%201.avif)

.png)

.png)

IRS Fresh Start Program (2026): What It Is, Who Qualifies, And How To Apply

The IRS Fresh Start Program is a set of relief options the IRS introduced in 2011 to help people pay off back taxes they cannot afford, through payment plans, settlements, lien relief, and penalty relief. It is not a single application, and it is not automatic tax forgiveness.

If you owe the IRS more than you can pay, the Fresh Start Program is usually where a realistic resolution begins. Below, we explain what the program actually is in 2026, whether it is legitimate, how each relief option works, who qualifies, what it costs, and how to apply, with the real numbers behind the "settle for pennies" claims you have probably heard on the radio.

What Is The IRS Fresh Start Program?

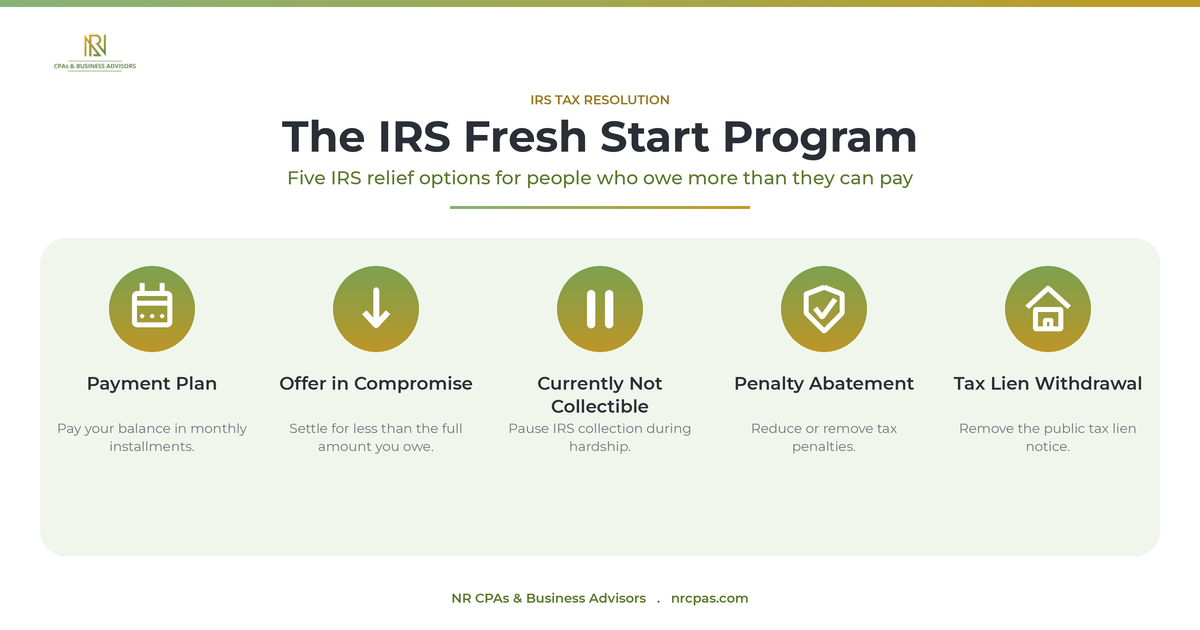

The IRS Fresh Start Program is a group of collection-relief policies, not one form you fill out. According to the IRS, it launched the program in 2011 and expanded it in the years since, easing the rules around payment plans, federal tax liens, and settlements so that more taxpayers could resolve their balances and avoid aggressive collection. When people say "the Fresh Start Program," they are really pointing to five tools the IRS already administers: installment agreements, the Offer in Compromise, Currently Not Collectible status, penalty abatement, and tax lien withdrawal.

Because it is an umbrella of options rather than a standalone benefit, you do not "sign up" for Fresh Start. You qualify for one or more of its relief programs based on what you owe and what you can pay. That distinction matters, and it is the first thing the marketing tends to blur.

Is The Fresh Start Program The Same As The Fresh Start Initiative?

Yes. The "Fresh Start Program" and the "Fresh Start Initiative" are the same thing, just different names for the 2011 IRS changes and the relief options they expanded.

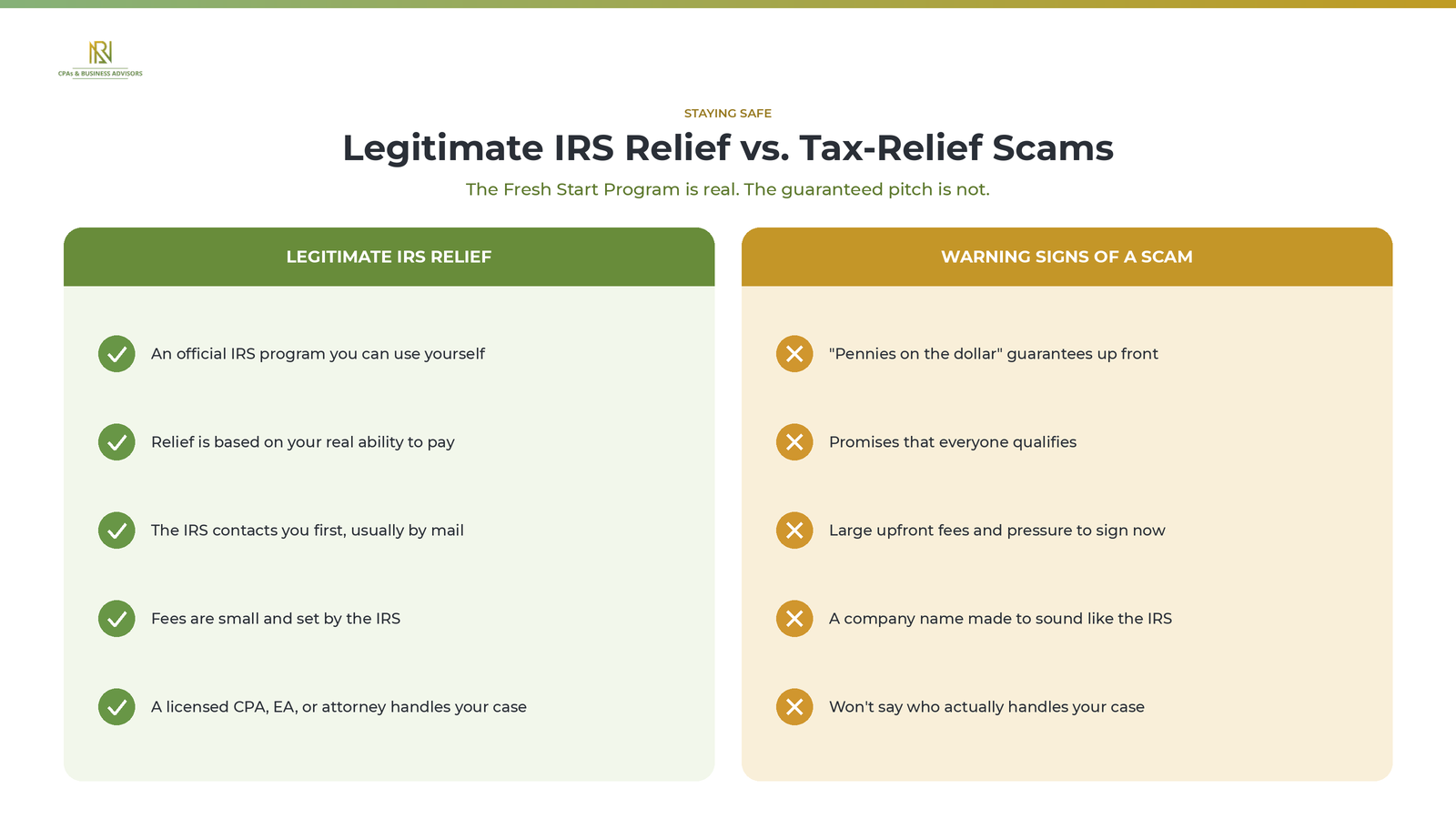

Is The IRS Fresh Start Program Legitimate?

Yes, the IRS Fresh Start Program is legitimate. It is a real set of IRS policies, administered directly by the IRS, and you can use every part of it yourself at no cost beyond the IRS's own fees. The skepticism is understandable, though, because the program's name has been borrowed by an entire advertising industry.

Why Do People Think The Fresh Start Program Is A Scam?

People doubt the program because tax-relief companies repackage it. A radio or late-night ad promises to wipe out your debt for "pennies on the dollar" through a "new IRS Fresh Start program," then routes you to a toll-free number. The underlying programs are genuine; the guaranteed, everyone-qualifies pitch is not. The IRS settles a debt only when the amount offered is the most it can realistically collect, not because a company "negotiated hard."

Is The "Fresh Start" Phone Call A Scam?

An unsolicited call or text promising Fresh Start "approval" before anyone has reviewed your finances is a red flag. According to the IRS, it initiates most contact about a balance by mail, not with a surprise phone call, and it does not pre-approve settlements over the phone. A legitimate firm will examine your filing history, income, and assets before telling you what you qualify for. Treat any caller who guarantees a result, demands a large upfront fee, or pressures you to decide immediately as a warning sign, not an opportunity.

Is The Fresh Start Program Tax Forgiveness?

No. The Fresh Start Program is not blanket tax forgiveness. People often search for "tax forgiveness," but the IRS does not erase what you owe simply because you ask. Fresh Start can reduce a balance through a settlement, pause collection during hardship, remove certain penalties, and make a balance payable over time, but it does so only when your finances justify it. Think of it as structured relief, not a clean slate.

How Does The IRS Fresh Start Program Work?

The Fresh Start Program works by giving you access to several IRS relief options, and the one you use depends on your ability to pay. The five core options are:

- A payment plan, or installment agreement, lets you pay the full balance over time in monthly amounts.

- An Offer in Compromise lets you settle for less than the full amount when you cannot pay it.

- Currently Not Collectible status pauses IRS collection when paying anything would create hardship.

- Penalty abatement reduces or removes certain penalties.

- Tax lien withdrawal removes the public Notice of Federal Tax Lien once you qualify.

Payment Plans (Installment Agreements)

A payment plan, or installment agreement, lets you pay your balance over time instead of all at once, and it is the option most taxpayers use. The IRS replaced its older Streamlined Installment Agreement with the Simple Payment Plan for individuals in 2025, and for businesses in 2026. According to the IRS, if you owe $50,000 or less in combined tax, penalties, and interest and have filed all required returns, you can generally set one up online without submitting any financial disclosures, with the balance paid off by the time the collection period expires. The IRS requires direct debit for balances between $25,000 and $50,000, and interest and the late-payment penalty continue until the debt is paid. You apply online or by filing Form 9465.

Offer In Compromise (OIC)

An Offer in Compromise lets you settle your tax debt for less than the full amount, but only when repaying it in full would be impossible or create real hardship. The IRS weighs your income, allowable living expenses, and the equity in your assets to calculate your Reasonable Collection Potential, essentially the most it believes it can collect, and it will not accept less than that figure. The IRS requires Form 656 and a financial statement on Form 433-A (OIC), a $205 application fee (waived for low-income applicants), and an initial payment of 20% for a lump-sum offer. Settlements are real but far from automatic: according to the IRS Data Book, the IRS received 33,591 offers in fiscal year 2024 and accepted 7,199, about 21%, against a roughly 37% acceptance rate across the prior decade. A complete, honest financial picture is what moves an offer from rejected to accepted.

Currently Not Collectible (CNC) Status

Currently Not Collectible status pauses IRS collection when paying anything toward your balance would keep you from covering basic living expenses. It does not erase the debt. Interest and penalties keep accruing, and the IRS can review your situation again later, but while the status is in place, the IRS stops levies and garnishments. You demonstrate the hardship with a financial statement on Form 433-F or 433-A.

Penalty Abatement

Penalty abatement reduces or removes the penalties stacked on top of your tax, and it is free to request. According to the IRS, First-Time Abatement is available if you have a clean compliance record for the prior three years, have filed all required returns, and have paid or arranged to pay the tax due. Reasonable-cause relief applies when something genuinely outside your control, such as a serious illness, a natural disaster, or a death in the family, kept you from filing or paying on time. You can request abatement by phone, in writing, or on Form 843.

Tax Lien Withdrawal

Tax lien withdrawal removes the public Notice of Federal Tax Lien so it no longer appears as if it had ever been filed, which helps your credit and your ability to refinance or sell property. Under the Fresh Start changes, the IRS lets you request withdrawal once you owe $25,000 or less (or pay the balance down to that amount), enter a Direct Debit Installment Agreement that fully pays the debt within 60 months or before the collection deadline, make three consecutive direct-debit payments, and stay current on all other filings. You request it on Form 12277. A withdrawal does not wipe out the balance. Interest and penalties continue until you pay in full.

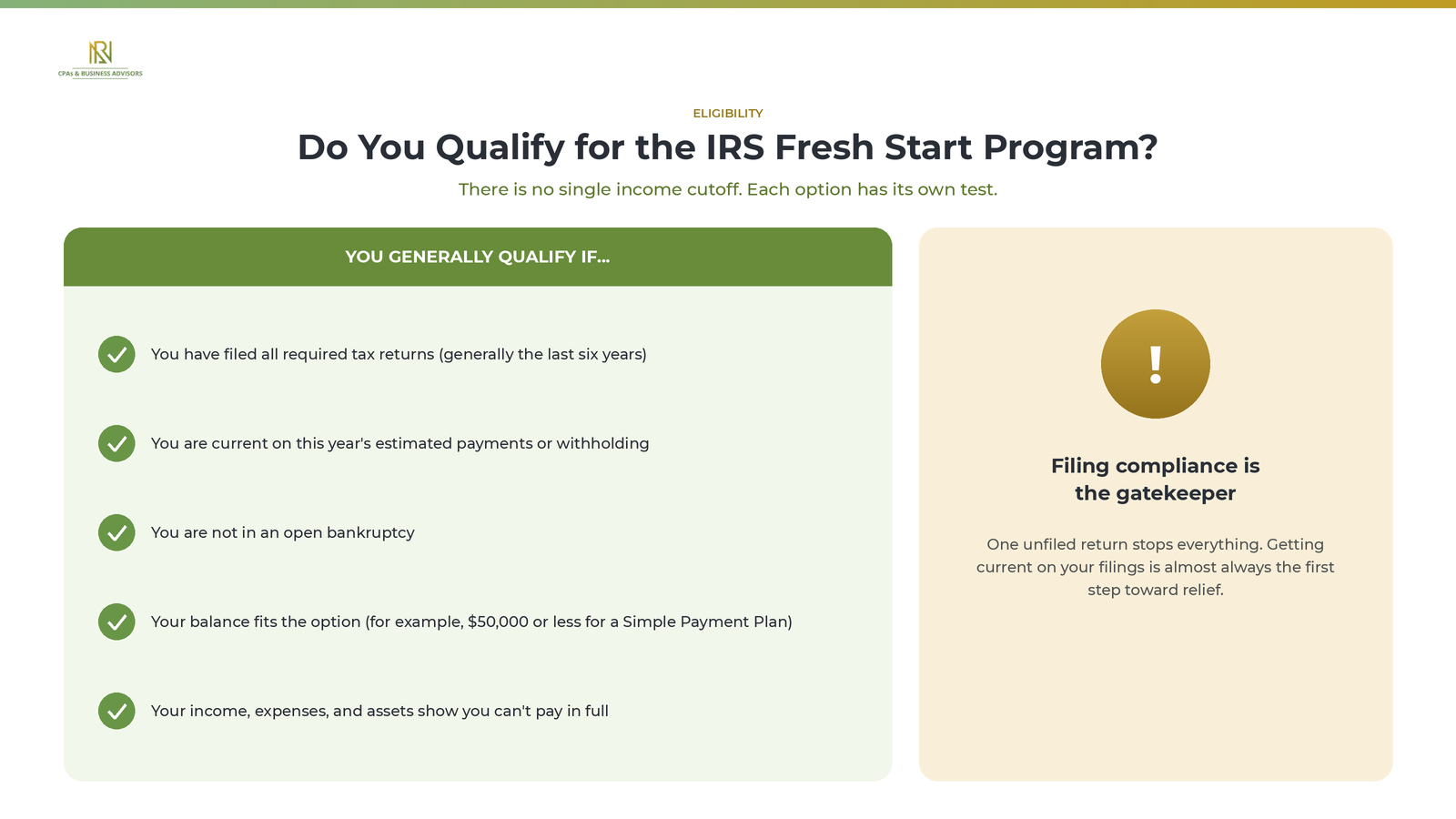

Who Qualifies For The IRS Fresh Start Program?

You qualify for the Fresh Start Program if you are current on all your required tax filings and can show the IRS you cannot comfortably pay your full balance. There is no single application and no single income cutoff; each relief option has its own test. Across all of them, the IRS generally expects you to meet these conditions:

- You have filed all legally required tax returns, generally the past six years.

- You are current on this year's obligations, such as estimated payments or paycheck withholding.

- You are not in an open bankruptcy proceeding.

- Your balance fits the option you want (for example, $50,000 or less for a Simple Payment Plan).

- For a settlement or a collection pause, your income, expenses, and assets show you cannot pay in full.

Filing compliance is the gatekeeper. If even one required return is unfiled, the IRS will not consider you for any Fresh Start relief until you catch up, which is why getting current is almost always the first step.

Income And Asset Limits

The Fresh Start Program has no fixed income limit. What matters is your ability to pay, which the IRS measures by comparing your income against allowable living expenses and the equity in your assets. Two people with the same income can get very different answers: someone with significant home or retirement equity may not qualify for a settlement even on a modest salary, because that equity counts toward what the IRS believes it can collect.

Fresh Start For The Self-Employed And Small Businesses

Self-employed taxpayers and small-business owners can use Fresh Start, with a few extra wrinkles. The IRS expects you to be current on estimated tax payments and, for a business, on payroll tax deposits before it will approve relief, and it distinguishes between your personal liability and the business's. If your self-employment income has dropped sharply, that decline is exactly the kind of hardship that can support a payment plan, a settlement, or penalty relief, provided your filings are current.

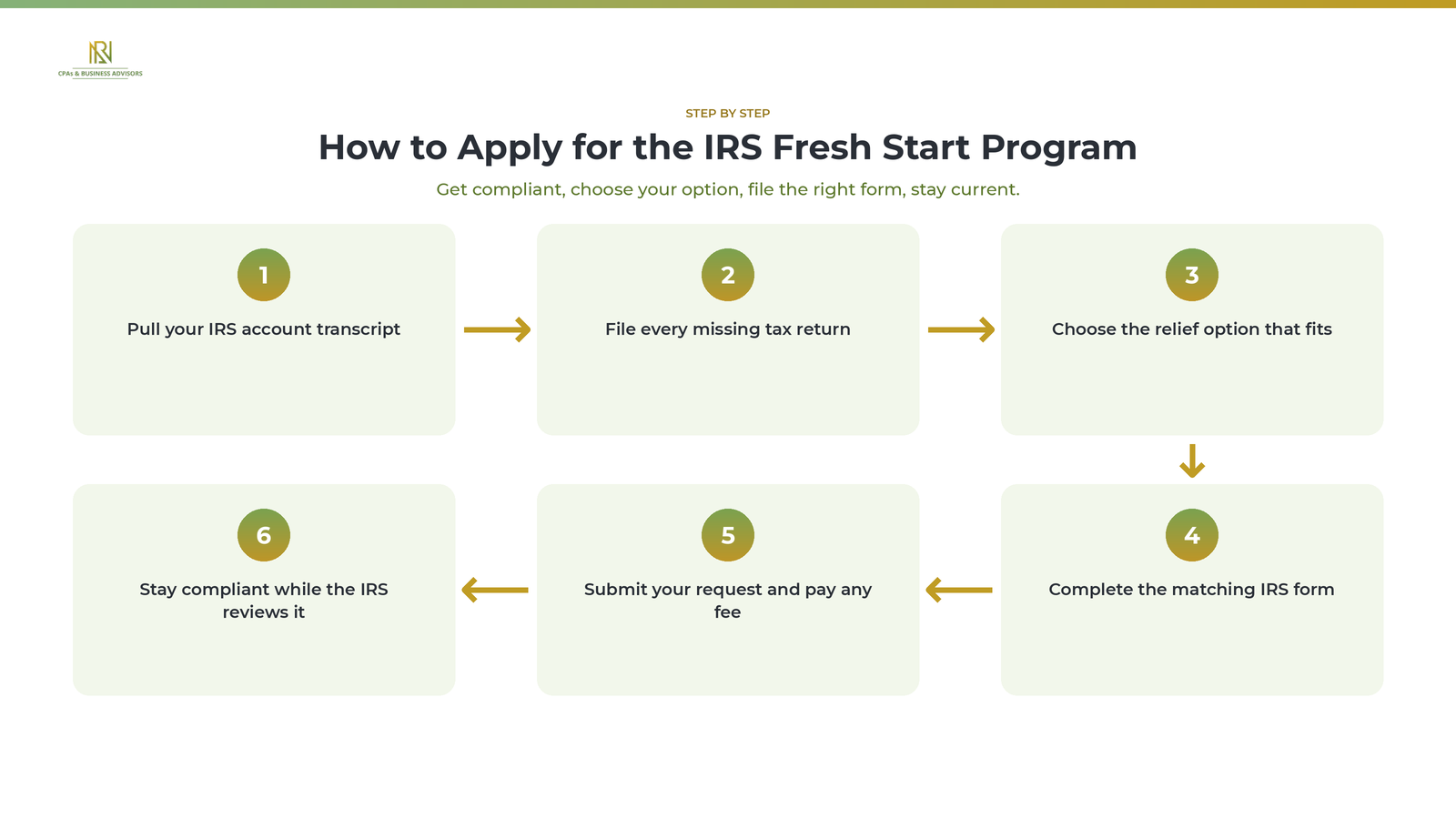

How Do You Apply For The IRS Fresh Start Program?

To apply for the Fresh Start Program, you get into filing compliance first, choose the relief option that fits your situation, file the matching form, and stay current while the IRS reviews it. The steps are:

- Pull your IRS account transcript so you know exactly what you owe and for which years.

- File every missing return. This is non-negotiable, and the IRS will reject your request without it.

- Choose the right option: a payment plan if you can pay over time, an Offer in Compromise or Currently Not Collectible status if you cannot, penalty abatement if penalties are the problem.

- Complete the correct form for that option (see below).

- Submit your request and pay any required fee or initial payment.

- Stay compliant during review: file and pay on time, and respond promptly to any IRS notice.

What Forms Do You Need?

The form depends on the relief option you are pursuing. You can download each directly from the IRS:

- Payment plan: Form 9465

- Offer in Compromise: Form 656 with Form 433-A (OIC)

- Penalty abatement: Form 843

- Tax lien withdrawal: Form 12277

- Currently Not Collectible: a financial statement on Form 433-F or 433-A

What Documentation Do I Need For Fresh Start?

For any option based on hardship or settlement, you will need documentation that backs up your financial picture: recent pay stubs or proof of income, bank statements, a list of monthly living expenses, and details of your assets and debts. For reasonable-cause penalty relief, add records that show what prevented you from filing or paying, such as medical records, an insurance claim, or similar proof.

How Much Does The IRS Fresh Start Program Cost?

The Fresh Start Program itself has no cost, but individual options carry IRS fees. According to the IRS, penalty abatement is free to request, an Offer in Compromise has a $205 application fee that is waived for low-income applicants, and a payment plan carries a setup fee that is lower when you apply online and pay by direct debit, and reduced or waived for low-income taxpayers. On top of the IRS's fees, you may choose to pay a tax professional to prepare and represent your case, which is a separate, optional cost. Note that "how much does Fresh Start cost" is a different question from "how much do I owe": the program does not change your underlying balance unless you qualify for a settlement.

Is The IRS Fresh Start Program Still Available In 2026?

Yes. The Fresh Start Program is still available in 2026, and the underlying relief options remain in place. The main recent change is administrative: in 2025 the IRS replaced the Streamlined Installment Agreement with the more flexible Simple Payment Plan for individuals, extending it to businesses in 2026, and it continues to use a higher dollar threshold before it files a lien than it did before 2011 (commonly cited around $10,000, up from $5,000). The program is not going away.

Is There A Fresh Start Program Deadline?

There is no single Fresh Start application deadline. You can pursue relief at any time. That said, timing still matters: according to the IRS, it generally has ten years from the date a tax is assessed to collect it, and penalties and interest keep growing until the balance is resolved, so acting sooner usually means lower costs and more options, especially before the IRS files a lien or starts levying.

What About The IRS "7-Year Rule," "3-Year Rule," Or "One-Time Forgiveness"?

There is no IRS program called the "7-year rule," the "3-year rule," or "one-time forgiveness," despite how often those phrases appear online. They usually describe something real under a misleading label. The "10-year rule" people sometimes mean is the collection statute, the roughly ten years the IRS has to collect. "One-time forgiveness" generally refers to First-Time Penalty Abatement, which removes penalties (not tax) for taxpayers with a clean recent record. And the idea of "settling for pennies" describes the Offer in Compromise, with the strict ability-to-pay test covered above. The relief is real; the catchy rule names are not.

Should You Apply Yourself Or Hire A Tax Professional?

You can apply for the Fresh Start Program yourself, and many people do, especially for a straightforward payment plan or a first-time penalty request, both of which the IRS designed to be self-service. Professional help earns its cost when the situation is more complex: a large balance, years of unfiled returns, an Offer in Compromise, or a case where the IRS has already filed a lien or begun garnishing wages. In those situations, a firm offering IRS tax resolution services can confirm what you actually qualify for, prepare the financial analysis correctly, and deal with the IRS on your behalf. In our experience, the cases that succeed are usually the ones that start with getting every return filed before anything is submitted.

How To Avoid Tax-Relief Scams

If you do hire help, the warning signs of a tax-relief mill are consistent. Be cautious of any company that:

- Guarantees it can settle your debt for "pennies on the dollar" before reviewing your finances.

- Promises that everyone qualifies for an Offer in Compromise.

- Demands a large upfront fee or pressures you to sign on the first call.

- Uses a name engineered to sound like the IRS or a government agency.

- Will not tell you whether a licensed CPA, Enrolled Agent, or tax attorney will actually handle your case.

Frequently Asked Questions

How much will the IRS usually settle for? There is no set percentage; according to the IRS, it accepts an offer equal to your Reasonable Collection Potential, which is what it calculates it could collect from your income and assets before the debt expires.

Will the IRS stop collections during Fresh Start? Yes. Once you are approved for a payment plan, an Offer in Compromise, or Currently Not Collectible status, the IRS generally pauses levies and wage garnishments.

Does applying for Fresh Start hurt your credit? Applying does not affect your credit, and the IRS no longer reports tax debt to credit bureaus; removing a lien notice through withdrawal can actually help.

What if I can't pay my back taxes at all? If paying anything would prevent you from covering basic living expenses, you may qualify for Currently Not Collectible status or an Offer in Compromise based on hardship.

Does the Fresh Start Program expire? The program is not scheduled to end, but each individual tax debt has its own roughly ten-year collection window, so the practical clock is the collection statute, not the program.

The IRS Fresh Start Program is a legitimate, still-active set of relief options (payment plans, settlements, hardship status, penalty relief, and lien withdrawal) for people who owe more than they can pay. It is not instant forgiveness, and the honest path runs through filing compliance and a clear-eyed look at what you can actually pay. Done right, it is the difference between an unmanageable balance and a resolved one.

.avif)

.avif)

Tax and Financial Insights

by NR CPAs & Business Advisors

Federal Tax Lien: How To Remove Or Withdraw It

A federal tax lien is the government's legal claim against your property when you fail to pay a tax debt after the IRS has assessed the amount owed and sent you a bill. According to the IRS, the lien attaches to all of your property, including real estate, vehicles, financial accounts, and business assets, as well as any property you acquire in the future while the lien is active. The lien protects the government's interest by establishing its priority over other creditors.

A federal tax lien is created automatically by law once three conditions are met: the IRS assesses the tax, sends you a Notice and Demand for Payment, and you neglect or refuse to pay the balance in time. According to the IRS, the agency then files a public document called a Notice of Federal Tax Lien (NFTL) with your state or county recording office to alert other creditors that the government has a legal right to your property. The lien itself exists from the moment you fail to pay, but the public notice is what damages your credit and affects your ability to sell or borrow against your assets.

How A Federal Tax Lien Affects You

A federal tax lien can significantly impact your finances, credit, and ability to conduct business. According to the IRS, the effects include the following.

- Credit damage. Once the Notice of Federal Tax Lien is filed, it becomes a public record. Lenders, landlords, and creditors can see it, and it can lower your ability to obtain credit, loans, or mortgages.

- Property restrictions. The lien attaches to all your current and future assets. You cannot sell or refinance real estate without satisfying or addressing the lien first.

- Business impact. The lien attaches to business property and accounts receivable, which can interfere with operations and relationships with vendors and clients.

- Bankruptcy limitations. According to the IRS, a tax lien and the Notice of Federal Tax Lien may continue even after bankruptcy in certain situations.

How To Remove A Federal Tax Lien

The IRS provides four methods for removing or reducing the impact of a federal tax lien: paying the debt in full, requesting a discharge, requesting subordination, and requesting a withdrawal.

Pay The Debt In Full

Paying your tax debt in full is the most direct way to eliminate a federal tax lien. According to the IRS, the agency releases the lien within 30 days after the balance, including penalties and interest, is paid in full. If you cannot pay the entire amount at once, an installment agreement allows you to pay over time, and the lien is released once the final payment is made.

Discharge Of Property

A discharge removes the lien from a specific piece of property, allowing you to sell or transfer it. According to the IRS, a discharge may be granted if the remaining property still subject to the lien is worth at least double the total tax liability plus all other encumbrances, or if the IRS receives payment equal to the government's interest in the property being discharged. This option is commonly used to facilitate real estate sales when the lien amount exceeds the property value.

Subordination

Subordination does not remove the lien but allows other creditors to move ahead of the IRS in priority. According to the IRS, this can make it easier to obtain a mortgage or loan because the lending institution's lien takes priority over the government's claim. The IRS may approve subordination if it determines that doing so will ultimately increase the total amount collected.

Withdrawal

A withdrawal removes the public Notice of Federal Tax Lien from the record, though you remain liable for the underlying debt. According to the IRS, a withdrawal may be granted if the agency filed the notice prematurely or not in accordance with its procedures, if you have entered into a Direct Debit installment agreement, or if the withdrawal would facilitate collection. Under the IRS Fresh Start program, taxpayers who owe $25,000 or less and have a Direct Debit installment agreement may request withdrawal of the NFTL after making three consecutive payments.

Federal Tax Lien vs Levy

A lien and a levy are two different IRS actions, and understanding the distinction is important. According to the IRS, a lien is a legal claim that secures the government's interest in your property. It does not take your property. A levy, by contrast, actually seizes your property to satisfy the tax debt. Levies can target wages, bank accounts, Social Security benefits, vehicles, and real estate.

The IRS typically files a lien first and proceeds to a levy only after sending multiple collection notices and a Final Notice of Intent to Levy. Addressing the lien early through payment, a resolution agreement, or one of the removal options above can prevent the situation from escalating to a levy.

How To Prevent A Federal Tax Lien

The simplest way to prevent a federal tax lien is to file your tax returns on time and pay the full amount owed. If you cannot pay in full, acting before the IRS files a lien gives you the most options. According to the IRS, setting up a payment plan before a lien is filed can prevent the public notice from being recorded. Taxpayers who owe $50,000 or less can apply for a streamlined installment agreement online, and those who qualify for the IRS Fresh Start program benefit from higher thresholds before the IRS will file a lien.

If you already owe the IRS and are unsure which resolution path to pursue, the full range of IRS resolution options includes installment agreements, Offers in Compromise, Currently Not Collectible status, and penalty relief.

Frequently Asked Questions About Federal Tax Liens

How Long Does A Federal Tax Lien Last?

A federal tax lien generally lasts until the underlying tax debt is paid in full or the 10-year Collection Statute Expiration Date (CSED) passes. According to the IRS, the NFTL will self-release 30 days after the 10-year collection period expires if the IRS does not refile it. However, certain actions such as installment agreements, Offers in Compromise, and bankruptcy can suspend or extend the CSED.

Can A Federal Tax Lien Be Filed Without Warning?

The IRS must send you a Notice and Demand for Payment before a lien can arise, and must notify you within five business days after filing the Notice of Federal Tax Lien. According to the IRS, you have the right to request a Collection Due Process (CDP) hearing to challenge the filing.

Does A Federal Tax Lien Show Up On My Credit Report?

The major credit bureaus no longer include tax liens on standard credit reports, but the Notice of Federal Tax Lien remains a public record. Lenders who search public records during the mortgage or loan approval process will still find it, and it can affect your ability to obtain financing.

IRS Innocent Spouse Relief: When You're Not Liable

Innocent spouse relief is an IRS program that can remove your responsibility for paying additional taxes, penalties, and interest when your spouse or former spouse understated the taxes owed on a joint return without your knowledge. According to the IRS, when you file a joint tax return, both spouses are jointly and severally liable for the full tax amount, which means the IRS can collect the entire balance from either spouse, even after a divorce. Innocent spouse relief is an exception to that rule for spouses who did not know about or benefit from the errors on the return.

According to the IRS, innocent spouse relief applies only to taxes due on your spouse's income from employment or self-employment. It does not cover taxes on your own income, household employment taxes, business taxes, or trust fund recovery penalties. The relief is available whether you are still married, separated, or divorced.

The Three Types Of Innocent Spouse Relief

The IRS evaluates three forms of relief when you file a request, and you do not need to specify which type applies to your situation because the IRS will automatically consider all three.

Innocent Spouse Relief

This is the primary form of relief, available when your joint return understated the tax due because of errors attributable to your spouse, and you did not know or have reason to know about those errors. According to the IRS, errors that qualify include unreported income, incorrect deductions or credits, and incorrect asset values. The IRS considers whether a reasonable person in your circumstances would have known about the errors and whether you received any financial benefit from the understated income.

Separation Of Liability Relief

This form of relief divides the understated tax, penalties, and interest between you and your spouse based on each person's share of the errors. According to the IRS, you are generally eligible if you are divorced, legally separated, or have not lived with your spouse for at least 12 months before filing the request. You must also demonstrate that you did not know about the errors when you signed the return.

Equitable Relief

If you do not qualify for innocent spouse relief or separation of liability, the IRS may grant equitable relief if holding you responsible for the tax debt would be unfair given all the facts and circumstances. According to the IRS, equitable relief considers factors including your current marital status, whether you suffered economic hardship, whether you knew or had reason to know about the understated tax, and whether you were a victim of domestic abuse that affected your ability to challenge the return.

Who Qualifies For Innocent Spouse Relief

To be eligible, you must have filed a joint return that understated the tax due because of errors attributable to your spouse, and you must not have known or had reason to know about those errors when you signed the return. According to the IRS, you are not eligible in any year where you signed an Offer in Compromise with the IRS, signed a closing agreement covering the same taxes, or a court has already issued a final decision denying you relief.

Victims of domestic abuse receive a special exception. According to the IRS, you may still qualify for relief even if you had some knowledge of the errors if you signed the return because of spousal abuse, threats, or coercion and were afraid to challenge the items on the return.

The IRS approval rate for innocent spouse relief is relatively low. According to Jackson Hewitt, the IRS received over 26,000 requests in a recent year and fully approved fewer than 5,000. The fact-based, case-by-case nature of the evaluation means that the strength of your documentation and the clarity of your explanation are critical to the outcome.

How To Apply For Innocent Spouse Relief

To request relief, file Form 8857, Request for Innocent Spouse Relief, with the IRS. According to the IRS, Form 8857 covers all three types of relief (innocent spouse, separation of liability, and equitable), so you do not need to determine which type fits your situation. The IRS will evaluate your information and apply the appropriate form of relief if you qualify.

Form 8857 is a seven-page form that requires detailed information about your tax situation, your relationship with your spouse, your knowledge of the return's contents, and your financial circumstances. You should include supporting documentation such as divorce decrees, court orders, financial records, and any correspondence that demonstrates you did not know about the errors. According to the IRS, you must file the request within two years of receiving an IRS notice of an audit or additional taxes due because of an error on your return.

While your request is being reviewed, continue to file your tax returns and pay any taxes you owe. If you received an IRS notice about a balance and cannot pay while the review is pending, you may be able to set up an installment agreement to manage the amount in the meantime.

Innocent Spouse vs Injured Spouse

Innocent spouse relief and injured spouse relief are two separate IRS programs that address different problems. They are frequently confused because of their similar names, but they apply in entirely different situations.

- Innocent spouse relief removes your liability for tax debt caused by your spouse's errors or omissions on a joint return. It addresses the underlying tax, penalties, and interest.

- Injured spouse relief protects your share of a joint tax refund from being applied to your spouse's past-due debts such as student loans, child support, or state taxes. It does not address tax liability at all. You request injured spouse relief by filing Form 8379.

If you owe the IRS because of your spouse's errors, you need innocent spouse relief (Form 8857). If your refund was taken to pay your spouse's separate debts, you need injured spouse relief (Form 8379).

What Happens After You Apply

After you submit Form 8857, the IRS will notify your current or former spouse that you filed a request, which allows them to participate in the review process. According to the IRS, the review can take six months or longer. When the review is complete, the IRS sends a letter of determination with its decision. If approved, the IRS removes your responsibility for the additional tax, penalties, and interest attributable to your spouse's actions.

If the IRS denies your request, both spouses have the right to appeal within 30 days of the determination letter. You can file Form 12509, Statement of Disagreement, and request a review by the IRS Independent Office of Appeals. If you cannot reach agreement through Appeals, you can petition the U.S. Tax Court. Taxpayers exploring other ways to resolve joint tax debt beyond innocent spouse relief can review the full range of IRS resolution options available for balances you cannot pay.

Frequently Asked Questions

Do I Have To Be Divorced To Qualify?

No, you do not have to be divorced to qualify for innocent spouse relief. According to the IRS, the relief is available whether you are married, separated, or divorced. However, separation of liability relief specifically requires that you are divorced, legally separated, or have not lived with your spouse for at least 12 months.

Will My Spouse Be Notified?

Yes, the IRS is required to notify your current or former spouse when you file Form 8857. According to the IRS, the other spouse has the right to participate in the review process and can appeal the decision if relief is granted.

What If I Knew About Some But Not All Of The Errors?

The IRS evaluates each item on the return separately, so you may receive partial relief for items you did not know about while remaining liable for items you were aware of. According to the IRS, the determination depends on whether a reasonable person in your situation would have known about each specific error.