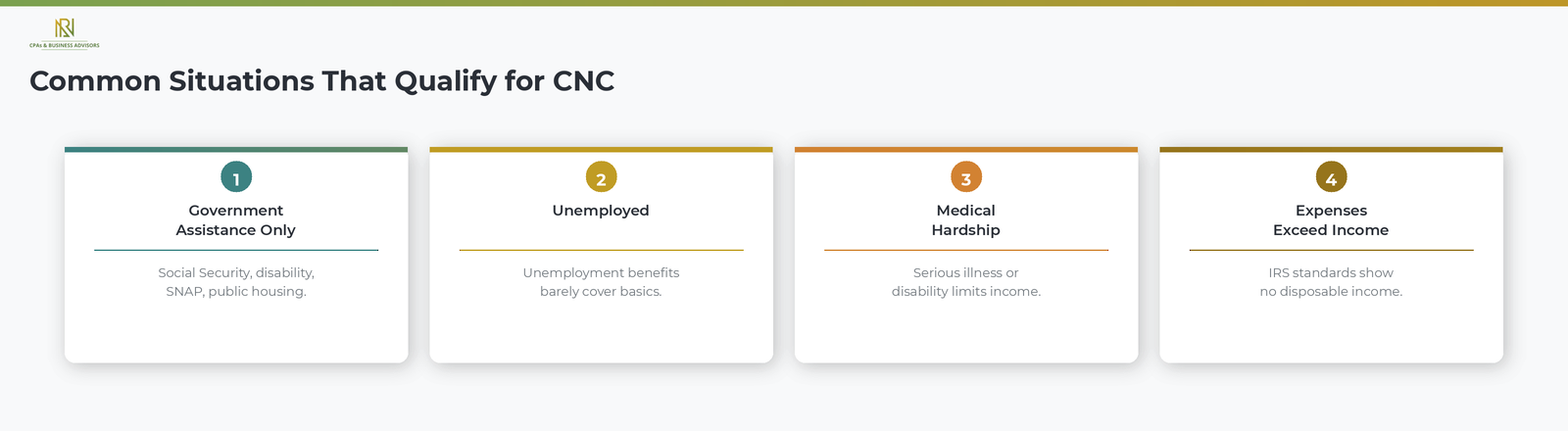

Common situations that support CNC eligibility include the following.

- Your only income is from government assistance. Social Security, disability benefits, unemployment compensation, or public assistance programs.

- You are unemployed with no other income. Especially when unemployment benefits barely cover basic expenses.

- You have a serious medical condition or disability. Particularly conditions that permanently limit your earning capacity.

- Your expenses exceed your income. Even after the IRS applies its own expense standards, there is no disposable income available for tax payments.

How To Request Currently Not Collectible Status

To request CNC status, call the IRS at 800-829-1040 or the phone number on your most recent notice and explain that you cannot afford to make any payments toward your tax debt. According to the IRS, the agent will ask you to provide financial information to verify your hardship. In most cases, you will need to complete Form 433-F, Collection Information Statement, which is a two-page form that documents your income, monthly expenses, debts, and assets.

For more complex financial situations, the IRS may require Form 433-A (for wage earners and self-employed individuals) or Form 433-B (for businesses). According to the IRS, you should be prepared to provide supporting documentation including pay stubs, bank statements, utility bills, rent or mortgage statements, and medical records if applicable. The IRS compares your reported expenses against its allowable expense standards to determine whether any payment is feasible.

When speaking with the IRS, be clear that you cannot afford any monthly payment, not just that you cannot pay the full amount. According to the IRS, if you can afford a small monthly payment, the agency will typically direct you toward an installment agreement or partial payment plan instead of CNC status.

What Happens While Your Account Is In CNC

While your account is in CNC status, the IRS suspends most active collection efforts but retains the right to take certain actions that protect the government's interest. According to the IRS, the following applies during CNC.

- No levies or garnishments. The IRS will not levy your wages, bank accounts, or other property.

- Tax refunds are still taken. The IRS will intercept and apply any federal tax refund you receive to the outstanding balance.

- A federal tax lien may be filed. According to the IRS, if you owe more than $10,000, the agency will generally file a Notice of Federal Tax Lien, which is a public record that can affect your credit and your ability to sell or refinance property.

- Penalties and interest continue. The balance grows while you are in CNC because the IRS does not stop charging penalties or interest during this period.

- Periodic reviews. The IRS may review your financial situation later and resume collection if your income improves.

When The IRS Can Remove CNC Status

The IRS can remove your account from CNC status and resume collection activity if your financial situation improves. According to the IRS, the agency assigns a closing code to each CNC account that corresponds to an income threshold. If your reported income exceeds that threshold, as indicated by W-2s, 1099s, or tax returns filed in subsequent years, the IRS may contact you to reassess your ability to pay.

If the IRS determines you can now afford payments, it will typically offer you the option to set up an installment agreement or pursue another resolution. If your income remains below the threshold indefinitely, your CNC status continues until the 10-year Collection Statute Expiration Date (CSED) expires, at which point the remaining debt is written off permanently.

How CNC Interacts With The 10 Year Collection Statute

One of the most important features of CNC status is that it does not pause or extend the IRS's 10-year collection clock. According to the IRS, the CSED continues to run while your account is in CNC. This means that if your income does not improve before the statute expires, the IRS loses its legal authority to collect the debt, and the balance is permanently written off.

This is a key distinction from other resolution options. Requesting an Offer in Compromise or an installment agreement suspends the CSED while the IRS evaluates your application, effectively giving the agency more time to collect. CNC status does not. For taxpayers with older tax debts and limited income prospects, CNC can be strategically advantageous because the clock keeps running in your favor.

However, CNC is not always the best long-term strategy. If your income is likely to improve, the IRS will remove you from CNC and resume collection, potentially with a larger balance due to accumulated penalties and interest. Taxpayers weighing CNC against other options like payment plans, Offers in Compromise, or penalty relief can compare all available paths in the IRS tax debt resolution overview.

Frequently Asked Questions About CNC Status

Does CNC Status Forgive My Tax Debt?

No, CNC status does not forgive or cancel your tax debt. According to the IRS, you still owe the full balance, and penalties and interest continue to accrue. The debt is only eliminated if the 10-year CSED expires while your account remains in CNC.

Will The IRS Take My Tax Refund While I Am In CNC?

Yes, the IRS will intercept and apply your federal tax refund to the outstanding balance even while your account is in CNC status. According to the IRS, refund offsets are one of the collection actions the agency continues during CNC.

How Long Can I Stay In CNC Status?

There is no fixed time limit on CNC status. According to the IRS, your account remains in CNC as long as your financial situation does not improve beyond the threshold the agency sets. The IRS may review your finances periodically, but CNC can last for years if your income remains at hardship levels.

IRS Penalty Abatement: How To Remove IRS Penalties

IRS penalty abatement is the removal or reduction of penalties the IRS has assessed against you for failing to file a return, failing to pay taxes owed, or failing to make required tax deposits on time. According to the IRS, abating a penalty does not eliminate the underlying tax you owe, but it removes the additional charges the IRS added on top of that balance. Because penalties often represent a significant portion of a taxpayer's total debt, a successful abatement can substantially reduce the amount you need to pay.

According to the IRS, when penalties are removed, the interest charged on those penalties is also automatically eliminated. However, interest on the unpaid tax itself continues to accrue until the balance is paid in full. Penalty abatement is available for individual taxpayers, businesses, and employers, though the eligibility criteria and process differ depending on the type of penalty and the relief program you qualify for.

Types Of IRS Penalty Relief

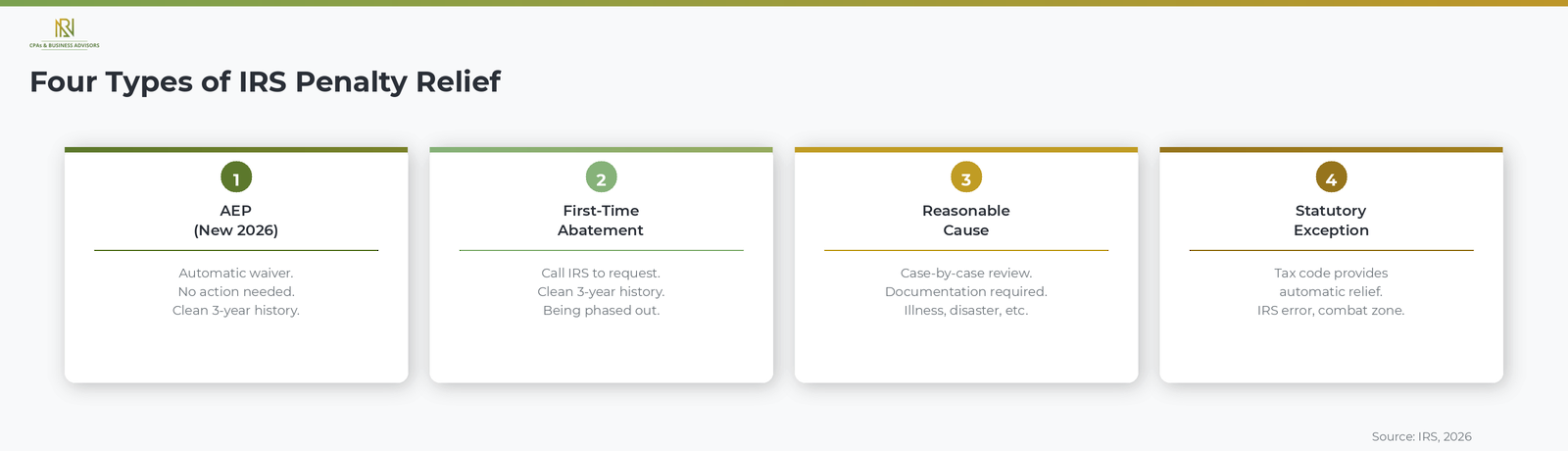

The IRS offers four main types of penalty relief: the Automatic Exemption from Penalty program, first-time penalty abatement, reasonable cause relief, and statutory exceptions. Each program has its own eligibility requirements and applies to different situations.

Automatic Exemption From Penalty Program

Starting in 2026, the IRS is phasing in the Automatic Exemption from Penalty (AEP) program, which automatically waives failure-to-file, failure-to-pay, and failure-to-deposit penalties for qualifying taxpayers without requiring any action on your part. According to the IRS, you qualify for AEP relief if you filed the same type of return on time for each of the previous three years and had no penalties assessed (other than estimated tax penalties) or any prior penalties were waived for reasonable cause. Unlike other programs, you do not need to call the IRS or submit paperwork. The IRS simply does not assess the penalty, and sends you a letter confirming the relief was applied.

According to the IRS, the AEP program applies to individual 1040 returns filed for tax year 2025 and later, and to certain quarterly business returns for tax year 2026 and later. The AEP program will fully replace the First-Time Penalty Abatement program for penalties related to returns originally due on or after January 1, 2027.

First-Time Penalty Abatement

First-Time Penalty Abatement (FTA) is an administrative waiver that removes failure-to-file, failure-to-pay, or failure-to-deposit penalties for taxpayers with a clean compliance history over the prior three years. According to the IRS, you qualify if you filed all required returns (or filed valid extensions), had no penalties assessed for the three preceding tax years, and have paid or arranged to pay any tax due. Unlike the AEP program, FTA is not automatic. You must contact the IRS by phone or submit Form 843, Claim for Refund and Request for Abatement, to request it.

According to the IRS, the FTA program is being phased out as the AEP program rolls in. FTA will be fully replaced for penalties associated with returns originally due on or after January 1, 2027. For penalties on returns due before that date, FTA remains available.

Reasonable Cause Relief

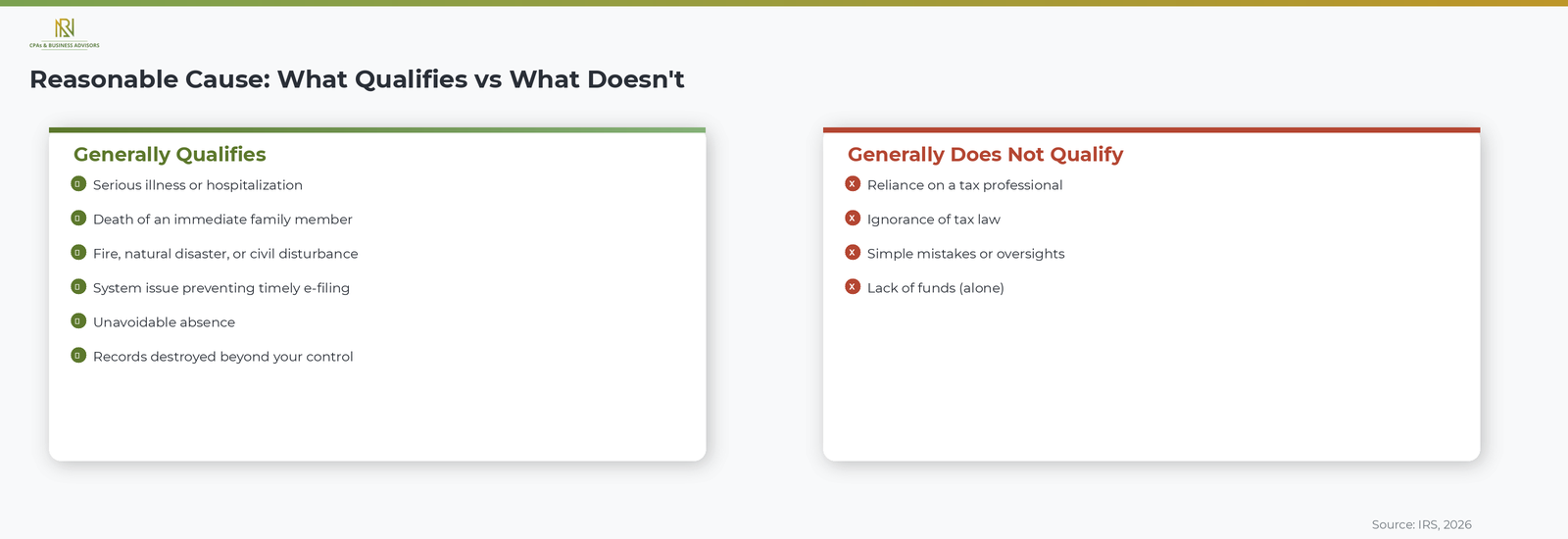

If you do not qualify for AEP or first-time abatement, the IRS can still remove penalties if you demonstrate that your failure to comply was due to reasonable cause and good faith. According to the IRS, reasonable cause is evaluated on a case-by-case basis considering all the facts and circumstances. Valid reasons include serious illness or death of an immediate family member, fires or natural disasters that destroyed records, system issues that prevented timely electronic filing or payment, and unavoidable absences.

According to the IRS, the following reasons generally do not qualify as reasonable cause on their own: reliance on a tax professional, ignorance of the law, simple mistakes or oversights, and lack of funds. However, lack of funds combined with other circumstances showing good-faith effort to comply may support a reasonable cause claim. You must provide supporting documentation such as medical records, court records, or correspondence that demonstrates the circumstances that prevented you from meeting your obligations.

Statutory Exceptions

In certain situations, the tax code itself provides an automatic exception that eliminates a penalty. According to the IRS, statutory exceptions include receiving incorrect written advice from the IRS that you reasonably relied on, being able to prove that your return or payment was mailed or e-filed before the deadline, being impacted by a federally declared disaster, and serving in a military combat zone.

Which Penalties Can Be Removed

The most common penalties eligible for abatement are the failure-to-file penalty, the failure-to-pay penalty, and the failure-to-deposit penalty. The failure-to-file penalty is 5 percent of the unpaid tax per month up to 25 percent. The failure-to-pay penalty is 0.5 percent per month up to 25 percent. Both penalties can be removed through AEP, FTA, or reasonable cause relief.

Accuracy-related penalties, which the IRS assesses when you underpay taxes due to negligence or a substantial understatement of income, can be removed through reasonable cause relief but are not eligible for AEP or first-time abatement. According to the IRS, the estimated tax penalty (for individuals who do not make sufficient quarterly payments) generally cannot be removed through any of the standard relief programs.

How To Request Penalty Abatement

The process for requesting penalty abatement depends on the type of relief you are seeking.

- AEP: No action required. The IRS applies the waiver automatically and sends you a confirmation letter.

- First-time abatement: Call the toll-free number on your IRS notice and request the abatement over the phone. If approved, the IRS sends a confirmation letter within 30 days.

- Reasonable cause: Call the IRS or submit Form 843 with a written explanation of your circumstances and supporting documentation. According to the IRS, phone requests are sometimes granted immediately, but complex cases may require a written submission.

- Statutory exception: Follow the instructions on your IRS notice or submit Form 843 with evidence of the exception (such as proof of timely mailing or a FEMA disaster declaration).

If you owe a balance beyond the penalties and cannot pay in full, you can set up an installment agreement to pay the remaining tax over time while your penalty abatement request is processed.

What To Do If Your Request Is Denied

If the IRS denies your penalty abatement request, you have 30 days from the date on the denial letter to appeal the decision to the IRS Independent Office of Appeals. According to the IRS, you must submit a written letter stating that you are appealing, include a copy of the denial notice, and provide any additional documentation or explanation you want the Appeals office to consider. Appeals officers review your case independently from the unit that issued the original denial.

If Appeals also denies your request, you can take the matter to court. According to the IRS, you can file a petition with the U.S. Tax Court before paying the disputed amount, or pay the penalty and file for a refund through the U.S. District Court or the U.S. Court of Federal Claims. Taxpayers who need to explore other ways to reduce their total IRS debt beyond penalty abatement, including Offers in Compromise and hardship status, can review the full range of IRS resolution options.

Frequently Asked Questions About Penalty Abatement

How Long Does It Take To Get Penalty Abatement?

It depends on the type of relief and how you request it. According to the IRS, first-time abatement requests made by phone can be approved immediately during the call. Written requests for reasonable cause relief may take several weeks to several months. The AEP program requires no wait time because the penalty is never assessed in the first place.

Can I Get Penalties Removed For Multiple Years?

First-time abatement and AEP apply to one tax period at a time. According to the IRS, you must have a clean three-year compliance history for each period you are requesting relief for. Reasonable cause relief can apply to multiple years if the same qualifying circumstance affected your ability to comply across those years, but you must demonstrate reasonable cause separately for each period.

Does Penalty Abatement Remove Interest Too?

Penalty abatement automatically removes the interest that was charged on the abated penalties, but it does not remove interest on the underlying tax. According to the IRS, interest on unpaid tax continues to accrue until the balance is paid in full, regardless of whether penalties are removed.