%201.avif)

.png)

.png)

Financial Consulting for Small Business Owners

Financial consulting for small business owners is a professional advisory service that helps business owners manage cash flow, plan taxes, build retirement savings, and make informed financial decisions at every stage of growth. Unlike basic bookkeeping, which records past transactions, financial consulting focuses on what comes next. A consultant analyzes your current financial position, identifies gaps, and creates a strategy that connects day-to-day operations to long-term business goals. According to a 2025 study by Equitable and SCORE, 83% of small business owners say it is important to consult with a financial professional for guidance on business decisions. This article covers what a financial consultant does, when to hire one, how consulting helps with cash flow and taxes, and how to find the right consultant for your business.

What Does a Financial Consultant Do for a Small Business?

A financial consultant for a small business analyzes your finances, identifies the highest-impact problems and opportunities, and creates actionable strategies to improve profitability, reduce risk, and support sustainable growth. Financial consultants work across several core areas: cash flow forecasting, budgeting, tax strategy, financial statement analysis, retirement planning, and succession planning. Each of these areas addresses a specific need that most small business owners face as their company grows past the startup phase.

Cash flow forecasting allows business owners to project future income and expenses so they can prepare for slow months before they arrive. Budgeting creates a spending framework that aligns with actual business goals rather than reactive cost-cutting. Tax strategy ensures you are not overpaying the IRS due to poor entity structure or missed deductions. Financial statement analysis gives you a clear view of profitability, debt levels, and operational efficiency. Retirement planning builds personal wealth alongside business wealth, and succession planning prepares the business for a future ownership transition.

A good business consulting engagement does not stop at delivering a report. The consultant works alongside you to put the strategy into action, train your team on the systems, and measure whether the changes produce the expected results. According to industry research, well-structured small business consulting engagements typically produce a 3 to 10 times return on the fees paid within the first year. That return shows up in higher revenue, lower costs, stronger cash flow, or a combination of all three.

How Does Financial Consulting Differ from Accounting?

Financial consulting differs from accounting in its focus, time orientation, and deliverables. Accounting records what already happened. Financial consulting uses that historical data to guide what should happen next. Both are necessary, but they serve different purposes, and many business owners delay getting consulting help because they assume their accountant already covers it.

An accountant prepares your books, files your tax returns, and makes sure your records are accurate and compliant. A financial consultant takes those accurate records and turns them into forward-looking strategies: cash flow projections, growth scenarios, tax-saving structures, and retirement timelines. A bookkeeper enters the transactions. An accountant verifies and reports them. A consultant interprets them and tells you what to do about them.

The difference matters most as the business grows. A company with $500,000 in revenue can often get by with a bookkeeper and a CPA who files taxes once a year. A company approaching $1 million or more typically needs forward-looking financial guidance that a standard accounting engagement does not provide. Accurate financial statements form the foundation, but the strategy built on top of those statements is where consulting adds value.

RolePrimary FocusTime OrientationTypical DeliverableBookkeeperRecording transactionsPast (what happened)Clean books, reconciled accountsAccountant / CPACompliance and reportingPast and presentTax returns, financial statementsFinancial ConsultantStrategy and decision supportPresent and futureCash flow forecasts, growth plans, tax strategiesVirtual CFOOngoing financial leadershipFuture-focusedBudgets, KPI dashboards, board-level reporting

Sources: Bureau of Labor Statistics Occupational Outlook Handbook; American Institute of CPAs (AICPA) professional role definitions; Business Research Insights virtual CFO market report, 2024.

What Are the Signs a Small Business Needs Financial Consulting?

The signs a small business needs financial consulting include persistent cash flow gaps, unexpected tax bills, difficulty making confident financial decisions, stalled growth, no retirement savings plan, and the absence of a succession strategy. These signs often appear gradually, and many owners do not recognize them until the problem has already compounded.

The following indicators suggest that outside financial guidance would benefit the business:

- You consistently run short on cash, even when sales look healthy on paper.

- Your tax bill surprises you every year because you file reactively instead of planning throughout the year.

- You make major financial decisions based on gut feeling rather than data-driven projections.

- Your business has grown, but your profit margin has not grown with it.

- You have no formal retirement savings plan outside the business itself.

- You have not created a plan for what happens to the business if you become unable to run it.

According to research compiled from industry surveys, 73% of small business owners report feeling "not completely prepared" for the financial demands of their business. That lack of preparation creates blind spots. Blind spots around cash flow problems are especially dangerous because cash shortages can force a profitable business to close. For owners across South Florida and nationwide, the earlier these signs are addressed, the less costly the correction becomes.

When Should a Small Business Owner Hire a Financial Consultant?

A small business owner should hire a financial consultant when the business reaches a level of complexity that exceeds the owner's financial expertise, when a major decision is on the horizon, or when an ongoing financial problem has not responded to internal effort. The timing depends on the business stage, but there are clear inflection points where professional financial guidance produces the highest return.

At the startup stage, a consultant helps you choose the right entity structure, set up accounting systems, and create a realistic budget. Entity selection alone can produce thousands of dollars in annual tax savings. At the growth stage, a consultant helps you manage cash flow during expansion, evaluate whether you can afford to hire, and build startup advisory frameworks that keep finances stable as revenue scales.

At the pre-exit stage, a consultant helps you plan for retirement, value the business, and structure the transition. According to the 2025 Equitable and SCORE study, 59% of small business owners find it difficult to completely retire, even though 42% started their business specifically to fund their retirement. That disconnect often traces back to delayed financial planning. Owners who wait until they are ready to sell discover that the business was never structured for a clean exit. The cost of delayed consulting compounds over time, just like the financial problems it was meant to prevent.

How Does a Financial Consultant Help with Cash Flow?

A financial consultant helps with cash flow by building cash flow forecasts, analyzing buffer days, optimizing receivables and payables timing, and identifying the root causes of cash shortages before they become emergencies. Cash flow consulting is one of the most valuable forms of financial consulting because cash problems are the leading cause of small business failure in the United States.

According to a widely cited U.S. Bank study, 82% of small businesses that fail do so because of poor cash flow management. Cash flow failure is not the same as unprofitability. A business can show a profit on the income statement and still run out of money because the timing of cash inflows does not match the timing of cash outflows. Payroll, rent, and supplier invoices come due on fixed schedules. Revenue arrives on its own schedule, often weeks or months after the work is completed.

JPMorgan Chase Institute research on 597,000 small businesses found that the median small business holds only 27 cash buffer days. Cash buffer days measure how long a business could survive with zero incoming revenue. Twenty-seven days means the median business is less than one month away from a cash crisis at any given time. Roughly 25% of small businesses operate with 13 or fewer buffer days. A virtual CFO or financial consultant monitors these metrics in real time and builds a plan to extend the cash runway before a gap appears.

Cash flow consulting also reduces the downstream problems that cash shortages create. According to U.S. Bureau of Labor Statistics data, approximately 49.4% of new businesses fail within five years and 65.3% fail within ten years. Cash flow mismanagement contributes to a disproportionate share of those closures. The businesses that survive typically have systems in place to forecast cash needs, collect receivables faster, and maintain reserves for slow periods. These are the exact systems a financial consultant builds.

Can a Financial Consultant Help with Tax Planning?

Yes, a financial consultant can help with tax planning by developing proactive, year-round strategies that reduce your tax liability, improve compliance, and align your tax position with your broader financial goals. Tax planning from a consulting perspective is different from tax preparation. Preparation happens after the tax year ends. Planning happens throughout the year, before the decisions that affect your tax bill are made.

Proactive tax planning covers several areas. Entity structure optimization determines whether your business should operate as a sole proprietorship, LLC, S-corporation, or C-corporation based on income level, self-employment tax exposure, and long-term goals. Quarterly estimated tax management prevents the underpayment penalties that catch many business owners off guard. Deduction and credit identification captures savings that reactive filers miss because they do not plan for them in advance.

One area where consulting and tax planning increasingly overlap is retirement plan design. Under the SECURE 2.0 Act provisions, small businesses with up to 50 employees can receive up to $5,000 in federal tax credits per year for the first three years of starting a new retirement plan. That credit directly offsets the administrative cost of offering a 401(k), SEP IRA, or SIMPLE IRA. A financial consultant identifies these opportunities and structures them so the business captures the maximum benefit. Owners interested in year-round strategies can explore additional proactive tax planning approaches that reduce surprises at filing time.

How Does Financial Consulting Support Business Growth and Retirement?

Financial consulting supports business growth and retirement by connecting short-term operational decisions to long-term wealth-building goals, including financial statement analysis for expansion decisions, retirement plan design, and succession planning for eventual ownership transition. Growth and retirement are not separate conversations. They are two sides of the same financial plan, and consulting bridges them.

On the growth side, a financial consultant helps you evaluate expansion opportunities using data rather than instinct. That evaluation includes analyzing whether the current profit margin supports the cost of a new location, a new hire, or a new product line. It includes building financial projections that show the break-even timeline and the capital required. According to the 2026 Federal Reserve Small Business Credit Survey, 60% of small businesses that applied for financing did so to meet operating expenses, and 46% did so to pursue expansion. The businesses that secured financing and used it effectively were typically the ones with organized financial records and clear projections, both deliverables of strategic planning and consulting work.

On the retirement side, the data is striking. According to the 2025 Equitable and SCORE study, small business owners who work with a financial professional expect to retire at age 63. Owners without a financial professional expect to retire at age 70. That 7-year gap reflects the compounding effect of early planning: earlier retirement contributions grow longer, tax-advantaged structures capture more savings, and succession planning creates a viable exit path. A separate SCORE survey found that 34% of small business owners have no retirement savings plan outside their company. Relying entirely on the business sale to fund retirement is risky. According to the Exit Planning Institute, only 20 to 30% of businesses listed for sale actually sell.

A 2026 Chase survey of approximately 1,000 small business owners confirmed that nearly half plan to retire within 10 years, yet few have a fully developed succession plan. In Miami's competitive entrepreneurial market and nationally, that planning gap represents one of the highest-value opportunities for financial consulting. The consultant helps the owner build a retirement savings vehicle, value the business accurately, and structure the business formation and ownership documents so the transition can happen on the owner's timeline.

Financial consulting touches each of the following areas across the growth-to-exit continuum:

- Cash flow forecasting and budget development for expansion readiness

- Financial statement analysis to evaluate profitability and debt capacity

- Retirement plan selection and tax credit optimization under SECURE 2.0

- Succession planning, including business valuation and buy-sell agreements

- Tax structure optimization to minimize the tax burden at sale or transfer

- Ongoing financial oversight through fractional CFO or advisory retainers

What's the Best Way to Find a Good Financial Consultant?

The best way to find a good financial consultant is to evaluate their credentials, verify their experience with businesses similar to yours, assess their communication style, and confirm that their fee structure is transparent and tied to clear deliverables. The right consultant produces measurable results. The wrong one wastes time and money.

Start with credentials. A Certified Public Accountant (CPA) license demonstrates competency in tax and accounting. An Enrolled Agent (EA) designation means the professional is authorized by the IRS to represent taxpayers. A Certified Financial Planner (CFP) certification signals expertise in investment and retirement planning. The strongest consultants for small business owners often hold a CPA or EA alongside practical business advisory experience, because the work requires both technical tax knowledge and strategic business insight.

Next, verify experience. Ask how many small business clients the consultant works with, what industries they serve, and whether they have handled situations similar to yours. A consultant who has helped 50 growing businesses manage cash flow and plan for exit is more valuable than one who primarily serves individuals. According to a 2025 industry survey, 64% of small business owners say trust in the consultant is the single most important factor in choosing who to work with, ranking above price, brand, or specific expertise. Trust builds through transparent communication, consistent follow-through, and honest advice, even when the honest answer is not the one you want to hear.

Fee transparency matters. Ask whether the consultant charges hourly, by project, or on a monthly retainer. Each structure fits different needs. Retainers work well for ongoing advisory relationships. Project-based fees work well for defined engagements like a cash flow overhaul or a tax structure review. Look for a consultant who explains exactly what the engagement covers and what deliverables you will receive. A strong financial and operational consulting relationship starts with clarity about scope, timeline, and expected outcomes.

What Is a Red Flag for a Financial Advisor?

A red flag for a financial advisor is any behavior that suggests a lack of transparency, credentials, or fiduciary responsibility. Specific red flags include guaranteeing specific financial outcomes, refusing to explain fees in detail, lacking verifiable professional certifications, pressuring you to make quick decisions, and being unwilling to provide references from current or past clients. A qualified consultant earns your trust through competency and honesty. Any professional who shortcuts that process deserves skepticism.

Is It Worth Seeing an Independent Financial Advisor?

Yes, seeing an independent financial advisor is worth it for most small business owners because independent advisors typically offer objective guidance free from the product-sales incentives that can affect advisors at large financial institutions. Independent advisors and boutique firms often specialize in small business clients, which means they understand the specific challenges of cash flow, entity structure, and retirement planning that larger firms may treat as secondary.

The financial advisory profession is growing because demand for personalized guidance continues to increase. According to the Bureau of Labor Statistics, the personal financial advisor market is projected to see 13% job growth between 2022 and 2032, far outpacing the national average of 3.71%. That growth reflects the reality that more business owners are seeking financial metrics support and strategic advisory as businesses become more complex. The virtual CFO segment alone is projected to grow from $3.91 billion in 2024 to $8.17 billion by 2032, according to Business Research Insights.

For small business owners, the most productive relationship is often with a CPA-led advisory firm that combines tax expertise with business strategy. This eliminates the coordination friction between a separate accountant, a separate financial planner, and a separate business consultant. One firm that understands both the tax code and the business model can deliver a more cohesive strategy than three separate professionals working in isolation.

Frequently Asked Questions

What Are the Alternatives to Using an Advisor?

The alternatives to using a paid advisor include free resources from the Small Business Administration (SBA), SCORE mentorship programs, Small Business Development Centers (SBDCs), and self-directed financial management using accounting software. These resources provide foundational support, but they typically do not replace the depth of customized strategy that a dedicated consulting services engagement delivers. Many business owners start with free resources and graduate to a paid consultant as the business grows and the financial decisions become more complex.

How Do I Know If My Financial Advisor Is Honest?

You know your financial advisor is honest when they explain their fees clearly, acknowledge the limits of their expertise, provide advice based on your data rather than generic templates, and recommend against unnecessary services. Honest advisors hold verifiable credentials, respond to questions directly, and do not promise outcomes they cannot control. Ask for references and verify their license through the CPA board or the IRS Enrolled Agent database.

How Long Does the Average Client Stay with a Financial Advisor?

The average client stays with a financial advisor for 5 to 10 years, according to financial industry surveys. The relationship tends to last longer when the advisor provides ongoing value rather than a one-time engagement. Business owners who work with an advisor on a retainer or fractional CFO basis typically maintain the relationship through multiple business cycles because the advisor's knowledge of the business compounds over time.

What Happens When You Stop Using a Financial Advisor?

When you stop using a financial advisor, the ongoing monitoring, forecasting, and strategy adjustments they provided also stop. Tax planning reverts to reactive filing. Cash flow projections stop updating. Retirement savings contributions may slow or stall. The financial impact depends on how much of the advisor's work was automated into systems the business can maintain on its own.

How Much Does Financial Consulting Cost for Small Businesses?

Financial consulting for small businesses typically costs $150 to $400 per hour for hourly engagements, $3,000 to $15,000 per month for ongoing retainers, and $5,000 to $50,000 for project-based work, according to 2025 consulting industry pricing surveys. The cost depends on the consultant's experience, the scope of the engagement, and the complexity of the business. The more productive way to evaluate cost is return on investment rather than the headline fee.

What Should You Look for in a Small Business Financial Consultant?

You should look for a small business financial consultant who holds professional certifications (CPA, EA, or CFP), has direct experience with businesses similar to yours in size and industry, communicates in clear language rather than jargon, charges transparently, and measures success through defined outcomes. Prioritize consultants who ask detailed questions about your business before proposing a solution, because the diagnosis must come before the prescription.

Putting It All Together

Financial consulting for small business owners is a strategic investment that strengthens cash flow, reduces tax liability, builds retirement savings, and prepares the business for long-term growth or a successful exit. The data is consistent: business owners who work with financial professionals make better decisions, retire earlier, and build more resilient companies than those who go it alone. The 7-year retirement gap between advised and unadvised owners, the 82% cash flow failure rate, and the planning gaps identified in the 2026 Federal Reserve and Chase surveys all point to the same conclusion. Professional financial guidance pays for itself.

If you are a small business owner looking for clear, practical financial consulting that connects your day-to-day operations to your long-term goals, we would welcome the conversation. At NR CPAs & Business Advisors, we work with entrepreneurs and growing businesses to bring structure, clarity, and measurable improvement to their financial decisions.

Reach out to our team at (954) 231-6613 to get started.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

Financial Consulting for Small Business Owners

Financial consulting for small business owners is a professional advisory service that helps business owners manage cash flow, plan taxes, build retirement savings, and make informed financial decisions at every stage of growth. Unlike basic bookkeeping, which records past transactions, financial consulting focuses on what comes next. A consultant analyzes your current financial position, identifies gaps, and creates a strategy that connects day-to-day operations to long-term business goals. According to a 2025 study by Equitable and SCORE, 83% of small business owners say it is important to consult with a financial professional for guidance on business decisions. This article covers what a financial consultant does, when to hire one, how consulting helps with cash flow and taxes, and how to find the right consultant for your business.

What Does a Financial Consultant Do for a Small Business?

A financial consultant for a small business analyzes your finances, identifies the highest-impact problems and opportunities, and creates actionable strategies to improve profitability, reduce risk, and support sustainable growth. Financial consultants work across several core areas: cash flow forecasting, budgeting, tax strategy, financial statement analysis, retirement planning, and succession planning. Each of these areas addresses a specific need that most small business owners face as their company grows past the startup phase.

Cash flow forecasting allows business owners to project future income and expenses so they can prepare for slow months before they arrive. Budgeting creates a spending framework that aligns with actual business goals rather than reactive cost-cutting. Tax strategy ensures you are not overpaying the IRS due to poor entity structure or missed deductions. Financial statement analysis gives you a clear view of profitability, debt levels, and operational efficiency. Retirement planning builds personal wealth alongside business wealth, and succession planning prepares the business for a future ownership transition.

A good business consulting engagement does not stop at delivering a report. The consultant works alongside you to put the strategy into action, train your team on the systems, and measure whether the changes produce the expected results. According to industry research, well-structured small business consulting engagements typically produce a 3 to 10 times return on the fees paid within the first year. That return shows up in higher revenue, lower costs, stronger cash flow, or a combination of all three.

How Does Financial Consulting Differ from Accounting?

Financial consulting differs from accounting in its focus, time orientation, and deliverables. Accounting records what already happened. Financial consulting uses that historical data to guide what should happen next. Both are necessary, but they serve different purposes, and many business owners delay getting consulting help because they assume their accountant already covers it.

An accountant prepares your books, files your tax returns, and makes sure your records are accurate and compliant. A financial consultant takes those accurate records and turns them into forward-looking strategies: cash flow projections, growth scenarios, tax-saving structures, and retirement timelines. A bookkeeper enters the transactions. An accountant verifies and reports them. A consultant interprets them and tells you what to do about them.

The difference matters most as the business grows. A company with $500,000 in revenue can often get by with a bookkeeper and a CPA who files taxes once a year. A company approaching $1 million or more typically needs forward-looking financial guidance that a standard accounting engagement does not provide. Accurate financial statements form the foundation, but the strategy built on top of those statements is where consulting adds value.

RolePrimary FocusTime OrientationTypical DeliverableBookkeeperRecording transactionsPast (what happened)Clean books, reconciled accountsAccountant / CPACompliance and reportingPast and presentTax returns, financial statementsFinancial ConsultantStrategy and decision supportPresent and futureCash flow forecasts, growth plans, tax strategiesVirtual CFOOngoing financial leadershipFuture-focusedBudgets, KPI dashboards, board-level reporting

Sources: Bureau of Labor Statistics Occupational Outlook Handbook; American Institute of CPAs (AICPA) professional role definitions; Business Research Insights virtual CFO market report, 2024.

What Are the Signs a Small Business Needs Financial Consulting?

The signs a small business needs financial consulting include persistent cash flow gaps, unexpected tax bills, difficulty making confident financial decisions, stalled growth, no retirement savings plan, and the absence of a succession strategy. These signs often appear gradually, and many owners do not recognize them until the problem has already compounded.

The following indicators suggest that outside financial guidance would benefit the business:

- You consistently run short on cash, even when sales look healthy on paper.

- Your tax bill surprises you every year because you file reactively instead of planning throughout the year.

- You make major financial decisions based on gut feeling rather than data-driven projections.

- Your business has grown, but your profit margin has not grown with it.

- You have no formal retirement savings plan outside the business itself.

- You have not created a plan for what happens to the business if you become unable to run it.

According to research compiled from industry surveys, 73% of small business owners report feeling "not completely prepared" for the financial demands of their business. That lack of preparation creates blind spots. Blind spots around cash flow problems are especially dangerous because cash shortages can force a profitable business to close. For owners across South Florida and nationwide, the earlier these signs are addressed, the less costly the correction becomes.

When Should a Small Business Owner Hire a Financial Consultant?

A small business owner should hire a financial consultant when the business reaches a level of complexity that exceeds the owner's financial expertise, when a major decision is on the horizon, or when an ongoing financial problem has not responded to internal effort. The timing depends on the business stage, but there are clear inflection points where professional financial guidance produces the highest return.

At the startup stage, a consultant helps you choose the right entity structure, set up accounting systems, and create a realistic budget. Entity selection alone can produce thousands of dollars in annual tax savings. At the growth stage, a consultant helps you manage cash flow during expansion, evaluate whether you can afford to hire, and build startup advisory frameworks that keep finances stable as revenue scales.

At the pre-exit stage, a consultant helps you plan for retirement, value the business, and structure the transition. According to the 2025 Equitable and SCORE study, 59% of small business owners find it difficult to completely retire, even though 42% started their business specifically to fund their retirement. That disconnect often traces back to delayed financial planning. Owners who wait until they are ready to sell discover that the business was never structured for a clean exit. The cost of delayed consulting compounds over time, just like the financial problems it was meant to prevent.

How Does a Financial Consultant Help with Cash Flow?

A financial consultant helps with cash flow by building cash flow forecasts, analyzing buffer days, optimizing receivables and payables timing, and identifying the root causes of cash shortages before they become emergencies. Cash flow consulting is one of the most valuable forms of financial consulting because cash problems are the leading cause of small business failure in the United States.

According to a widely cited U.S. Bank study, 82% of small businesses that fail do so because of poor cash flow management. Cash flow failure is not the same as unprofitability. A business can show a profit on the income statement and still run out of money because the timing of cash inflows does not match the timing of cash outflows. Payroll, rent, and supplier invoices come due on fixed schedules. Revenue arrives on its own schedule, often weeks or months after the work is completed.

JPMorgan Chase Institute research on 597,000 small businesses found that the median small business holds only 27 cash buffer days. Cash buffer days measure how long a business could survive with zero incoming revenue. Twenty-seven days means the median business is less than one month away from a cash crisis at any given time. Roughly 25% of small businesses operate with 13 or fewer buffer days. A virtual CFO or financial consultant monitors these metrics in real time and builds a plan to extend the cash runway before a gap appears.

Cash flow consulting also reduces the downstream problems that cash shortages create. According to U.S. Bureau of Labor Statistics data, approximately 49.4% of new businesses fail within five years and 65.3% fail within ten years. Cash flow mismanagement contributes to a disproportionate share of those closures. The businesses that survive typically have systems in place to forecast cash needs, collect receivables faster, and maintain reserves for slow periods. These are the exact systems a financial consultant builds.

Can a Financial Consultant Help with Tax Planning?

Yes, a financial consultant can help with tax planning by developing proactive, year-round strategies that reduce your tax liability, improve compliance, and align your tax position with your broader financial goals. Tax planning from a consulting perspective is different from tax preparation. Preparation happens after the tax year ends. Planning happens throughout the year, before the decisions that affect your tax bill are made.

Proactive tax planning covers several areas. Entity structure optimization determines whether your business should operate as a sole proprietorship, LLC, S-corporation, or C-corporation based on income level, self-employment tax exposure, and long-term goals. Quarterly estimated tax management prevents the underpayment penalties that catch many business owners off guard. Deduction and credit identification captures savings that reactive filers miss because they do not plan for them in advance.

One area where consulting and tax planning increasingly overlap is retirement plan design. Under the SECURE 2.0 Act provisions, small businesses with up to 50 employees can receive up to $5,000 in federal tax credits per year for the first three years of starting a new retirement plan. That credit directly offsets the administrative cost of offering a 401(k), SEP IRA, or SIMPLE IRA. A financial consultant identifies these opportunities and structures them so the business captures the maximum benefit. Owners interested in year-round strategies can explore additional proactive tax planning approaches that reduce surprises at filing time.

How Does Financial Consulting Support Business Growth and Retirement?

Financial consulting supports business growth and retirement by connecting short-term operational decisions to long-term wealth-building goals, including financial statement analysis for expansion decisions, retirement plan design, and succession planning for eventual ownership transition. Growth and retirement are not separate conversations. They are two sides of the same financial plan, and consulting bridges them.

On the growth side, a financial consultant helps you evaluate expansion opportunities using data rather than instinct. That evaluation includes analyzing whether the current profit margin supports the cost of a new location, a new hire, or a new product line. It includes building financial projections that show the break-even timeline and the capital required. According to the 2026 Federal Reserve Small Business Credit Survey, 60% of small businesses that applied for financing did so to meet operating expenses, and 46% did so to pursue expansion. The businesses that secured financing and used it effectively were typically the ones with organized financial records and clear projections, both deliverables of strategic planning and consulting work.

On the retirement side, the data is striking. According to the 2025 Equitable and SCORE study, small business owners who work with a financial professional expect to retire at age 63. Owners without a financial professional expect to retire at age 70. That 7-year gap reflects the compounding effect of early planning: earlier retirement contributions grow longer, tax-advantaged structures capture more savings, and succession planning creates a viable exit path. A separate SCORE survey found that 34% of small business owners have no retirement savings plan outside their company. Relying entirely on the business sale to fund retirement is risky. According to the Exit Planning Institute, only 20 to 30% of businesses listed for sale actually sell.

A 2026 Chase survey of approximately 1,000 small business owners confirmed that nearly half plan to retire within 10 years, yet few have a fully developed succession plan. In Miami's competitive entrepreneurial market and nationally, that planning gap represents one of the highest-value opportunities for financial consulting. The consultant helps the owner build a retirement savings vehicle, value the business accurately, and structure the business formation and ownership documents so the transition can happen on the owner's timeline.

Financial consulting touches each of the following areas across the growth-to-exit continuum:

- Cash flow forecasting and budget development for expansion readiness

- Financial statement analysis to evaluate profitability and debt capacity

- Retirement plan selection and tax credit optimization under SECURE 2.0

- Succession planning, including business valuation and buy-sell agreements

- Tax structure optimization to minimize the tax burden at sale or transfer

- Ongoing financial oversight through fractional CFO or advisory retainers

What's the Best Way to Find a Good Financial Consultant?

The best way to find a good financial consultant is to evaluate their credentials, verify their experience with businesses similar to yours, assess their communication style, and confirm that their fee structure is transparent and tied to clear deliverables. The right consultant produces measurable results. The wrong one wastes time and money.

Start with credentials. A Certified Public Accountant (CPA) license demonstrates competency in tax and accounting. An Enrolled Agent (EA) designation means the professional is authorized by the IRS to represent taxpayers. A Certified Financial Planner (CFP) certification signals expertise in investment and retirement planning. The strongest consultants for small business owners often hold a CPA or EA alongside practical business advisory experience, because the work requires both technical tax knowledge and strategic business insight.

Next, verify experience. Ask how many small business clients the consultant works with, what industries they serve, and whether they have handled situations similar to yours. A consultant who has helped 50 growing businesses manage cash flow and plan for exit is more valuable than one who primarily serves individuals. According to a 2025 industry survey, 64% of small business owners say trust in the consultant is the single most important factor in choosing who to work with, ranking above price, brand, or specific expertise. Trust builds through transparent communication, consistent follow-through, and honest advice, even when the honest answer is not the one you want to hear.

Fee transparency matters. Ask whether the consultant charges hourly, by project, or on a monthly retainer. Each structure fits different needs. Retainers work well for ongoing advisory relationships. Project-based fees work well for defined engagements like a cash flow overhaul or a tax structure review. Look for a consultant who explains exactly what the engagement covers and what deliverables you will receive. A strong financial and operational consulting relationship starts with clarity about scope, timeline, and expected outcomes.

What Is a Red Flag for a Financial Advisor?

A red flag for a financial advisor is any behavior that suggests a lack of transparency, credentials, or fiduciary responsibility. Specific red flags include guaranteeing specific financial outcomes, refusing to explain fees in detail, lacking verifiable professional certifications, pressuring you to make quick decisions, and being unwilling to provide references from current or past clients. A qualified consultant earns your trust through competency and honesty. Any professional who shortcuts that process deserves skepticism.

Is It Worth Seeing an Independent Financial Advisor?

Yes, seeing an independent financial advisor is worth it for most small business owners because independent advisors typically offer objective guidance free from the product-sales incentives that can affect advisors at large financial institutions. Independent advisors and boutique firms often specialize in small business clients, which means they understand the specific challenges of cash flow, entity structure, and retirement planning that larger firms may treat as secondary.

The financial advisory profession is growing because demand for personalized guidance continues to increase. According to the Bureau of Labor Statistics, the personal financial advisor market is projected to see 13% job growth between 2022 and 2032, far outpacing the national average of 3.71%. That growth reflects the reality that more business owners are seeking financial metrics support and strategic advisory as businesses become more complex. The virtual CFO segment alone is projected to grow from $3.91 billion in 2024 to $8.17 billion by 2032, according to Business Research Insights.

For small business owners, the most productive relationship is often with a CPA-led advisory firm that combines tax expertise with business strategy. This eliminates the coordination friction between a separate accountant, a separate financial planner, and a separate business consultant. One firm that understands both the tax code and the business model can deliver a more cohesive strategy than three separate professionals working in isolation.

How To File Unfiled (Back) Tax Returns?

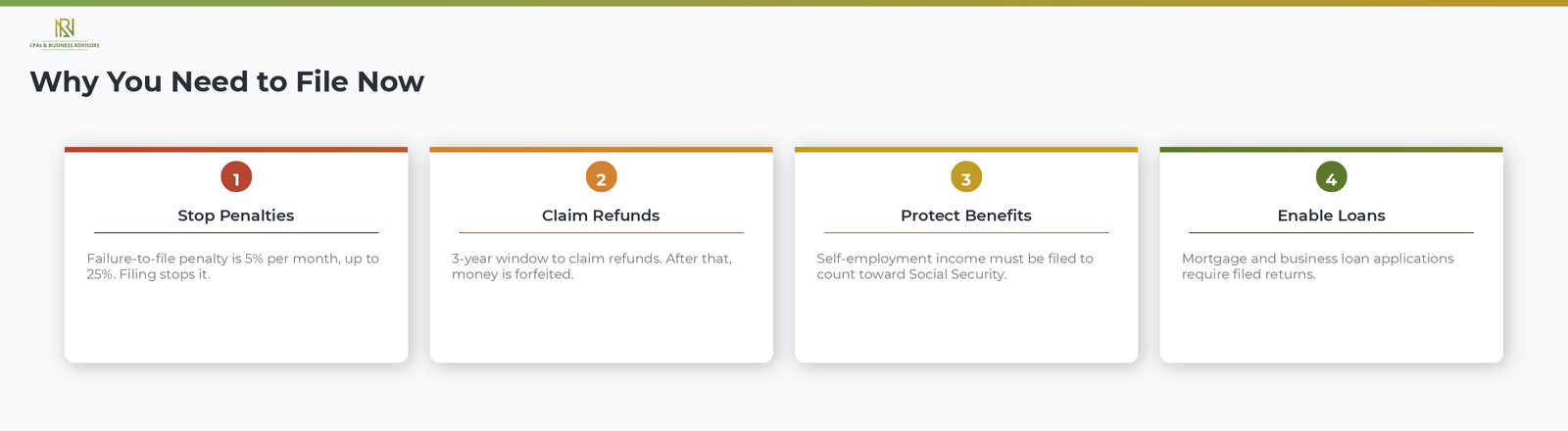

Filing unfiled tax returns, even if they are years late, stops the IRS from increasing your penalties, preserves your right to claim refunds and credits, and prevents the agency from filing a return on your behalf that gives you none of the deductions or credits you may be entitled to. According to the IRS, the failure-to-file penalty is 5 percent of the unpaid tax for each month or part of a month that a return is late, up to a maximum of 25 percent. This penalty is separate from and more expensive than the failure-to-pay penalty, which is 0.5 percent per month. Filing, even when you cannot pay the balance, stops the larger penalty from growing.

Beyond penalties, unfiled returns create problems that extend into other areas of your financial life. According to the IRS, the agency holds income tax refunds when its records show that one or more returns are past due. Self-employed individuals who do not file will not have their earnings reported to the Social Security Administration, which means lost credits toward retirement and disability benefits. Mortgage lenders, business loan providers, and federal financial aid programs all require copies of filed tax returns as part of the approval process.

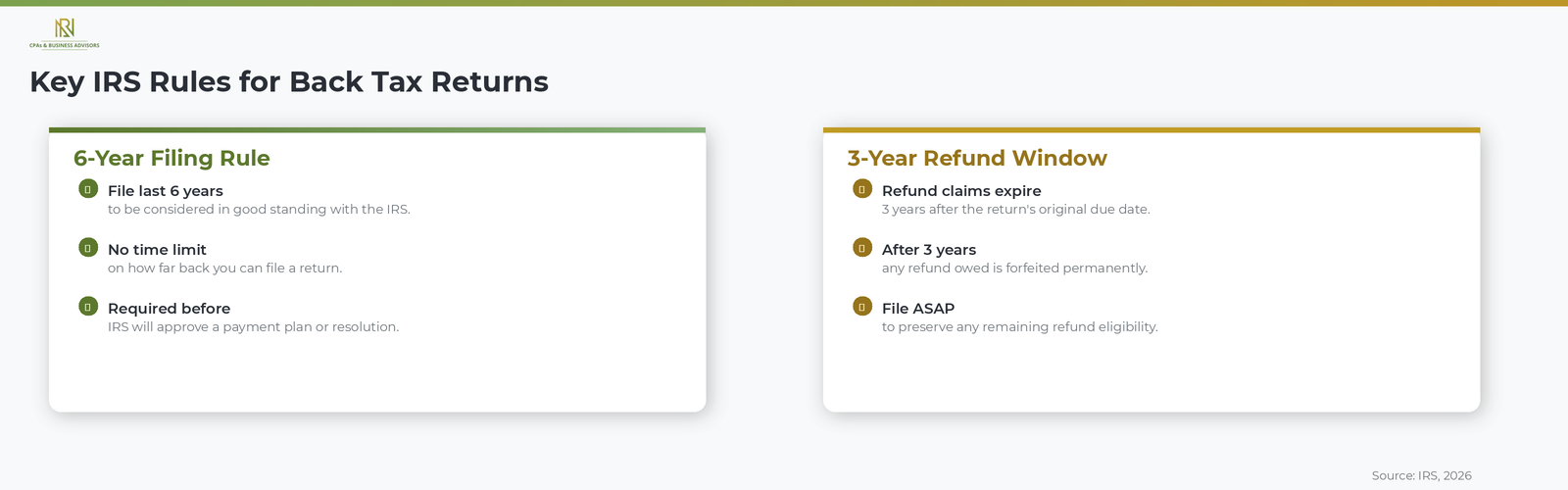

How Many Years Of Back Taxes Do You Need To File

The IRS generally requires you to file the last six years of unfiled tax returns to be considered in compliance, though the agency prefers that you file all outstanding returns. According to the IRS, there is no statute of limitations on filing a past-due return, meaning you can file a return for any prior year regardless of how long ago it was due. However, the IRS only allows you to claim a refund within three years of the return's original due date. After that three-year window closes, any refund you would have been owed is forfeited permanently.

If you have multiple years of unfiled returns, the IRS typically asks you to start with the oldest unfiled year and work forward. Filing all six years brings your account into good standing and is usually required before the IRS will approve a payment plan or other resolution for any balance you owe. For a full overview of the resolution options available once you have filed, our guide to handling a tax balance you cannot pay covers installment agreements, Offers in Compromise, and hardship status.

How To Reconstruct Tax Records For Past Years

If you no longer have the W-2s, 1099s, or other income documents you need to prepare a past-due return, the IRS can provide transcripts of the income information it has on file for you. According to the IRS, you can request wage and income transcripts by filing Form 4506-T, Request for Transcript of Tax Return. These transcripts cover the last 10 tax years and include the information reported to the IRS by your employers, banks, and other payers.

Wage and income transcripts show the data from forms such as W-2s, 1099s, and 1098s, but they do not include information about deductions or credits you may qualify for. To fill in those gaps, gather any records you still have, including bank and brokerage statements, mortgage interest statements, property tax records, charitable donation receipts, and documentation of business expenses if you were self-employed. If you cannot locate certain records, your bank or financial institution may be able to provide duplicate statements for prior years.

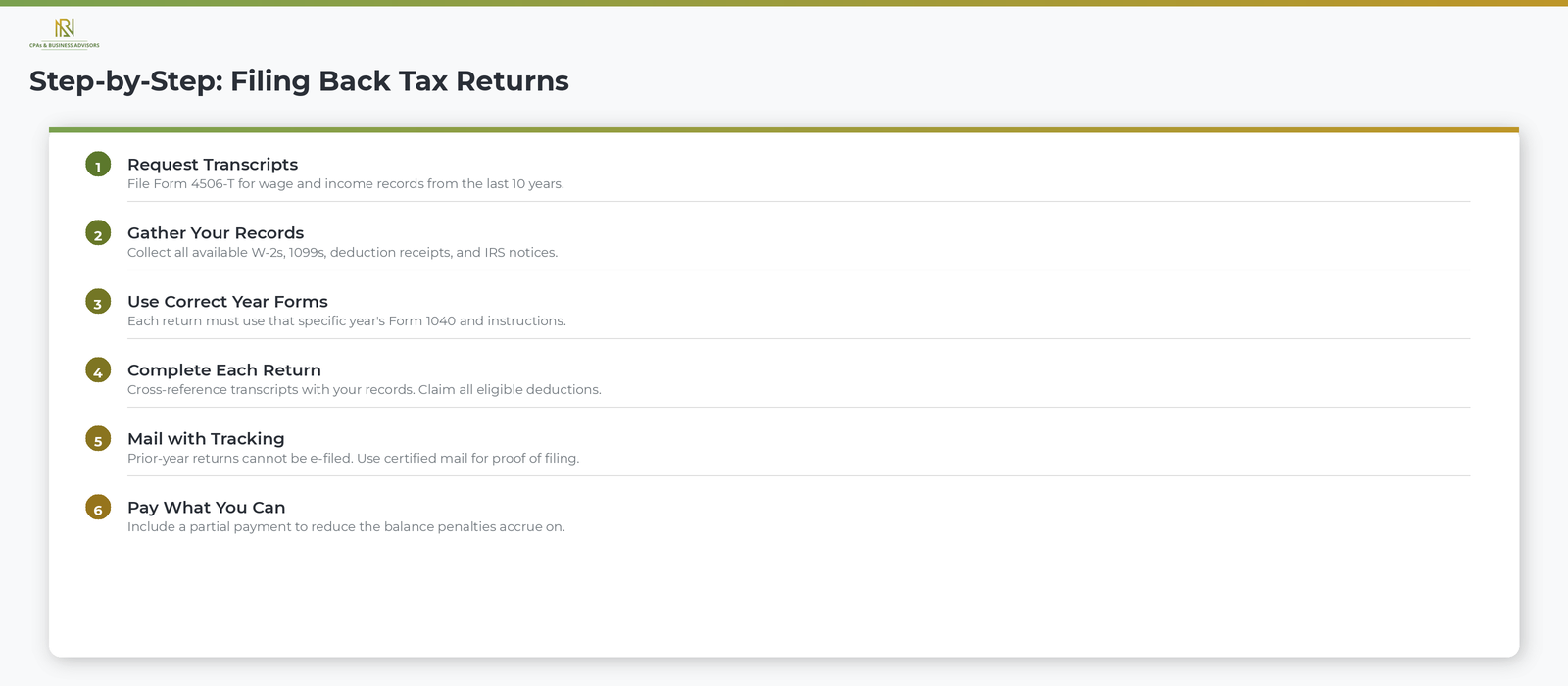

Step By Step Guide To Filing Back Tax Returns

Filing a back tax return follows the same general process as filing a current-year return, with a few important differences in the forms and filing method you use. Follow these steps to file each unfiled return.

- Request your transcripts. File Form 4506-T with the IRS to get wage and income transcripts for each unfiled year. You can request transcripts online through your IRS Online Account, by mail, or by calling 800-829-1040.

- Gather your records. Collect all available income documents, deduction and credit documentation, and any IRS notices you have received for each unfiled year.

- Use the correct year's tax forms. According to the IRS, you must file each return using the tax forms and instructions for the specific year the return covers. A 2021 return must be filed on 2021 forms, a 2022 return on 2022 forms, and so on. Prior-year forms are available on the IRS website under "Prior Year Products."

- Complete the return carefully. Cross-reference the information on your transcript with the documents you gathered to make sure all income is reported and all eligible deductions and credits are claimed. Review each return against the transcript before filing.

- Mail the return. According to the IRS, prior-year returns generally cannot be e-filed and must be mailed to the address listed in the instructions for that year's Form 1040. Use certified mail or a trackable delivery service so you have proof of filing.

- Pay what you can. If the return shows a balance due, include a payment for as much as you can afford. Even a partial payment reduces the balance on which penalties and interest accrue.

According to the IRS, it takes approximately six weeks to process an accurately completed past-due return. If you received a notice about unfiled returns, send the completed return to the address indicated on the notice rather than the standard filing address.

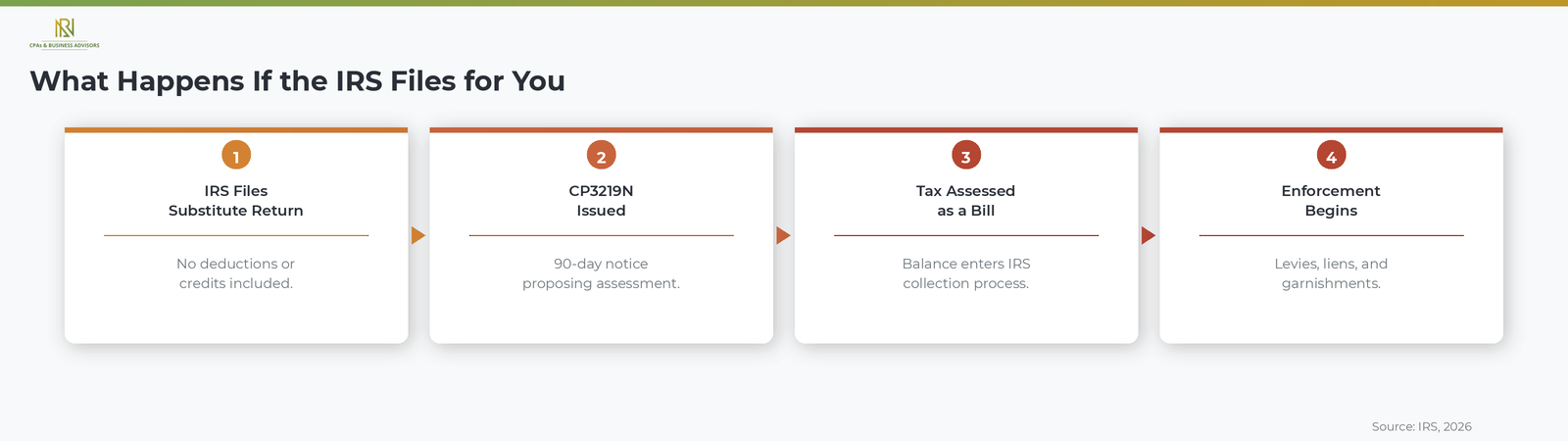

What Happens If The IRS Files A Return For You

If you do not file voluntarily, the IRS can file a substitute return on your behalf, and this substitute return will not include deductions, credits, or exemptions you may be entitled to claim. According to the IRS, a substitute return is based solely on the income information the agency received from third parties such as employers and banks. Because it does not account for deductions like business expenses, itemized deductions, or tax credits such as the Earned Income Credit, the substitute return almost always results in a higher tax bill than the return you would have filed yourself.

After preparing a substitute return, the IRS sends a CP3219N, which is a Notice of Deficiency (also called a 90-day letter) proposing the tax assessment. You have 90 days to either file your own return or petition the U.S. Tax Court. Taxpayers who want to understand the CP3219A Notice of Deficiency in detail, including the 90-day deadline and Tax Court options, can review our full guide to the statutory notice of deficiency. If you do neither, the IRS proceeds with the assessment, and the balance enters the standard collection process.

How To Handle The Balance After Filing

Filing back tax returns often results in a balance due, and the IRS expects you to address that balance even if you cannot pay it in full. According to the IRS, you have several options for resolving the amount owed.

- Pay in full. The fastest way to stop penalties and interest from accruing further.

- Short-term payment extension. According to the IRS, you can request an additional 60 to 120 days to pay your balance in full through the IRS Online Payment Agreement tool or by calling 800-829-1040, with no setup fee.

- Installment agreement. A monthly payment plan that spreads the balance over time. Our step-by-step guide to installment agreements explains the application process and balance thresholds.

- Offer in Compromise. If the full balance is unlikely to be collected, you may be able to settle for less than you owe.

- Currently Not Collectible status. If you cannot afford to pay anything, the IRS may temporarily pause collection.

Taxpayers who are filing multiple years of back returns and facing a combined balance may also qualify for the IRS Fresh Start program, which expands eligibility for installment agreements and eases lien thresholds for individuals and businesses working to get back into compliance.

Frequently Asked Questions About Filing Back Taxes

How Far Back Can You File Taxes?

You can file a tax return for any prior year with no time limit on how far back you go. According to the IRS, there is no statute of limitations on filing a past-due return. However, refund claims must be filed within three years of the return's original due date, and the IRS generally requires the last six years of returns to consider you in compliance.

Can You File Back Taxes Online?

Most prior-year returns cannot be e-filed and must be printed and mailed to the IRS. According to the IRS, e-filing is generally only available for the current tax year and the two most recent prior years. Returns for earlier years must be completed on the appropriate year's forms and mailed to the address in the instructions.

What Happens If You Have Not Filed Taxes In Several Years?

The IRS tracks unfiled returns and can take enforcement action including filing a substitute return, assessing penalties, holding your refunds, and eventually pursuing levies and liens. According to the IRS, the best course of action is to file all outstanding returns as soon as possible, pay what you can, and contact the IRS to discuss resolution options for any remaining balance.