%201.avif)

.png)

.png)

Benefits of Outsourcing CFO Services

Outsourcing CFO services gives your business access to experienced financial leadership without the salary, benefits, and overhead of a full-time executive hire. You get the same strategic planning, cash flow oversight, and financial reporting that a traditional CFO provides, but on a flexible, part-time basis that fits your actual needs and budget.

In this article, we cover the specific benefits of outsourcing CFO services, what an outsourced CFO actually does, how costs compare to a full-time hire, which industries benefit the most, and how to tell when your business is ready for this kind of financial support.

What Are the Benefits of Outsourcing CFO Services

The benefits of outsourcing CFO services are lower cost, access to senior-level expertise, flexible engagement, faster results, better financial visibility, and reduced fraud risk. Each of these benefits addresses a real problem that growing businesses face when they need financial leadership but are not ready for a full-time executive.

According to Mordor Intelligence, the global finance and accounting outsourcing market reached $54.79 billion in 2025 and is projected to grow to $85.92 billion by 2031. That kind of growth tells you that businesses are not just trying outsourcing. They are making it a permanent part of how they operate. The shift is driven by cost savings, talent shortages, and the need for better financial data.

A Deloitte Global Outsourcing Survey from 2024 found that 80% of executives plan to maintain or increase their outsourcing investment over the next 12 months. That is a strong signal that outsourcing financial leadership is no longer a temporary fix. It is a long-term strategy for companies of all sizes. We see this firsthand with our virtual CFO clients, who consistently tell us that having a financial partner on call has changed how they make decisions.

Cost Savings Compared to a Full-Time CFO

The most immediate benefit of outsourcing is cost. A full-time CFO in the United States earns a median base salary between $300,000 and $450,000 per year, according to Salary.com data for 2025. When you add bonuses, health insurance, retirement contributions, and equity, total compensation can easily exceed $750,000 annually.

An outsourced CFO, by contrast, typically costs between $3,000 and $10,000 per month on a retainer basis, or $150 to $500 per hour for project work. For a business paying $5,000 per month, that comes out to $60,000 per year. That is roughly 15% of what a full-time CFO costs in base salary alone. According to Insignia Resources, businesses save 20% to 60% on finance operations by outsourcing, depending on the scope of services and the provider.

Access to Broader Expertise

When you hire a single full-time CFO, you get one person's experience. When you outsource, you often get a team. Most outsourced CFO firms employ multiple financial professionals with experience across different industries, growth stages, and financial challenges. That means your business benefits from a wider pool of knowledge than any single hire could provide.

According to a 2025 report from Robert Half, 62% of finance leaders struggle to hire qualified accountants. The U.S. accounting workforce dropped by roughly 10% from 2019 to 2024, falling to about 1.78 million professionals. That talent shortage means the pool of available full-time CFOs is shrinking, and the ones who are available command higher salaries. Outsourcing sidesteps that problem entirely by connecting you with experienced professionals who are already in practice.

Flexibility and Scalability

Business needs change. During a fundraising round, you might need 30 hours a month of CFO support. During a stable quarter, you might only need 10. An outsourced CFO adjusts to your schedule. You scale up when things are busy and scale back when they are not, without the awkwardness or cost of hiring and laying off a full-time employee.

This flexibility is especially valuable for businesses with seasonal revenue patterns, rapid growth phases, or project-based financial needs like mergers, audits, or system implementations.

Objectivity and Fraud Prevention

An outsourced CFO provides an outside perspective on your finances. Because they are not embedded in your internal politics or culture, they can identify problems that an in-house team might overlook or hesitate to flag. This includes everything from wasteful spending patterns to potential fraud.

Internal fraud is a real risk for businesses of all sizes. Having a third-party financial leader overseeing your books, establishing controls, and enforcing separation of duties adds a layer of protection that an in-house-only setup simply cannot match.

What Does an Outsourced CFO Do

An outsourced CFO does everything a full-time CFO does, but on a part-time, remote, or project basis. Their core responsibilities include financial planning and analysis, cash flow management, budgeting and forecasting, financial reporting, tax strategy coordination, fundraising support, and strategic advising.

The specific work depends on what your business needs most. A startup raising its first round of capital might need help building a financial model and organizing investor-ready reports. A construction company with $5 million in revenue might need cash flow forecasting and job costing analysis. A restaurant group expanding to a second location might need help with budgeting and financial statements that lenders will accept.

According to a Deloitte 2025 CFO Signals survey, 87% of finance leaders report a talent shortage in their accounting departments. Only 1 in 10 CFOs say they have no finance talent gaps at all. An outsourced CFO fills those gaps with experienced professionals who can start delivering results immediately, without a months-long recruiting and onboarding process.

What Are the 5 Functions of a CFO

The 5 functions of a CFO are financial planning, cash flow management, financial reporting, risk management, and strategic growth advising. Each function plays a direct role in keeping the business financially healthy and positioned for growth.

Financial Planning

A CFO builds annual budgets, revenue forecasts, and spending plans that give the business a clear financial roadmap. They also create scenario models so the leadership team can see what happens under different conditions, like a 20% drop in revenue or a major new hire. According to PwC, 47% of CFOs cite data quality and availability as a top concern in financial reporting. A good CFO fixes that by building clean, reliable planning systems.

Cash Flow Management

Cash flow is the most common financial concern for small business owners. According to a Q4 2025 survey by OnDeck and Ocrolus, 29% of small business owners rank cash flow as their top challenge, second only to inflation at 31%. A CFO manages cash flow by building rolling forecasts, speeding up collections, timing payments strategically, and maintaining adequate reserves.

Financial Reporting

A CFO produces the reports that banks, investors, and internal leadership need to make decisions. This includes monthly profit and loss statements, balance sheets, cash flow statements, and custom dashboards that track key performance indicators. Clean, timely reports build trust with every stakeholder who has a financial interest in your business.

Risk Management

A CFO identifies and mitigates financial risks before they cause damage. This includes monitoring customer concentration, tracking debt levels, watching for compliance issues, and building contingency plans for economic downturns. According to McKinsey, companies that engage in proactive scenario planning are 33% more likely to recover financially within six months after a disruption.

Strategic Growth Advising

Beyond the numbers, a CFO advises on when and how to grow. They model the financial impact of new hires, new locations, new products, and new markets. They help the business owner weigh risk against opportunity and make growth decisions based on data, not gut feeling. This is where business consulting and CFO work overlap most.

How Much Does CFO Services Cost

CFO services cost between $3,000 and $10,000 per month for ongoing retainer work, or $150 to $500 per hour for project-based engagements. Most businesses can expect to pay roughly $40,000 to $60,000 annually for outsourced CFO services, according to data from GrowthForce.

Compare that to a full-time CFO. According to Salary.com, the median base salary for a CFO in the United States is approximately $437,000. When you factor in bonuses, benefits, retirement, and equity, total annual compensation can exceed $750,000. For small and midsize businesses, that kind of fixed cost is hard to justify, especially when the CFO role may not require 40 hours of work every single week.

Cost FactorFull-Time CFOOutsourced CFOAnnual Base Salary$300,000 to $450,000Not applicableAnnual Total Compensation$500,000 to $750,000+$40,000 to $120,000Health Insurance and Benefits$15,000 to $30,000+$0 (included in fee)Equity and Stock OptionsOften requiredNot requiredRecruiting and Onboarding Time120 to 180 daysDays to weeksFlexibility to ScaleFixed commitmentScale up or down monthlyBreadth of ExpertiseOne person's experienceTeam-based, multi-industry

Sources: Salary.com (2025), GrowthForce, Cowen Partners Executive Search, Staffing Soft

The cost of outsourcing also includes access to modern financial tools and technology that the CFO firm already uses. Most outsourced providers work with platforms like QuickBooks Online, Xero, NetSuite, and specialized forecasting software. You get the benefit of those tools without having to buy and implement them yourself.

Which Industry Benefits the Most From Outsourcing

The industries that benefit the most from outsourcing CFO services are technology and SaaS, healthcare, e-commerce, professional services, construction, and restaurants. Any industry with complex revenue streams, tight margins, or fast growth tends to see the biggest return on outsourced financial leadership.

According to Insignia Resources, e-commerce leads outsourcing adoption at 70%, followed by healthcare at 65%. These industries deal with high transaction volumes, complex compliance requirements, and fast-changing financial dynamics that demand CFO-level oversight.

We work with clients across several of these sectors. Startups and tech companies benefit from outsourced CFO support during fundraising and rapid scaling. Restaurant businesses benefit from cash flow forecasting and cost control that keeps tight margins from turning into losses. Nonprofits, cannabis businesses, and companies with international operations all have specialized financial needs that an outsourced CFO with industry experience can handle more effectively than a generalist in-house hire.

Is Outsourcing Good or Bad for Business

Outsourcing is good for business when it is done strategically. The data consistently supports this. According to Deloitte's 2024 Global Outsourcing Survey, 63% of companies increased their outsourcing budgets in 2024. Another survey found that only 34% of executives now cite cost as their primary outsourcing driver, down from 70% in 2020. That shift means businesses are outsourcing for better reasons, not just to save money, but to gain expertise, speed, and flexibility.

The concern people sometimes raise about outsourcing is that an outside provider will not understand the business as well as an internal employee. That is a fair concern, and it is why choosing the right provider matters. A good outsourced CFO firm takes time to learn your business, your industry, and your goals. They attend leadership meetings, review your reports weekly, and become a functional part of your team even though they are not on your payroll.

The data on outsourcing failures usually points to poor provider selection or unclear expectations, not to the outsourcing model itself. When the scope, deliverables, and communication cadence are defined upfront, outsourcing consistently delivers strong results. According to Gartner's 2025 CFO Priorities report, AI adoption in finance has nearly doubled in two years, and CFOs are looking for outsourcing partners who bring technology along with expertise. The businesses that get the best results are the ones that treat their outsourced CFO as a strategic partner, not just a vendor.

What Size Companies Have a CFO

Companies of all sizes can have a CFO, but the model varies. Most businesses start looking for a full-time CFO when they reach $50 to $75 million in annual revenue, according to industry benchmarks from Driven Insights. Below that threshold, a fractional or outsourced CFO is usually the more practical and cost-effective choice.

Startups and small businesses under $5 million in revenue often rely on their founder or a bookkeeper for financial management. Between $5 million and $20 million, the financial complexity typically outgrows what a bookkeeper can handle, and an outsourced CFO becomes critical. Between $20 million and $50 million, the outsourced CFO engagement often expands to 20 to 35 hours per month, according to Sayva Solutions.

Even large companies use outsourced CFOs for specific situations. Interim CFO placements during leadership transitions, project-based work like mergers and acquisitions, and specialized compliance projects are all common reasons larger organizations bring in outside financial leadership.

For businesses at any stage, the key question is not whether you need a CFO. The question is whether you need one full time or whether an outsourced model gives you the same results at a lower cost. For most businesses under $50 million, the answer is clear. Outsourcing delivers more value per dollar than a full-time hire. This is why fractional CFO services have grown so rapidly over the past several years.

Can You Outsource a CFO

Yes, you can outsource a CFO. Outsourcing a CFO means hiring an external financial professional or firm to handle the strategic financial leadership of your business on a part-time, remote, or project basis. The outsourced CFO works with your existing team, your accountant, and your bookkeeper to provide the high-level planning, analysis, and decision support that those roles do not cover.

The model works because modern technology makes remote financial management seamless. Cloud-based accounting platforms, video conferencing, shared dashboards, and real-time reporting tools allow an outsourced CFO to have the same visibility into your numbers as someone sitting in your office. According to the global virtual CFO market research from Business Research Insights, the virtual CFO market was valued at roughly $3.91 billion in 2024 and is growing at a compound annual growth rate of about 9.6% through 2032.

The key to making it work is clear communication and a structured engagement. The best outsourced CFO relationships include weekly or biweekly check-in calls, monthly financial reviews, defined deliverables, and transparent reporting. When those elements are in place, the outsourced model performs just as well as, and often better than, a full-time in-house CFO for businesses that do not need 40 hours of CFO work every week.

How an Outsourced CFO Works With Your Existing Team

An outsourced CFO does not replace your bookkeeper, accountant, or controller. They work above those roles, turning the data your team produces into strategy, forecasts, and financial decisions.

Think of it as a layer of leadership. Your bookkeeper handles daily transactions, bank reconciliations, and data entry. Your accountant or CPA handles tax planning and compliance. Your outsourced CFO takes the financial data those team members produce and builds the bigger picture: cash flow forecasts, budget models, investor reports, and strategic recommendations.

This layered approach also improves the quality of your team's work. An outsourced CFO often identifies gaps in your accounting processes, recommends better systems, and sets up reporting standards that make everyone's job easier. According to a Deloitte 2025 CFO Signals survey, only 1 in 10 CFOs report no talent shortages. Most companies are operating with understaffed finance teams. An outsourced CFO fills the leadership gap without requiring you to hire additional full-time employees.

For businesses that are still building their internal finance function, an outsourced CFO can also help with hiring. They know what skills to look for in a controller or bookkeeper, and they can train new hires on the systems and processes that will keep your financial operations running smoothly. Solid startup advisory guidance at this stage sets the foundation for everything that follows.

Signs Your Business Is Ready for an Outsourced CFO

Your business is ready for an outsourced CFO when financial decisions are becoming too complex or too important to handle without senior-level guidance. Here are the most common signs we see.

Revenue is growing but profit is not keeping pace. Cash flow feels unpredictable even though sales are strong. You are preparing for a bank loan, investor pitch, or line of credit and need professional financial documents. Your bookkeeper or accountant is great at recording data but cannot answer strategic questions about growth, margins, or forecasting. You are expanding to a new location, adding employees, or entering a new market. You want to sell the business eventually and need to build a clean financial track record.

According to the 2025 Small Business Credit Survey, only 46% of small employer firms were profitable in 2024, while 35% broke even and 19% operated at a loss. Those numbers show that most small businesses are not generating enough profit to grow comfortably on their own. An outsourced CFO can often find the margin improvements, cash flow fixes, and cost savings that turn a breakeven business into a profitable one.

Here in Miami, we work with businesses that are at exactly this inflection point. The complexity has grown beyond what the founder or a basic finance team can manage, and the business needs someone who can see the full picture and help chart the course forward.

Frequently Asked Questions

Are 90% of CFOs Outsourcing Accounting Functions

No, 90% of CFOs are not outsourcing accounting functions. That number is sometimes cited without proper context. However, outsourcing is widespread and growing. According to Deloitte's 2024 Global Outsourcing Survey, 80% of executives plan to maintain or increase outsourcing investments. And 87% of finance leaders report talent shortages in accounting, according to the Deloitte 2025 CFO Signals survey, which is pushing more companies toward outsourced solutions.

How Much Do Outsourced CFOs Make

Outsourced CFOs make between $150 and $500 per hour on a project basis, or between $3,000 and $10,000 per month on a retainer. Annual earnings vary widely depending on the number of clients and the complexity of the work. Experienced outsourced CFOs working with multiple clients can earn well over $200,000 per year.

How Much Does a CFO Charge Per Hour

A CFO charges between $150 and $500 per hour for outsourced or fractional work. The rate depends on the provider's experience, the complexity of your financial situation, and your geographic market. For comparison, the equivalent hourly rate for a full-time CFO earning a $437,000 base salary is roughly $210 per hour, according to Salary.com.

What Are the 4 Types of Outsourcing

The 4 types of outsourcing are professional outsourcing, IT outsourcing, manufacturing outsourcing, and process-specific outsourcing. Professional outsourcing includes services like accounting, legal, and CFO functions. IT outsourcing covers software development and tech support. Manufacturing outsourcing involves producing goods through a third party. Process-specific outsourcing focuses on individual business functions like payroll or customer service.

What Are the Three Types of Outsourcing

The three types of outsourcing based on location are onshore (same country), nearshore (nearby country in a similar time zone), and offshore (a distant country, typically for cost savings). For CFO services, onshore outsourcing is the most common because financial strategy requires close communication, real-time collaboration, and familiarity with U.S. tax law and regulations.

What Do CFO Services Include

CFO services include financial planning and analysis, cash flow forecasting, budgeting, financial statement preparation, tax strategy coordination, fundraising support, investor reporting, cost optimization, risk management, and strategic growth advising. The specific services depend on the client's needs and the scope of the engagement.

What Are the Most Outsourced Services

The most outsourced services in finance and accounting are tax preparation, bookkeeping, payroll, accounts payable and receivable, and financial reporting. According to research cited by Digital Minds BPO, tax preparation is outsourced by 71% of companies that use accounting outsourcing, making it the most commonly outsourced accounting task. CFO-level services like strategic planning and forecasting are a growing segment of the outsourcing market.

Putting It All Together

Outsourcing CFO services gives your business senior-level financial leadership at a fraction of the cost of a full-time hire. The benefits are clear: lower overhead, broader expertise, flexible engagement, better financial visibility, and a strategic partner who helps you make smarter decisions with your money. The data backs it up. The finance and accounting outsourcing market is growing by billions of dollars every year because businesses are getting real, measurable results from this model.

If your business is growing and you need financial guidance that goes beyond basic bookkeeping, we are here to help. At NR CPAs & Business Advisors, we provide outsourced CFO services built around your specific goals, industry, and growth stage. Give us a call at (954) 231-6613 to talk about what that looks like for your business.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

IRS Notices Explained: What Each Letter Means And What To Do?

What Is An IRS Notice

An IRS notice is official correspondence that the Internal Revenue Service sends through the U.S. mail to inform you about a specific issue with your federal tax return or account. According to the IRS, the agency sends notices for reasons ranging from a simple math correction on your return to an unpaid balance or a request for additional documentation. Receiving a notice does not necessarily mean you made a mistake or owe additional tax, and many notices can be resolved by following the instructions printed on the document.

The IRS draws a practical distinction between two categories of mail. A notice is typically system-generated and addresses a specific account issue such as a balance due, a refund adjustment, or a processing change. A letter, by contrast, often comes from an individual IRS employee or department and may request information, confirm an action, or relate to an ongoing examination. Both arrive by U.S. mail, and both include a notice or letter number in the upper right corner of the first page that identifies exactly what the correspondence is about.

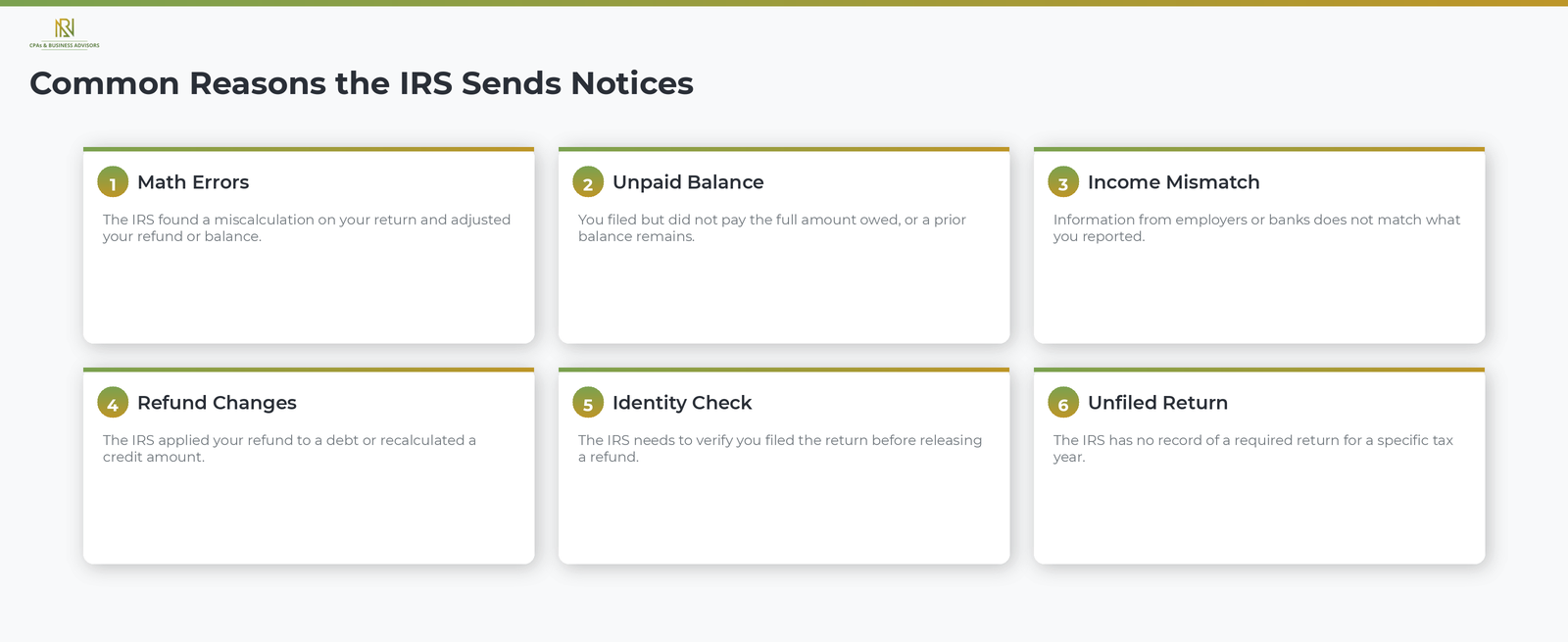

Common Reasons The IRS Sends Notices

The IRS sends notices most often because of a discrepancy on your tax return, an unpaid balance, or a change the agency made to your account. According to the IRS, the most frequent triggers include the following situations.

- Math errors or miscalculations on your return. The IRS caught an arithmetic mistake and adjusted your refund or balance accordingly.

- An unpaid tax balance. You filed a return but did not pay the full amount owed, or a prior balance remains on your account.

- Unreported or underreported income. Information the IRS received from employers, banks, or other third parties does not match what you reported on your return.

- Refund changes. The IRS applied your refund to a prior debt or adjusted the amount because of a credit recalculation.

- Identity verification. The IRS needs to confirm that you filed the return before releasing a refund.

- Unfiled returns. The IRS has no record of a required return for a specific tax year.

Not every IRS notice signals a problem. Some correspondence simply confirms a change you requested, acknowledges information you submitted, or notifies you that the IRS closed its review of your account.

Most Common Types Of IRS Notices

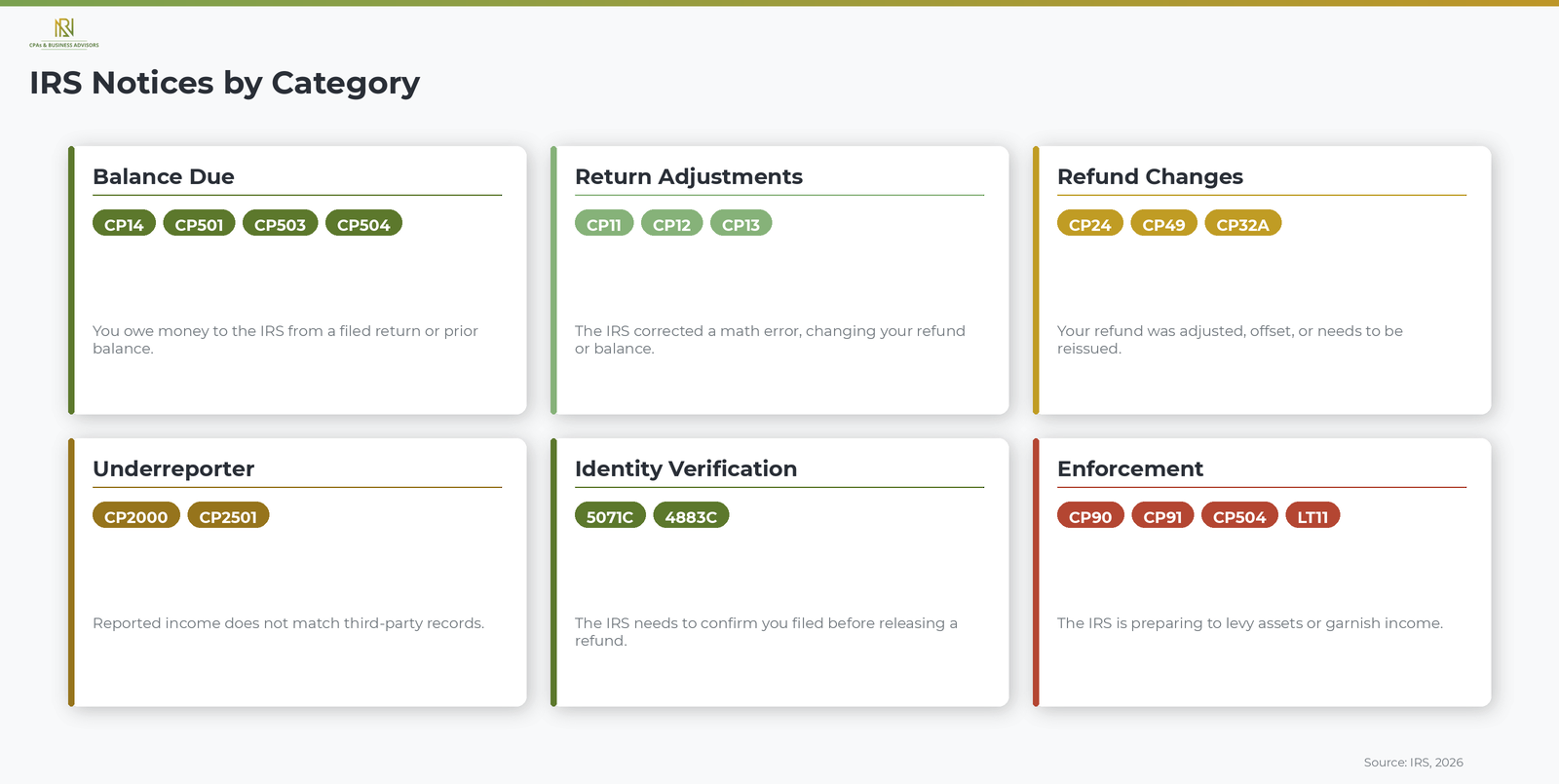

IRS notices fall into several broad categories based on why the agency issued them. Understanding which category your notice belongs to helps you assess its urgency and determine what kind of response it requires. The notice number, printed in the upper right corner of the first page, identifies the specific type.

Balance Due Notices

Balance due notices inform you that you owe money to the IRS. The most common is the CP14, which is the initial notice the agency sends when a filed return shows an unpaid amount. If you received a CP14 notice, our complete guide to this balance due letter explains the specific charges, deadlines, and response options. Subsequent reminders in the collection sequence include the CP501, CP503, and CP504, each carrying increased urgency.

Return Adjustment Notices

The IRS sends adjustment notices when it corrects an error on your return. A CP11 means the correction resulted in a balance you now owe. A CP12 means the correction resulted in a larger refund or a change to the amount you expected. A CP13 means the correction left your balance at zero with no additional amount owed and no refund due. According to the IRS, each of these notices explains exactly what changed and how the recalculated amount was determined.

Refund-Related Notices

These notices address changes to the amount or timing of your refund. A CP24 notifies you that the IRS found a difference between your estimated tax payments and the amount posted to your account, resulting in a potential overpayment credit. A CP49 notifies you that the IRS applied all or part of your refund to a prior tax debt. A CP32A asks you to contact the IRS so the agency can reissue a refund check.

Underreporter Notices

An underreporter notice means the income or payment information the IRS received from third parties does not match what you reported. The CP2000 is the primary notice in this category and one of the most frequently issued IRS letters. According to the IRS, a CP2000 is not a bill but a proposed adjustment that explains how the recalculated tax was determined. Taxpayers who receive a CP2000 notice can review our full guide to this underreporter letter for response steps and dispute options.

Identity Verification Notices

Identity verification notices ask you to confirm that you filed the return in question before the IRS will release a refund. Common examples include Letter 5071C and Letter 4883C. According to the IRS, these letters are part of the agency's efforts to prevent tax-related identity theft and typically require you to verify your identity online at IRS.gov or by calling the toll-free number printed on the letter.

Enforcement And Collection Notices

Enforcement notices signal that the IRS is preparing to take collection action against your assets. A CP504 warns that the IRS intends to levy your state tax refund. A CP90 or LT11 is a final notice of intent to levy bank accounts, wages, and other property, and it grants you the right to request a Collection Due Process hearing within 30 days. Certain enforcement notices, such as the CP90, may arrive as certified mail requiring your signature. A CP91 warns that the IRS intends to levy up to 15 percent of your Social Security benefits.

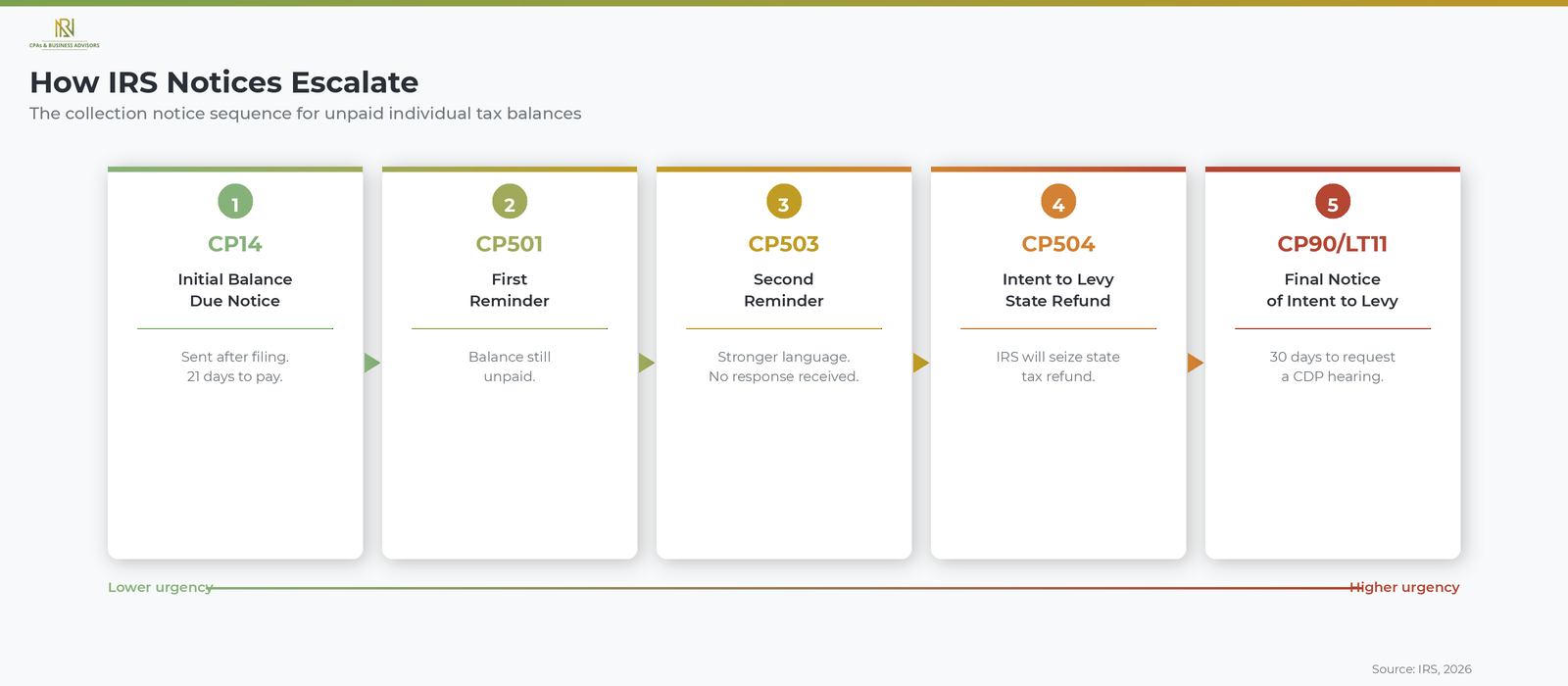

How IRS Notices Escalate From Reminder To Enforcement

IRS collection notices follow a specific sequence that grows more urgent at each stage, and each notice includes a deadline that starts the clock on the next escalation step. According to the IRS, the standard progression for an unpaid individual tax balance works as follows.

- CP14: the initial balance due notice, sent shortly after you file a return with an unpaid amount.

- CP501: a first reminder that your balance remains unpaid.

- CP503: a second reminder with stronger language, noting that the IRS still has not received your payment or a response.

- CP504: a notice of intent to levy your state income tax refund if you do not pay or contact the IRS to arrange a resolution.

- CP90 or LT11: the final notice of intent to levy your wages, bank accounts, and other assets. This notice also informs you of your right to a Collection Due Process hearing, which you must request within 30 days.

Responding at any point in this sequence can slow or stop the escalation. Taxpayers who cannot pay the full amount may qualify for a structured IRS payment plan or installment agreement. Our guide to these structured repayment options covers the application process, payment thresholds, and how interest is calculated on the remaining balance. Those facing significant financial hardship may also qualify for the IRS Fresh Start program, which provides expanded installment terms and penalty relief for eligible individuals and businesses.

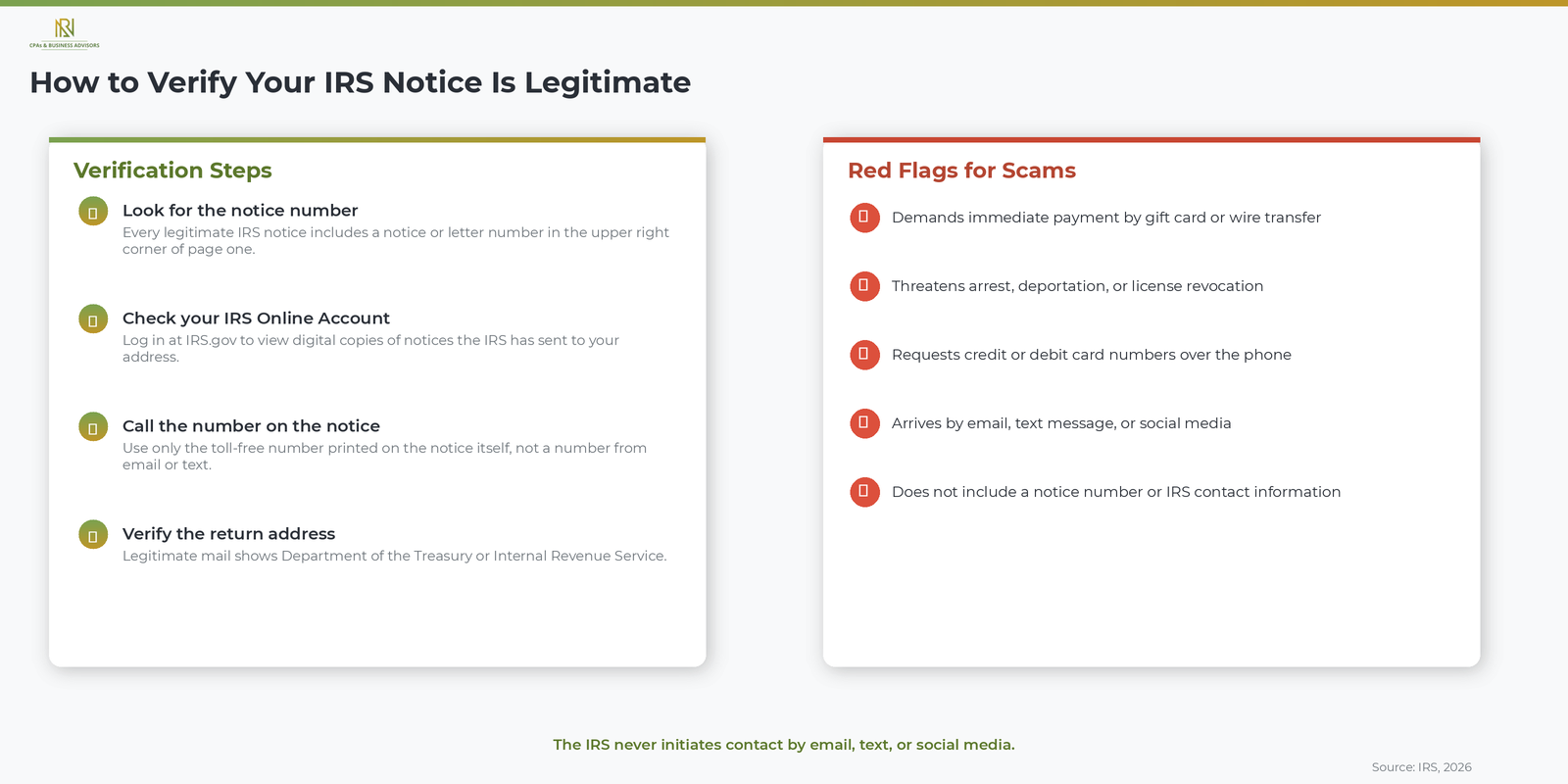

How To Verify Your IRS Notice Is Legitimate

A legitimate IRS notice arrives by U.S. mail, references a specific tax year and notice number, and never asks you to click a link or provide personal information through email or text. According to the IRS, the agency does not initiate contact with taxpayers by email, text message, or social media to request personal or financial information. Any communication that does so is a scam.

To confirm that a notice you received is genuine, take the following steps.

- Look for the notice or letter number in the upper right corner of the first page. Every legitimate IRS notice includes one.

- Log in to your IRS Online Account at IRS.gov. According to the IRS, many notices are viewable in your online account, which allows you to verify the correspondence directly against what the agency has on file.

- Call the toll-free number printed on the notice itself, not a number from an email, a text, or a website you found through a search.

- Check the return address. Legitimate IRS mail comes from a recognized IRS processing center, and the envelope typically includes "Department of the Treasury" or "Internal Revenue Service" in the return address.

According to the IRS, common red flags for fraudulent correspondence include demands for immediate payment by gift card or wire transfer, threats of arrest or deportation, and requests for credit or debit card numbers over the phone.

What To Do When You Receive An IRS Notice

Read the notice carefully, compare the information to your own tax records, and respond by the deadline printed on the document. Most IRS notices explain exactly what changed, why it changed, and what action you need to take. If you agree with the notice, follow the payment or documentation instructions provided. If you disagree, the notice will explain how to dispute the changes, which typically involves mailing a written response with supporting documents to the address on the notice.

The most critical step is acting before the deadline. Late responses can limit your options for disputing proposed changes or requesting a hearing. For a complete walkthrough of what to do when you receive an IRS notice, including what documentation to gather and how to organize your reply, our step-by-step response guide covers every stage from opening the envelope to confirming the issue is resolved.

When To Get Professional Help With An IRS Notice

Consider working with a CPA, Enrolled Agent, or tax attorney when your notice involves a large balance due, a proposed audit, an enforcement action such as a levy or lien, or a situation you do not fully understand. A qualified tax professional can communicate directly with the IRS on your behalf, identify resolution options you may not be aware of, and ensure your rights as a taxpayer are protected throughout the process. According to the IRS, you can authorize a representative by filing Form 2848, Power of Attorney and Declaration of Representative. Simple notices confirming a small refund adjustment or a zero-balance correction typically do not require professional assistance.

Frequently Asked Questions About IRS Notices

What Is The Most Common IRS Notice?

The CP14 is the most commonly issued IRS notice. According to the IRS, a CP14 is sent when a filed tax return shows an unpaid balance. The notice lists the amount owed, the payment due date, and the options available for resolving the balance.

How Do I Know If My IRS Notice Is Real?

A real IRS notice arrives by U.S. mail, includes a notice number in the upper right corner, and references a tax year tied to your account. According to the IRS, the agency never initiates contact by email, text, or social media. You can verify any notice by logging in to your IRS Online Account at IRS.gov.

What Happens If I Ignore An IRS Notice?

Ignoring an IRS notice allows penalties and interest to accumulate and moves your case further along the collection process. According to the IRS, unresolved balances can eventually lead to a federal tax lien on your property, levies on your bank accounts and wages, and garnishment of up to 15 percent of your Social Security benefits.

Can I View My IRS Notices Online?

Yes, many IRS notices are available through your IRS Online Account. According to the IRS, you can log in at IRS.gov to view digital copies of notices the agency has sent to your address on file, which provides a convenient way to review your correspondence without waiting for mail delivery.

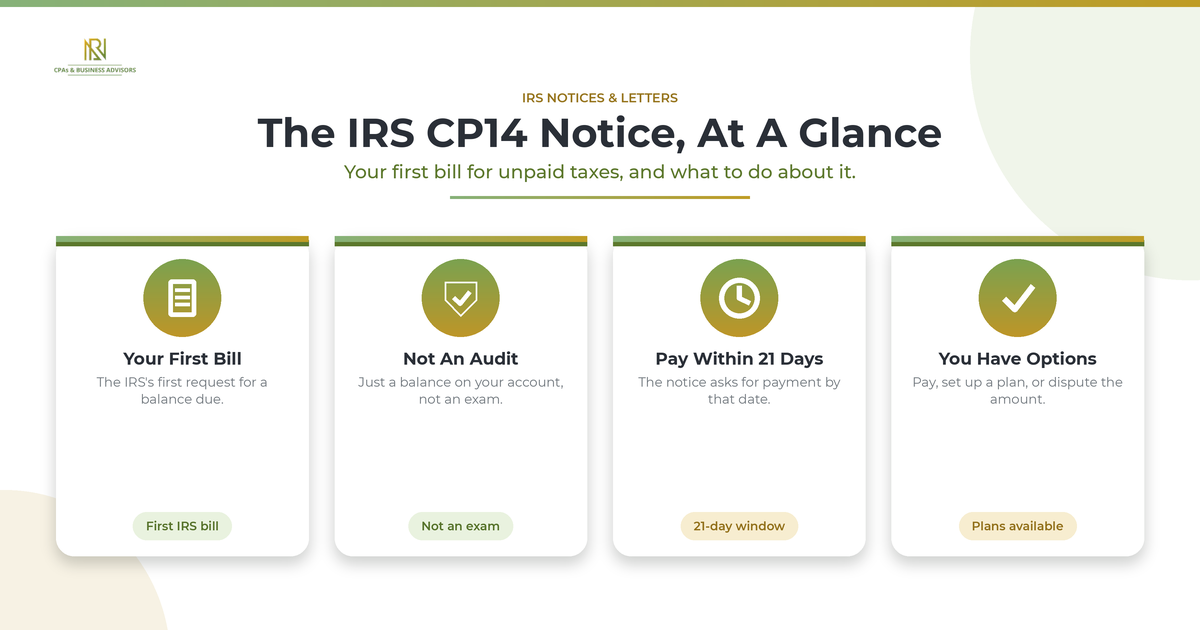

IRS CP14 Notice: Your First Bill For Unpaid Taxes

An IRS CP14 notice is the IRS's first bill, a letter telling you that you owe money on unpaid taxes and asking you to pay within 21 days. According to the IRS, it is not an audit; it means your return was processed and your account shows a balance due, including any interest and penalties. If you already paid, you may not owe anything, so it is worth verifying before you send a payment.

What Is An IRS CP14 Notice?

A CP14 is the IRS's first billing notice, formally the Notice of Tax Due and Demand for Payment, sent when your account shows an unpaid balance. According to the IRS, it is issued after your tax return is processed and the records show you owe money on unpaid taxes. The notice lays out the tax year, the amount you owe in tax, interest, and penalties, and a deadline to pay. Receiving one does not mean you are being audited or that a lien or levy has started. It is the opening step in resolving a balance, and the IRS sends millions of them each year.

Is A CP14 Notice Bad?

A CP14 is serious but routine, and it is fixable. It is the IRS's standard first request for payment, not a penalty notice in itself and not a sign of an audit, though the balance it shows can include penalties and interest on top of the tax. What matters is acting on it rather than ignoring it, because the amount only grows while it sits. Handled promptly, most CP14 balances are straightforward to pay or dispute.

Why Did You Get A CP14 Notice?

You received a CP14 because the IRS processed a return showing a balance due that was not paid in full by the deadline. According to the IRS, the two basic triggers are filing a return with a balance due and not paying the taxes owed by the due date. Common underlying causes include underpaid estimated taxes, an extension that postponed your filing date but not your payment due date, or a balance left after the IRS adjusted your return. Sometimes it is simply a timing issue, where you paid but the payment had not yet posted to your account when the notice was generated.

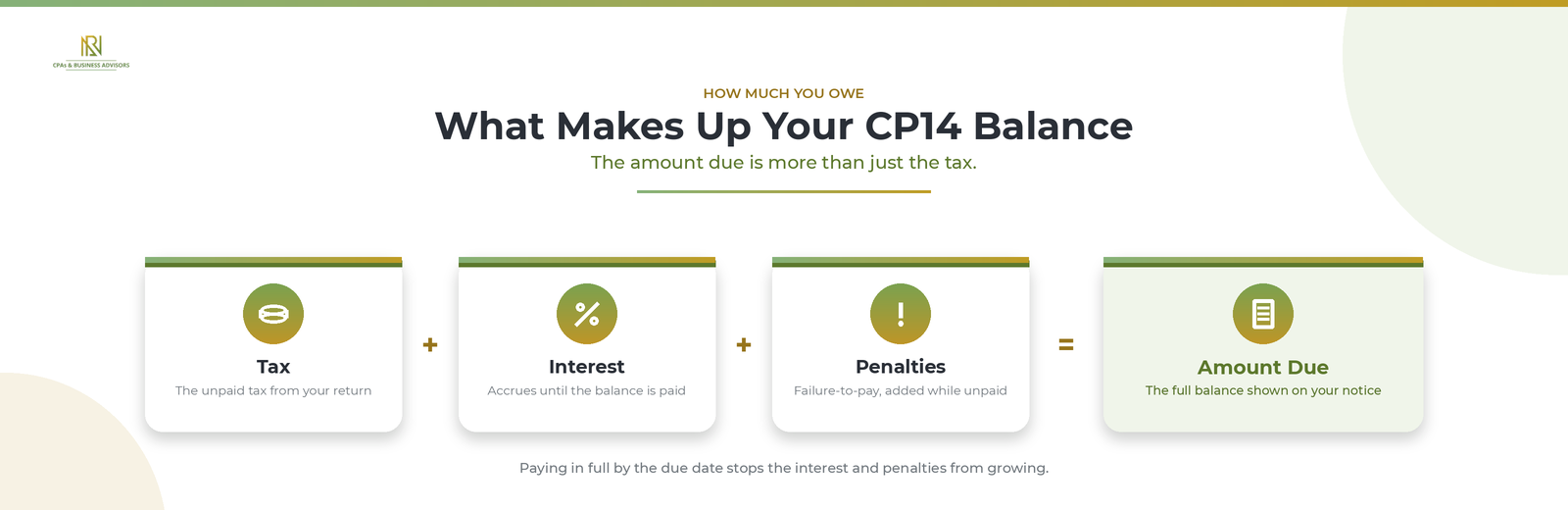

How Much You Owe And When It's Due

The CP14 shows your full balance, tax plus interest and penalties, and asks you to pay within 21 days of the notice date. According to the IRS, interest accrues on the unpaid amount and a failure-to-pay penalty is added while the balance goes unpaid, so paying in full by the date on the notice stops further interest and penalties from building. The Taxpayer Advocate Service notes that if the balance is not fully paid within about 60 days, the IRS can move forward with collection. The 21-day request is the window to act, not a hard cutoff after which nothing else happens.

What If You Already Paid?

If you already paid in full, don't pay again; verify your account first, because the IRS has acknowledged sending CP14 notices in error. According to the IRS, some taxpayers who paid on time, electronically or by check, received a CP14 because the payment had not finished processing or posted with an error, and it advised those taxpayers not to respond or pay a second time while it corrects the accounts, with penalties and interest adjusted automatically once the payment is applied. To confirm where you stand, sign in to your IRS Online Account and review your tax account transcript, checking that each payment posted to the right year and amount. A misapplied payment, a still-processing amended return, or an estimated payment credited to the wrong period are common reasons a balance shows when you don't actually owe it. If your records don't match the notice, dispute it in writing to the address on the notice, including your name, the tax year, and copies of your proof such as cancelled checks or payment confirmations, and keep your originals.

How To Pay Your CP14

If the amount is correct, the fastest resolution is to pay it. According to the IRS, you can pay online, and paying by the due date on the notice limits the interest and penalties you owe. Include the notice's reference details with your payment so it is applied to the right year, and keep a record of the confirmation. Paying the full balance closes the notice; if you can't pay all of it, you still have options.

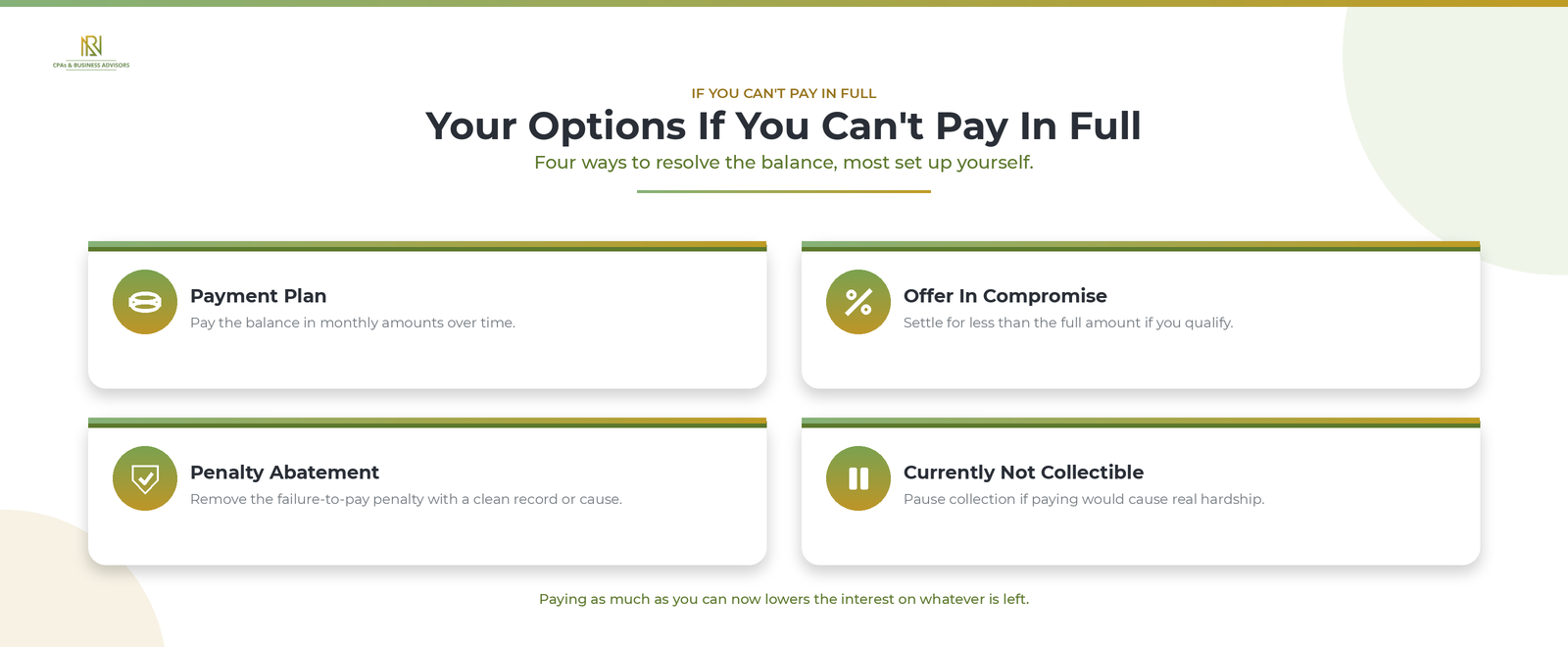

What If You Can't Pay In Full?

If you can't pay the whole balance, you have several options, and you can set most of them up yourself. According to the IRS, the main paths are:

- A payment plan, or installment agreement, that lets you pay the balance in monthly amounts over time, available online for many individual balances.

- An offer in compromise, which settles the debt for less than the full amount when you qualify.

- First-time penalty abatement or reasonable-cause relief, which can remove the failure-to-pay penalty if you have a clean recent history or a valid reason.

- A temporary delay of collection, sometimes called currently not collectible status, if paying would create real hardship.

Even if you choose a plan, paying as much as you can now reduces the interest that keeps accruing on the remaining balance. Setting up an installment agreement with your response also signals to the IRS that you intend to resolve the balance.

What Happens If You Ignore A CP14 Notice?

Ignoring a CP14 doesn't stop the balance; it grows the debt and moves you toward collection. According to the IRS, interest and the failure-to-pay penalty keep accruing on the unpaid amount, and if you don't resolve the balance the account advances through further notices demanding payment. Left unaddressed, that path leads to enforced collection, which can include a federal tax lien or a levy on wages or bank accounts. Because the CP14 is the first and easiest point to deal with the balance, responding now, by paying, arranging a plan, or disputing it, is far cheaper than waiting.

Should You Handle It Yourself Or Get Help?

You can handle most CP14 notices yourself, especially when the balance is correct and you can pay or set up a plan online. According to the IRS, you can resolve a debt and manage your account without calling. Consider professional help when the balance is large, when you believe the notice is wrong and need to build a documented dispute, or when paying would cause hardship. A CPA or enrolled agent can pull your transcripts, verify the amount, and deal with the IRS for you, and a firm offering IRS tax resolution services can manage the response end to end. If cost is a barrier, a Low Income Taxpayer Clinic may help for free or a small fee. Either way, if you're not sure what your letter is asking, start with our overview of the general steps for any IRS letter.

Frequently Asked Questions

What is a CP14 notice? It is the IRS's first bill, telling you that you owe money on unpaid taxes and asking for payment within 21 days.

Is a CP14 notice bad? It is serious but routine and fixable. It is not an audit, and acting on it promptly keeps interest and penalties from growing.

How do I respond to a CP14 notice? Verify the balance against your records, then pay it, set up a payment plan if you can't pay in full, or dispute it in writing if the amount is wrong.

Is notice CP14 a civil penalty? No. The CP14 is a demand for payment of tax you owe, though the balance can include penalties and interest in addition to the tax.

What if I paid my taxes but received a CP14? Don't pay twice. Check your IRS account to confirm the payment posted, and if you paid in full and on time, the IRS has said affected taxpayers should not respond while it corrects the account.

A CP14 notice is the IRS letting you know about a balance and asking you to settle it, not a penalty or an audit. Confirm the amount is right, pay it or arrange a plan if it is, and dispute it with proof if it isn't. Dealt with inside the window it gives you, a CP14 is one of the simpler IRS notices to put behind you.